Goldman Sachs tracked more than 20,000 American workers across four decades of federal employment data and found that being displaced by technology produces measurably worse financial outcomes than any other form of job loss. The gap does not close for ten years. Published on 24 April 2026, the study lands at precisely the moment AI displacement has shifted from theoretical risk to visible labour market drag, with AI now reducing U.S. monthly payroll growth by 16,000 jobs and Goldman’s own economists flagging 2026 as the year these effects show up in the data. What follows is an analysis of what the Goldman findings actually quantify, why the financial consequences for technologically displaced workers are structurally worse than other displacement, which workers and sectors face the greatest exposure, and what the research signals for investors watching labour-intensive industries.

Technology displacement carries a financial penalty that other job losses do not

Not all job loss is equal. That is the finding Goldman’s data makes hardest to ignore. Workers displaced from technology-affected industries face a 3% larger real earnings loss upon re-employment compared to non-displaced peers, a gap that workers displaced from other sectors do not experience to any meaningful degree.

Re-employment, however, does not reset the clock. Over the following decade, technologically displaced workers accumulate 10 percentage points less earnings growth than workers who were never displaced, and 5 percentage points less than peers who lost jobs in non-technology-affected industries. They also take approximately one additional month to secure new employment compared to other displaced workers.

Technologically displaced workers accumulate 10 percentage points less earnings growth over a decade than never-displaced peers, a gap that persists regardless of re-employment timing.

The study draws on subjects born between the 1950s and 1980s, spanning four decades of labour market data. The sample size, more than 20,000 U.S. workers, gives the findings statistical weight that smaller displacement studies have lacked.

| Worker Type | Re-employment Wage Impact | 10-Year Earnings Growth Gap | Average Time to Re-employment |

|---|---|---|---|

| Never displaced | Baseline (no loss) | Baseline | N/A |

| Displaced from other sectors | Negligible earnings impact | 5 pp better than tech-displaced | Baseline for displaced cohort |

| Displaced from technology-affected sectors | 3% larger real earnings loss | 10 pp below never-displaced; 5 pp below other displaced | ~1 additional month |

For investors, these figures provide the empirical baseline for assessing the structural earnings headwinds facing workers in high-exposure sectors, and by extension, the consumer spending power those sectors support.

When big ASX news breaks, our subscribers know first

Why earnings gaps persist: the role of occupational shifts and skill erosion

The earnings gap persists because of what Goldman identifies as occupational downgrading: displaced workers shift into routine roles requiring fewer analytical and interpersonal skills than their previous positions. This is not a one-time step down. It is a compounding process. The longer a worker occupies a downgraded role, the further their original skill set drifts from market value. Employers stop seeing them as candidates for the work they once did.

Roles vulnerable to downgrading share specific characteristics:

- High proportion of routine, repeatable tasks

- Limited requirement for interpersonal or contextual judgement

- Significant overlap between task composition and current AI capabilities

The distinction matters for forecasting. The wage gap does not close because workers in downgraded roles are not rebuilding the skills that would restore their earnings trajectory. They are maintaining a lower baseline while their former occupation evolves without them.

NBER research on AI-induced displacement corroborates the scarring mechanism Goldman identifies, finding that long-term earnings losses from technology-driven job loss can persist for more than a decade and distribute unevenly across worker cohorts depending on occupational mobility and educational attainment.

From telephone operators to content creators: the pattern repeats

Goldman cites telephone operators and typists as historical precedents, occupations where automation eliminated the role, workers shifted into lower-skill positions, and the decade-long earnings gap followed. The pattern is documented, not speculative.

Goldman economist Briggs has characterised 2026 as the “big story” year for AI labour effects in knowledge and content sectors, positioning current AI-exposed workers, particularly those in entry-level content creation, as the contemporary equivalent of those earlier displaced cohorts. The mechanism is the same: role automated, worker downgraded, earnings trajectory permanently altered.

What the numbers actually mean for workers facing displacement today

A 10-percentage-point earnings growth gap over a decade is not an abstraction. It translates into slower wealth accumulation, delayed homeownership, and reduced retirement savings compounding across the most productive earning years. According to Business Insider’s April 2026 coverage, these scarring effects extend well beyond wages into broader household financial outcomes, with the damage intensifying during economic downturns.

Consumer spending pressure is already visible in the macro data, with the U.S. personal savings rate at 4.0% in early 2026 indicating that household expenditure is increasingly funded by savings drawdowns rather than income growth, a dynamic that compounds the long-run demand headwind Goldman’s displacement research implies for affected cohorts.

The Goldman findings also reveal that displacement risk is not uniformly distributed. According to Fortune’s April 2026 reporting on the research by Pierfrancesco Mei and Jessica Rindels, younger, college-educated urban workers experience roughly half the earnings loss of the overall displaced population, a difference attributed to greater occupational mobility. The corollary is equally clear: workers with limited geographic, educational, or industry mobility face disproportionate harm.

Recession timing acts as a force multiplier. Three factors amplify displacement outcomes:

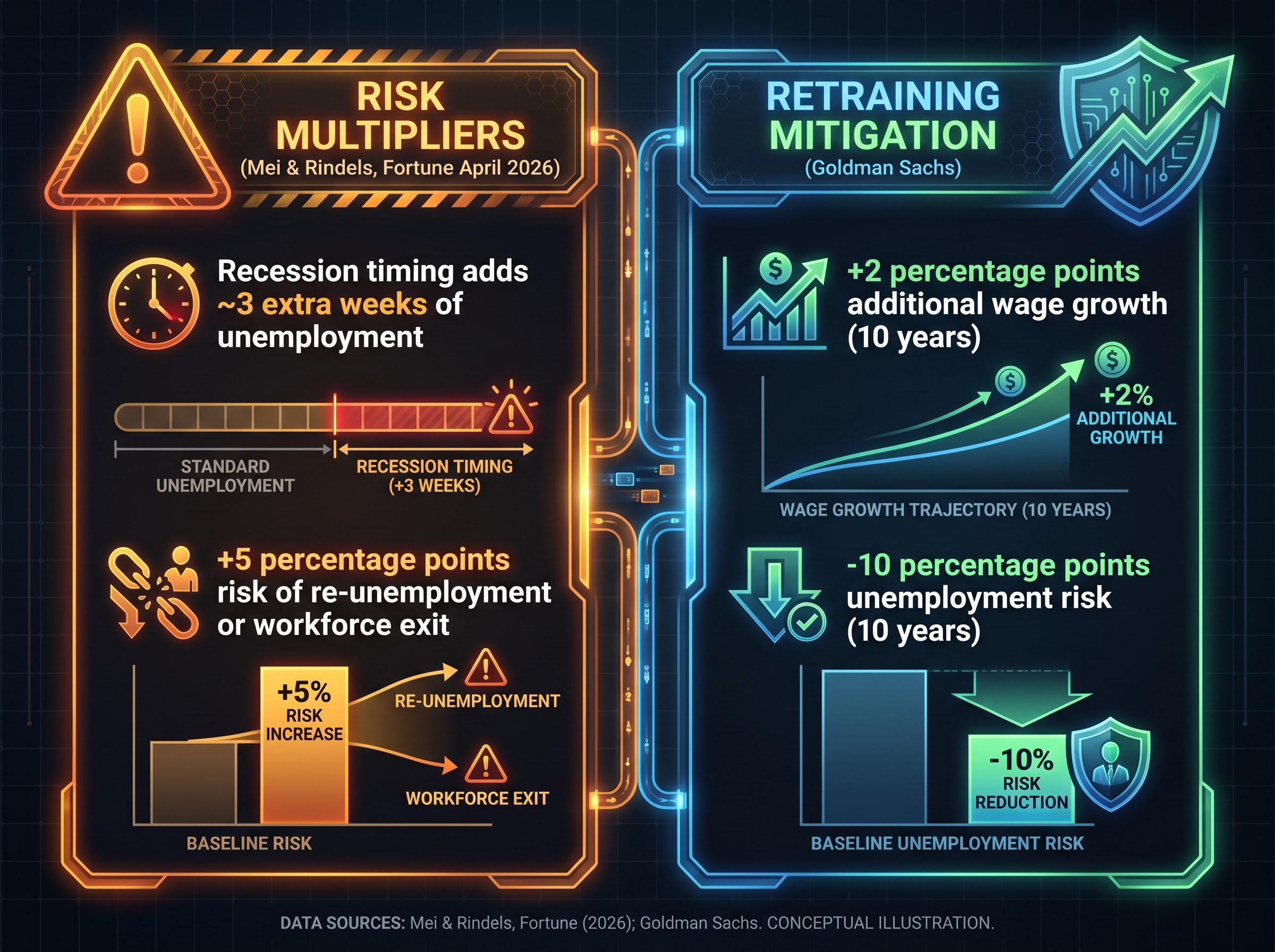

- Recession timing: Displacement during a downturn adds approximately 3 extra weeks of unemployment, according to Mei and Rindels

- Limited occupational mobility: Workers without transferable skills or credentials face longer recovery periods and steeper downgrading

- Geographic concentration: Regional labour markets dependent on a narrow set of industries offer fewer re-employment alternatives

Goldman economists Mei and Rindels found that recession-timed displacement raises the risk of re-unemployment or permanent labour force exit by 5 percentage points, a finding with direct implications for regional consumer credit risk.

These demographic and timing variables establish that AI displacement risk concentrates along existing structural fault lines. The workers most likely to be displaced are often the least equipped to recover from it.

How large is the actual exposure: unpacking the global estimates

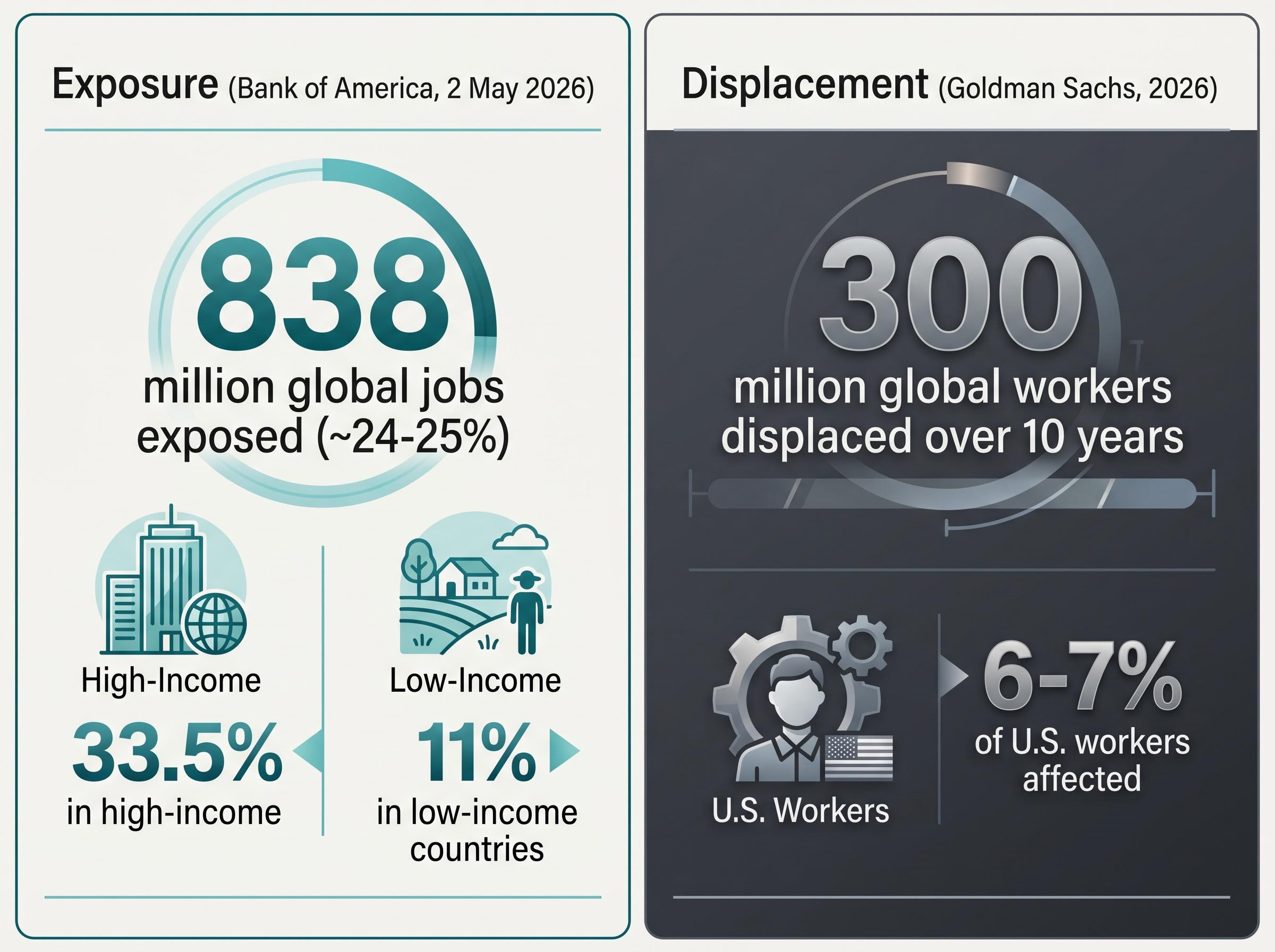

Two headline figures dominate the AI displacement conversation, and they are not measuring the same thing. Bank of America reported on 2 May 2026 that approximately 838 million jobs worldwide, roughly 24-25% of global employment, are exposed to generative AI. Separately, Goldman Sachs projects that 300 million workers globally face potential displacement over the next 10 years, with 6-7% of U.S. workers affected over that horizon.

The distinction is between exposure and displacement. Exposure measures how many jobs contain tasks that AI could perform. Displacement measures how many workers are projected to actually exit the workforce as a result. One is a capability assessment; the other is a labour market projection.

| Source | Figure | What It Measures | Time Horizon | Geographic Scope |

|---|---|---|---|---|

| Goldman Sachs (2026) | 300 million workers | Jobs exposed to potential displacement | 10 years | Global |

| Bank of America (May 2026) | 838 million jobs (~24-25%) | Jobs with tasks performable by AI | Not time-bound | Global |

The income-level disparity sharpens the picture further. Bank of America data shows 33.5% of jobs in high-income countries are exposed, versus 11% in low-income countries. Yet an ILO-World Bank paper published on 27 March 2026 found that developing countries may face AI disruption without capturing proportional productivity or wage benefits, an asymmetric risk that exposure figures alone do not convey.

Several factors intervene between exposure and actual job losses, as the ILO outlined in an April 2026 brief:

- Deployment pace and firm-level adoption decisions

- Labour market institutions and regulatory frameworks

- Policy responses and retraining infrastructure

- Worker and union bargaining capacity

Conflating these two metrics, treating 838 million exposed jobs as 838 million lost jobs, overstates the risk. Treating Goldman’s 300 million displacement projection as the ceiling understates it. Getting this distinction right is foundational to any sectoral or geographic investment thesis built on AI labour market assumptions.

Retraining as mitigation: what the evidence says and what it does not

Goldman’s data offers a genuine positive finding. Workers who retrain experience 2 percentage points of additional wage growth and a 10-percentage-point reduction in unemployment risk over 10 years. The effect is meaningful and statistically supported across the study’s four-decade dataset.

The evidence confirms and the gaps remain:

- Confirmed: Retraining is associated with measurable improvements in both wage trajectory and employment stability

- Confirmed: The mitigation effect persists across the full decade measured

- Unconfirmed: Whether any specific government-administered programme produces these outcomes

- Unconfirmed: Large-scale public retraining initiatives with verified implementation details, as of early May 2026

The policy gap: what is still unconfirmed

The U.S. Warner-Hawley AI Workforce Act has been discussed in general terms, but confirmed implementation details remain unavailable as of the current date. The ILO and EU Commission have been identified as forthcoming sources for verified policy programme announcements in mid-2026.

A structural tension sits beneath this gap. The demographic factors that Goldman’s research identifies as amplifying displacement harm, limited geographic mobility, lower educational attainment, narrow industry experience, are the same barriers that restrict access to effective retraining. The workers who need mitigation most are frequently the least positioned to reach it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The next major ASX story will hit our subscribers first

What this signals for sectors carrying the highest structural labour risk

Goldman’s displacement framework points to specific sectoral fault lines. Tech, knowledge, and creative sectors, particularly entry-level content creation roles, face the steepest structural earnings headwinds. The mechanism identified in the study, occupational downgrading in roles with high AI-substitution overlap, concentrates in precisely these areas.

The picture is not uniformly negative. AI buildout is simultaneously generating employment gains in complementary sectors:

The hardware and software divergence inside the technology sector in 2026, with semiconductor equipment up nearly 48% while software applications have fallen 23%, maps almost precisely onto the substitution-risk versus complementary-growth split that Goldman’s displacement framework describes at the occupational level.

- Substitution-risk sectors: Knowledge work, content creation, analytical and administrative roles where AI performs core tasks

- Complementary-growth sectors: Infrastructure development, data centre operations, power systems, and AI deployment support roles

Goldman’s net figure of 16,000 fewer monthly U.S. payroll jobs already reflects this partial offset. The drag is the residual after augmentation effects are subtracted.

Bank of America’s analysis suggests that companies at the AI frontier are likely to capture a disproportionate share of productivity gains, a dynamic that could widen the gap between firms adopting AI effectively and those absorbing the labour cost consequences without the offsetting efficiency.

Goldman’s own modelling suggests that if displacement accelerates beyond current projections, the resulting underperformance against labour market forecasts could prompt Federal Reserve rate cuts, a scenario with broad asset class implications across equities, fixed income, and currency markets.

For equity analysis, the dual signal warrants differentiated treatment. Sectors experiencing occupational downgrading face declining entry-level labour costs, which may provide near-term margin relief. Over the longer term, however, the same displacement compresses consumer spending power among the affected cohorts, creating a headwind that offsets the margin benefit. The Goldman study does not predict mass unemployment. It establishes that the workers displaced by this cycle face a financial trajectory measurably worse than other displacement, and that the structural conditions producing those historical outcomes are replicating now.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The decade-long reckoning that AI displacement data is only beginning to reveal

The Goldman study’s contribution is not a prediction of AI-driven mass job destruction. It is the empirical demonstration that technology displacement inflicts a distinct and persistent financial penalty, one that compounds through occupational downgrading rather than healing through re-employment, and that the current AI cycle is producing the structural conditions that generated those outcomes historically.

Three forward-looking implications emerge from this analysis. First, the exposure-displacement distinction matters: treating 838 million exposed jobs and 300 million displacement-risk workers as interchangeable figures misprices risk in both directions. Second, demographic and geographic mobility barriers determine which worker cohorts face the worst outcomes, concentrating harm along lines that are already visible in labour market data. Third, retraining evidence exists but the policy infrastructure to deliver it at scale remains unverified as of early May 2026.

The sectors most exposed to occupational downgrading are also the sectors where entry-level labour costs are declining structurally. That creates a dual signal: near-term margin improvement paired with long-run consumer spending contraction among displaced cohorts. Investors building equity theses around AI adoption would benefit from treating these as separate, and potentially opposing, forces rather than a single directional bet.

Investors wanting to stress-test the Federal Reserve rate-cut scenario against actual earnings data will find our full explainer on Q1 2026 earnings and AI monetisation covers the 27.1% blended EPS growth rate, hyperscaler capex commitments above $700 billion, and the forward P/E constraints that determine how much margin for error remains if displacement-driven labour drag intensifies through the second half of 2026.

—