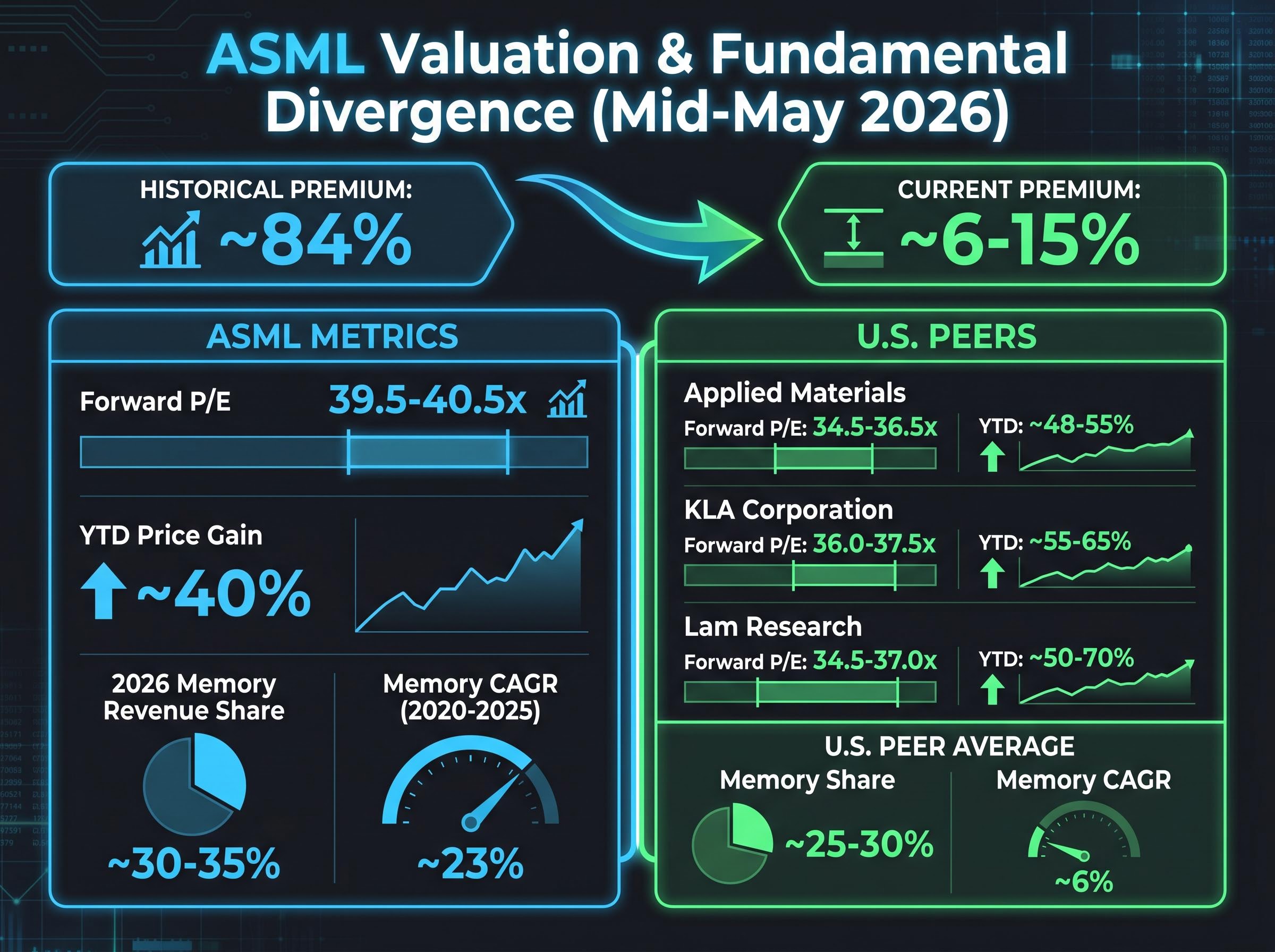

ASML holds an uncontested monopoly on the most advanced lithography tools in semiconductor manufacturing. Every leading-edge chip produced today passes through an ASML system. Yet the company’s valuation premium over its U.S. equipment peers has collapsed from a 10-year historical average of roughly 84% to approximately 6-15% as of mid-May 2026. A 20 May 2026 upgrade from UBS, lifting the price target to €1,900 and placing 2027 and 2028 earnings-per-share estimates 15-20% above consensus, has brought fresh attention to whether this compression reflects a rational re-rating or a mispricing. The analysis that follows examines the two most underappreciated fundamentals behind the constructive thesis: ASML’s accelerating memory market exposure and the long-term demand logic of High NA EUV. It also interrogates why the premium collapsed, so readers can assess whether the discount is structural or transient.

How a monopoly lost its premium: unpacking ASML’s valuation compression

The paradox is worth stating plainly. ASML’s monopoly on extreme ultraviolet (EUV) lithography is stronger in 2026 than it was in 2020. Every major foundry and memory manufacturer now depends on its tools. Yet the market has stripped out virtually all of the premium it once assigned for that dominance.

The current forward price-to-earnings multiples tell the story in a single frame.

| Company | Forward P/E (mid-May 2026) | YTD Price Gain | Implied Premium/Discount to ASML |

|---|---|---|---|

| ASML | 39.5-40.5x | ~40% | Baseline |

| Applied Materials | 34.5-36.5x | ~48-55% | ~10-15% discount |

| KLA Corporation | 36.0-37.5x | ~55-65% | ~5-10% discount |

| Lam Research | 34.5-37.0x | ~50-70% | ~8-15% discount |

ASML trades at roughly 39.5-40.5x forward earnings. Its U.S. peers average 35-37x. That implies a 10-15% premium, down from the historical norm of approximately 84%. The compression is the product of four distinct forces, not a single macro event:

- Cyclical order normalisation: EUV bookings surged during the 2021-2023 post-COVID upcycle, then moderated as foundries digested capacity. Slower bookings growth relative to peak expectations contributed to a de-rating.

- China export controls: U.S. and Dutch restrictions on advanced lithography sales to China introduced a geopolitical risk discount that U.S. peers do not carry to the same degree.

- EUV dominance priced in: The option value embedded in ASML’s multiple when EUV adoption was uncertain has largely dissipated now that EUV is mainstream for advanced logic and memory.

- Near-term earnings volatility: Customer capex push-outs, High NA R&D burdens, and mixed memory signals reduced the market’s willingness to pay a large premium relative to more diversified peers.

Some of these forces are likely permanent. Others may not be.

Semiconductor earnings revisions across the sector have exceeded 20% in 2026, driven by hyperscaler AI capex commitments, which provides important context for evaluating whether ASML’s compressed premium reflects genuine fundamental deterioration or a market that has re-rated a monopoly alongside a broadly re-rated sector.

When big ASX news breaks, our subscribers know first

What EUV dominance being “priced in” actually means for long-run value

When analysts describe ASML’s EUV monopoly as “priced in,” they mean the market no longer assigns option value for EUV adoption. During the 2017-2022 period, uncertainty about whether foundries would fully commit to EUV lithography, a technology where a single tool costs more than $150 million, supported a sustained premium. That uncertainty has been resolved. TSMC, Samsung, and every leading memory manufacturer now depend on EUV for their most advanced nodes.

The re-rating makes sense on those terms. What it may not fully account for is the distinction between penetration rate and intensity.

Penetration vs. intensity: why the distinction matters

EUV penetration measures how many fabs use the technology. Intensity measures how many EUV layers each wafer requires at successive node generations. Penetration is approaching saturation for leading-edge logic. Intensity is not.

Samsung, SK Hynix, and Micron have all confirmed EUV adoption starting at the 1a DRAM node, with increasing layer counts projected at 1b and 1c nodes, according to semiconductor trade press. Each node generation requires more EUV steps per wafer, meaning ASML’s revenue per customer grows even without new customer additions.

UBS analysis projects that 2027 production capacity could accommodate over 50% year-on-year expansion in leading-edge wafer output, against anticipated demand growth of approximately 25-30%. The finding suggests supply bottleneck concerns may be overstated.

Intensity growth is a recurring revenue dynamic. Investors who treat EUV as fully priced in may be conflating the end of adoption optionality with the beginning of the intensity growth curve.

The memory growth engine most investors are not modelling correctly

The least appreciated dimension of ASML’s investment case is not that the company has memory revenue. It is the rate at which that revenue has compounded relative to peers, and the structural reasons why the gap is likely to widen.

According to UBS analysis, ASML’s memory revenues grew at approximately 23% compound annual growth rate (CAGR) between 2020 and 2025, compared with approximately 6% for comparable U.S. equipment peers. Memory is projected to represent roughly 30-35% of ASML’s total revenues in 2026, versus approximately 25-30% for the U.S. peer group.

| Company | Memory Revenue Share (~2026) | Memory Revenue CAGR 2020-2025 | Key Memory Exposure Type |

|---|---|---|---|

| ASML | ~30-35% | ~23% | EUV lithography monopoly (all EUV DRAM layers) |

| U.S. Peers (avg.) | ~25-30% | ~6% | Deposition, etch, inspection (competitive categories) |

The structural difference matters. ASML’s lithography monopoly means every EUV-enabled DRAM node transition flows exclusively through its tools. U.S. peers compete across deposition, etch, and inspection categories where memory capex is allocated more broadly among multiple suppliers.

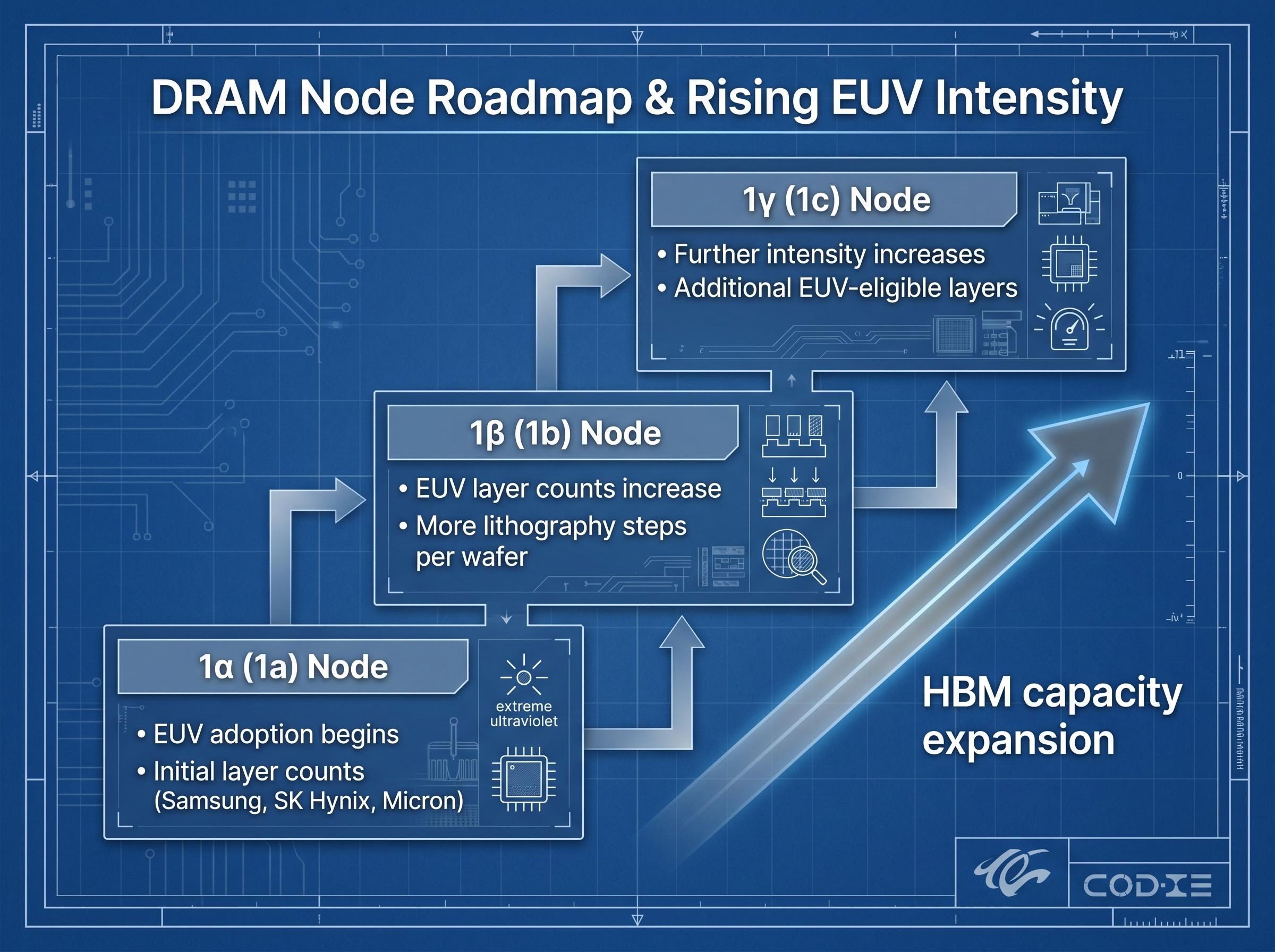

The DRAM node roadmap connects directly to rising EUV intensity:

- 1α (1a) node: EUV adoption begins. Initial layer counts established across Samsung, SK Hynix, and Micron.

- 1β (1b) node: EUV layer counts increase. More lithography steps per wafer raise tool utilisation and consumables demand.

- 1γ (1c) node: Further intensity increases projected, with trade press indicating additional EUV-eligible layers at each successive generation.

HBM (high-bandwidth memory) capacity expansion, running in parallel with standard DRAM node transitions, adds incremental demand. The combined effect is a sequential and cumulative tailwind that extends into the late 2020s, according to industry coverage from Semiconductor Engineering.

The demand picture underneath these node transitions is shaped by a memory chip supercycle that differs structurally from previous DRAM upcycles, with AI data centre operators now accounting for an estimated 70% of total memory shipment volumes and hyperscaler capex commitments extending the cycle well beyond typical inventory correction windows.

The TechInsights DRAM technology roadmap confirms that Samsung and SK Hynix have expanded EUV lithography across their D1a and D1b node generations, with further EUVL step increases planned for D1c, providing independent technical verification of the layer intensity growth trajectory underpinning ASML’s memory revenue compounding.

This exclusivity is not fully reflected in peer-relative multiples.

High NA EUV and the next option layer the market has not priced

High NA EUV is the second generation of ASML’s extreme ultraviolet lithography platform, offering a wider numerical aperture (0.55 versus 0.33 for current EUV) that enables finer patterning at sub-2nm nodes. In commercial terms, it represents a potential re-rating catalyst analogous to where first-generation EUV stood in approximately 2018: technically proven, commercially unproven, and not yet embedded in consensus earnings models at full adoption rates.

UBS estimates that High NA EUV could deliver 20-40% cost reductions on specific chip fabrication layers versus alternative patterning techniques, with throughput improvements exceeding 100% compared with most alternative approaches.

The current adoption picture requires honest framing. Intel has been publicly identified as an early evaluation customer for High NA tools. TSMC, the most commercially significant potential adopter, has experienced some delays, and no formal TSMC-specific High NA production start date has been publicly confirmed as of May 2026.

Why the TSMC delay is not the signal bears think it is

UBS projects meaningful commercial adoption within approximately two to three years. The delay in TSMC’s specific commitment does not necessarily indicate technology failure; it is consistent with the foundry’s historical pattern of evaluating new lithography platforms over multiple process development cycles before committing to volume production. First-generation EUV followed a similar extended evaluation period before the market priced in its full adoption trajectory.

If the High NA adoption cycle follows even a loosely analogous path to first-generation EUV, investors who wait for a formal TSMC commitment may find themselves buying into a multiple that has already partially re-rated.

Geopolitical risk and China exposure: a permanent discount or a priced-in ceiling?

The bearish argument deserves serious treatment. U.S. and Dutch export restrictions on advanced lithography tools sold to China have introduced a persistent geopolitical risk premium into ASML’s multiple. This is a real overhang that U.S. peers do not carry to the same degree, and dismissing it would be analytically dishonest.

The more precise question is whether this risk functions as an open-ended liability or a bounded discount with a calculable ceiling. China’s contribution to ASML’s revenue represents a known quantity. The downside from further restrictions, while uncertain in timing, operates within a defined revenue range rather than exposing the entire business to systemic risk.

The structural durability of export controls is grounded in national-security law with bipartisan Congressional backing, placing restrictions outside the jurisdiction of trade negotiators and making further liberalisation less likely than headline diplomatic optimism implies; ASML’s approximately 29% China revenue share in 2023 represents the upper bound of a calculable ceiling rather than an open-ended liability.

Why the memory recovery offsets the China ceiling

The memory capex recovery underway in 2025-2026 is concentrated in geographies insulated from China restrictions:

- Samsung (South Korea): Increasing semiconductor capex focused on memory and HBM, responding to AI and server demand recovery.

- SK Hynix (South Korea): Expanding capex to boost HBM and advanced DRAM capacity, with 2025-2026 identified as a significant investment period for AI accelerator supply.

- Micron (United States): Elevating DRAM and HBM investment in support of AI and data-centre demand, with a capex mix shift toward DRAM/HBM over NAND.

UBS characterises ASML as offering the most favourable risk-to-reward profile in the semiconductor equipment sector as of May 2026. The geographic concentration of the three largest memory capex spenders outside China provides a revenue offset that bears on the China question more directly than headline geopolitical risk alone suggests.

The next major ASX story will hit our subscribers first

The UBS thesis in context: what has to be true for the valuation gap to close

The evidence assembled across memory exposure, High NA optionality, and geopolitical risk framing converges on a specific question: under what conditions does the valuation gap close, and under what conditions does it persist?

UBS analyst Francois-Xavier Bouvignies and his team have reinstated ASML as the leading pick in European semiconductors, with a price target of €1,900 (up from €1,600) and EPS estimates of €48.42 for 2027 and €59.73 for 2028, both approximately 15-20% above consensus.

Three conditions must hold simultaneously for the thesis to prove correct:

- Memory capex sustains through 2027-2028: The recovery led by Samsung, SK Hynix, and Micron must extend beyond a single-year rebound into a multi-year investment cycle.

- High NA EUV reaches commercial adoption within two to three years: At least one major foundry customer must commit to volume production on High NA tools within the projected window.

- China-related risk does not escalate beyond currently discounted levels: Export restrictions must remain bounded at approximately current scope rather than expanding to target ASML’s installed DUV base.

The falsification conditions are the mirror image:

- TSMC’s High NA delays extend beyond 2028 with no alternative foundry commitment.

- Memory capex peaks in 2026 rather than sustaining, reducing the intensity tailwind.

- New restrictions target ASML’s DUV installed base or service revenue in China, broadening the risk beyond current scope.

UBS describes ASML as offering the most favourable risk-to-reward profile in the semiconductor equipment sector, a characterisation that carries weight given the firm’s coverage breadth across the space.

These statements reflect UBS analyst projections and are subject to change based on market developments and company performance. Past performance does not guarantee future results.

Monopoly discount or market misread: the case for watching ASML closely through 2027

The more interesting question is not whether ASML is cheap today. It is whether the four forces that collapsed the premium are structurally permanent or cyclically transient. The answer will be written by observable data over the next 18 months.

The scale of the potential re-rating remains substantial. A 10-year historical premium of approximately 84% has compressed to roughly 6-15%. Year-to-date, ASML has returned approximately 40% versus 48-70% for its U.S. peers. The re-rating has not yet begun.

For investors with a 12-to-24-month horizon, the most durable output of this analysis is not a price target but a set of forward catalysts:

- Memory capex guidance in Samsung, SK Hynix, and Micron earnings calls through 2026-2027

- Any formal TSMC commitment on High NA commercial deployment

- U.S. and Dutch policy updates on China export controls affecting lithography

- ASML quarterly order book data, particularly the memory-to-logic booking mix

For investors wanting to stress-test the assumption that memory capex sustains through 2027-2028, our deep-dive into the AI memory re-rating thesis examines the KB Securities analyst case for SK Hynix and Samsung in detail, including the foundry-style long-term supply agreements and the three compounding HBM supply constraints that KB argues could permanently re-rate memory earnings from commodity to infrastructure multiples.

The valuation story will be told in those data points. Knowing which numbers to watch is more durable than any single analyst’s price target.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.