What ASML’s High NA EUV Actually Does to Chip Manufacturing

1 hr ago

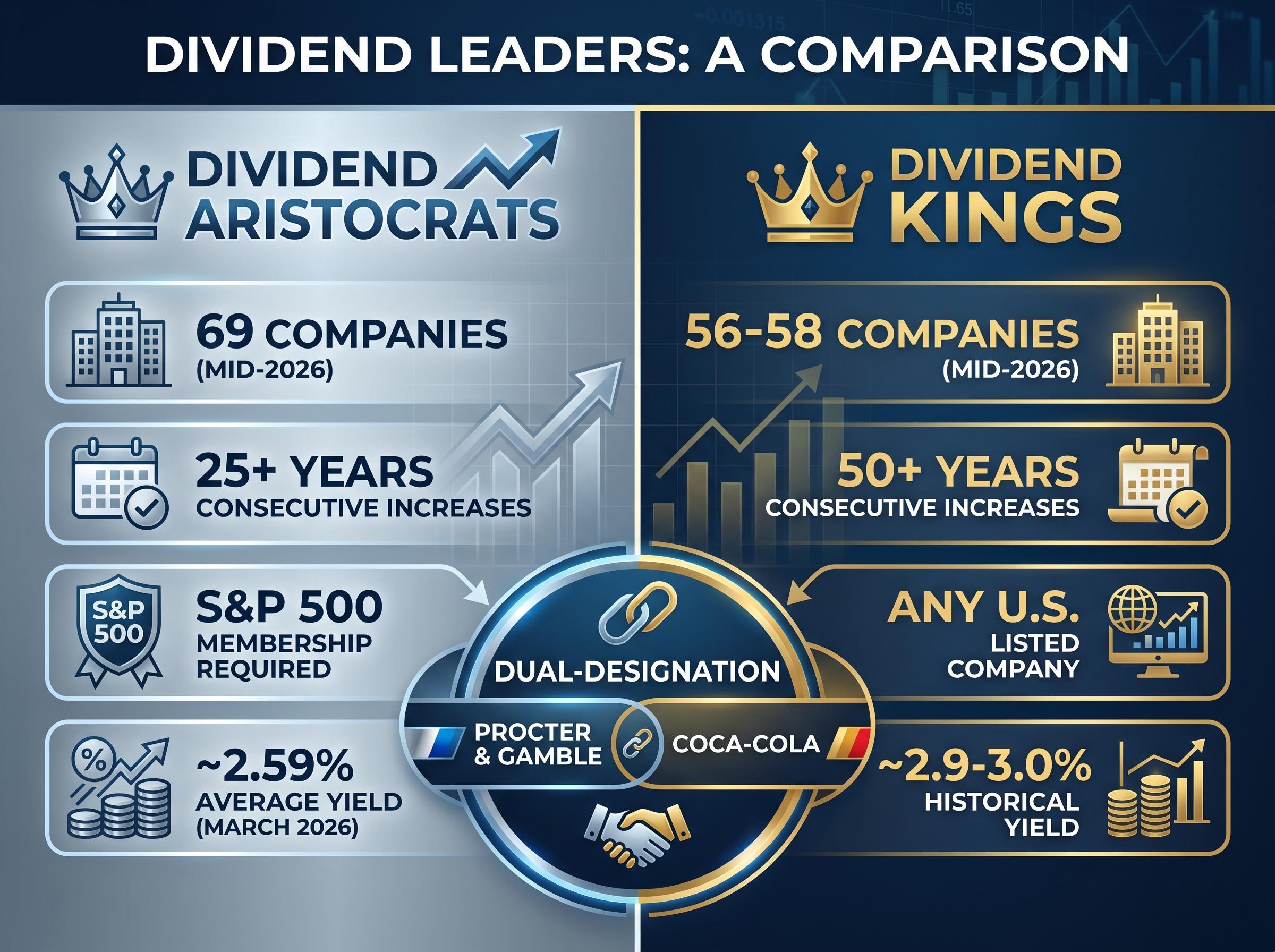

If two companies have both raised their dividend every single year for decades, why does the investing world treat one as meaningfully more elite than the other? The answer is not simply a number. It is a structural filter that screens for corporate survival across an entirely different time horizon. Dividend Aristocrats and Dividend Kings are the two most widely cited pedigree classifications in dividend investing, and as of mid-2026, 69 companies hold Aristocrat status while between 56 and 58 carry the King designation. The distinction between the two is frequently mentioned but rarely unpacked in a way that helps investors understand what the gap actually signals about business durability. What follows is a complete breakdown of how each classification is defined, what the qualification gates reveal about financial resilience, and how to deploy both frameworks as a practical dividend stock screening tool.

Dividend yield alone is an incomplete screening metric. A stock yielding 6% might reflect a healthy, growing payout, or it might reflect a share price in freefall while the dividend has not yet been cut. Yield tells an investor what a company pays today. It says nothing about whether that payment will still arrive next year, or the year after, or the decade after that.

Dividend yield as a metric carries a structural blind spot: the share price falls by approximately the payment amount on the ex-dividend date, meaning a company paying a rising dividend is not necessarily creating new wealth for shareholders at the moment of distribution.

Consecutive-growth streaks solve a different problem. A company that has increased its dividend per share every year for 25 or 50 years has, by definition, maintained that discipline through recessions, sector disruptions, commodity shocks, and multiple changes in senior leadership. The streak itself becomes a durability filter, compressing decades of balance sheet performance into a single, verifiable credential.

A long consecutive dividend-growth streak is a survivorship credential, not a loyalty programme. It tells investors the company generated sufficient earnings across multiple economic cycles to fund an increasing payout each year, regardless of conditions.

Classifications like Aristocrats and Kings emerged as shorthand for investors seeking demonstrated payout discipline without running full fundamental analysis on every candidate in a universe of thousands. The minimum Aristocrat threshold of 25 years spans roughly six to seven typical business cycles. The King threshold of 50 years spans the careers of multiple management teams entirely. Both are designed to filter for the kind of corporate financial resilience that a single strong quarter or even a strong decade cannot replicate.

Reaching Aristocrat status involves clearing multiple simultaneous requirements, not simply accumulating years. The qualification criteria function as a layered set of gates, each narrowing the eligible field considerably.

The three core requirements are:

S&P 500 membership is itself a significant filter. It excludes mid-cap and small-cap companies regardless of how long their dividend streaks may be. The index is officially maintained by S&P Dow Jones Indices and rebalanced annually, with additions and removals driven by whether companies cross or break the required thresholds.

The S&P Dow Jones Indices Aristocrats methodology specifies equal-weighting across constituents and quarterly rebalancing, meaning the index is not simply a static list but a rules-governed vehicle with defined processes for adding and removing members as companies cross or break the required thresholds.

As of mid-2026, 69 companies hold Aristocrat status, per the ProShares NOBL factsheet. The average yield across the group stood at approximately 2.59% as of 31 March 2026. Well-established members include Procter & Gamble, Coca-Cola, PepsiCo, and Caterpillar, which was added at the February 2024 rebalance after crossing the 25-year threshold. 3M was removed at the same rebalance following dividend streak disruption related to its Solventum spin-off.

Walgreens Boots Alliance cut its dividend in January 2024, ending a multi-decade streak and triggering removal from the Aristocrats index. The case illustrates what streak disruption means in practice: a single cut, regardless of the company’s prior track record, results in immediate loss of the designation.

Removals from the Aristocrats list, when they happen, tend to carry a signal. They indicate that the financial conditions or strategic choices at a company have shifted enough to break a discipline that had persisted for a quarter-century or more.

The Dividend King threshold is 50 consecutive years of annual dividend increases, double the Aristocrat requirement. That additional 25 years is not merely a longer version of the same achievement. It represents an entirely different category of corporate endurance.

A company reaching King status has maintained its payout discipline across the tenures of multiple chief executives, through inflationary environments (the 1970s and early 1980s), financial crises (2008), a global pandemic (2020), and structural shifts in its own industry. The streak spans eras, not just cycles.

The other structural distinction is equally important: Kings have no index-membership requirement. Any publicly listed U.S. company can qualify, regardless of whether it sits in the S&P 500. This opens the designation to mid-cap and smaller companies that would never appear on the Aristocrats list despite having longer and arguably more impressive payout records.

Prominent Dividend Kings include:

As of mid-2026, between 56 and 58 companies hold the Dividend King designation, depending on the source. That count has risen from 53 in 2024 and 54 in early 2025, reflecting new companies crossing the 50-year threshold each year. Both 3M and Walgreens Boots Alliance lost King status, confirming that even long-tenured members can have their designation withdrawn.

“Dividend King” has no regulatory or index-provider authority behind it. The term emerged as an industry designation and is maintained through consensus across financial research platforms, most notably Sure Dividend and Simply Safe Dividends. This is why membership counts vary slightly by source: Sure Dividend reports 58 Kings as of May 2026, while Simply Safe Dividends reports 56 as of April 2026.

The unofficial status does not diminish the achievement. It simply means investors building a Kings watchlist should cross-reference lists from multiple sources and verify individual company streaks independently rather than relying on a single authority.

The overlap between the two classifications is substantial. Any Dividend King with S&P 500 membership automatically satisfies the 25-year Aristocrats threshold, placing it on both lists simultaneously. Coca-Cola, Procter & Gamble, and Johnson & Johnson are prominent dual-designation examples.

The smaller Kings count relative to Aristocrats, 56-58 versus 69, reflects the severity of the additional 25 years rather than any selectivity in screening methodology. Fewer companies have survived half a century of unbroken payout growth than have survived a quarter-century within the S&P 500.

| Feature | Dividend Aristocrats | Dividend Kings | Implication for investors |

|---|---|---|---|

| Streak required | 25+ consecutive years | 50+ consecutive years | Kings filter for multi-generational discipline |

| Index status | Official S&P Dow Jones Indices index | Unofficial; tracked by research outlets | Aristocrats have standardised rebalancing rules |

| Eligible universe | S&P 500 members only | Any U.S. listed company | Kings include mid-cap names excluded from Aristocrats |

| Current count (mid-2026) | 69 companies | 56-58 companies | Fewer companies survive the longer threshold |

| Primary investable vehicle | ProShares NOBL ETF | No dedicated official-index ETF | Aristocrats offer simpler single-vehicle access |

| Approximate average yield | ~2.59% (March 2026) | Historically ~2.9-3.0% | Kings have tended to yield slightly more |

Investors outside the United States can apply analogous frameworks in their own markets, though streak requirements are shorter: 10 years in the UK and pan-Europe, 5 years in Canada, and 7 years in the Asia-Pacific region, reflecting different corporate payout cultures and smaller market sizes.

A 50-year dividend-growth streak is not a statistic. It is a consequence of specific, repeatable business characteristics that allowed the company to generate increasing free cash flow across half a century of economic conditions.

The corporate qualities that tend to produce long streaks cluster around four areas:

Portfolio resilience across economic regimes is the deeper goal that dividend-pedigree classifications serve: a company maintaining a 50-year payout streak has by definition generated sufficient free cash flow through inflation shocks, financial crises, and structural industry shifts, precisely the range of conditions a resilient portfolio must be built to survive.

Payout ratio is worth particular attention. Companies that distribute nearly all of their earnings leave no margin for error. Companies with sustainable payout ratios, typically in the 40-60% range for consistent growers, retain enough earnings to absorb a downturn without reducing the dividend.

The survivorship element is real but also a limitation. Looking only at current Kings excludes companies that attempted long streaks and failed. Membership in either classification should not be treated as a guarantee that the streak will continue indefinitely. The removals of 3M and Walgreens from both lists illustrate that even decades-long tenures can end when business models or financial structures change materially.

Sure Dividend’s Ben Reynolds has described Kings as having “impressive stability but may sacrifice some growth,” a trade-off that income-focused investors should weigh explicitly. The discipline required to maintain a 50-year streak often correlates with mature, slower-growth business models concentrated in sectors like consumer staples and industrials.

Both classifications are most useful when treated as first-pass filters that efficiently narrow the investable universe to companies with demonstrated payout discipline. They are not buy signals on their own.

The layering principle works in sequence:

Sector concentration risk is a structural consequence of dividend-pedigree strategies, since consumer staples and industrials dominate both the Aristocrats and Kings lists; high-dividend ETFs such as VYM and SCHD hold less than 6% in Technology while allocating over 18-24% to Financials, creating implicit sector bets that most investors do not anticipate when they buy a dividend label.

The ProShares NOBL ETF provides a single-vehicle way to access the full Aristocrats index for investors who prefer diversified exposure over individual stock selection. No equivalent official-index ETF exists for Dividend Kings, meaning King-focused investors typically build individual positions.

Income-focused investors, particularly those in or approaching retirement, may find higher-yielding Kings in consumer staples and industrials more aligned with their need for capital preservation and steady cash flow. The historically higher average yield of the Kings group (approximately 2.9-3.0% in recent years, compared with 2.59% for Aristocrats as of March 2026) reflects this tilt toward mature, income-generating businesses.

Growth-oriented investors may prefer Aristocrats with stronger earnings growth rates and lower current yields but greater long-term total return potential. The S&P 500 membership requirement ensures Aristocrats skew toward companies with the scale and market positioning to compound capital over time.

A blended approach is common: holding a core of Aristocrats for index-linked diversification alongside targeted Kings positions for higher current income. The international dimension is also relevant. Investors outside the United States can apply analogous streak-based frameworks in their own markets, adjusting expectations for the shorter streak requirements (for example, 10 years in the UK, 7 years in Asia-Pacific) that reflect local corporate payout norms.

The distinction between Dividend Aristocrats and Dividend Kings is structural, not cosmetic. Aristocrats represent 25 years of demonstrated payout discipline within the S&P 500. Kings represent 50 years across any listed U.S. company, an achievement that reflects a different order of corporate resilience and embedded financial culture.

Both classifications function as screening tools of genuine value, but neither substitutes for fundamental analysis of payout sustainability, earnings quality, and business model durability. A streak is a credential. It is not a forecast.

As more companies approach the 50-year threshold in coming years, the Kings count rising from 53 in 2024 to 56-58 by mid-2026, the line between the two tiers will sharpen further. For investors building or maintaining dividend-focused portfolios, understanding exactly what each designation measures, and where its explanatory power ends, is increasingly worth the effort.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

A Dividend Aristocrat must be an S&P 500 member with at least 25 consecutive years of annual dividend increases, while a Dividend King requires 50 consecutive years of increases and has no index-membership requirement, meaning any publicly listed U.S. company can qualify.

As of mid-2026, between 56 and 58 companies hold the Dividend King designation depending on the source, with Sure Dividend reporting 58 Kings as of May 2026 and Simply Safe Dividends reporting 56 as of April 2026.

Yes, any Dividend King that is also an S&P 500 member automatically qualifies as a Dividend Aristocrat, with Coca-Cola, Procter and Gamble, and Johnson and Johnson being prominent examples of dual-designation companies.

The ProShares NOBL ETF tracks the S&P 500 Dividend Aristocrats index, offering single-vehicle diversified exposure; no equivalent official-index ETF exists for Dividend Kings, so King-focused investors typically build individual stock positions.

A single dividend cut or freeze is enough to end a consecutive-growth streak and trigger immediate removal from both designations, as demonstrated by Walgreens Boots Alliance cutting its dividend in January 2024 and 3M having its streak disrupted by its Solventum spin-off.