BlackRock Raises AI and Tech Decoupling to Top Risk Tier

Jul 11, 2026

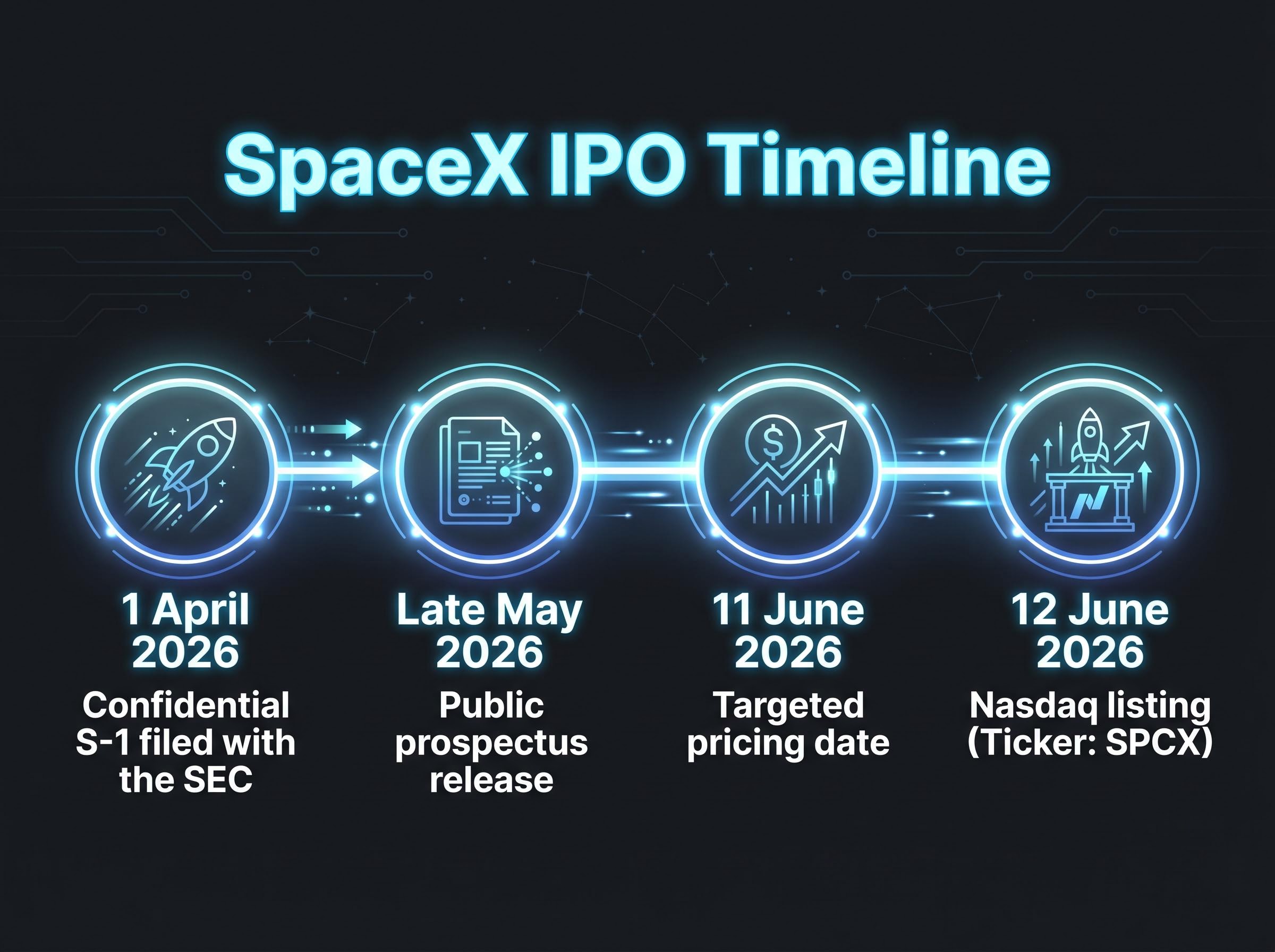

SpaceX‘s IPO prospectus is expected to land today, 20 May 2026, setting the clock on what financial markets are treating as the most consequential public offering in history. With a June 12 Nasdaq debut on the horizon and a valuation target of $1.75 trillion to $2 trillion, the company is preparing to raise more money in a single offering than Saudi Aramco and Alibaba combined. The confidential S-1 was filed with the SEC on 1 April 2026, and once the public prospectus drops, retail and institutional investors will have weeks to form a view before pricing.

What follows covers everything a U.S. investor needs to evaluate before SpaceX shares begin trading: the timeline, the record-breaking scale, the business segments generating revenue, the financial profile the prospectus is expected to disclose, governance and conflict-of-interest risks, and the realistic options for retail participation.

The window is already compressed. SpaceX confidentially filed its draft S-1 registration statement with the SEC on 1 April 2026, and the public prospectus is expected imminently. Morgan Stanley and Goldman Sachs, the lead underwriters, have already conducted testing-the-waters meetings with institutional investors, according to Bloomberg. That means large allocators are forming views right now, ahead of the retail audience.

The four milestones that define the IPO timeline:

12 June 2026 is the anchor date. That is when SPCX is expected to begin trading on Nasdaq, and for most retail investors, it is the first realistic opportunity to own SpaceX equity.

For investors who want to form a view before the stock starts trading, the window between the public prospectus release and pricing is typically short. Early preparation is not optional; it is the price of informed participation.

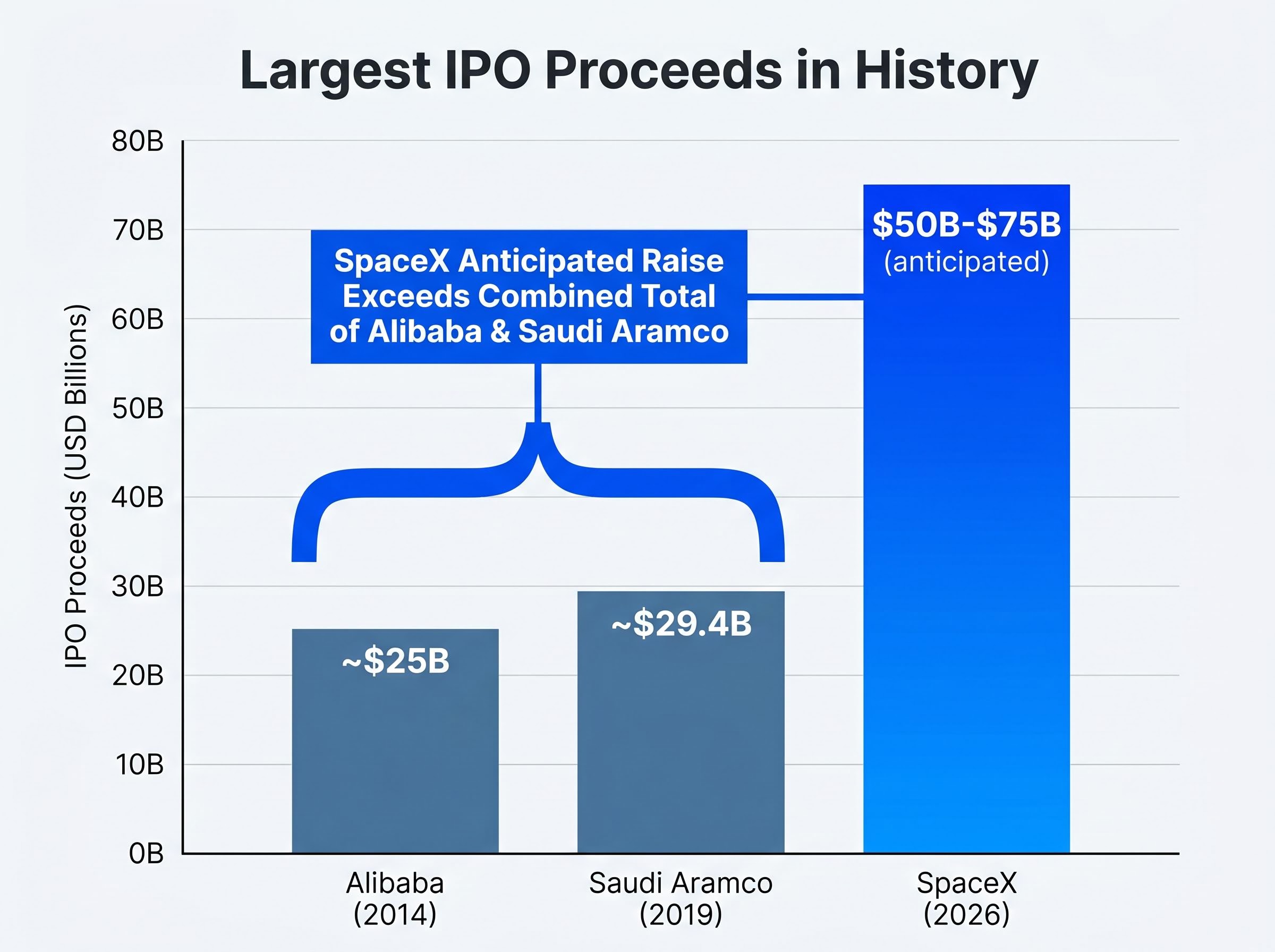

Start with the proceeds. SpaceX is expected to raise $50 billion to $75 billion in its IPO. To put that in context, the prior record belongs to Saudi Aramco, which raised approximately $29.4 billion when it listed in 2019. Before that, Alibaba held the mark at approximately $25 billion from its 2014 NYSE listing.

SpaceX’s anticipated proceeds would exceed both of those combined.

| Company | IPO Year | Proceeds Raised |

|---|---|---|

| SpaceX | 2026 | $50B-$75B (anticipated) |

| Saudi Aramco | 2019 | ~$29.4B |

| Alibaba | 2014 | ~$25B |

SpaceX’s anticipated IPO proceeds of $50 billion to $75 billion would exceed the prior two record holders, Saudi Aramco and Alibaba, combined.

The valuation target of $1.75 trillion to $2 trillion reflects the post-filing anchor reported by Reuters and CNBC through April and May 2026. An offering of this magnitude is not comparable to a standard large-cap IPO. It will require institutional capital at a scale that shapes how much room remains for retail participation, and it will affect index construction and capital flows well beyond the first day of trading.

Tech sector positioning ahead of the listing adds another layer of risk: sell-side consensus forecasts for technology growth have climbed above independent industry-level estimates, Fisher Investments has moved underweight the sector, and global fund managers are most overweight US technology since before the 2021 peak, a backdrop that compounds the capital absorption pressure of a $50-75 billion offering.

Most people know SpaceX for rockets. Falcon 9 launches, Starship test flights, astronauts reaching the International Space Station. That is the visible brand.

The financial engine is something else. Starlink, the company’s satellite internet service, generated $8.2 billion in revenue in 2024, accounting for roughly 63% of SpaceX’s $13.1 billion standalone total. The launch business brought in $4.2 billion from external customers in the same period, but a significant share of the rocket fleet’s capacity never touches an outside customer at all. Of the 134 Falcon launches in 2024, 66% were dedicated to deploying Starlink satellites, missions that generate zero external revenue.

By the end of 2024, Starlink had approximately 4.6 million customers. Subscriber growth and pricing power in that segment are the clearest forward-looking signal in the business.

The three operating segments at a glance:

Investors buying SPCX are not buying a space company alone. xAI, Elon Musk’s artificial intelligence venture, is now consolidated into SpaceX’s group financials. That means its losses flow directly into the numbers shareholders will own.

In 2025, xAI generated an adjusted EBITDA loss of $1 billion to $1.5 billion, according to reporting by The Information’s Cory Weinberg. That single segment is responsible for much of the group’s GAAP net loss, and it raises a question the S-1 risk section will need to address directly: whether SpaceX capital is being allocated to subsidise Musk’s AI ambitions.

Two sets of numbers matter, and confusing them is the most common misreading of SpaceX’s financial profile. The 2024 standalone figures, SpaceX only, show $13.1 billion in revenue. The 2025 consolidated figures, SpaceX plus xAI, show more than $18.5 billion. Revenue did not nearly double organically in one year. The jump reflects the consolidation of xAI into the group.

The private market valuation step-up embedded in the $1.75-2 trillion target is substantial: the last verified secondary market transaction valued SpaceX at approximately $800 billion in December 2025, meaning the IPO price range represents a premium of more than 100% over where informed private buyers transacted less than six months ago.

The deeper tension sits in the capex line. SpaceX spent approximately $21 billion in capital expenditure in 2025, against that $18.5 billion revenue base. The company is spending more than it earns, and this requires continued external funding.

| Segment | 2025 Adjusted EBITDA | Direction | Key Driver |

|---|---|---|---|

| Starlink | More than $7B | Positive | Subscriber growth and pricing |

| Launch | ~$1B | Positive | Falcon 9 reliability |

| xAI | -$1B to -$1.5B | Negative | AI infrastructure spend |

| Group GAAP Net Loss | ~$5B | Negative | Capex and xAI consolidation |

In 2025, SpaceX’s capital expenditure of approximately $21 billion exceeded total revenue of more than $18.5 billion.

The bull case rests on Starlink’s $7 billion in adjusted EBITDA and the growth trajectory that implies. The risk case rests on a $5 billion GAAP net loss, a capex programme that outpaces revenue, and a valuation of $1.75 trillion to $2 trillion that demands sustained high growth to justify. An informed investor needs to hold both of those truths at once.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Elon Musk is the largest shareholder of SpaceX. The exact percentage of his stake has not been publicly confirmed; the definitive ownership table will appear in the public S-1 prospectus. Other known shareholder categories include institutional investors such as Fidelity, sovereign and strategic funds, and early employees and venture capital backers.

The governance question is not about Musk’s stake alone. It is about the four entities he simultaneously leads: SpaceX, xAI (now consolidated into SpaceX), Tesla, and X (formerly Twitter). Each creates a potential conflict around capital allocation, time, and decision-making. The absorption of xAI into SpaceX’s financial structure has already sharpened this concern.

Analysts broadly anticipate founder-friendly governance provisions, potentially including dual-class shares or super-voting arrangements, though no prospectus language has been publicly confirmed. Four disclosures in the public S-1 will matter most:

Founder governance risks at high-profile tech IPOs have a documented track record of producing valuation discounts at listing; the OpenAI experience, where an unresolved conflict-of-interest investigation is being weighed against an $852 billion private valuation, provides a directly comparable stress test for how markets price CEO-level governance uncertainty into an offering of this scale.

Intensive SEC review is expected given the offering’s scale, SpaceX’s national security profile as a U.S. launch provider and Starshield contractor, and Musk’s history with securities regulators (particularly at Tesla). Foreign ownership limits and potential national security scrutiny of certain IPO allocations are relevant given SpaceX’s role as a defence contractor.

No specific SEC enforcement action targeting the SpaceX IPO has been reported as of 20 May 2026. The scrutiny expected is an intensive standard review, not an unusual enforcement posture.

No named retail allocation programme has been confirmed by SpaceX, Morgan Stanley, or Goldman Sachs as of 20 May 2026. The primary offering is expected to be heavily oversubscribed and dominated by institutional allocations. That is the honest starting point.

Three pathways exist, ranked from most to least accessible for a typical U.S. retail investor:

For most U.S. retail investors, SPCX on Nasdaq after 12 June is the realistic and most accessible entry point.

The prospectus expected today is not the finish line. It is the starting point for serious evaluation.

Starlink‘s adjusted EBITDA of more than $7 billion anchors the bull case. Capital expenditure of approximately $21 billion exceeding revenue anchors the risk case. The gap between those two realities is where the investment decision lives.

The public S-1 will resolve the open questions: Musk’s exact ownership stake, the share class and voting structure, full related-party transaction disclosures, and segment-level financial detail. Four sections of the prospectus deserve attention first:

Pricing is targeted for 11 June 2026. First trading on 12 June 2026. The weeks between now and then are the preparation window.

For investors who want a structured framework before the document lands on SEC EDGAR, our dedicated guide to reading the S-1 prospectus walks through the specific sections that matter most, including the risk factors, use of proceeds, and ownership table, and flags the valuation step-up from the last verified secondary market transaction that investors will need to reconcile.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The SpaceX IPO is the public offering of SpaceX shares on the Nasdaq stock exchange, targeted for June 12, 2026 under the ticker SPCX, with pricing expected on June 11, 2026.

SpaceX is anticipated to raise between $50 billion and $75 billion in its IPO, which would exceed the combined proceeds of the previous two record holders, Saudi Aramco (approximately $29.4 billion in 2019) and Alibaba (approximately $25 billion in 2014).

For most U.S. retail investors, the most accessible option is to purchase SPCX shares on the Nasdaq open market after the stock begins trading on June 12, 2026, using any standard U.S. brokerage account.

Starlink is SpaceX's satellite internet service and its primary financial engine, generating $8.2 billion in revenue in 2024 (roughly 63% of SpaceX's standalone total) and more than $7 billion in adjusted EBITDA in 2025.

Key risks include SpaceX's capital expenditure of approximately $21 billion in 2025 exceeding its total revenue of more than $18.5 billion, a group GAAP net loss of approximately $5 billion, losses from the consolidated xAI division, and a valuation target that represents more than a 100% premium over the last verified private market transaction.