Aristocrat Leisure’s ALL share price has declined roughly 9.6% since the start of 2025, even as the company’s underlying revenue has compounded at 11.7% annually over the past three years. That divergence between operational momentum and market pricing is the kind of signal that forces a direct question: is the discount a warning about deteriorating fundamentals, or has the market repriced a quality compounder without a corresponding deterioration in its earnings base?

As of 19 May 2026, ALL trades at a trailing price-to-sales multiple of approximately 4.73x, sitting around 16% below its five-year historical average of 5.64x. The pullback reflects a mix of macro-driven multiple compression, sector rotation away from consumer discretionary names, and specific investor uncertainty about the digital and real-money gaming (RMG) pivot. What follows is a structured examination of what is driving the valuation gap, how to interpret a price-to-sales discount correctly, what the company’s two revenue engines look like in practice, and what risk factors demand attention before any investment conclusion is drawn.

What the ALL share price decline actually tells you

ALL has pulled back from a late-2025 trading range of approximately A$62-72 to around A$51.74 as of 19 May 2026. That represents a material decline. The instinct for many investors is to assume that a falling share price signals deteriorating fundamentals. In this case, the diagnosis points elsewhere.

A$51.74 on 19 May 2026. Down approximately 9.6% from the start of 2025, while three-year annualised revenue growth sits at 11.7%.

The dominant driver of ALL’s weakness has been valuation multiple compression, not earnings erosion. The company’s FY24 normalised net profit after tax grew approximately 16% year-on-year. Revenue continued to expand across land-based and digital segments. What changed was the price investors were willing to pay per dollar of that revenue.

Three identifiable forces have compressed the multiple:

- Macro and rate environment: Higher-for-longer interest rate expectations through 2025 drove a broad de-rating of growth-adjacent and consumer discretionary names across the ASX.

- Sector rotation: The ASX Consumer Discretionary Index (XDJ) returned just 0.95% per year over the past five years, compared with 4.12% for the ASX 200, placing ALL in a structurally underperforming sector basket.

- Digital and RMG uncertainty: Investor scepticism about the pace and profitability of Aristocrat’s real-money gaming pivot and its Pixel United digital portfolio weighed specifically on the stock’s forward multiple.

Consumer discretionary underperformance on the ASX is not incidental to Aristocrat’s de-rating; the XDJ has returned just 0.90% annualised over five years against 4.21% for the broader ASX 200, a gap driven by rate cycle mechanics that compress household spending capacity and push institutional capital toward defensive and industrial allocations.

Understanding that distinction matters. Investors who conflate a falling share price with deteriorating fundamentals risk selling a quality franchise at exactly the point where valuations begin to look more favourable.

When big ASX news breaks, our subscribers know first

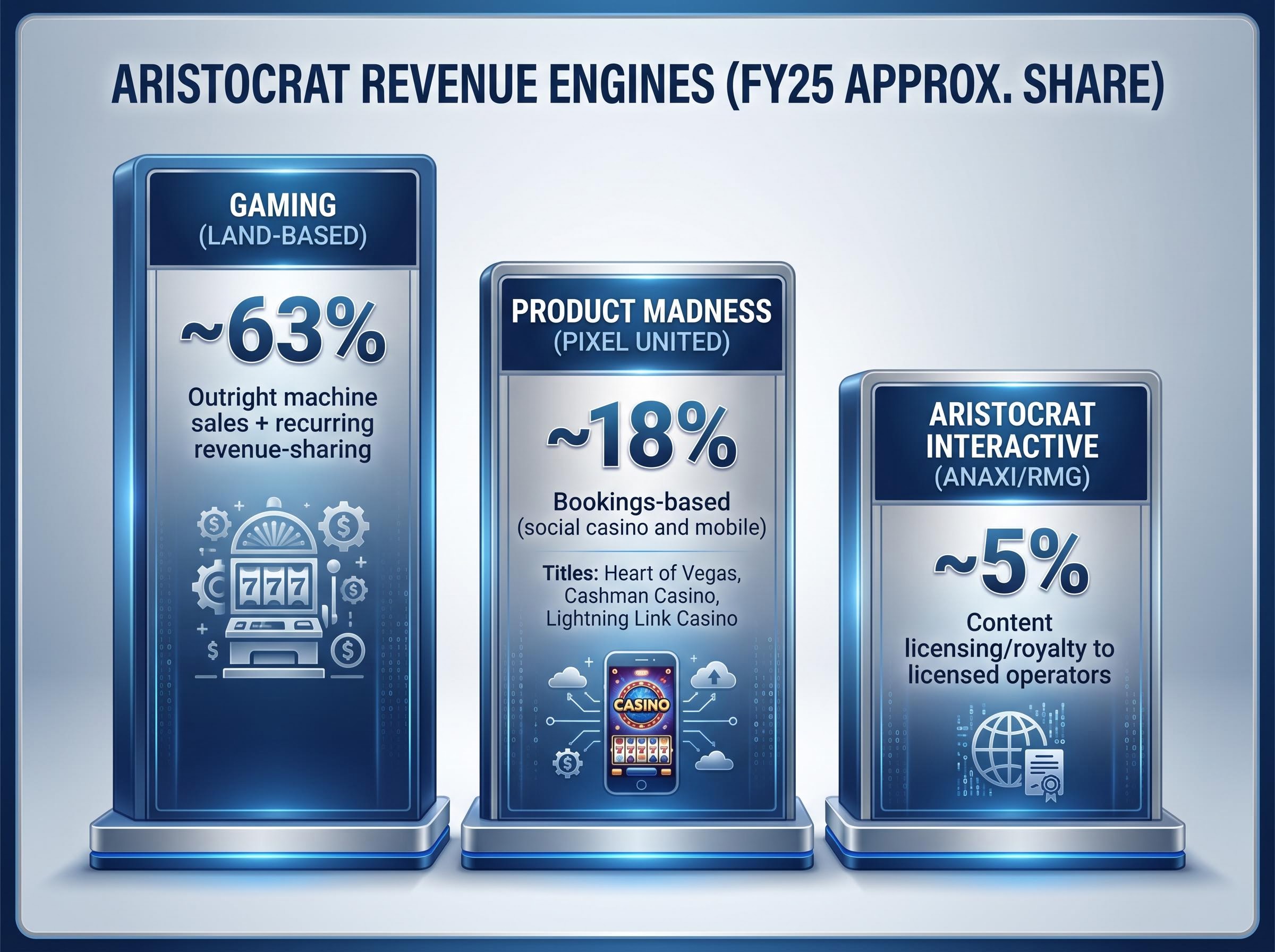

How Aristocrat actually makes its money

Before evaluating whether the discount is justified, investors need a clear picture of what they are buying. Aristocrat operates two distinct revenue engines, each with different margin profiles, growth trajectories, and risk characteristics.

| Segment | FY25 Revenue Share (Approx.) | Primary Revenue Mechanism |

|---|---|---|

| Gaming (Land-Based) | ~63% | Outright machine sales + recurring revenue-sharing arrangements |

| Product Madness (Pixel United) | ~18% | Bookings-based (social casino and mobile titles) |

| Aristocrat Interactive (Anaxi/RMG) | ~5% | Content licensing/royalty to licensed operators |

Land-based gaming: machines plus recurring revenue

The Gaming segment generates nearly two-thirds of group revenue. Venues choose between purchasing machines outright or entering revenue-sharing (gaming operations) arrangements where Aristocrat retains ownership and receives a percentage of net gaming revenue over time.

The revenue-sharing model is where Aristocrat’s earnings stability lives. It generates recurring income that is independent of lumpy machine replacement cycles, and it has performed well across North American and ANZ markets. Strong demand for premium gaming operations continued through 2025 trading updates.

Digital: social casino, mobile, and real-money gaming

Pixel United operates social casino titles, including Heart of Vegas, Cashman Casino, and Lightning Link Casino, alongside casual mobile games. Revenue is bookings-based, meaning it depends on in-app purchases and engagement metrics rather than hardware sales.

Anaxi is Aristocrat’s RMG content platform, supplying the company’s slot intellectual property to licensed online casino operators in regulated jurisdictions. It does not operate a gambling platform directly. As of FY24 materials, Anaxi remained in investment and build-out mode, contributing modest revenue but serving as a strategic foundation for future growth. This distinction is relevant to how investors price the digital opportunity: Anaxi’s value depends on regulatory pathways and operator adoption, not on Aristocrat running its own gambling operations.

Reading the 16% P/S discount: a methodology note for retail investors

Price-to-sales (P/S) measures a company’s market capitalisation relative to its revenue. It tells investors how much the market is paying for each dollar of sales the business generates. For a company like Aristocrat, it functions as a secondary cross-check rather than a primary valuation tool.

The current trailing P/S of approximately 4.73x sits roughly 16% below the five-year average of 5.64x. That gap looks like a signal. Whether it is a useful one depends on understanding what can cause it and what it leaves out.

- What a P/S discount means: The market is assigning a lower valuation per dollar of revenue than it has historically. This can reflect genuine deterioration, or it can reflect temporary sentiment-driven compression.

- What can cause it: A P/S ratio compresses when the share price falls (reducing the numerator), when revenue grows (expanding the denominator), or when both occur simultaneously. For ALL, both forces are operating: the share price has declined while revenue has continued to grow at 11.7% annually.

- What additional analysis it demands: P/S ignores profitability, margin mix between segments, and capital allocation quality. A company investing heavily in a low-margin digital expansion (as Aristocrat is doing with Anaxi) may warrant a lower P/S than one generating the same revenue from a higher-margin, capital-light model. More sophisticated approaches, including discounted cash flow analysis and EV/EBITDA comparisons, are needed for a complete investment case.

The trailing P/S of 4.73x sits approximately 16% below the five-year average of 5.64x, according to market data as of 19 May 2026.

The metric is a prompt for deeper questions, not a self-contained buy signal.

For investors who want to work through the mechanics in more depth before drawing a conclusion on ALL, our dedicated guide to price-to-sales ratios for ASX growth stocks walks through how recurring revenue structures, reinvestment cycles, and margin mix each affect what a sustainable P/S multiple should look like for a platform business.

The bull and bear case for ALL at current prices

The investment debate around ALL at these levels carries genuine tension on both sides. Neither case is a straw man.

Bull case:

- Morgan Stanley retained an Overweight rating (as of H2 2025 coverage), describing Aristocrat’s valuation as “undemanding relative to growth” and citing the strength of its intellectual property portfolio.

- Macquarie maintained an Outperform rating, labelling Aristocrat a “preferred exposure to global gaming.”

- FY24 normalised NPAT grew approximately 16% year-on-year, demonstrating that earnings power has not deteriorated.

- North American land-based momentum remains strong, supported by premium gaming operations and machine demand.

- Anaxi’s RMG optionality offers long-term upside if regulatory pathways continue to open across US states.

- The current dividend yield of approximately 1.5% exceeds the five-year average of roughly 1.3%, suggesting the market has priced in caution.

The buyback expansion to $2.5 billion extended through May 2027, announced alongside the HY26 results, operates alongside the interim dividend rather than in lieu of it, with management deploying both income and capital return levers simultaneously as constant-currency NPAT growth of 17.1% demonstrated that the operational earnings base remains intact despite AUD/USD translation drag.

Bear case:

- The de-rating may be partly structural rather than cyclical, reflecting higher competitive intensity in mobile gaming that compresses Pixel United’s margin potential.

- Elevated user-acquisition costs across the social casino and casual mobile industry could cap digital segment profitability regardless of revenue growth.

- Anaxi remains in investment and build-out mode, with the pace and profitability of RMG expansion uncertain and dependent on state-by-state US legalisation timelines.

- Management’s commitment to “disciplined investment” in digital does not resolve the question of when that investment converts to margin-accretive returns.

Management’s stated US$1 billion Interactive Revenue Target by FY29 sets a concrete yardstick for assessing whether Anaxi’s investment phase is on track, with recurring revenue already exceeding 70% of group revenue and group EBITA margin expanding from 28.6% in FY22 to 36.9% in HY26, providing the margin baseline against which RMG-phase returns can eventually be benchmarked.

The unresolved question at the centre of this debate is specific: whether incremental digital and RMG investment will convert to margin-accretive revenue growth within a timeframe that justifies current multiples. Investors’ own risk tolerance and time horizon determine which side of that question they land on.

Risks that do not show up in the P/S ratio

A single valuation metric captures none of the qualitative risks that could widen rather than close the discount. Three categories warrant monitoring.

- Regulatory risk: Australian Federal and state regulators have continued tightening gambling advertising standards and harm minimisation requirements since January 2024. These measures can constrain customer acquisition channels for operators licensing Aristocrat content and increase compliance costs for land-based venues. In North America, Anaxi’s growth runway depends on continued state-by-state iCasino legalisation, a process that remains uneven and subject to political reversal.

- Platform and distribution risk: Pixel United and Anaxi depend on Apple App Store and Google Play for distribution. Changes to platform fees, Apple’s App Tracking Transparency and IDFA policies, and content rules around gambling-adjacent apps represent material risks that sit outside Aristocrat’s direct control.

- Competitive dynamics: In both social casino and casual mobile, elevated user-acquisition costs and continuous content refresh requirements have been noted across the industry since 2024. Aristocrat has responded with portfolio optimisation, pruning underperforming titles, but margin pressure is an industry-wide condition, not a company-specific one.

The Australian gambling reforms published by the Department of Social Services in April 2026 introduced new harm minimisation measures covering advertising restrictions and expanded financial counselling services, adding compliance obligations that affect the operating environment for land-based venues licensing Aristocrat content.

Regulatory uncertainty in real-money gaming is a sector-wide investor concern affecting all participants in the space, not a risk specific to Aristocrat alone.

These risks are precisely the ones most likely to surprise investors who rely on headline valuation metrics. Each represents a concrete monitoring point: regulatory news flow in key US states, platform policy changes from Apple and Google, and quarterly trends in user-acquisition costs across digital segments.

A 16% discount to history is a prompt, not a conclusion

The core tension in Aristocrat’s investment case is clear. Solid land-based earnings, a proven 11.7% three-year annualised revenue growth record, and a broadly constructive broker consensus (Overweight from Morgan Stanley, Outperform from Macquarie) sit on one side. On the other: genuine uncertainty in digital execution, RMG regulatory timing, and the margin trajectory of a business investing heavily in a segment that contributes just 5% of group revenue.

A trailing P/S of 4.73x against a five-year average of 5.64x creates the conditions for an investment opportunity. It does not constitute one on its own. The 9.6% share price decline since the start of 2025 has occurred within a consumer discretionary sector that has itself underperformed the ASX 200, adding a macro headwind that has little to do with Aristocrat’s specific fundamentals.

Before treating the valuation gap as actionable, investors could investigate:

- Profitability trends by segment: Are land-based margins stable, and is digital margin compression accelerating or stabilising?

- RMG revenue contribution milestones: What revenue and margin targets has management set for Anaxi, and is the trajectory tracking to plan?

- Regulatory news flow: Which US states are advancing iCasino legalisation, and what is the realistic timeline for Anaxi’s addressable market to expand?

- User-acquisition cost trends: Are quarterly trends in Pixel United’s customer acquisition costs improving, or is competitive intensity compressing returns further?

These questions convert a headline valuation discount into a structured due-diligence process. The discount may prove to be an entry point, or it may reflect a market that has correctly identified structural headwinds that a single ratio cannot capture.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.