Finfluencer Rules Won’t Work Until the Penalty Beats the Profit

2 hrs ago

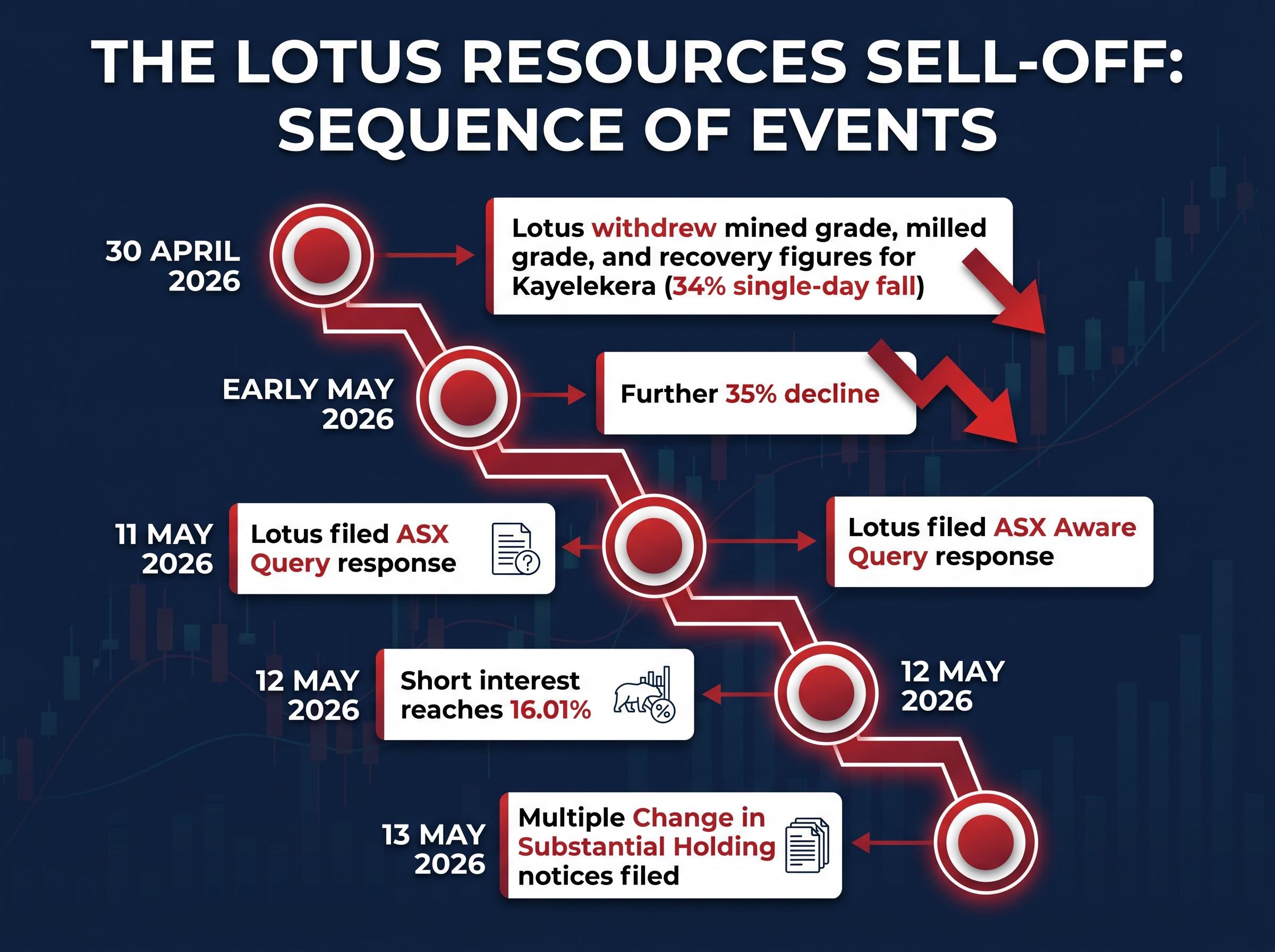

In less than three weeks, Lotus Resources (ASX: LOT) shed more than 60% of its value and attracted the highest short interest of any stock on the ASX. The sellers are still adding to their positions. On 30 April 2026, Lotus withdrew its reported mined grade, milled grade, and recovery figures for the Kayelekera uranium project in Malawi, citing inconsistencies in laboratory sampling and assaying. That single disclosure triggered a 34% single-day collapse, followed by a further 35% decline over subsequent sessions. As of 12 May 2026, with the stock sitting near multi-year lows not seen since 2020, short interest stood at 16.01%, the highest reading on the ASX, representing a 6.31% increase over the prior month. What follows is an examination of why professional short sellers have not only held but expanded their positions after an already severe fall: what the data retraction signals about project integrity, what conditions would need to be met before bearish conviction unwinds, and what retail investors should understand about the difference between a price shock and a credibility event.

The sequence of events moved faster than most investors could process:

ASX Guidance Note 8 on continuous disclosure defines market-sensitive information as anything a reasonable person would expect to have a material effect on price, which means a withdrawal of foundational production data sits squarely within the scope of information requiring immediate release under Listing Rules 3.1 and 3.1A.

What stands out in this timeline is not the initial drop. A 34% single-day fall is violent, but single-day shocks in small-cap resources stocks can stabilise within days if the market reads the event as bounded. The additional 35% decline, arriving without any new negative disclosure, is the detail that reframes the event.

Operational setbacks, whether production delays, cost blowouts, or grade variability, tell the market that outcomes were worse than expected. The underlying measurement and reporting framework remains intact. Investors can recalibrate models and reassess.

A data retraction is structurally different. When a company withdraws mined grade, milled grade, and recovery figures, the market loses confidence not in the outcome but in the measurement system that produced it. Mined grade, milled grade, and recovery rate are the foundational inputs to every resource valuation model applied to Kayelekera. Without reliable figures, the project’s economics cannot be independently assessed. That distinction explains why professional short sellers read the retraction as something more durable than a single bad announcement, and why the selling continued well after the initial shock had been absorbed.

Short interest in Lotus Resources reached 16.01% as of 12 May 2026, the highest level on the ASX. That figure does not represent traders who positioned early and are now sitting passively. The 6.31% month-on-month increase from 7 April to 12 May 2026 reflects capital that entered the trade after the initial collapse, a sign of accelerating conviction rather than opportunistic positioning.

| Metric | Current Reading | Week-on-Week Change | Month-on-Month Change | Recent Peak |

|---|---|---|---|---|

| LOT Short Interest | 16.01% | +0.90% | +6.31% | 16.42% |

Month-on-month short interest increase: 6.31%. New short positions are being established well after the initial price shock, indicating that sophisticated market participants view the bearish thesis as unresolved rather than priced in.

For a stock to carry 16% short interest, a substantial volume of shares must be borrowed and sold with an ongoing financing cost. That cost is only justified if the position holder expects further downside or, at minimum, expects the stock to remain depressed long enough for the carry to be worthwhile. Short interest data also carries a four-day reporting lag (disclosure is not required until three business days after the transaction date), meaning the 16.01% figure reflects positioning as of 11 May 2026, not the current day.

Short interest as an early warning signal has a documented lead time advantage over published company disclosures: institutional short sellers had already lifted LOT positions to approximately 11% in the weeks before the 30 April retraction, meaning the stress was visible in borrowing data before it appeared in the price.

For investors without a mining background, the three figures Lotus withdrew are worth understanding in plain terms:

Together, these three figures form the basis for calculating how much uranium a project actually produces per tonne of material processed. Remove confidence in any one of them, and the financial model built around the project loses its foundation.

Laboratory sampling and assaying is the technical process that generates these figures. Ore samples are collected at various stages, sent to a laboratory, and chemically analysed to determine mineral content. When Lotus cited “inconsistencies” in this process, the implication is that the system producing the numbers may not have been generating reliable results.

The limitations of conventional laboratory assaying methods are part of what makes Lotus’s retraction so difficult for markets to resolve quickly: traditional fire assay and wet chemical processes involve manual sample preparation steps that introduce variability at multiple stages, and re-assaying a full dataset is a time-intensive process that cannot be compressed by investor pressure alone.

The JORC Code 2012 sampling and assaying requirements mandate that companies disclose the nature and quality of sampling procedures, measures taken to ensure sample representivity, and the basis for confidence in reported grades, standards that make a retraction of mined grade and recovery figures a direct challenge to the project’s compliance with Australian mineral reporting norms.

Markets do not wait for confirmed outcomes when a data retraction is announced. The uncertainty itself is priced immediately. The continued build in short interest after 30 April occurred with no new negative news, which is itself informative: the market had already priced in a prolonged period of uncertainty rather than waiting for a resolution announcement. A production miss can be quantified and modelled. A measurement failure raises questions about what else in the dataset may be unreliable, and those questions do not resolve until an independent review is completed.

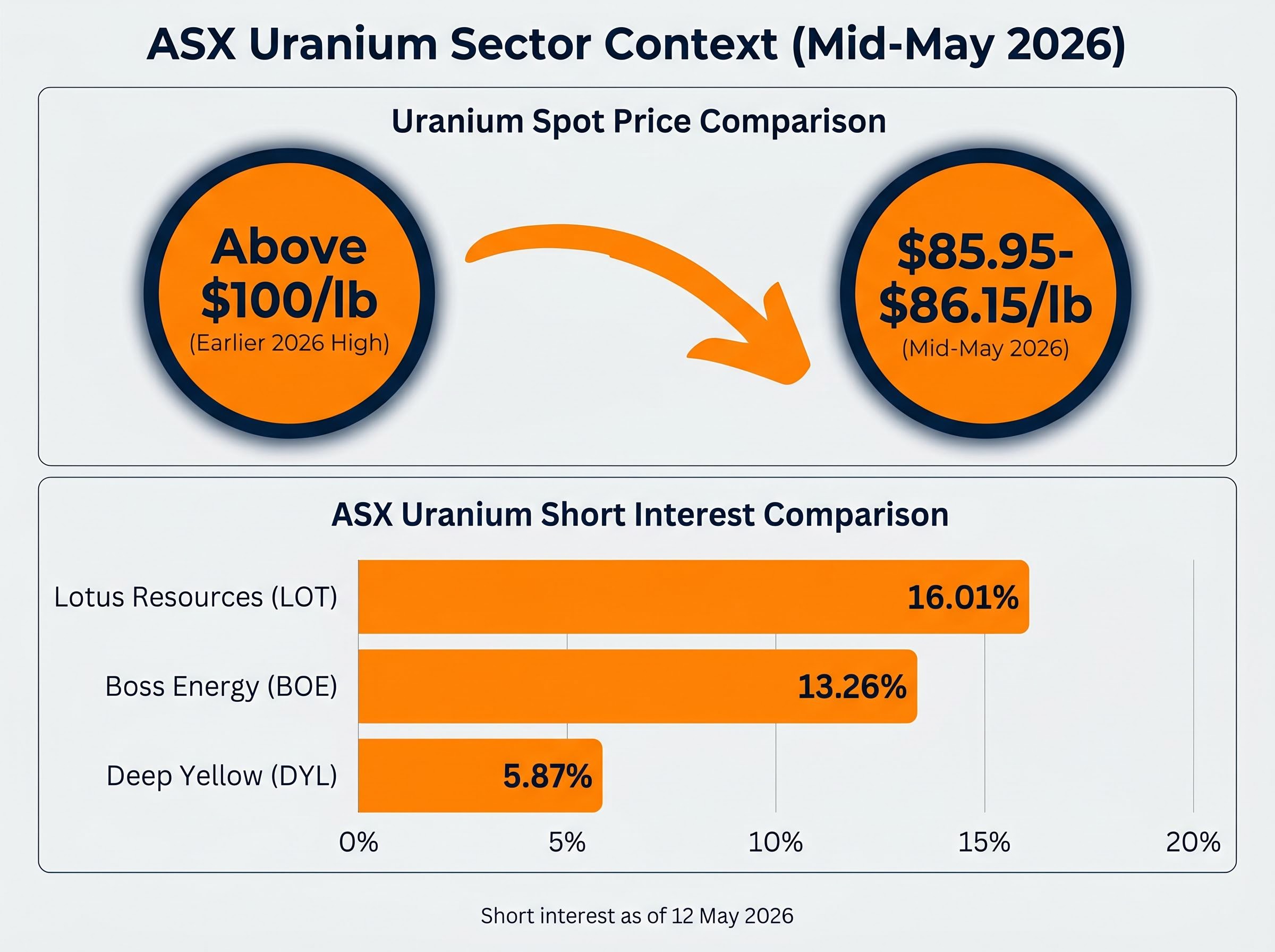

The uranium spot price sat at approximately $85.95-$86.15/lb as of mid-May 2026, down from above $100/lb earlier in the year. That pullback matters for Lotus not as a primary bearish driver but as the absence of a potential offset.

Uranium spot price: approximately $86/lb as of mid-May 2026, against a 2026 high above $100/lb. The sector is not providing the tailwind that could partially offset company-specific credibility concerns.

Bearish positioning is not confined to Lotus. Across ASX uranium equities, short interest has been elevated:

Uranium short interest across the ASX is not isolated to Lotus: Boss Energy carried 13.38% short interest as of early May 2026, with analyst commentary explicitly linking its credibility overhang to the Lotus situation, suggesting that professional sellers are applying a sector-level thesis rather than treating the two positions as independent company-specific bets.

The sector context does not cause the Lotus short thesis. The data retraction is entirely company-specific. But a uranium price at $86/lb and falling, rather than rallying toward new highs, removes the possibility that commodity momentum could provide a partial re-rating for LOT even while the credibility question remains open.

The resolution pathway for a data-integrity event of this kind typically requires a chain of steps, not a single announcement. Based on the pattern observed in comparable ASX resources disclosure events, the conditions likely required before bearish positioning unwinds are:

The ASX Aware Query response filed on 11 May 2026 represents engagement with regulatory scrutiny, but it is not a technical resolution. The multiple Change in Substantial Holding notices filed on 13 May 2026 suggest active repositioning rather than a stabilising shareholder base. With the stock trading at approximately A$0.61-A$0.675 as of mid-May 2026, the market is pricing in a prolonged uncertainty period.

No directly comparable, well-documented ASX precedent exists for a data retraction of this kind with a clearly documented short-interest unwind pattern. In comparable cases involving major operational or disclosure shocks in ASX resources stocks, markets have sometimes continued applying a credibility discount even after clarification was provided, particularly where the original data formed the basis for material investment decisions. The absence of a clean precedent is itself informative: the resolution path for Lotus is likely to be protracted and case-specific rather than following a predictable timeline.

The combination of a credibility event, an unresolved data-integrity question, a softening uranium sector, and the absence of a formal independent review creates conditions for sustained short interest rather than natural unwinding. Time passing without resolution is not neutral; it reinforces the bearish thesis.

For retail investors monitoring subsequent Lotus announcements, the interpretive framework is specific: treat each disclosure not as a short-term trading signal but as evidence for or against the company meeting the resolution conditions outlined above. An independent review, revised resource figures, and sustained operational proof are the markers that matter.

The fact that 16% of the float has been borrowed and sold short is not a prediction of where the stock ultimately trades. It is, however, a real-time signal that the balance of sophisticated opinion remains firmly against a near-term recovery. The burden of proof sits entirely with the company, and the market is not waiting to be proven wrong about Lotus. It is waiting to be proven right about the data.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. These statements are speculative and subject to change based on market developments and company performance.

Short interest represents the percentage of a company's shares that have been borrowed and sold short by investors betting on a price decline. A 16.01% reading for Lotus Resources means a substantial portion of the float has been sold short, signalling that sophisticated market participants expect the stock to remain under pressure or fall further.

Lotus Resources withdrew these figures on 30 April 2026, citing inconsistencies in laboratory sampling and assaying at the Kayelekera uranium project in Malawi. These three metrics are the foundational inputs for every resource valuation model, so their withdrawal removed the market's ability to independently assess the project's economics.

Short sellers would likely need to see an independent third-party review of sampling methodology, revised resource and reserve disclosures following a validated re-assay programme, management accountability steps, and sustained operational proof that project economics remain intact before bearish conviction begins to unwind.

The uranium spot price was approximately $86 per pound in mid-May 2026, down from above $100 per pound earlier in the year. While the price decline is not the primary cause of Lotus's problems, a softening commodity market removes any potential sector-level tailwind that could partially offset the company-specific credibility concerns.

An operational miss, such as a production delay or cost overrun, means results were worse than expected but the underlying measurement system remains intact and investors can recalibrate their models. A data retraction means the measurement system itself is in question, making it impossible to independently assess project economics until an independent review is completed.