SK Hynix’s $26.5B Nasdaq Listing Shatters ADR Demand Records

11 hrs ago

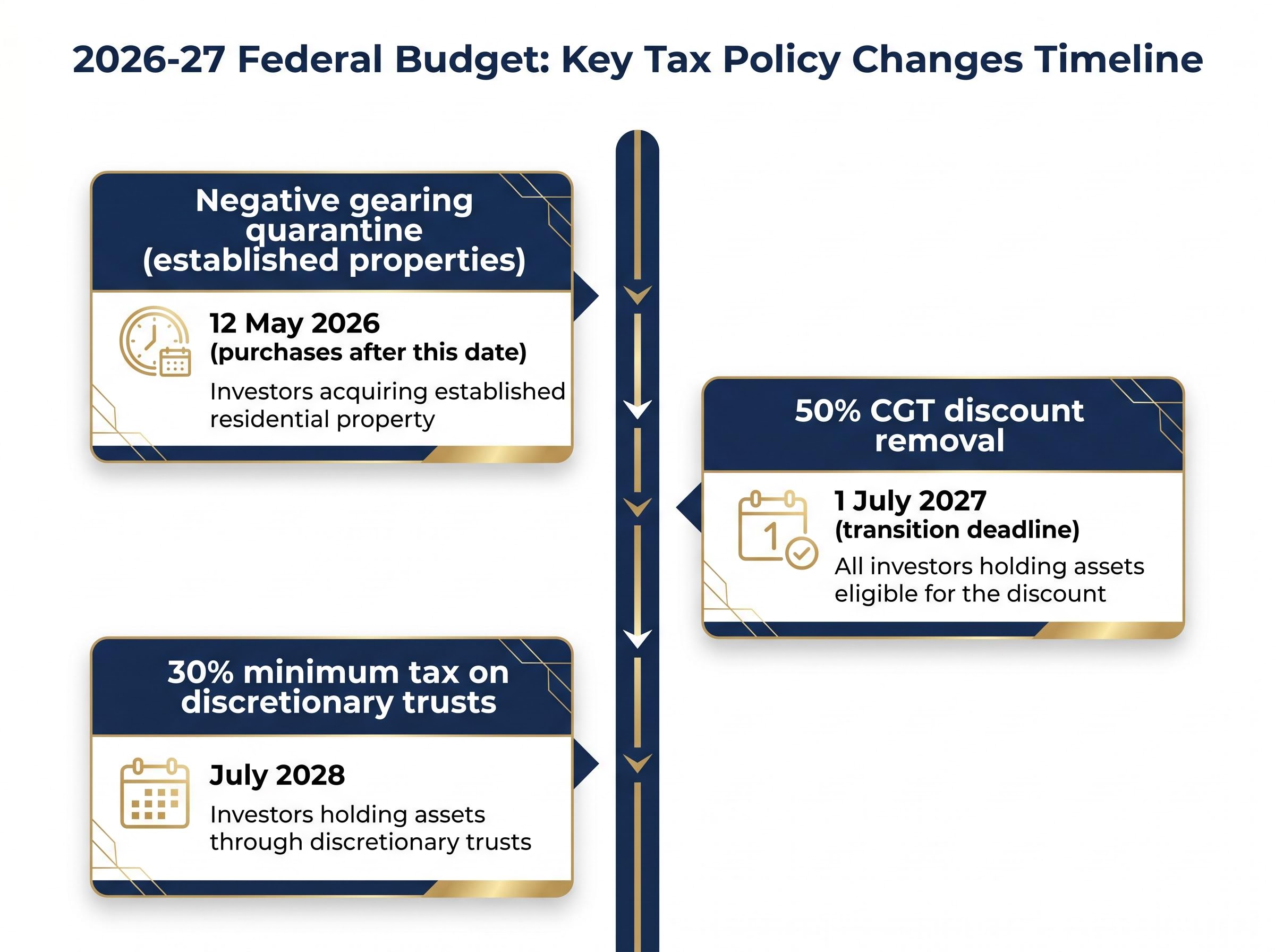

On 12 May 2026, the Australian government announced the end of a tax framework that has shaped property investment strategy for 27 years. The 50% capital gains tax (CGT) discount is being removed. Negative gearing on established properties is being quarantined. And the clock is already running.

The 2026-27 Federal Budget introduced the most significant restructuring of Australian investment taxation since the CGT discount was first established in 1999. For property investors, these are not abstract policy shifts. They alter the after-tax economics of holding, selling, and acquiring real estate in ways that require concrete decisions before 1 July 2027.

What follows breaks down exactly what has changed, how each measure works mechanically, what the deadlines are, and what structural implications follow for investors currently holding or considering established residential property.

The budget introduced three distinct instruments that compound on each other. Treating them as a single policy change is the fastest way to misread the timeline.

The negative gearing quarantine applies to established residential properties purchased after 12 May 2026; it is already in effect. The CGT discount removal carries a transition deadline of 1 July 2027, giving investors a window to adjust positions. A third measure, the 30% minimum tax on discretionary trusts, takes effect from July 2028.

Each operates on a different timeline, affects a different investor profile, and demands a different response.

| Policy change | Effective date | Who is affected |

|---|---|---|

| Negative gearing quarantine (established properties) | 12 May 2026 (purchases after this date) | Investors acquiring established residential property |

| 50% CGT discount removal | 1 July 2027 (transition deadline) | All investors holding assets eligible for the discount |

| 30% minimum tax on discretionary trusts | July 2028 | Investors holding assets through discretionary trusts |

The distinction between date-triggered and transition-window changes is where most early coverage has generated confusion. The sections that follow address each mechanism in turn.

In 1999, the federal government replaced cost base indexation with a simpler mechanism: hold an asset for longer than 12 months, and only 50% of the capital gain is included in taxable income. The remaining half is disregarded entirely.

The design was deliberate. It rewarded patience. An investor who bought a Sydney apartment in 2002 and held it for two decades paid tax on only half the nominal gain, regardless of how much of that gain was attributable to inflation versus real appreciation. For high-growth markets, the discount became the single largest driver of after-tax returns.

AHURI modelling on negative gearing and CGT reform found that investment property loan growth driven by these concessions has historically crowded out first-home buyers, with the financial benefits heavily skewed toward higher-income investors, providing the academic foundation for the government’s argument that the existing framework required structural correction.

Domain Research projects record-high home prices in Sydney, Brisbane, and Adelaide by the end of FY2026. Commonwealth Bank’s pre-budget forecast estimated national dwelling price growth of approximately 5% for 2026. In practical terms, this means the accumulated unrealised gains sitting inside investor portfolios, particularly in Sydney and Melbourne, are at or near historic peaks.

The replacement framework taxes investors on real gains above inflation rather than nominal gains. Cost base indexation adjusts the original purchase price using the Consumer Price Index (CPI) before the gain is calculated, so only the portion of appreciation exceeding general price-level changes is subject to tax. A 30% minimum tax floor applies regardless of the indexation outcome.

Consider a simplified example:

For long-hold investors, particularly those with pre-2000 acquisitions where decades of nominal appreciation have accumulated, the difference between these two models can represent tens or hundreds of thousands of dollars in additional tax liability. Understanding the mechanism is the prerequisite for any restructuring decision before 1 July 2027.

City-level variation in CGT outcomes is material: PropTrack analysis finds Melbourne investors are more likely to benefit from the new indexation model than Brisbane investors, reflecting the different inflation-adjusted growth trajectories of each market over the past decade and producing meaningfully different after-tax liability profiles for investors in otherwise comparable positions.

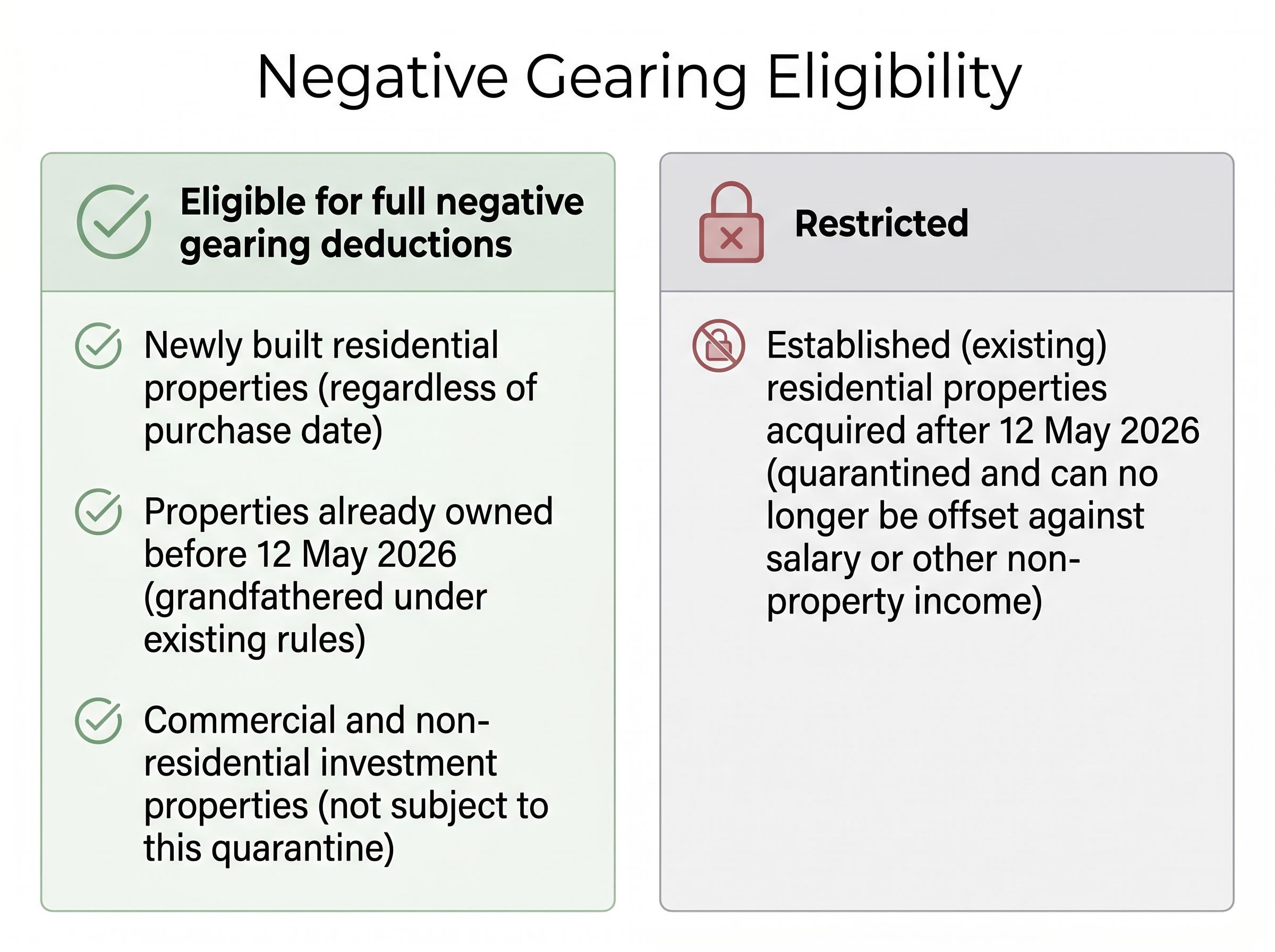

Negative gearing occurs when rental income on an investment property is less than the total costs of holding it (mortgage interest, maintenance, management fees), generating a loss. Under the previous framework, that loss could be offset against salary and other income, reducing the investor’s overall tax bill.

The quarantine draws a clear line. Here is where it falls:

What remains eligible for full negative gearing deductions:

What is now restricted:

The grandfathering provision is the single most practically important detail for existing investors. Those who already hold established residential investment properties are not immediately affected. The restriction applies only to new acquisitions of established stock from 12 May 2026 onward.

Housing Industry Association (13 May 2026): HIA stated that restricting negative gearing to new builds “doesn’t increase the supply of new homes,” warning of reduced commencements of approximately 22,700 fewer homes over five years.

Industry modelling from REIA, conducted by Qaive and Tulipwood, estimates approximately 25,500 fewer homes built over the same period. Both figures point to a supply-side consequence that may offset the policy’s intended demand-side effects.

Residential developers on the ASX, including Stockland, Mirvac, and Lendlease, are flagged by multiple major bank analysts as potential structural beneficiaries of the negative gearing quarantine, because the policy redirects investor demand away from established stock and toward new builds, which remain eligible for full negative gearing deductions.

The formal transaction data has not arrived yet. But the signals have.

Commonwealth Bank’s updated post-budget housing outlook, published on 13 May 2026, modelled a price downside risk of approximately 3% nationally. More notably, CBA explicitly identified shifts in investor sentiment as a near-term risk capable of amplifying price effects beyond that baseline scenario.

CBA flagged “shifts in investor sentiment” as a key factor that could push price declines beyond the modelled 3% downside, noting that behavioural responses to tax policy changes have historically moved faster than the policy implementation itself.

In the week following the budget, multiple broker and analyst sources reported an immediate pull-back in established-property investor enquiries. The pattern was consistent across commentary published between 13 and 18 May 2026, though it remains anecdotal rather than statistically confirmed.

What is not yet available:

The first reliable data is expected in subsequent months. In the interim, industry modelling provides the clearest quantitative signals:

Early market signals matter because they indicate where investor sentiment is moving before official data confirms it, giving attentive investors a window to act before consensus repositioning is complete.

The CGT discount removal does not stop at property. The same 50% discount has been the foundation of retail equity investment strategy since 1999, rewarding investors who held shares for longer than 12 months with a halved tax liability on gains. Its removal reshapes the incentive structure for equities as directly as it does for real estate.

Without the discount, the tax benefit of holding an asset for 13 months versus 11 months disappears. The likely consequence is higher portfolio turnover and shorter average holding periods, as the friction cost of selling and redeploying capital falls relative to the old framework. For growth-oriented investments, where returns are concentrated in capital appreciation rather than income, the after-tax arithmetic deteriorates meaningfully.

The rotation is already being mapped. Growth-oriented sectors, including technology, biotechnology, and early-stage resources, lose the historical tax advantage that made patient capital accumulation through price appreciation the optimal strategy. Sectors that generate consistent income through dividends, particularly those with established franking credit histories, become relatively more attractive on an after-tax basis.

Franked dividend income becomes structurally more attractive on an after-tax basis when the alternative, capital appreciation, is taxed more heavily, and the major banks and diversified miners carry a specific tailwind from this shift because their return profiles are concentrated in fully franked distributions rather than price appreciation.

| Sector category | Post-2027 positioning | Mechanism |

|---|---|---|

| Technology, biotech, early-stage resources | Disadvantaged | Returns concentrated in capital gains; loss of 50% discount increases effective tax rate on appreciation |

| Banks, mining majors, mature industrials | Advantaged | Returns concentrated in franked dividends; relative after-tax attractiveness increases as capital gains are taxed more heavily |

Vantage Markets analyst Hebe Chen characterised the anticipated shift toward yield over growth as “structurally embedded rather than cyclical,” noting that the policy change permanently alters the tax calculus rather than creating a temporary dislocation.

Property investors reviewing their portfolios ahead of 2027 are frequently equity investors as well. The same tax logic that reshapes property decisions reshapes equity allocation, making this reallocation relevant well beyond the housing market.

The transition window closes on 1 July 2027. Accounting for valuation lead times, professional adviser capacity, and the legislative clarification timeline, that window is narrower than it appears.

The most important near-term action is obtaining independent market valuations on long-held assets. Establishing a cost base at 2027 market values is the mechanism for sheltering decades of historical appreciation under existing rules before the new framework applies. Without a defensible valuation, the interaction between accumulated gains and the new indexation model may produce significantly higher liabilities than necessary.

This is particularly urgent for assets acquired before 1985 (pre-CGT assets), where the interaction with the new framework may produce unusually large liability resets given the absence of an original cost base record.

The new framework brings a category of holdings into scope that the CGT regime has never previously touched: pre-1985 assets, which have sat entirely outside capital gains tax since the system was introduced, will be subject to the new rules for the first time, creating liability exposure for a group of long-term investors who may have assumed they were permanently exempt.

The recommended sequence:

No exposure draft legislation for the CGT or negative gearing quarantine measures has been released as of 19 May 2026. The ATO “New legislation” section and the Treasury Legislation page are the primary monitoring points for rule clarification as the legislative pathway progresses.

The ATO’s negative gearing and CGT reform guidance published on 12 May 2026 confirms that cost base indexation and the 30% minimum tax floor will replace the 50% discount for assets disposed of from 1 July 2027, making it the definitive reference point as exposure draft legislation is developed.

Vantage Markets analysis describes the era of tax-advantaged holding as a default strategy as closing, with the new environment rewarding precise structuring, timing, and execution. Investors who wait until late 2026 to begin this process may find their options materially narrowed.

The two tracks of this overhaul operate on different timelines. The negative gearing quarantine is already in effect for established properties acquired after 12 May 2026. The CGT discount window remains open until 1 July 2027, but the transition period is finite and the professional advisory pipeline is likely to tighten as the deadline approaches.

This is not a temporary adjustment. It is a deliberate dismantling of the tax architecture that made buy-and-hold property the default wealth-building strategy for Australian retail investors since 1999. The structural logic runs through equities as well as real estate, reshaping the incentive framework for how capital is deployed, held, and realised.

Formal legislative detail is still to come. Investors who act on valuations and portfolio reviews now will be better positioned to adapt once the rules are confirmed than those who wait for certainty that may arrive later than expected.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Readers should consult a registered tax adviser or financial planner to assess their specific circumstances before the 1 July 2027 deadline.

The 2026-27 Federal Budget introduced three key changes: the removal of the 50% capital gains tax discount (effective 1 July 2027), the quarantine of negative gearing deductions on established residential properties purchased after 12 May 2026, and a 30% minimum tax on discretionary trusts taking effect from July 2028.

From 1 July 2027, investors will no longer be able to halve their taxable capital gain on assets held for more than 12 months; instead, gains will be calculated using cost base indexation adjusted for CPI, with a 30% minimum tax floor, which can result in significantly higher tax liabilities for long-hold investors.

No, the negative gearing quarantine only applies to established residential properties purchased after 12 May 2026; properties already held before that date are grandfathered under the existing rules and remain fully eligible for negative gearing deductions.

Investors should obtain independent market valuations on all long-held investment properties to establish a defensible cost base, identify any pre-1985 assets newly brought into scope, review growth-asset exposure across property and equities, and monitor the ATO and Treasury Legislation pages for exposure draft legislation.

The removal of the 50% CGT discount reduces the tax advantage of buy-and-hold growth investing in equities, making income-focused sectors such as major banks and mining companies with fully franked dividends relatively more attractive on an after-tax basis compared to growth sectors like technology and biotechnology.