Foxconn Beats Q2 Estimates by 6% as AI Server Demand Surges

17 hrs ago

Japan’s 30-year government bond yield hit an all-time high on Monday 18 May 2026. The 10-year US Treasury yield reached its highest level since February 2025. Oil is trading above $100 a barrel. All three facts arrived in the same session.

A global bond market selloff that had been building for more than a week accelerated sharply in early Asian trading on 18 May 2026, with sovereign yields rising across the United States, Japan, Germany, and the United Kingdom. The catalyst: a Middle East conflict now exceeding two months, a drone strike on UAE infrastructure, and crude oil prices crossing the threshold that markets treat as a hard inflation signal. What follows is a breakdown of what is driving yields higher across every major sovereign debt market, what those yield levels mean in historical context, how central bank rate expectations have shifted, and what the moves signal for investors reassessing fixed-income exposure today.

The selloff’s proximate trigger was not a vague macro fear. It was a specific sequence of escalation over recent days that markets could trace from a warzone to a trading screen.

Analysts at OCBC characterised the convergence of these events as materially raising the probability of a wider conflict.

OCBC analysts noted that the combination of fresh attacks on UAE and Saudi targets, a presidential ultimatum, and the upcoming high-level security meeting collectively elevated the risk of renewed large-scale military escalation in the region.

The transmission mechanism from geopolitics to bond markets runs through oil. WTI crude rose approximately $2.32 (+2.30%) to around $103.34 on 18 May 2026. Brent climbed roughly $1.98 (+1.81%) to approximately $111.24. Oil above $100 a barrel reprices inflation expectations directly: investors holding fixed-rate government debt demand higher yields to compensate for the erosion of purchasing power that elevated energy costs produce.

Energy-driven supply shocks transmit into the real economy through two channels simultaneously: consumer spending power erodes as fuel costs rise, and corporate margins compress as input and logistics costs increase, with travel operators and discretionary retailers typically registering the earliest and sharpest pressure.

Whether this yield move proves durable depends in part on whether the conflict, now more than two months old, escalates further or finds a path toward resolution.

The breadth of the move matters as much as the magnitude. This is not a single-country dislocation; it is a repricing event spanning four of the world’s largest sovereign debt markets.

| Instrument | Yield Level | Date | Notable Benchmark |

|---|---|---|---|

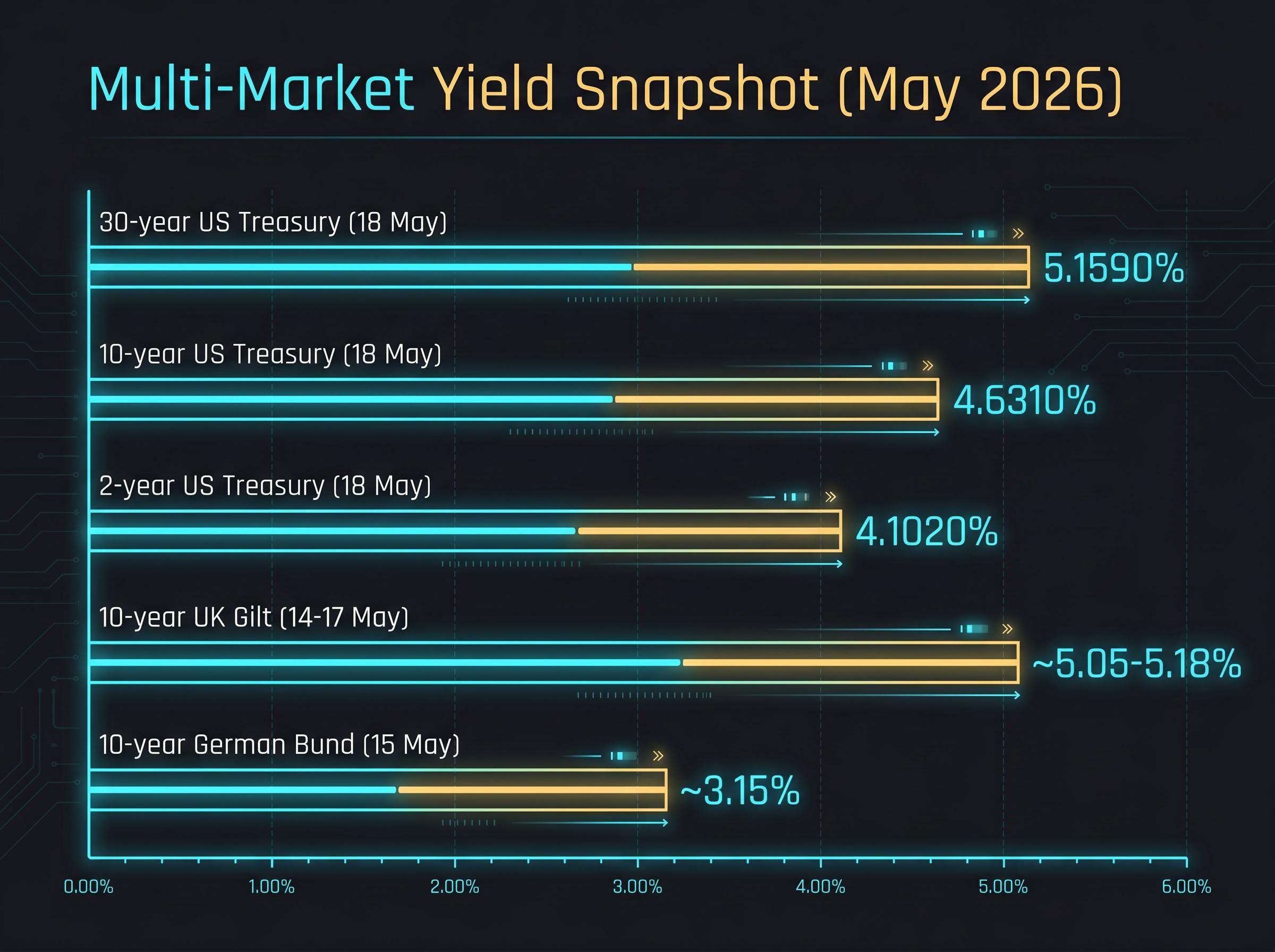

| 10-year US Treasury | 4.6310% | 18 May 2026 | Highest since February 2025 |

| 30-year US Treasury | 5.1590% | 18 May 2026 | Highest since late 2024 |

| 2-year US Treasury | 4.1020% | 18 May 2026 | 14-month peak |

| 10-year German Bund | ~3.15% | 15 May 2026 | Bund futures down ~0.4% on 18 May |

| 10-year UK Gilt | ~5.05-5.18% | 14-17 May 2026 | Elevated across the week |

French OAT futures also declined approximately 0.4% on 18 May 2026, reinforcing the picture of a Europe-wide selloff running alongside the US and Japanese moves.

The 10-year US Treasury’s rise of roughly 20 basis points over the prior week illustrates the pace. These are not gradual adjustments; they are markets recalibrating in compressed timeframes.

Geopolitical risk transmitting across asset classes simultaneously is visible in the Asian session data from 18 May 2026, where the Hang Seng fell approximately 1.7% and the ASX 200 dropped approximately 1.6% alongside the bond selloff, illustrating how a single supply shock can reprice equities, fixed income, and currencies in the same trading window.

Japan’s yield moves share the same geopolitical and inflation trigger as the US and European selloff, but the severity of the records set in Tokyo on 18 May 2026 points to something structurally distinct.

The 30-year Japanese government bond yield surged 17 basis points to an all-time high of 4.170%. The 10-year JGB yield touched 2.800%, the highest since October 1996, a 28-year peak. For a market defined by decades of ultra-low yields, these are moves of historic proportion.

Two distinct pressures are acting on JGBs simultaneously:

Plans for supplementary bond issuance to cushion the war’s economic impact introduce a supply-side dimension to JGB selling that US and European bonds do not face in the same way. More issuance increases the supply of bonds in the market, which depresses prices and pushes yields higher, independent of what inflation expectations are doing.

Goldman Sachs directional guidance from May 2026 specifically recommended underweighting long-dated JGBs on these supply pressures, providing institutional validation that the Japan-specific risk is being priced separately from the broader global selloff.

The cross-asset implication is direct: Japan’s JGB market is one of the world’s largest, and a sustained move higher in JGB yields can force repatriation of Japanese capital from overseas bond markets, amplifying the global selloff further.

For investors tracking the full cross-asset implications of Japan’s JGB moves, our dedicated guide to Japan’s yen intervention and US Treasury selling examines how the Ministry of Finance’s estimated $40-50 billion in implied Treasury liquidations during Golden Week 2026 has added a separate source of upward pressure on US yields that operates independently of the oil and inflation trigger driving the broader global selloff.

For readers holding bond ETFs or fixed-income funds, the headline numbers require a framework to interpret. Bond yields and bond prices move in opposite directions, and understanding that relationship is the foundation for reading this selloff.

The extra yield that investors demand to hold longer-dated bonds when the future is uncertain is called term premium. Geopolitical shocks and inflation scares push term premium higher because the range of possible outcomes widens. That is precisely what is happening now.

A 30-year US Treasury at 5.1590% and a 30-year JGB at 4.170% represent historically elevated real borrowing costs. These yields flow through to government financing costs, corporate borrowing rates, and mortgage rates globally.

Goldman Sachs directional guidance from May 2026 noted that yield rises driven by term premium and geopolitical risk, rather than growth downgrades, may create selective entry opportunities for investors willing to add high-quality duration.

The 10-year US Treasury’s 20-basis-point rise over the prior week underscores how quickly these costs are repricing.

The geopolitical trigger has set off a parallel repricing of what central banks will do next. The shift is visible in live market pricing, and it runs counter to the rate-cutting expectations that dominated earlier in 2026.

| Central Bank | Current Rate Expectation | Projected Timeline |

|---|---|---|

| US Federal Reserve | Rate hike probability above 50% | By December 2026 (per CME FedWatch) |

| European Central Bank | Potential rate increase | As early as June 2026 (per market pricing) |

| Bank of England | Approximately two rate increases priced in | During 2026 |

The Fed repricing is the starkest. As of 18 May 2026, CME FedWatch-derived probabilities placed the likelihood of a Federal Reserve rate increase by December 2026 above 50%. Markets that entered the year expecting cuts are now pricing hikes.

CME FedWatch probabilities are derived from Fed Funds futures contract prices, translating live market positioning into an implied likelihood of each possible policy outcome at upcoming Federal Reserve meetings.

The 2-year US Treasury yield, the maturity most sensitive to policy rate expectations, sits at 4.1020%, a 14-month peak. The short end of the curve is confirming what the probabilities suggest.

Charu Chanana, Chief Investment Strategist at Saxo, characterised the shift as a return to an elevated-for-longer rate environment in market sentiment.

The reinforcing dynamic matters. Higher central bank rate expectations push short- and medium-term yields up directly, while also reinforcing long-end selloffs by signalling that the era of suppressed policy rates is extending rather than ending.

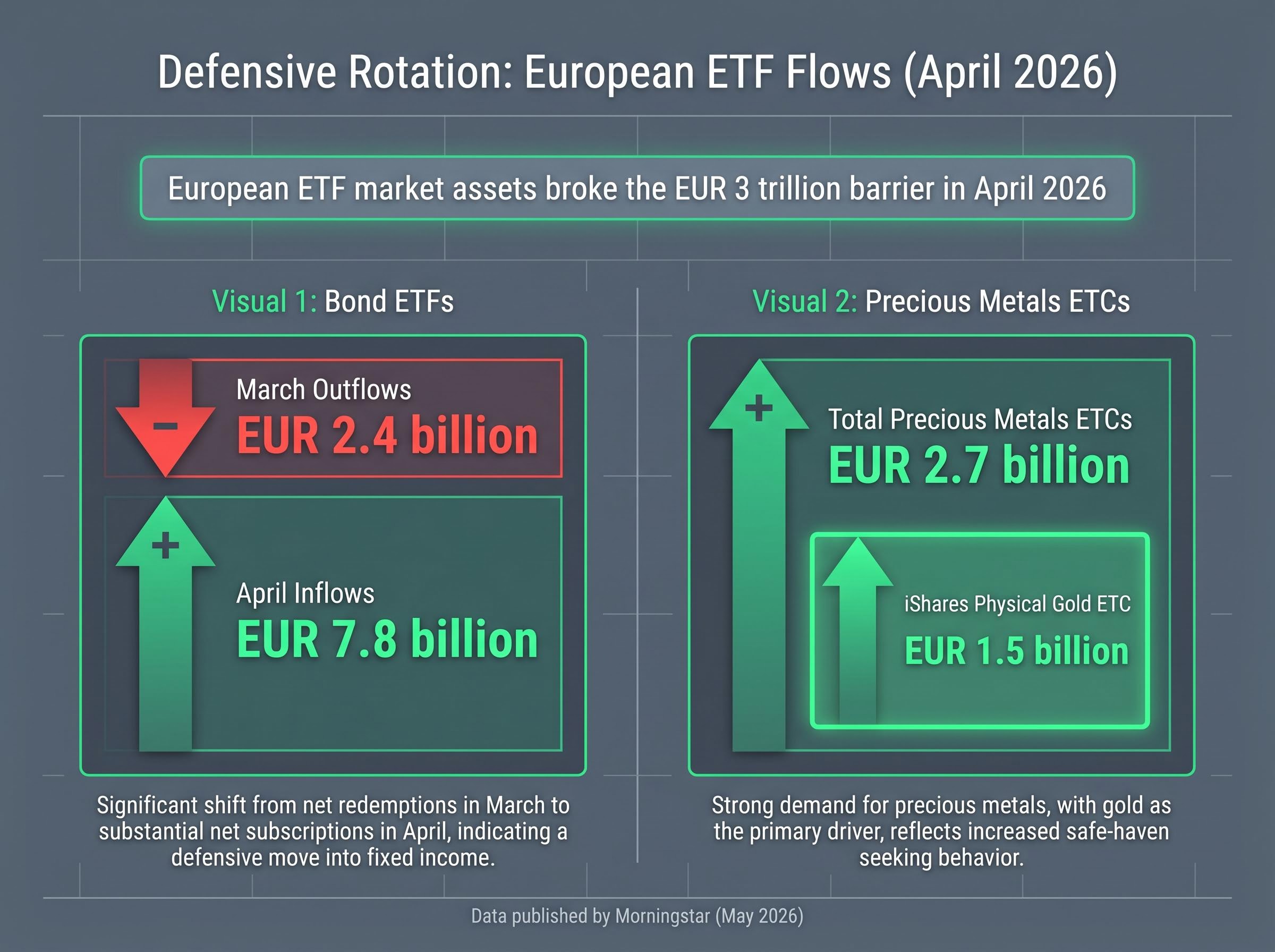

The rotation into defensive positioning was already underway before the 18 May peak. April 2026 European ETF flow data, published by Morningstar in May 2026, showed EUR 7.8 billion flowing into bond ETFs, fully reversing March’s EUR 2.4 billion in outflows. Demand concentrated in government bond ETFs, consistent with a preference for portfolio ballast.

Three signals from the April flow data paint the defensive picture:

The European ETF market’s total assets broke the EUR 3 trillion barrier in April 2026, underscoring the scale of the market in which these flows are occurring.

JPMorgan Asset Management’s general May 2026 directional guidance recommended increasing allocations to 5-10 year US Treasuries and UK gilts, arguing that yields now more than compensate for revised rate paths. The firm recommended trimming high yield and leveraged loans if energy prices remain elevated, and proposed raising fixed-income from underweight toward neutral, funded from rate-sensitive equities including US growth, technology, and small-cap names.

Goldman Sachs directional guidance favoured 7-10 year US Treasuries and German Bunds, maintaining an overweight in investment-grade credit versus high yield.

The two firms differ on specific maturity preferences, but converge on the same structural call: reduce credit risk, increase exposure to high-quality sovereign duration.

Investors wanting to translate the yield moves into specific portfolio action will find our deep-dive into portfolio positioning during a synchronised yield surge, which examines the historical sector rotation patterns triggered by rapid yield increases, including the shift from long-duration growth into value, financials, and commodity-linked names that session data from 18 May 2026 already shows beginning.

Three converging forces sustain the selloff as trading resumes: geopolitical escalation with oil above $100 a barrel; central bank rate expectations repriced upward across the Fed, ECB, and Bank of England; and Japan-specific supply pressure from emergency budget issuance. None of these forces has a near-term resolution date.

The open question is binary. If the Middle East conflict de-escalates, the oil and inflation trigger could reverse, and yields would likely retrace a portion of the move. If it intensifies, the yield moves deepen. That makes positioning in long-duration bonds particularly binary right now.

At yields last seen in 2024 or earlier, the entry point question for fixed income is more live today than at any point in the past year. So is the risk of further moves higher if the conflict widens.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A bond market selloff occurs when investors sell government or corporate bonds in large volumes, pushing bond prices down. Because bond yields move inversely to prices, falling prices cause yields to rise, signalling that investors are demanding higher compensation to hold fixed-rate debt.

The selloff was triggered by a convergence of Middle East escalation events including a drone strike on UAE nuclear facility infrastructure, stalled Iran peace talks, and oil prices crossing $100 a barrel, which raised inflation expectations and prompted investors to sell sovereign bonds across the US, Japan, Germany, and the UK.

Japan's 30-year JGB yield surged to a record 4.170% due to two pressures acting simultaneously: the global inflation shock from oil above $100 a barrel, and Japan-specific supply pressure from reports of supplementary budget issuance to fund emergency economic measures related to the conflict.

As of 18 May 2026, CME FedWatch-derived probabilities placed the likelihood of a Federal Reserve rate increase by December 2026 above 50%, a dramatic shift from earlier in 2026 when markets were pricing rate cuts rather than hikes.

JPMorgan Asset Management recommended increasing allocations to 5-10 year US Treasuries and UK gilts while trimming high yield and leveraged loans, and Goldman Sachs favoured 7-10 year US Treasuries and German Bunds with an overweight in investment-grade credit, with both firms converging on reducing credit risk and increasing high-quality sovereign duration.