What ASML’s High NA EUV Actually Does to Chip Manufacturing

1 hr ago

Most dividend investors can name the Dividend Aristocrats. Far fewer can explain precisely why a Dividend King outranks one, or why a company can be a King without ever appearing on the Aristocrats list. The two designations are frequently mentioned together and just as frequently conflated, yet the distinction between them is not cosmetic. The qualification thresholds, the governing bodies (or absence of them), and the investor signals each designation sends are meaningfully different. Understanding those differences shapes how the designations function as screening tools. This article explains how each tier is defined, what earning that status actually demonstrates about a company, where the two lists overlap and diverge, and how investors can use both classifications purposefully when building a dividend-focused portfolio.

The Dividend Aristocrat designation is not simply a streak counter. It is a composite quality filter administered by S&P Dow Jones Indices, and each of its requirements does distinct structural work.

To qualify, a company must satisfy three criteria simultaneously:

The streak thresholds that define Aristocrat and King status are most meaningful when investors already have a solid grounding in dividend mechanics, specifically the relationship between payout dates, share price adjustments on the ex-dividend date, and how yield figures can mislead when detached from total return context.

S&P 500 membership is worth emphasising. It is not an administrative footnote. The requirement means that every Aristocrat has already passed through one of the most widely followed quality and size screens in global equity markets. A mid-cap company with a 30-year dividend growth streak would not qualify if it sat outside the S&P 500.

Because S&P Dow Jones Indices formally governs the index, reconstitution happens on a defined annual schedule. Companies that shrink out of the S&P 500, lose liquidity, or cut a dividend are automatically removed. The list is self-pruning: it maintains a quality floor passively, without requiring investor judgement.

The S&P Dow Jones Indices methodology for the Dividend Aristocrats Index codifies the eligibility criteria, annual reconstitution schedule, and quarterly re-weighting process that give the designation its formal, self-pruning character, distinguishing it sharply from the informal tracking arrangements that govern the Kings list.

Current composition: The S&P 500 Dividend Aristocrats Index contains 69 companies as of the 2026 rebalancing, up from 66 in 2024. (Sources: ProShares NOBL factsheet, Simply Safe Dividends)

Three companies were added during the 2025 rebalancing, bringing the total from 66 to 69:

The index reconstitutes annually, and this is when additions and removals are formalised. No removals were reported for the 2025 cycle.

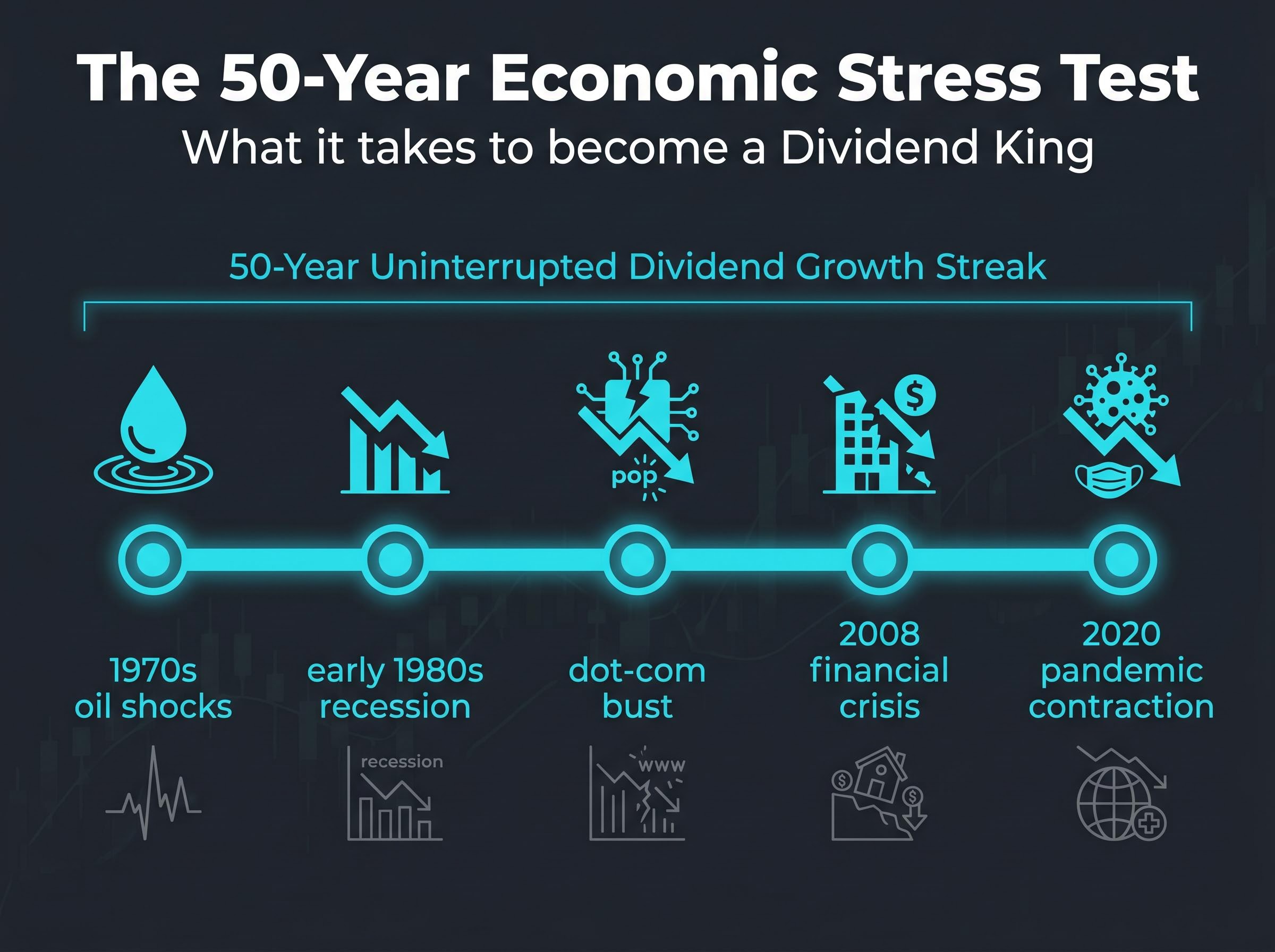

A Dividend King must have raised its dividend every year for at least 50 consecutive years. That is double the Aristocrat threshold, and the weight of it becomes apparent when measured against actual economic history.

Fifty consecutive years of uninterrupted dividend growth means a company has maintained rising payouts through the 1970s oil shocks, the early 1980s recession, the dot-com bust, the 2008 financial crisis, and the 2020 pandemic contraction. The streak itself is a signal of corporate durability that few other metrics can replicate.

The second point that separates Kings from Aristocrats is governance, or rather its absence. There is no official index provider for Dividend Kings. The designation is informal, tracked independently by financial media outlets rather than administered by any single authority.

The sources that maintain Kings lists include:

The count discrepancy itself is a useful data point. It reflects the informal nature of the designation: different sources may apply slightly different eligibility interpretations or update on different schedules.

Because there is no S&P 500 membership requirement, the Kings universe can include smaller and mid-cap companies that would never qualify as Aristocrats regardless of their streak length. This structural openness gives the Kings list a different character, one defined entirely by longevity rather than by size or index membership.

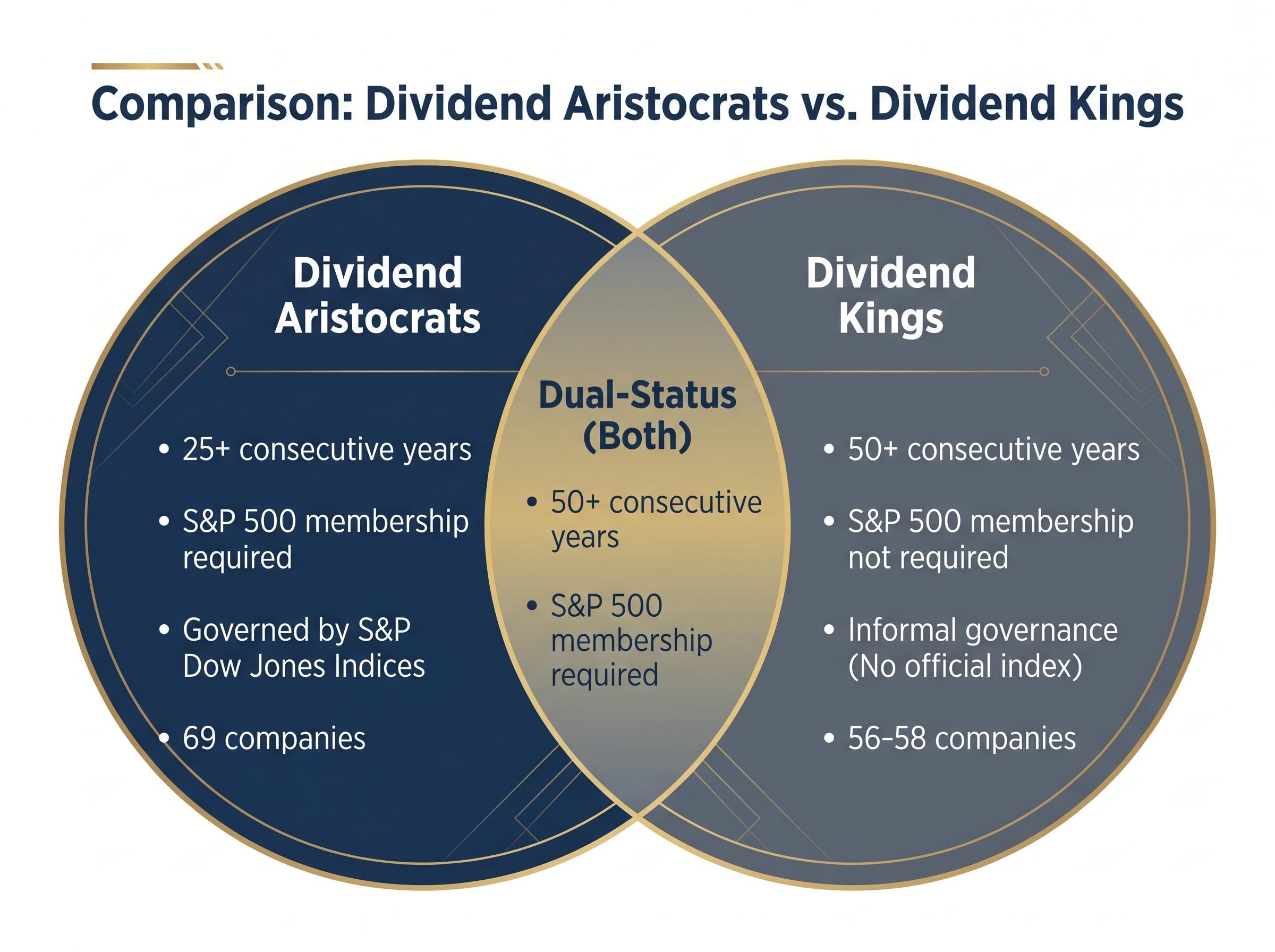

The most common misconception is that Dividend Kings are a subset of Dividend Aristocrats, a “tier above” within the same list. The relationship is more interesting than that.

The two lists are not nested. A company can be a King without being an Aristocrat if it is not a member of the S&P 500. A company can be an Aristocrat without being a King if its dividend growth streak falls between 25 and 49 years. Companies that hold S&P 500 membership and have streaks of 50-plus years occupy the intersection, qualifying under both designations simultaneously.

What each list primarily signals is also distinct. Aristocrats signal durable dividend growth combined with size and liquidity discipline. Kings signal extreme streak longevity regardless of company size.

| Feature | Dividend Aristocrats | Dividend Kings | Dual-Status (Both) |

|---|---|---|---|

| Streak requirement | 25+ consecutive years | 50+ consecutive years | 50+ consecutive years |

| S&P 500 membership | Required | Not required | Required (via Aristocrats) |

| Governing body | S&P Dow Jones Indices | None (informal) | Formal + informal |

| Approximate member count | 69 | 56-58 | Varies by cycle |

Understanding this Venn structure prevents a common investor error: treating Kings as simply a “better” list than Aristocrats. The two designations measure overlapping but distinct qualities. Combining both as screening inputs gives a more complete picture than either alone.

The ProShares NOBL ETF, which tracks the S&P 500 Dividend Aristocrats Index, reports an average dividend yield of approximately 2.59% (as of Q1-Q2 2026). This figure provides a useful benchmark for the Aristocrats universe as a whole.

No equivalent single yield figure exists for the full Kings universe. Because Kings have no official index or tracking ETF, investors must assess individual holdings on a company-by-company basis when evaluating yield from this group.

The Aristocrat and King designations are outputs, not inputs. They are the visible result of specific corporate financial characteristics operating consistently over long periods. Understanding what those characteristics are transforms the streak number from a label into a diagnostic tool.

Three requirements underpin every multi-decade dividend growth streak:

Payout sustainability sits at the centre of what long streaks actually measure, and recent market data from early 2026 illustrates why this matters in practice: dividend-growth strategies that screen for earnings quality and sustainable payout ratios outperformed pure high-yield approaches across a period when many investors expected the opposite.

A 50-year streak means rising dividends through every major recession since the mid-1970s. That is not a historical curiosity. It is evidence of earnings durability and payout discipline operating together across generational structural shifts.

These three characteristics are what the Aristocrat and King designations are actually measuring. Knowing this helps investors evaluate whether a candidate company outside either list possesses the same underlying financial qualities that produce multi-decade streaks.

Both designations function best as starting screens that narrow the investable universe to companies with demonstrated financial consistency. They are not buy signals on their own.

The recommended screening sequence for investors using these designations:

The complementary use case is straightforward. Aristocrats provide a size-and-liquidity-filtered view of long-term dividend growers: 69 companies constrained to the S&P 500, formally governed by S&P Dow Jones Indices. Kings extend the universe to smaller companies with even longer streaks: 56-58 companies with no size constraint, useful for investors who prioritise streak longevity over index membership.

After the initial screen, the work of analysing individual payout ratios, earnings trajectories, and sector exposures remains with the investor. The designation gets the list short. It does not make the decision.

Reinvesting dividends from companies with consistent annual increases compounds on two axes simultaneously. The reinvested dividends purchase additional shares, growing the investor’s share count. The rising per-share payment then applies to that larger share count each year.

This dual compounding effect is particularly relevant for investors with multi-decade holding horizons, where the difference between a static dividend and a consistently growing one becomes increasingly material over time. The longer the streak, the longer both compounding axes have operated in the investor’s favour.

Dividend Aristocrats are a formally governed, S&P 500-constrained universe of companies with 25-plus years of consecutive dividend growth. Dividend Kings are an informally tracked, size-unrestricted universe requiring 50-plus years. The two lists overlap where large-cap companies have maintained half-century streaks, but they are not nested subsets, and they measure related but not identical qualities.

The most productive investor application treats both designations as complementary first-pass filters rather than competing rankings. Combined, they identify a broad universe of companies whose financial discipline has been stress-tested across multiple economic cycles.

That stress-testing is precisely where the designations earn their analytical value. Achieving either threshold requires the kind of payout discipline, earnings durability, and capital allocation consistency that is genuinely difficult to sustain across decades. The streak is not the achievement. It is the evidence.

For investors wanting to stress-test the dividend-growth framework against a broader set of portfolio strategies, our dedicated guide to dividend investing vs total return compares a decade of backtested performance data, examines the 2026 rate environment where Treasuries and high-yield savings accounts both yield above the Aristocrats index average, and maps which approach tends to build more wealth across different investor lifecycle stages.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Dividend Aristocrats are S&P 500 companies with at least 25 consecutive years of dividend increases, formally governed by S&P Dow Jones Indices, while Dividend Kings are informally tracked companies with at least 50 consecutive years of increases and no S&P 500 membership requirement.

Yes, a company can be a Dividend King without being a Dividend Aristocrat if it is not a member of the S&P 500, since S&P 500 membership is a mandatory requirement for Aristocrat status but not for King status.

As of the 2026 rebalancing, the S&P 500 Dividend Aristocrats Index contains 69 companies, up from 66 in 2024, with Erie Indemnity, Eversource Energy, and FactSet Research Systems added during the 2025 rebalancing.

Both designations work best as first-pass filters that narrow the investable universe to companies with proven financial consistency; investors should then follow up with payout ratio analysis, earnings growth review, and sector concentration checks before making individual stock decisions.

A 50-year streak of uninterrupted dividend increases means the company has maintained rising payouts through every major economic downturn since the mid-1970s, serving as evidence of earnings durability, sustainable payout ratios, and a management culture committed to consistent shareholder returns.