The Memo That Halved Meta’s AI Infrastructure Cost Estimate

3 hrs ago

Australia’s most significant rewrite of investment tax rules in nearly three decades landed in a budget dominated by property headlines on 12 May 2026. The consequences, however, fall hardest on equity investors who have not yet connected the policy to their ASX portfolios. The 2026-27 Federal Budget confirms the removal of the 50% capital gains tax discount for individuals, trusts, and partnerships from 1 July 2027, replacing it with CPI indexation of the cost base and a 30% minimum tax on real gains. That mechanism shift changes the after-tax return profile of every growth-oriented ASX holding outside superannuation. What follows maps the structural consequences for Australian equity portfolios: which sectors face compression, which benefit, how investor behaviour will shift, and what the 13-month transition window before July 2027 means for portfolio decisions.

Public attention has centred on what the capital gains tax changes mean for residential property. The equity-market implications are at least as significant, and less well understood.

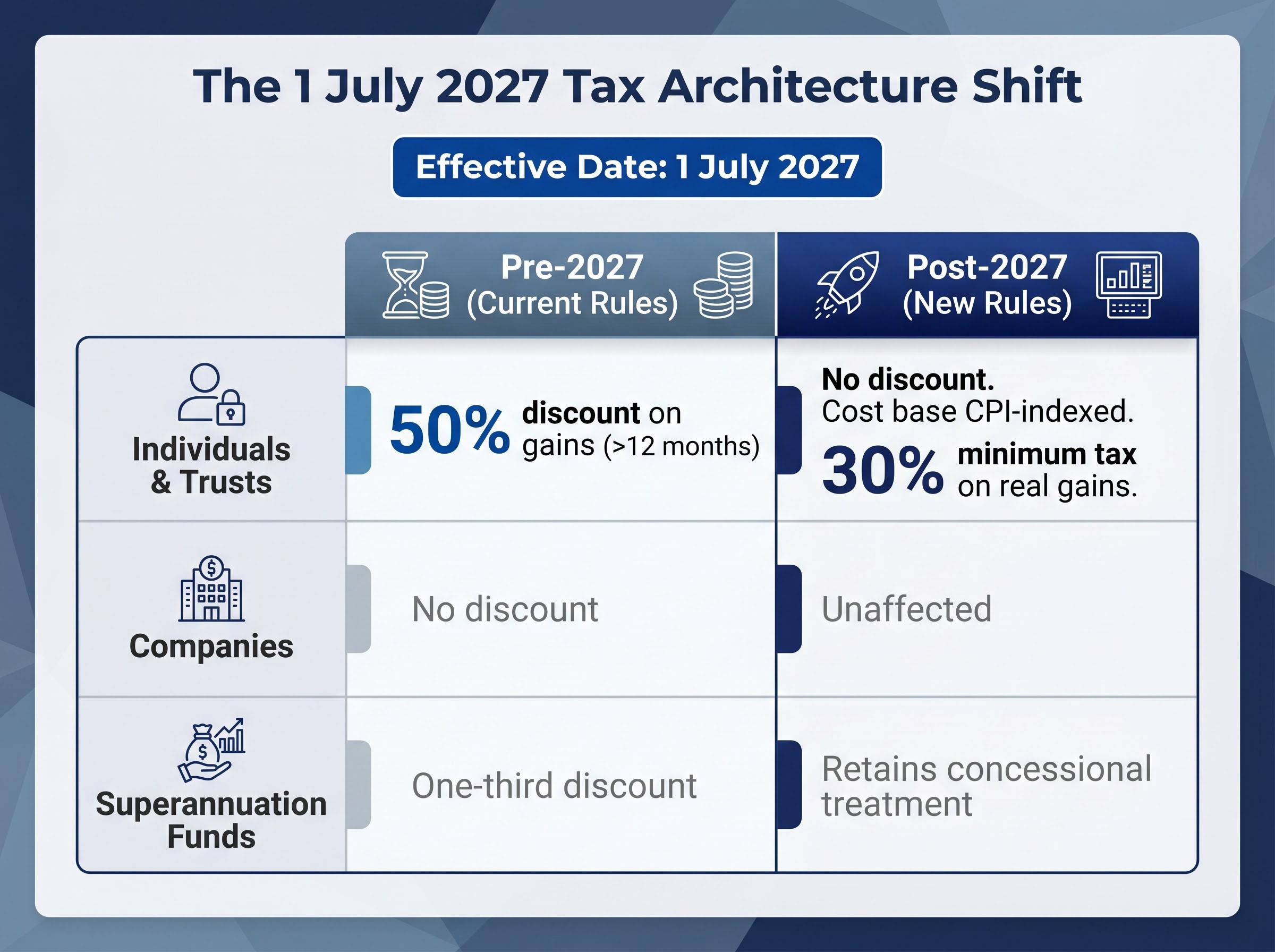

The 50% CGT discount, introduced on 21 September 1999 under the Howard Government, will cease to apply from 1 July 2027 for individuals, trusts, and partnerships holding assets for more than 12 months. In its place, the cost base of an asset will be indexed to CPI, and a 30% minimum tax will apply to the resulting real gain. The model partially reverts to the pre-1999 indexation framework, though the minimum tax floor is a new structural addition absent from the earlier regime.

CGT indexation mechanics interact with holding period and the inflation environment in ways the 30% minimum floor alone does not capture: investors who accumulated positions during the high-inflation years of 2022-2024 may face a lower effective tax burden under indexation than under the flat 50% discount, while those with long-held gains from the low-inflation era face the greatest risk of a higher bill.

The Treasurer’s 2026-27 Budget announcement confirms the removal of the 50% CGT discount and its replacement with CPI indexation of the cost base plus a 30% minimum tax on real gains, with an effective date of 1 July 2027 applying to individuals, trusts, and partnerships.

The before-and-after mechanics break down as follows:

The two anchor facts: The effective date is 1 July 2027. The 30% minimum tax floor on real gains is the new structural baseline for every personal-name and trust-held equity position.

Gains accrued on assets held before 1 July 2027 retain access to the existing discount rules on those pre-reform gains. The reform applies prospectively to new gains only.

The practical implication is that holdings straddling the 1 July 2027 date will require apportionment calculations, splitting the gain into a pre-reform component (eligible for the old discount) and a post-reform component (subject to the new indexation and minimum tax rules). Investors with long-held positions face the most complex calculations.

The 50% CGT discount was not merely a tax concession. It was the structural foundation of a specific investment philosophy that shaped an entire generation of Australian retail portfolios.

The 12-month holding threshold created a rational, tax-driven incentive to hold growth assets indefinitely, accumulating unrealised gains rather than triggering a taxable event. For a top-marginal-rate individual, the effective tax rate on a long-term capital gain dropped from 47% (including the Medicare levy) to roughly 23.5% under the discount. That differential made deferral the optimal default.

From 1 July 2027, that incentive disappears. With no discount available, the calculus of when to realise gains changes at its foundation. Three distinct behavioural shifts follow:

Trusts lose the discount simultaneously with individuals. This is significant because a large subset of retail ASX investors use discretionary trusts for portfolio management, and those structures now face the full impact of the reform.

A second layer of pressure arrives 12 months later: the July 2028 minimum tax on discretionary trusts adds further structural change to the after-tax economics of trust-based investing. The compounding of both measures within a 12-month window concentrates the adjustment for this cohort.

A trust rollover relief window running from 1 July 2027 gives trustees three years to restructure without triggering adverse CGT events, a concession that partially softens the compounded effect for discretionary trust investors facing both the discount removal and the July 2028 minimum tax within a 12-month period.

With capital gains losing their discount, franking credits become the most tax-efficient return mechanism available to personal-name and trust-held equity portfolios. Understanding why requires a brief framework on how the imputation system works.

When an Australian company pays tax on its profits at the 30% company tax rate, it can attach franking credits to dividends paid from those profits. Those credits represent tax already paid at the company level. When a shareholder receives a fully franked dividend, the franking credit offsets their personal tax liability on that income, preventing the same profit from being taxed twice. For a top-marginal-rate individual, the effective after-tax return on a fully franked dividend is materially different from the after-tax return on a realised capital gain under the post-2027 rules.

The following comparison illustrates the divergence for a top-marginal-rate individual on a $100 pre-tax return:

| Return type | Pre-tax return | Indicative after-tax treatment |

|---|---|---|

| Capital gain (pre-2027 rules, 50% discount) | $100 | ~$76.50 (effective rate ~23.5%) |

| Capital gain (post-2027 rules, 30% min. tax on real gain) | $100 | ~$53-$70 depending on indexation and holding period |

| Fully franked dividend | $100 | ~$70 after grossing up and applying franking credit offset |

The core principle: The CGT reform degrades capital gains as a return mechanism but leaves the franking system entirely intact. The relative attractiveness of franked income rises not because franking improved, but because the alternative deteriorated.

Companies themselves are unaffected by the discount removal (no discount existed for companies), preserving their capacity to pass through fully franked dividends. Growth assets held inside superannuation retain concessional CGT treatment, meaning the rotation incentive applies specifically to personal-name and trust holdings.

The sectors most exposed to the reform share a common characteristic: their returns are delivered primarily through capital appreciation rather than franked income.

ASX technology, biotech, and early-stage resources companies face structural compression. Valuations in these sectors depend on anticipated future capital gains, and for investors holding in personal names or trusts, the after-tax return on realising those gains is now meaningfully lower. The return profile of these assets, long duration, low or no current yield, and capital-gain dependent, places them directly in the reform’s path.

The beneficiary cohort sits at the opposite end of the return spectrum. Commonwealth Bank, NAB, Westpac, ANZ, BHP, and Rio Tinto represent the canonical examples: mature businesses with strong franking credit histories delivering returns as franked income that the reform leaves entirely untouched.

The grossed-up yield on bank shares is the honest comparison baseline: CBA’s headline cash yield of sub-3% becomes approximately 4% once the franking credit is included, a differential that pension-phase SMSF members receive as a direct ATO cash refund rather than merely a tax offset, widening the gap further relative to any capital-gain-dependent asset whose after-tax return is now subject to the 30% minimum floor.

| Sector / asset type | Structural impact post-2027 |

|---|---|

| ASX technology | Headwind |

| Biotech | Headwind |

| Early-stage resources | Headwind |

| Major banks (CBA, NAB, WBC, ANZ) | Tailwind |

| Diversified miners (BHP, RIO) | Tailwind |

| Infrastructure | Tailwind (income-oriented) |

| REITs | Nuanced (income tailwind, depreciation recapture rules warrant separate analysis) |

The characteristics that determine whether a sector faces headwind or tailwind are specific:

Between 12 May 2026 and 1 July 2027, the 50% discount remains available for gains realised on assets held longer than 12 months. That creates a structured planning window, not a countdown to panic.

Investors with accrued gains in growth-oriented positions face two primary rational responses. The first is to crystallise those gains before 1 July 2027 while the discount applies, locking in the most favourable after-tax treatment on what may represent decades of accumulated appreciation. The second is to obtain independent market valuations on long-held holdings to document the pre-reform cost base, particularly on pre-1985 acquired assets where the cost-base question is most complex.

The four priority actions for investors with growth-stock exposure ahead of 1 July 2027:

The superannuation contrast: Growth assets held inside super retain concessional CGT treatment. The rotation incentive is concentrated in personal-name and trust holdings. For investors with capacity to contribute, the relative attractiveness of holding growth assets inside super rather than in personal names widens materially after 1 July 2027.

REA Group offers an instructive example of the transition dynamics at work: the listed property platform may see temporary activity uplift from a pre-2027 divestment wave before facing longer-term structural headwinds as the reform reshapes property investment patterns.

The 2026-27 Budget did not just adjust a tax rate. It removed the structural incentive that shaped how Australian retail investors related to equity markets for 27 years. Three shifts are now confirmed:

These shifts are legislated rather than cyclical. A change in economic conditions cannot reverse them. As property becomes structurally less attractive under the same reform, capital migrating toward equities will arrive more selective and more yield-focused, reinforcing the tailwind for quality dividend payers.

Investors who recalibrate around the post-2027 incentive structure during the 13-month transition window position themselves for the market that is forming. Those who leave ASX portfolios unchanged are implicitly betting that removing the discount changes nothing about equity-market logic. That bet is difficult to justify once the mechanism is understood.

For investors wanting to model the specific wealth impact across different holding periods and contribution scenarios, our comprehensive walkthrough of CGT portfolio protection strategies examines a 30-year terminal wealth comparison between the old and new regimes, covers low-turnover ETF structuring, and walks through superannuation contribution timing relative to the 30 June 2026 cap deadline.

This article is for informational purposes only and should not be considered financial advice. The interaction of the new rules with specific holdings, trust structures, and superannuation balances varies materially by investor. Professional tax and financial advice should be obtained for individual circumstances. Past performance does not guarantee future results, and forward-looking statements regarding investor behaviour and sector rotation are speculative and subject to change based on market developments and final legislative detail.

The 2026-27 Federal Budget removes the 50% CGT discount for individuals, trusts, and partnerships from 1 July 2027, replacing it with CPI indexation of the cost base and a 30% minimum tax on real capital gains. Companies and superannuation funds are largely unaffected by the change.

From 1 July 2027, investors holding growth-oriented ASX shares in personal names or trusts will no longer receive a 50% reduction on taxable gains; instead, only CPI indexation offsets the gain before the 30% minimum tax applies, materially reducing after-tax returns on capital-appreciation-dependent assets.

ASX technology, biotech, and early-stage resources companies face headwinds because their returns rely on capital appreciation now taxed less favourably, while major banks (CBA, NAB, Westpac, ANZ), diversified miners (BHP, Rio Tinto), and infrastructure stocks receive a tailwind as their fully franked dividends become the most tax-efficient return mechanism under the new rules.

Investors should review unrealised gains across all personal-name and trust-held equity positions, obtain independent valuations on long-held assets to document the pre-reform cost base, assess whether to rotate toward franked-income assets before the effective date, and review trust structures in light of both the CGT discount removal and the July 2028 minimum tax on discretionary trusts.

Franking credits represent company tax already paid on profits and offset the shareholder's personal tax liability on dividend income; because the CGT reform degrades the after-tax return on capital gains while leaving the franking system entirely intact, fully franked dividends become the structurally superior return mechanism for tax-sensitive portfolios outside superannuation from 1 July 2027.