Woolworths has rallied 12.1% since the start of 2025, pushing the share price back toward A$33.50 and reinforcing its status as one of the ASX’s most widely held defensive names. Beneath the rally, however, the financial profile tells a less comfortable story. FY24 return on equity sits at just 1.9%, the debt-to-equity ratio exceeds 300%, and the forward dividend yield now trails the RBA cash rate of 3.85%. With the ACCC’s supermarket pricing inquiry adding regulatory uncertainty and new CEO Amanda Bardwell managing cost pressures, competitive intensity from Aldi, and political scrutiny simultaneously, the risk-reward equation at current levels is more nuanced than the defensive label typically invites. This analysis examines whether the consumer staples moat, franked dividends, and grocery market dominance justify a low-to-mid-20s forward P/E, or whether elevated leverage and weak capital efficiency are being underpriced.

What the 12% rally actually tells us about WOW’s market position

The 12.1% gain since January 2025 is real, and for shareholders who held through the stock’s slide to $25.51 earlier in the 52-week range, the recovery toward A$33.50 has been welcome. But the current price sits almost exactly in the middle of that $25.51-$38.24 range, neither confirming the optimism of the highs nor reflecting the pessimism of the lows.

- Current price: approximately A$33.50 (as of 16 May 2026; day range $33.40-$33.67)

- 52-week range: $25.51-$38.24

- YTD gain from January 2025: 12.1%

At these levels, Woolworths trades on a forward P/E in the low-to-mid-20s, consistent with the broader ASX 200 Consumer Staples sector, which has commanded a 20-30% premium to the wider market through much of 2025-2026 on defensive demand. The question is whether that premium reflects genuine earnings quality or simply the willingness of cautious investors to pay more for perceived safety.

A share price move, by itself, reveals little about whether valuation is supported by fundamentals or stretched by sentiment. The numbers beneath the rally are where the answer sits.

When big ASX news breaks, our subscribers know first

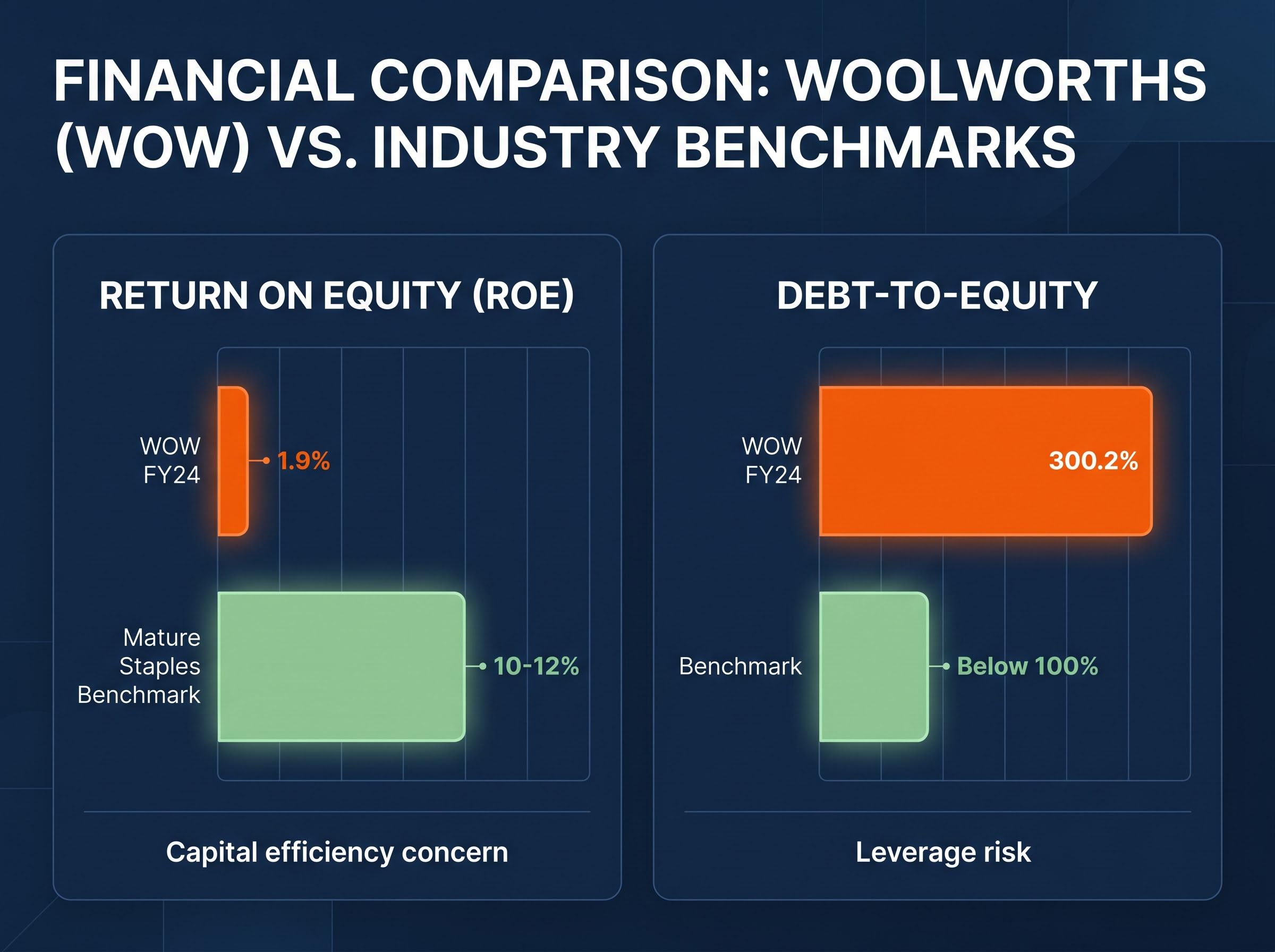

The balance sheet problem: what a 300% debt-to-equity ratio actually means for WOW investors

A debt-to-equity ratio above 100% means a business carries more debt than equity. Woolworths sits at triple that benchmark.

The FY24 debt-to-equity ratio of 300.2% did not materialise from a single aggressive borrowing decision. It reflects a combination of prior capital management activity, supply-chain investment cycles, and equity erosion from past write-downs. The result, however, is a balance sheet that carries implications regardless of how it got there.

The Australian Financial Review characterised Woolworths’ balance sheet in March 2025 as one that “no longer screams fortress,” noting investors were “paying a premium for a balance sheet that no longer screams ‘fortress’.”

At H1 FY25 results in February 2025, management reiterated a focus on maintaining BBB-range credit metrics, with net debt roughly stable versus FY24 year-end. That stability, though, is not the same as deleveraging.

Three financial flexibility implications follow from leverage at this level:

- Deleveraging capacity is constrained. Reducing debt requires either asset sales or surplus cash flow, both of which are limited in a low-margin grocery business reinvesting to compete.

- Earnings shock absorption is narrow. A balance sheet at 300% debt-to-equity has less room to absorb an unexpected downturn in operating earnings without credit rating pressure.

- Interest servicing depends on stable cash flows. The business must sustain its operating performance to meet obligations, leaving little margin for error if competitive or regulatory conditions tighten further.

Understanding ROE and why 1.9% is a problem for a mature consumer staples business

Return on equity measures the net profit a company generates per dollar of shareholder equity. It is one of the clearest indicators of how efficiently a business deploys the capital entrusted to it by shareholders. A company earning a high ROE is compounding wealth on behalf of its owners; a company earning a low ROE is, in effect, tying up capital without generating adequate returns.

Return on equity benchmarks vary meaningfully across sectors, with consumer staples typically requiring a 10-12% threshold before a premium valuation multiple is considered warranted, because a low ROE signals the business is retaining and deploying capital less efficiently than the multiple implies.

For mature consumer staples businesses, a 10-12% ROE is generally considered the minimum threshold at which the premium valuation these stocks attract is warranted. The logic is straightforward: if investors are paying above-market multiples for stability and compounding, the compounding needs to actually show up in the returns.

Damodaran sector ROE benchmarks compiled from January 2026 data show consumer-facing and food-adjacent industries operating at ROE levels well above single digits, providing an empirical basis for the 10-12% threshold that mature staples businesses are typically expected to clear before premium multiples are considered warranted.

Woolworths’ FY24 ROE of approximately 1.9% does not clear that bar.

| Metric | WOW FY24 | Mature Staples Benchmark | Implication |

|---|---|---|---|

| Return on Equity | 1.9% | 10-12% | Capital efficiency concern |

| Debt-to-Equity | 300.2% | Below 100% | Leverage risk |

The sources of that weakness are identifiable. FY24 CEO commentary cited “material cost inflation across wages, logistics and energy” as ongoing headwinds. Amanda Bardwell, who took the CEO role in September 2024, described FY25 as “another year of disciplined investment rather than margin expansion.” Morningstar has noted that returns on capital and equity have “trended down to low single digits” as competition and regulation bite.

Why the ROE benchmark matters more than the headline earnings number

Reported earnings can look stable while ROE deteriorates, because the equity base itself changes. Write-downs, capital management activity, and restructuring charges all alter the denominator in the ROE calculation. In Woolworths’ case, prior write-downs have eroded the equity base, which mechanically inflates debt-to-equity and suppresses ROE in ways that can distort simple period-to-period comparisons.

Australian fund managers have been direct in their assessment. Commentary cited on Livewire Markets in May 2025 described the ROE as “anemic” and argued it “no longer justifies a double-digit earnings multiple premium to the market.” That is not a fringe view; it reflects a growing discomfort among institutional holders with the gap between the valuation multiple and the capital returns it is supposed to represent.

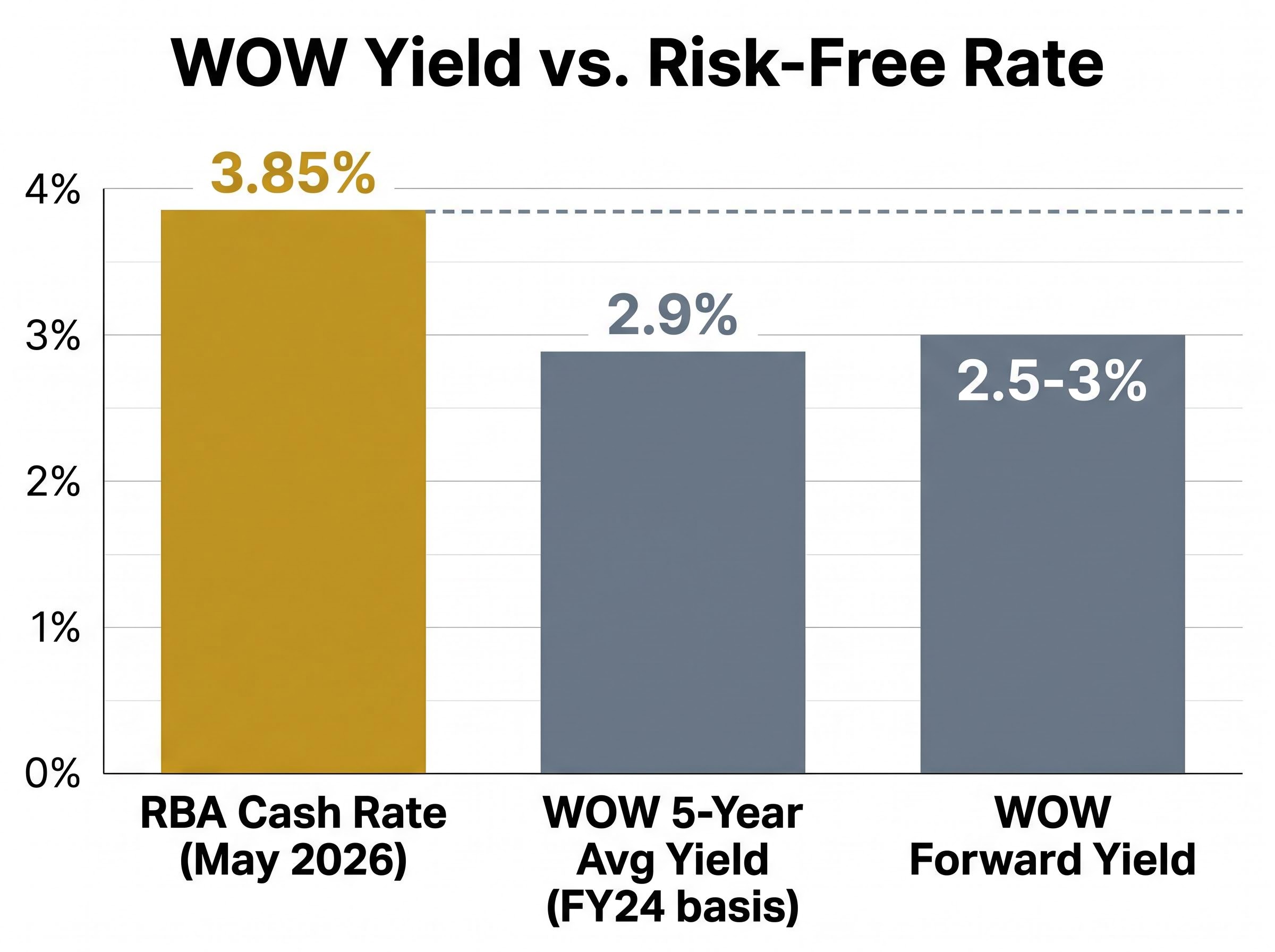

Dividend yield, the RBA cash rate, and the income case for WOW at current prices

For many Australian investors, particularly self-managed super funds and retirees, Woolworths’ fully franked dividend has long been part of the reason to own the stock. The franking credit gross-up adds real after-tax value, and the consistency of payments from a dominant grocery retailer has made WOW a core income holding in many portfolios.

The franking credit gross-up changes the income calculation materially depending on an investor’s marginal tax rate, with SMSF pension-phase accounts potentially receiving the full credit as a cash refund while investors on the top marginal rate derive a smaller incremental benefit over an equivalent unfranked yield.

That thesis, however, now faces an uncomfortable comparison. The RBA cash rate stands at 3.85% as of May 2026. Woolworths’ five-year average dividend yield has been approximately 2.9% on an FY24 basis, with forward yield closer to 2.5-3% at current price levels. Even after grossing up for franking credits, the yield premium over risk-free cash has compressed to a point where the equity risk being carried is working harder than usual to justify the position.

“Woolies will defend the dividend, but that means even less flexibility to deleverage.” — Australian fund manager commentary

Three considerations frame the income case at current levels:

- Gross yield versus the RBA rate. Even with franking credits, the gross-up may only bring the effective yield to roughly par with term deposit rates, without the capital risk.

- Franking credit benefit. For investors in lower tax brackets or zero-tax pension phase, franking credits remain genuinely valuable, though the benefit narrows as the base yield compresses.

- Payout ratio sustainability. With earnings growth weak, the elevated payout ratio leaves limited buffer for real dividend growth after inflation. The AFR listed Woolworths in February 2026 among “expensive yield plays” where low ROE and high payout “leave little buffer if earnings falter.”

The dividend is likely safe. Whether it is compelling is a different question.

Broker opinion, regulatory risk, and the competitive pressures Aldi keeps applying

Broker consensus on Woolworths is genuinely divided, and the split itself is instructive. The constructive houses see a dominant franchise deserving a premium; the neutral houses see a valuation that already reflects that dominance without leaving room for upside.

| Broker | Rating | 12-Month Price Target | Key Thesis |

|---|---|---|---|

| Goldman Sachs | Buy | A$37.00 | Dominant franchise; defensive cashflows |

| Morgans | Accumulate | A$37.30 | Scale advantages; cost-out upside |

| UBS | Hold (Neutral) | A$34.50 | Valuation “full versus COL on FY26 earnings” |

| Macquarie | Hold | A$33.50 | Earnings risk from competition and regulatory scrutiny |

The consensus average target of approximately A$34.68-$34.91 implies minimal upside from the current share price. When the average broker target sits within a few percent of where the stock trades, the market is effectively saying there is no obvious margin of safety.

The regulatory and competitive environment explains why even constructive brokers are not projecting dramatic gains:

- ACCC supermarket pricing inquiry. The inquiry into pricing practices, gross margins, and supplier treatment remains ongoing. No forced structural changes have been announced, but headline risk persists and the potential for mandatory codes or penalties has not been ruled out.

- Parliamentary scrutiny. Federal hearings into supermarket pricing in 2025-2026 have kept political pressure elevated, with market concentration (WOW and Coles combined exceeding 60% share) a recurring focus.

- Aldi’s store rollout. Aldi continues to expand via price leadership and new store openings, holding mid-teens market share. Coles has simultaneously stepped up promotional intensity, leaving Woolworths competing on multiple fronts with limited scope for price-led margin expansion.

The ACCC pricing conduct ruling against Coles in May 2026, which found promotional timing breaches while clearing the price increases themselves as commercially justifiable, illustrates the specific type of regulatory exposure the inquiry has created for both major supermarkets, with civil penalty risk remaining unresolved.

Macquarie has explicitly flagged earnings risk from these dynamics. Even Goldman Sachs’ constructive case rests on a benign regulatory outcome, and that is far from guaranteed.

The next major ASX story will hit our subscribers first

A 12% gain and a full valuation: what WOW’s risk-reward looks like from here

The analytical threads across this piece converge on a single observation: Woolworths trades on a premium valuation at a moment when the financial metrics underpinning that premium are at their weakest in years. The forward P/E in the low-to-mid-20s sits alongside 1.9% ROE, 300% debt-to-equity, a dividend yield below the cash rate, and a consensus price target implying minimal upside.

Morningstar retains a narrow economic moat rating on the stock but notes shares trade at a premium to assessed fair value. Ord Minnett (Accumulate, target A$37.00) argues the premium multiple is “justified by dominant franchise and defensive cashflows” despite the low ROE. Multiple Australian equity managers, by contrast, are underweight staples, characterising Woolworths as an “expensive bond proxy.”

What the bull case requires:

- Sustained earnings recovery under Amanda Bardwell, with cost-out programmes delivering meaningful margin improvement

- Regulatory outcomes from the ACCC inquiry and parliamentary scrutiny that prove benign

- Aldi failing to accelerate market share gains, preserving Woolworths’ 35%+ grocery share

What the bear case rests on:

- ROE remaining depressed in low single digits, confirming the capital efficiency problem as structural rather than cyclical

- Leverage preventing financial flexibility precisely when competitive or regulatory conditions demand it

- The yield advantage evaporating further relative to cash and fixed income alternatives

Investors considering Woolworths at current levels are not choosing between a strong investment and a weak one. They are making a judgement about how much of the optimistic scenario is already priced in at A$33.50.

Investors wanting to stress-test the bull case against historical precedent will find our deep-dive into the contrarian case for consumer staples, which examines valuation gaps between staples and technology sectors, Morningstar and Magellan fund manager positioning, and the historical return data from the dot-com and GFC cycles when defensives re-rated from similarly depressed relative valuations.

WOW’s moat is real, but the price for accessing it has rarely been this complicated

Woolworths retains genuine structural advantages: over 35% grocery market share, a fully franked dividend history, supply-chain scale efficiencies, and the demand stability that comes with selling food and everyday essentials. None of that is in dispute.

What is in dispute is whether those advantages, at their current level of financial expression, justify the multiple investors are being asked to pay. An ROE of 1.9%, leverage at 300%, a forward yield that trails the risk-free rate, and a regulatory environment that caps the margin expansion scenario all argue for caution.

Amanda Bardwell faces a multi-variable challenge: restoring capital efficiency, managing a leveraged balance sheet, navigating regulatory scrutiny, and competing with Aldi simultaneously. Investors buying at current levels are, in effect, backing that execution.

Woolworths is not a simple sell, nor a simple buy. But investors treating it as a default defensive holding should revisit the assumptions that justified that posture before the financial profile deteriorated to its current state. The full FY25 annual results (available via the Woolworths Group Investor Centre) and a comparison of the forward yield against current term deposit and bond rates would be a practical starting point.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.