CURE and CLNE: the ASX ETFs Returning 25% in 2026

7 hrs ago

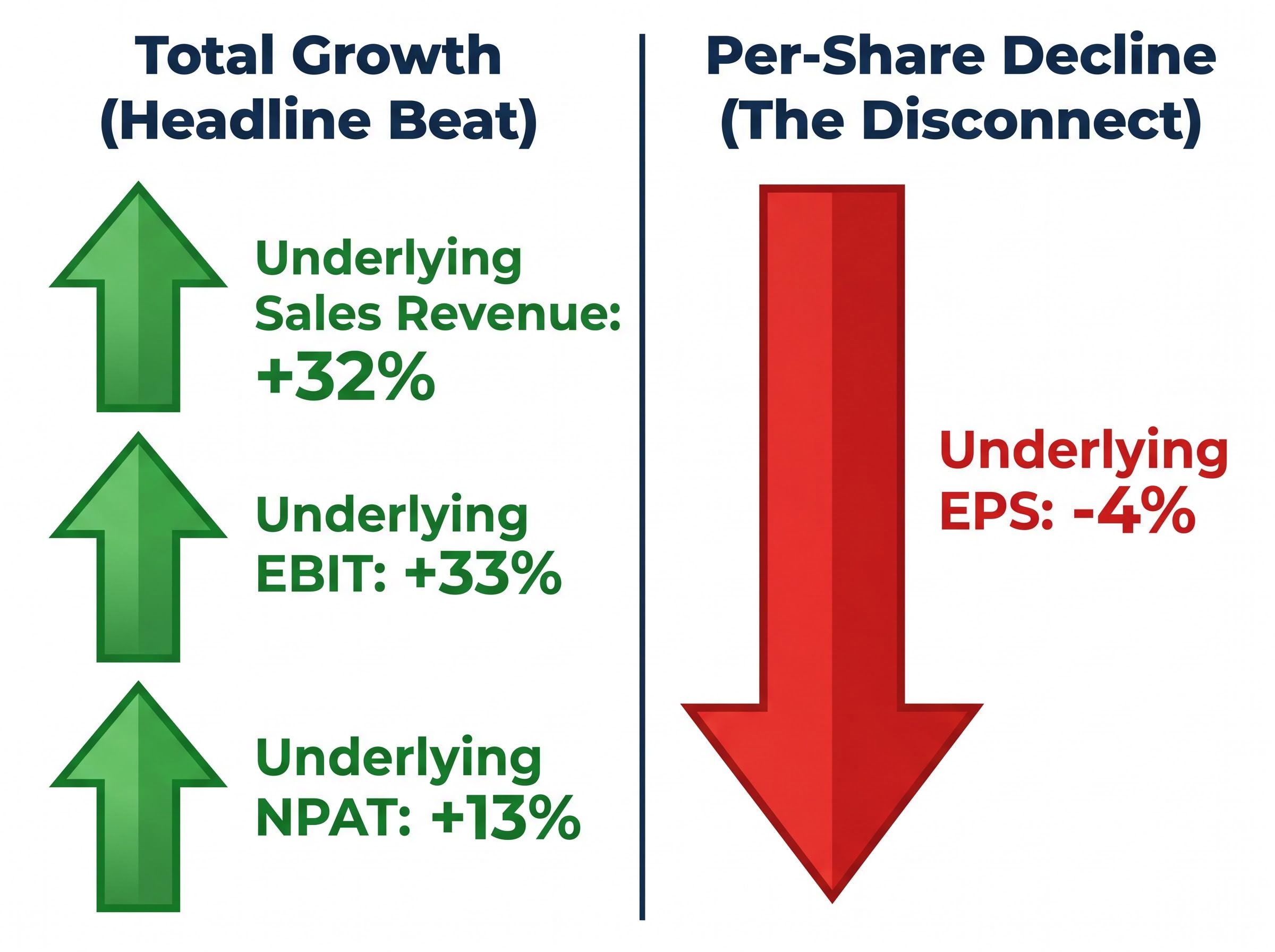

Elders posted 32% revenue growth and 33% EBIT expansion for its first half of FY26. The market responded by sending the stock down roughly 21% on results day.

For investors tracking the Elders share price near the lower end of its five-year range, the disconnect demands more than a headline scan. What appeared to be a strong set of numbers concealed a specific tension: earnings per share, the metric the market actually prices, moved in the opposite direction to every other headline figure. The 4% decline in underlying EPS to $0.181, driven by the cost of integrating the Delta Agribusiness acquisition, reframed a growth story into a dilution story in the space of a single trading session.

This analysis unpacks the H1 FY26 result in full, explains why the selloff occurred despite the headline beat, and assesses what Elders’ own second-half outlook signals for investors watching the stock at approximately $7.20-$7.25.

On the surface, Elders’ H1 FY26 result read as a recovery half. Underlying sales revenue rose 32% to $1.77 billion. Underlying EBIT climbed 33% to $76.6 million. Statutory net profit after tax increased 17% to $39.5 million, and operating cash flow more than doubled, up 115% to $67 million. The interim dividend held steady at $0.18 per share.

Operating cash flow more than doubling to $67 million was one of the cleaner signals in the result, and the accompanying cash conversion surge to 176.6% from 93.1% in the prior half suggests the underlying business generated cash meaningfully ahead of reported earnings, a dynamic that receives less attention than the EPS decline but matters for assessing balance sheet trajectory.

One metric broke the pattern. Underlying earnings per share fell 4% to $0.181, even as underlying NPAT grew 13% to $37.9 million.

Underlying earnings per share fell 4% to $0.181, the one number in the result that moved against the grain.

That single figure reshaped the market’s reading of every other number in the release. Revenue growth matters, but investors price per-share returns. When total earnings grow but per-share earnings compress, the market treats the growth as having been bought rather than earned. The table below captures the full picture.

| Metric | Prior Period | H1 FY26 | Change |

|---|---|---|---|

| Underlying Sales Revenue | $1.34B | $1.77B | +32% |

| Underlying EBIT | $57.6M | $76.6M | +33% |

| Underlying NPAT | $33.5M | $37.9M | +13% |

| Underlying EPS | $0.189 | $0.181 | -4% |

| Operating Cash Flow | $31.2M | $67.0M | +115% |

| Interim Dividend | $0.18 | $0.18 | Maintained |

The breadth of the H1 result was genuine. Most of Elders’ operating divisions grew EBIT, and the drivers were distinct enough to suggest the business was not reliant on a single tailwind.

Eastern Young Cattle Indicator data from Meat and Livestock Australia confirms the significant recovery from 2023 lows, with the index providing the livestock pricing benchmark that underpins Elders’ rural services EBIT performance across agency and livestock trading divisions.

The Killara Feedlot was divested during the half and excluded from underlying earnings.

Within rural services, the Elders Finance broker network expansion added to costs even as it broadened the division’s revenue base. AIRR’s result illustrated the tension running through the broader business: sales and margins improved, but labour costs ate into the gains. That same tension, growth absorbing its own cost of delivery, became the defining theme of the result once the segmental picture was assembled in full.

The gap between Elders’ EBIT growth and its EPS decline is not a contradiction. It is a mechanical outcome of acquisition-funded expansion, and understanding the mechanism is the key to reading this result correctly.

The sequence works as follows:

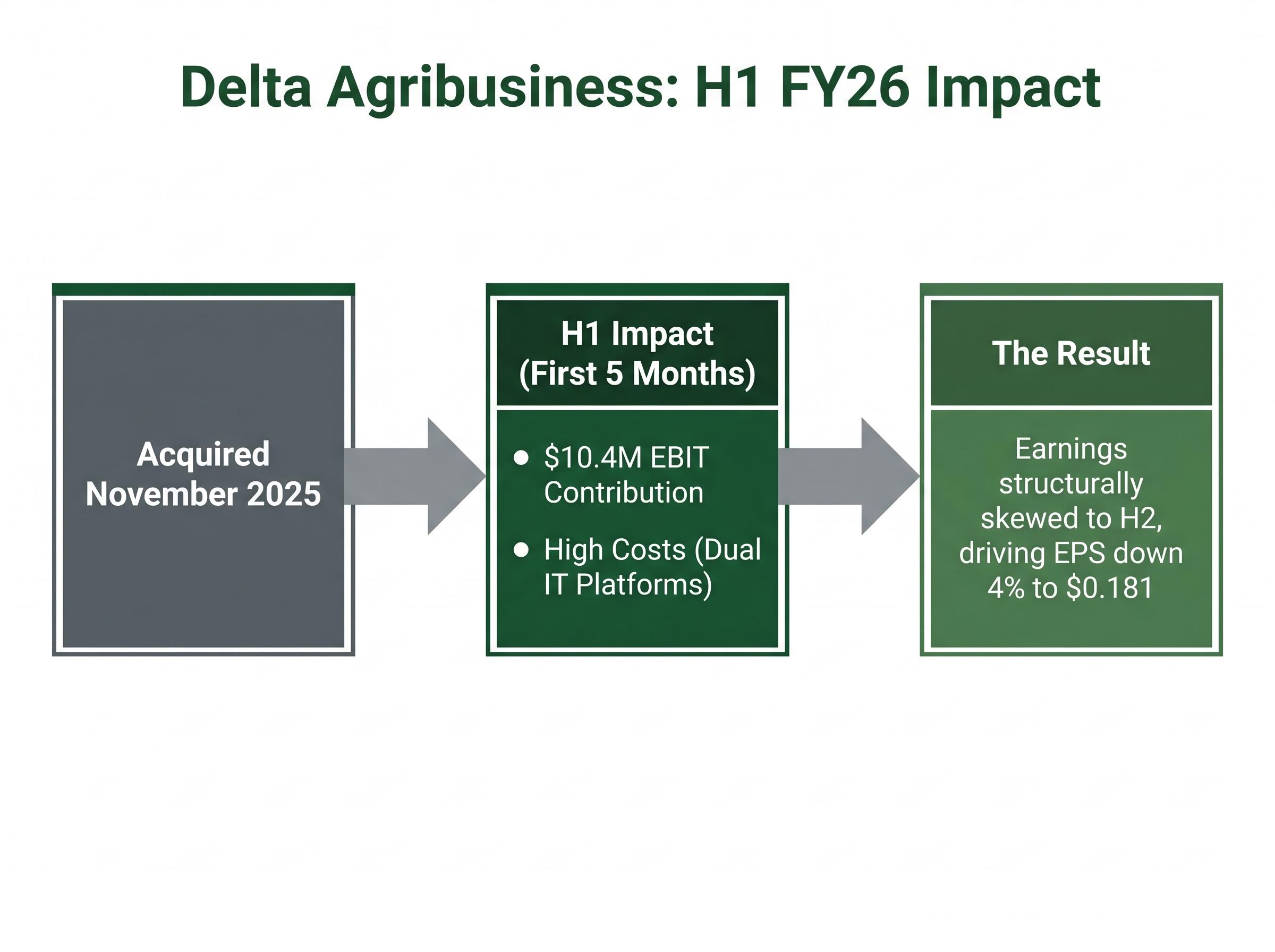

Delta Agribusiness, acquired in November 2025, contributed $10.4 million in EBIT across its first five months under Elders ownership. However, Delta’s earnings are structurally skewed toward the second half of the financial year, meaning H1 captured the acquisition’s costs, including dual IT platforms running simultaneously, before capturing the full weight of its returns.

Markets price earnings per share, not total earnings, and Delta’s first five months cost more than they returned on a per-share basis.

The result: NPAT grew 13%, but EPS fell 4% to $0.181. The market priced the per-share number. This distinction applies not only to Elders but to any acquisition-driven earnings result where total growth masks per-share dilution.

Beyond the acquisition arithmetic, three distinct cost headwinds sat inside the H1 result:

The Rabobank Rural Confidence Survey for Q1 2026 documented mounting input costs, including fuel, fertiliser, and labour, as the primary concerns weighing on Australian farmer sentiment, providing sector-wide context for the cost headwinds Elders reported inside its own H1 result.

The distinction between temporary and persistent pressures matters. Dual IT platforms are a transition-phase cost; once Elders consolidates to a single system, that line item should compress. Labour inflation and fuel exposure are different. They reflect structural and external conditions that management can manage around but cannot eliminate.

Elders noted that established supplier relationships helped manage demand and support growers ahead of season despite input cost pressures. Whether that relationship advantage translates into margin protection or simply volume preservation is a question the H2 result will need to answer.

Elders’ forward commentary pointed to several constructive tailwinds for the second half:

External conditions reinforce parts of that view. The Bureau of Meteorology’s seasonal outlook for early 2026 flagged improving rainfall probabilities across eastern cropping zones heading into the winter season. According to Meat & Livestock Australia data, the Eastern Young Cattle Indicator has recovered significantly from 2023 lows, supporting agency volumes and restocking sentiment. The Rabobank Rural Confidence Survey (early 2026) showed farmer sentiment recovering in cropping and mixed-farming regions. Diesel prices moderated from their March 2026 peak, reducing (though not eliminating) fuel cost risk.

Per capita recession dynamics in Australia through 2025-2026 have created a specific challenge for rural services businesses: total population-driven demand can grow while individual household capacity to spend on rural and residential property transactions, advisory services, and crop inputs contracts, a distinction that headline GDP figures do not capture and that matters for evaluating Elders’ real estate and agency volume assumptions.

Improving rainfall probabilities across eastern cropping zones into the 2026 winter season represent one of the cleaner tailwinds in Elders’ H2 outlook.

What management did not provide is equally telling. No specific synergy dollar values from the Delta integration have been disclosed. No clear timeline for resolving the dual IT platform has been committed to publicly. No updated full-year EPS guidance was offered. The tailwinds are real, but the commitments remain directional rather than numerical.

The 21% results-day decline did not arrive in isolation. Elders traded above $12 in 2022 before a sustained multi-year fall brought the stock to its current range of approximately $7.20-$7.25, with a 52-week low of $5.86 and a 52-week high of $7.91.

That trajectory mirrors a broader pattern. Agribusiness valuations across Australian listed peers, including GrainCorp and others, have compressed as the market transitioned from the post-La Nina boom expectations of 2020-2022 to normalised earnings and rising cost realities. Investors who bought the sector for peak-cycle returns found the cost base rising faster than revenues could sustain those margins.

Agribusiness earnings compression across the ASX peer group has been a consistent theme in the 2025-2026 period, with GrainCorp’s FY26 guidance pointing to EBITDA roughly one-third below the prior year as global grain oversupply and margin contraction worked through the supply chain, providing context for the broader sector de-rating that has weighed on valuations beyond any company-specific factors.

The Elders share price has more than halved from its 2022 peak above $12, and whether the current $7.20 level represents the floor or a waypoint remains the central question.

The maintained interim dividend of $0.18 per share offers one signal: management chose not to cut the payout despite cost pressures, which implies confidence in underlying cash generation. Whether that confidence is validated depends on whether the market is penalising Elders for a temporary transition or repricing it for a structurally higher cost base as the easy volume tailwinds of the wet years recede.

Two competing readings of the H1 FY26 result remain defensible.

The optimistic case holds that the EPS dip is a transition artefact. Delta’s earnings are genuinely skewed to H2, the winter crop outlook has improved, and integration costs are by nature temporary. Once the dual IT platforms consolidate and Delta’s full-year contribution materialises, per-share earnings should recover.

The cautious case holds that the cost base has structurally shifted higher, that synergies remain unquantified, and that the market has seen agribusiness earnings promises before, particularly during and after the 2020-2022 wet-year boom, that did not sustain.

Three concrete signposts in H2 FY26 will help resolve the question:

The maintained dividend of $0.18 per share is the one firm signal management sent about its confidence in the business. Investors will need the H2 result to confirm whether that confidence was warranted.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Despite 32% revenue growth and 33% EBIT expansion, Elders' underlying earnings per share fell 4% to $0.181 because the Delta Agribusiness acquisition added costs, including dual IT platforms and integration spend, that exceeded its immediate per-share earnings contribution in the first half.

Underlying EPS (earnings per share) measures how much profit a company generates for each share on issue, stripping out one-off items. It matters because investors price per-share returns, not total earnings, so when EPS declines even as total profits grow, the market often treats that as dilution from an acquisition rather than genuine organic growth.

Delta Agribusiness, acquired in November 2025, contributed $10.4 million in EBIT across its first five months under Elders ownership. However, Delta's earnings are structurally skewed toward the second half of the financial year, meaning H1 captured more of its costs than its returns.

Investors should watch three things: Delta's EBIT contribution relative to the $10.4 million recorded in H1 (a materially higher number is expected), evidence of IT platform consolidation reducing corporate costs, and winter crop conditions through June-August 2026 that will determine whether the seasonal tailwind converts to actual revenue.

Elders maintained its interim dividend at $0.18 per share despite cost pressures in H1 FY26, which management's decision to hold the payout implies confidence in underlying cash generation, supported by operating cash flow more than doubling to $67 million in the half.