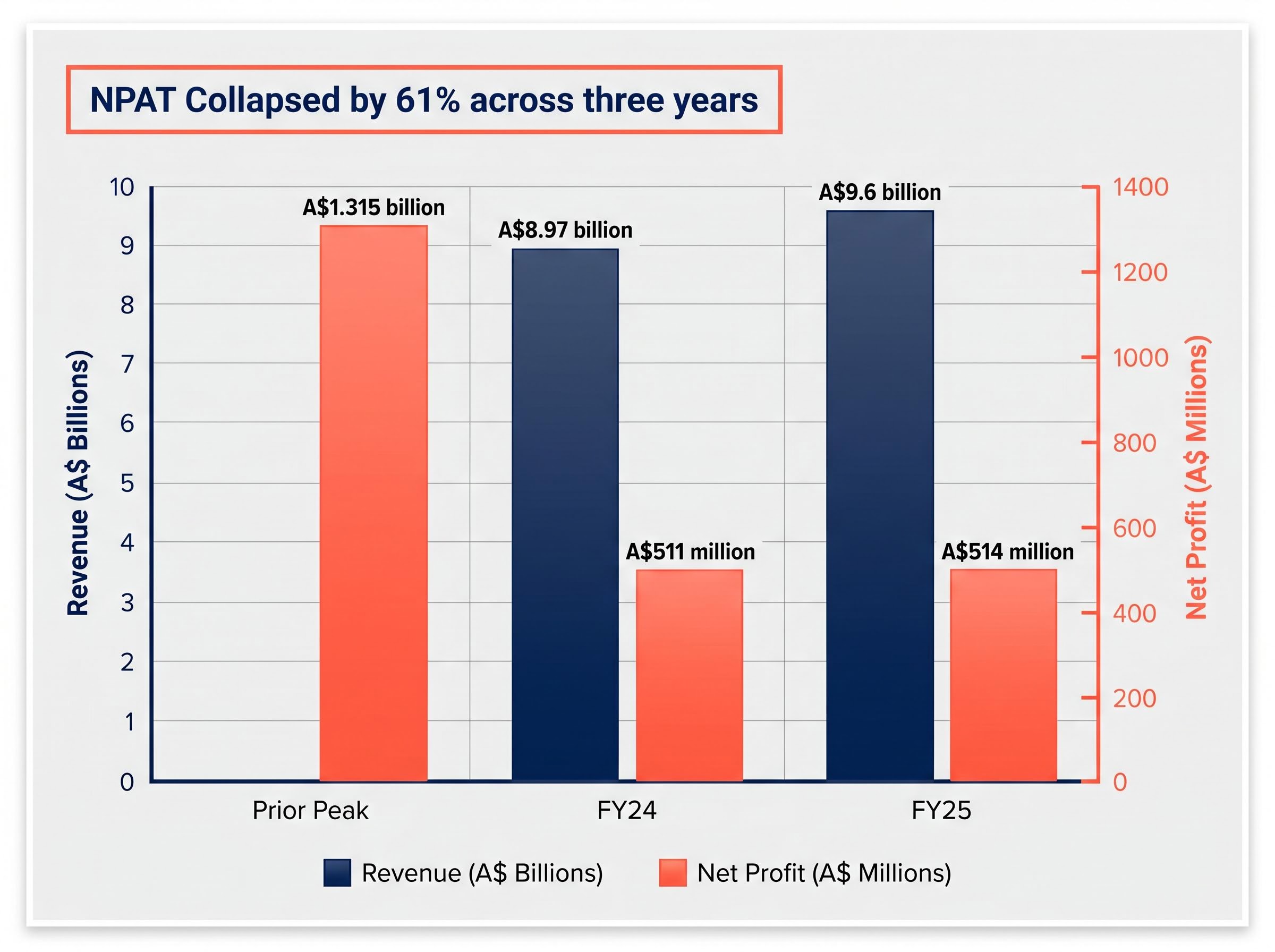

Sonic Healthcare shares have lost roughly 30% of their value since the start of FY2026, falling from around A$27 to approximately A$18.65 by late May 2026. The headline revenue line barely flinched over the same period that net profit after tax collapsed by 61%, from A$1.315 billion to A$511 million across three years. That divergence, a stable top line masking a hollowed-out bottom line, is the central question facing any investor evaluating the stock today. The share price decline has compressed the price-to-sales ratio to roughly 1.03x, a 47% discount to the five-year average of 1.94x. Whether that discount represents genuine mispricing or a fundamentally altered earnings profile is what this analysis sets out to unpack, examining the structural causes of the profit collapse, the balance sheet risk layer, and what three distinct valuation frameworks reveal about the current price.

Revenue held up. Profit collapsed. Here is what happened between those two lines.

FY24 revenue came in at A$8.97 billion, reflecting a three-year compound annual growth rate of just 0.8%. The top line barely moved. Net profit after tax (NPAT), the amount a company earns after all expenses and taxes, told a completely different story.

Non-discretionary demand in healthcare is often cited as a floor for pathology revenue, and Sonic Healthcare’s top-line stability across the post-COVID normalisation period provides a concrete illustration of that principle, with revenue holding near A$9 billion even as the high-margin testing mix evaporated.

NPAT fell at a three-year CAGR of approximately -27%, from A$1.315 billion to A$511 million.

The proximate cause was the evaporation of COVID PCR testing revenue. During the pandemic years, Sonic Healthcare generated substantial income from high-margin diagnostic testing that required the same laboratory infrastructure but commanded premium pricing. As testing volumes normalised, three revenue categories bore the brunt:

- PCR testing revenue, which fell steeply as public health mandates ended and demand collapsed

- High-margin pandemic-era add-on tests, which disappeared alongside PCR volumes

- Volume mix, which shifted back toward routine pathology work operating at structurally lower margins

The base pathology business that remained was growing modestly, but it could not replicate the margin profile of pandemic-era testing. Gross margin settled at 32.8% in FY24, reflecting the new reality of the underlying business without its COVID supplement.

FY25 signals the floor may be in, but not a return to peak

FY25 full-year results, released in August 2025, showed revenue of A$9.6 billion and NPAT of A$514 million. That NPAT figure represents only a A$3 million improvement on FY24, which is stabilisation rather than recovery.

EBITDA growth told a slightly more encouraging story, rising approximately 8% to A$1.725 billion. The gap between EBITDA growth and NPAT growth suggests that items below the EBITDA line, including interest costs on debt and depreciation from acquisitions, continue to compress net profit even as operating performance improves.

When big ASX news breaks, our subscribers know first

Four cost pressures that compressed the margin between revenue and profit

The earnings collapse was not one problem. It was four simultaneous structural headwinds, each operating on a different timeline and each requiring a distinct management response.

- Labour inflation: Wages for pathologists, scientists, and nursing staff rose across Australia, Germany, and the United States. Tight labour markets forced overtime and agency costs higher to maintain service levels. This pressure was immediate.

- Consumables, transport, and energy costs: Rising reagent prices, fuel costs, and electricity expenses hit laboratory operating budgets directly. Management acknowledged inflationary pressures in consumables and utilities in the FY24 results presentation.

- Medicare and payer reimbursement constraints: In Australia, Medicare pathology rebates remained constrained in several test categories, limiting revenue per test. In Europe and the United States, public and private payer pricing pressure created a similar ceiling. This headwind is structural and slow-moving.

- Contract repricing lag: Multi-year contracts with health systems and insurers limited immediate pass-through of rising costs. Management cited renegotiation timelines as a factor compressing short-term margins. Resolution here takes years, not quarters.

Medicare Benefits Schedule uncertainty adds a specific dimension to the reimbursement picture, with pathology changes effective 1 March 2026 introducing a new layer of regulatory risk that sits alongside the broader payer pricing constraints already compressing Sonic Healthcare’s revenue per test.

The 2024-25 Budget pathology reforms reintroduced annual indexation for certain pathology services from 1 July 2025, marking a partial policy reversal after years of constrained rebate growth, though the adjustment falls short of fully compensating laboratories for cumulative cost inflation over the prior cycle.

| Cost Pressure | Management Response |

|---|---|

| Labour inflation across three geographies | Lab automation investment and central lab consolidation to reduce headcount dependency |

| Rising reagent, transport, and energy costs | Procurement efficiency programmes and supplier renegotiation |

| Constrained Medicare/payer reimbursement | Volume growth strategy and cost-per-test reduction through scale |

| Multi-year contract repricing lag | Staggered renegotiation cycles; LADR acquisition in Germany (FY25) to build scale leverage |

The management responses, automation, procurement efficiency, and scale acquisitions, are structurally sound. They are also two-to-three-year initiatives, not quarterly fixes. Investors assessing a recovery timeline should calibrate expectations accordingly.

What price-to-sales, DCF, and DDM each say about the 47% discount

Three valuation frameworks offer three different readings of the same share price, and none of them resolves the question alone.

Sonic Healthcare’s price-to-sales ratio sits at approximately 1.03x against a five-year average of 1.94x, a discount of roughly 47%.

Price-to-sales (P/S) is the simplest lens. It divides the company’s market capitalisation by its annual revenue, measuring how much investors pay per dollar of sales. At 1.03x, the stock screens as deeply discounted relative to its own history. The limitation is that P/S ignores profitability entirely. A company trading at a low P/S with collapsing margins may deserve that discount.

Discounted cash flow (DCF) analysis estimates what a business is worth today by projecting its future cash flows and discounting them back to present value using a required rate of return. For Sonic Healthcare, the output is highly sensitive to the earnings recovery assumption. A scenario where NPAT recovers to A$700 million within three years produces a materially different intrinsic value than one where NPAT remains near A$514 million.

The dividend discount model (DDM) anchors on the income stream. Sonic Healthcare paid a final dividend of A$0.63 per share in FY25 (35% franked), and the FY24 total dividend was A$1.06 per share (0% franked). DDM is only as reliable as its dividend growth assumption, and a compressed earnings base places that assumption under scrutiny.

| Valuation Method | What It Measures | SHL Reading | Key Limitation |

|---|---|---|---|

| Price-to-Sales (P/S) | Market value per dollar of revenue | 1.03x vs five-year average of 1.94x | Ignores profitability; a low P/S may be warranted if margins are permanently lower |

| Discounted Cash Flow (DCF) | Present value of projected future cash flows | Highly sensitive to NPAT recovery speed and discount rate assumptions | Outputs vary dramatically based on earnings trajectory; slower recovery path reduces intrinsic value materially |

| Dividend Discount Model (DDM) | Present value of expected future dividends | Current yield supported by A$0.63 final dividend (FY25), but growth assumption is uncertain | Only as reliable as the dividend growth rate; compressed earnings threaten payout sustainability |

The single most important insight from holding all three frameworks simultaneously: the P/S ratio alone cannot answer the value-versus-trap question. The answer depends entirely on the earnings trajectory that DCF and DDM attempt to model.

For investors wanting to apply this kind of multi-lens thinking more systematically, our full explainer on share valuation methods on the ASX walks through a structured five-step sequence combining P/S, DCF, EV/EBITDA, and DDM, with worked examples showing how each method catches blind spots the others miss.

The balance sheet and ROE numbers that risk-conscious investors should not overlook

The valuation discount may attract attention. The balance sheet and capital efficiency metrics demand equal scrutiny before any investment judgment.

- Net debt: A$3.871 billion. This is a substantial absolute figure, particularly in a compressed earnings environment. It reflects years of acquisition-funded growth.

- Debt-to-equity ratio: 55.9%. Equity still exceeds debt, which means the balance sheet is not distressed, but the leverage is meaningful at a time when NPAT remains well below peak.

- Return on equity (ROE): 6.8% in FY24. This figure indicates the company generated A$6.80 of profit for every A$100 of shareholder equity, a modest return for a large-cap ASX healthcare operator.

The A$3.871 billion debt load carries servicing costs that sit below the EBITDA line, contributing to the gap between EBITDA growth (8% in FY25) and NPAT growth (7%). In a period where interest rates rose across the prior cycle, the cost of carrying that debt would have increased, adding another layer of downward pressure on net profit.

ROE of 6.8%: reading what it signals about capital efficiency

Return on equity measures how effectively a company converts shareholder capital into profit. A 6.8% ROE means Sonic Healthcare is generating returns below what many institutional investors expect from a large-cap healthcare operator. If an investor’s required return on equity exceeds 6.8%, the current ROE is not meeting that threshold.

This metric stood materially higher when earnings were at their pandemic peak. The decline reflects both the NPAT compression and the accumulated equity base from years of acquisition spending. Recovery in ROE requires NPAT growth to outpace any further equity base expansion.

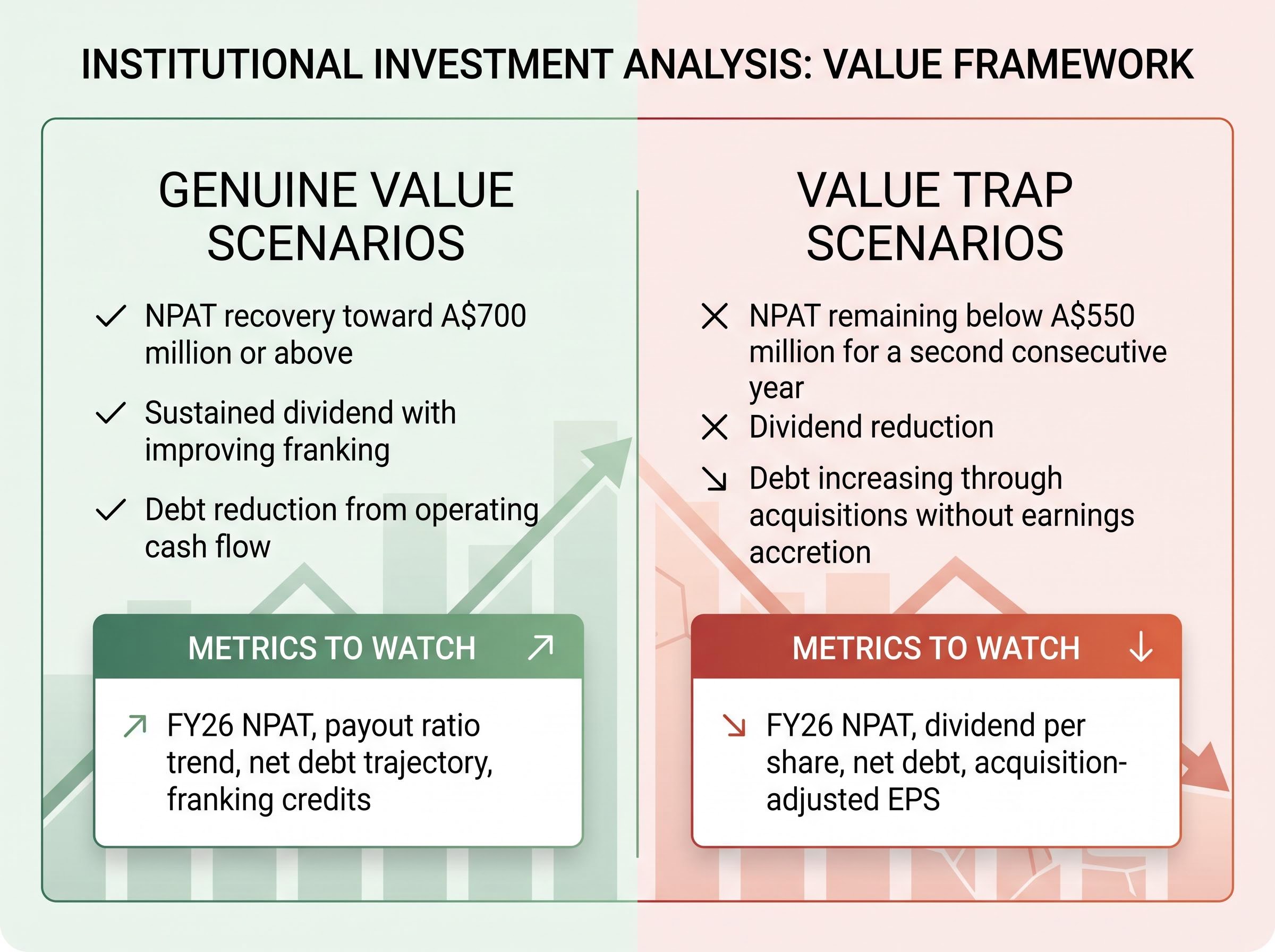

Value or value trap? The conditions that would resolve the question

The share price decline from approximately A$27 to A$18.65 has already priced in substantial pessimism. But pessimism already being priced in is not, by itself, a reason to buy. The distinction between genuine value and a value trap rests on specific financial conditions that will become visible over the coming reporting cycles.

A significant analyst consensus valuation gap sits beneath the surface of the current price, with a 15-analyst consensus target of A$22.00 sitting against a Morningstar fair value estimate of A$33.00, a spread that signals material disagreement among informed professionals about the pace and credibility of the earnings recovery path.

| Scenario | Supporting Conditions | Key Metrics to Watch |

|---|---|---|

| Genuine value | NPAT recovery toward A$700 million or above; sustained dividend at or above current levels with improving franking; debt reduction funded from operating cash flow | FY26 NPAT, payout ratio trend, net debt trajectory, franking credits |

| Value trap | NPAT remaining below A$550 million for a second consecutive year; dividend reduction; debt increasing through acquisitions without earnings accretion | FY26 NPAT, dividend per share, net debt, acquisition-adjusted EPS |

Sonic Healthcare’s geographic diversification across Australia, New Zealand, Germany (including the LADR acquisition), and the United States provides genuine structural breadth. The company is not a single-market operator exposed to one payer system. Management issued EPS growth guidance alongside the FY25 results, which represents a directional positive.

The conditions listed above are not predictions. They are the specific financial evidence that would confirm or deny the investment thesis over the next 12 to 18 months.

A 47% discount demands a question, not an assumption

The analytical picture holds together in three layers. Revenue is structurally stable. Earnings are recovering slowly from a structural reset driven by the loss of high-margin COVID testing and compounded by four simultaneous cost headwinds. The valuation screens as cheap on P/S, but the three frameworks examined here converge on the same conclusion: the discount is only meaningful if the NPAT recovery path is credible. Management’s FY25 EPS growth guidance addresses that question; it does not yet resolve it.

The next catalysts worth monitoring are the FY26 full-year results (due August 2026), any developments in Australian Medicare rebate policy, and further debt reduction announcements.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.