Why Your ETF Portfolio May Be Less Diversified Than You Think

8 mins ago

From 1 July 2027, the 50% capital gains tax discount that Australian investors have relied on for more than two decades will be replaced by a system that taxes only inflation-adjusted gains, but imposes a 30% minimum rate on those gains regardless of the investor’s marginal tax bracket. The Albanese Government’s 2026-27 Federal Budget, delivered on 12 May 2026, announced the most significant restructuring of Australia’s capital gains tax framework since the Howard-era introduction of the discount in 1999. The reform affects individuals and trusts holding shares, property, and other capital assets, though it is not yet legislated; draft legislation had not been released as of 16 May 2026.

What follows is an explanation of exactly how the new system works mechanically, how it compares to the current 50% discount through worked dollar examples, what the grandfathering arrangement means for assets already held, and why long-term investors face a calculation complexity that the Australian Taxation Office (ATO) has not yet fully addressed.

The 50% CGT discount has been unchanged since September 1999. It was designed as a rough proxy for inflation relief: rather than requiring taxpayers to calculate the real value of their gains, the government simply halved the nominal gain and taxed the remainder at the investor’s marginal rate. The Albanese Government’s position, outlined in the Budget fact sheet “Negative Gearing and Capital Gains Tax Reform” published at budget.gov.au, is that the discount has become an over-generous concession that rewards asset holders regardless of whether their gains reflect genuine economic value or simply rising prices.

The Budget fact sheet on CGT reform, published at budget.gov.au on 12 May 2026, sets out the Government’s rationale that the 50% discount has become an over-generous concession that rewards asset holders regardless of whether gains reflect genuine economic value or simply rising price levels.

The replacement is a two-part structure:

The structural contrast is direct: the old system applied a flat 50% reduction to the nominal gain; the new system calculates the real gain first, then taxes it at a minimum of 30%.

The 30% minimum floor also dismantles a retirement income timing strategy that allowed some investors to pay as little as 8.25% effective CGT by timing asset disposals to years when their taxable income was low, a planning technique that the new minimum rate renders ineffective regardless of the investor’s income in the disposal year.

Superannuation funds are excluded from the new regime, preserving their existing concessional CGT treatment. The reform applies to individuals and trusts, and the 1 July 2027 commencement date gives a window of over 14 months between the announcement and when the new rules take effect.

Cost-base indexation means the original purchase price of an asset is multiplied by the change in the Consumer Price Index between the date of acquisition and the date of disposal. The result is an inflation-adjusted cost base, and only the amount by which the sale price exceeds this adjusted figure is treated as a taxable capital gain. The concept itself is not new to Australian tax law: it existed for assets acquired before 21 September 1999, when indexation factors were frozen at the September 1999 CPI quarter and replaced by the 50% discount. The reform reintroduces ongoing annual CPI adjustment.

The ATO indexation guidance for pre-1999 assets documents the methodology that was frozen at the September 1999 CPI quarter when the 50% discount was introduced, providing a direct reference point for the calculation approach the new regime is reactivating and extending to all post-12-month disposals.

The calculation follows three steps:

To illustrate the effect of indexation alone: the ABS Consumer Price Index rose by approximately 32% cumulatively between 2015 and 2025. An asset purchased for $100,000 in 2015 would have an indexed cost base of approximately $132,000 by 2025, meaning only the portion of the sale price above $132,000 would be treated as a taxable gain under the new system.

The interaction between a low-inflation environment and the 30% floor deserves particular attention: as the RBA works to bring inflation back toward its 2-3% target band, annual CPI uplifts to the cost base will be modest, meaning a larger share of nominal gains will be treated as real gains and exposed to the minimum rate.

The ATO maintains an existing indexation factor table for the pre-1999 regime, and the ABS publishes CPI quarterly (catalogue 6401.0), with the most recent release being the March quarter 2026 (published April 2026).

As of 16 May 2026, Treasury has not specified whether the ABS headline CPI series or a specific sub-index will be used as the reference series for cost-base indexation under the new regime. This detail is expected in forthcoming consultation papers or draft legislation.

The distinction is material. Different CPI series produce different indexation factors, and every tax calculation under the new regime depends on this input. Investors and advisers should monitor Treasury’s consultation releases for clarity on this point.

The clearest way to understand the reform’s effect is to run the same asset through both systems. Two examples follow: one relatively short-hold exchange-traded fund (ETF) investment, and one longer-hold property investment.

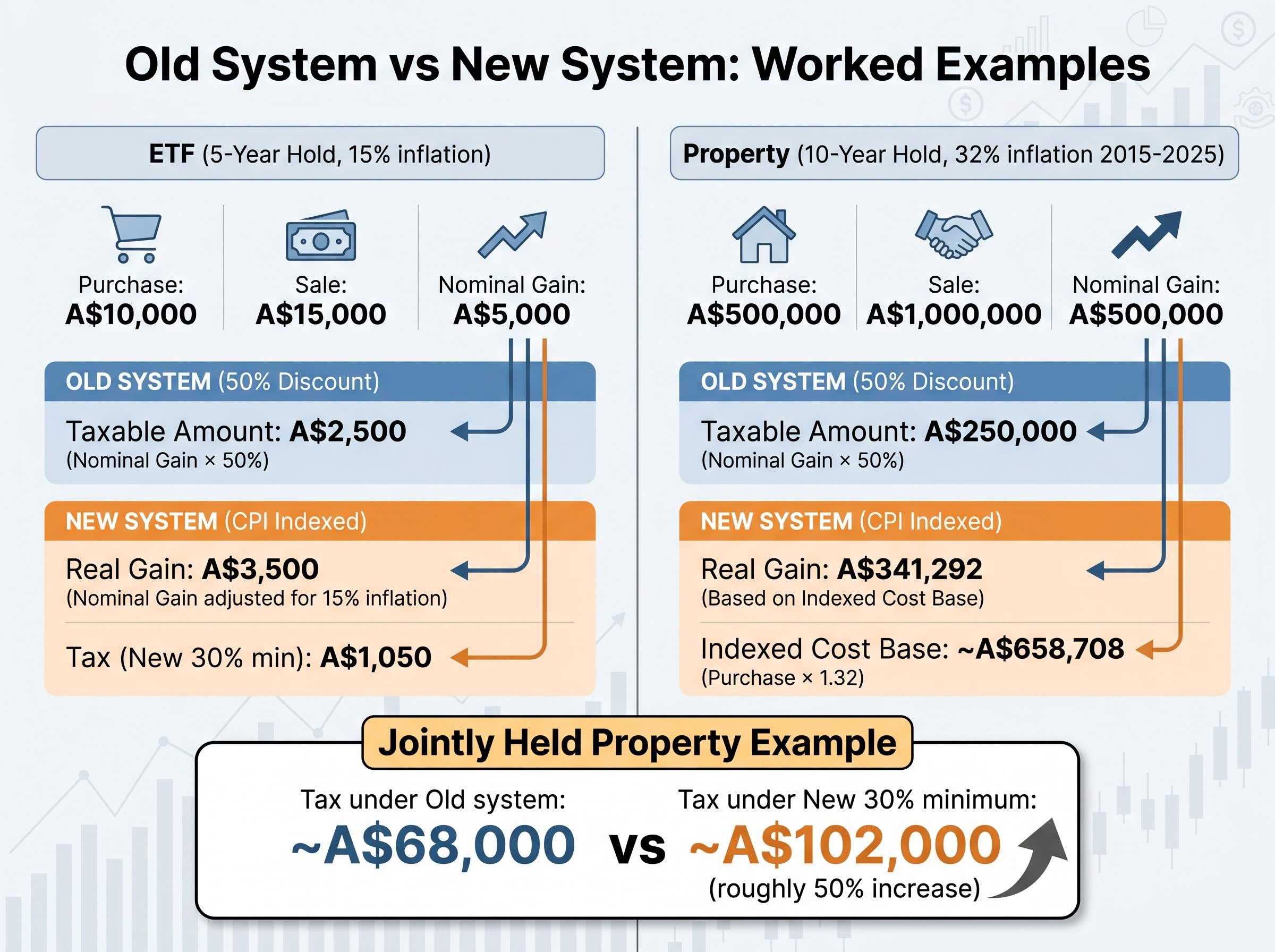

Example 1: ETF held for five years. An investor purchases an ETF for $10,000. After five years and 15% cumulative inflation, the ETF is sold for $15,000, producing a nominal gain of $5,000.

Under the old system, the 50% discount reduces the taxable gain to $2,500, taxed at the investor’s marginal rate. Under the new system, the indexed cost base is $11,500 (original cost multiplied by 1.15), producing a real gain of $3,500. The 30% minimum tax on $3,500 yields tax of $1,050.

Example 2: Property held for ten years. A property is purchased for $500,000 in 2015 and sold for $1,000,000 in 2025, with cumulative CPI inflation of approximately 32% over the decade.

| Metric | ETF (5-Year Hold) | Property (10-Year Hold) |

|---|---|---|

| Purchase Price | $10,000 | $500,000 |

| Sale Price | $15,000 | $1,000,000 |

| Nominal Gain | $5,000 | $500,000 |

| Taxable Amount (Old: 50% Discount) | $2,500 | $250,000 |

| Real Gain (New: CPI Indexed) | $3,500 | $341,292 |

The property example exposes the asymmetry at work. The indexed cost base (approximately $658,708) shelters a larger dollar amount of the gain than the old 50% discount, because cumulative inflation over a decade is substantial. The taxable gain under the new system ($341,292) is, however, larger than the discounted gain under the old system ($250,000). Combined with the 30% minimum tax floor, the new system produces a higher tax outcome in this scenario.

For a jointly held property (two owners splitting the gain equally), the combined tax payable under the old system would be approximately $68,000 at the top marginal rate with the 50% discount applied. Under the new 30% minimum, the combined tax rises to approximately $102,000, an increase of roughly 50% in the tax burden for this scenario.

The direction of the difference depends on the interplay between cumulative inflation and asset growth. In high-growth, high-inflation scenarios, the new system’s larger indexed cost base does not fully offset the 30% minimum rate when the old discount would have produced a lower effective rate.

The final after-tax outcome under the new system is also sensitive to the investor’s income bracket and holding period in ways the old 50% discount was not, because the interaction between the indexed cost base and the 30% minimum floor produces different effective rates depending on when the asset was purchased relative to high-inflation or low-inflation periods.

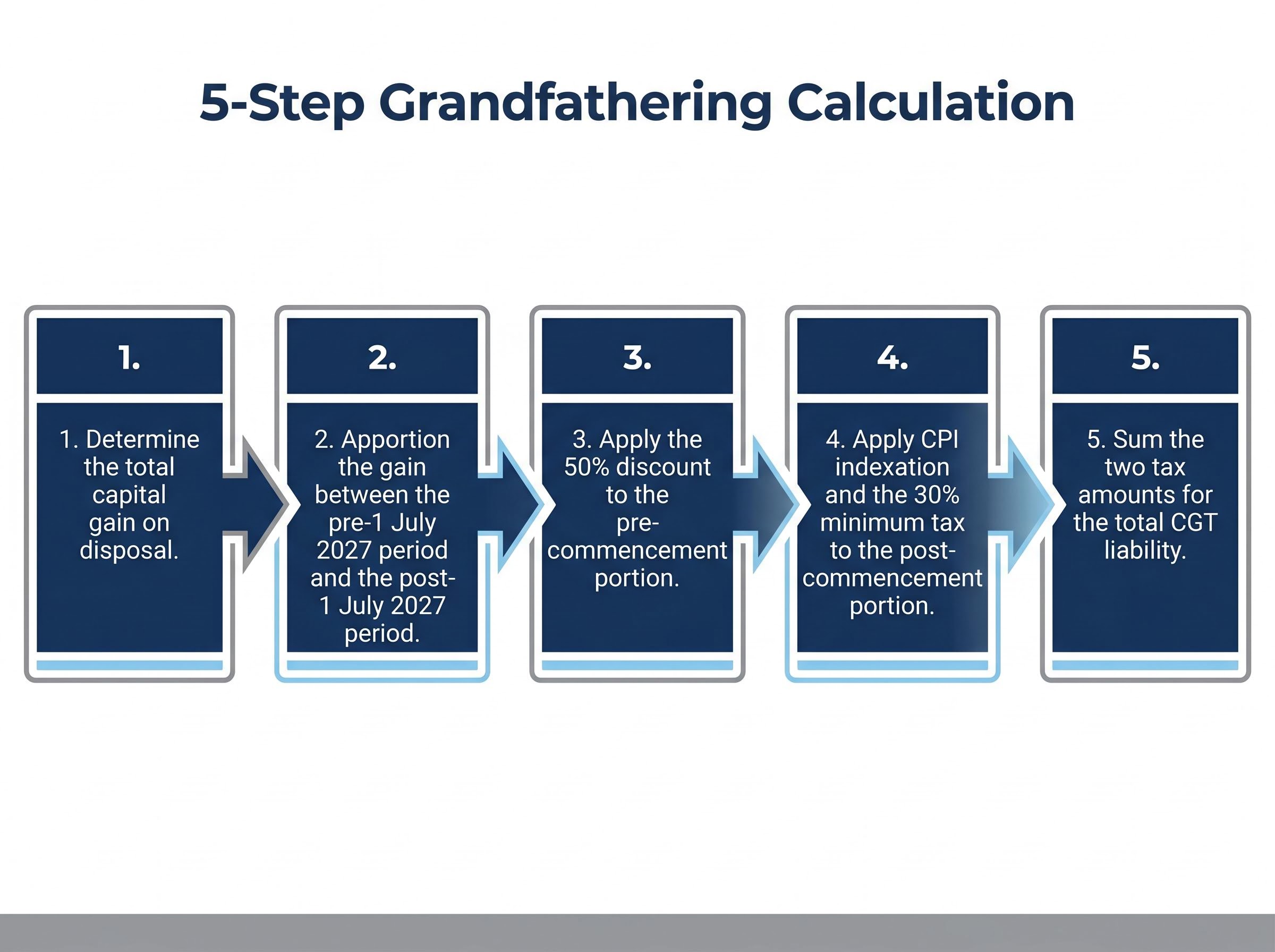

The apparent good news is straightforward: gains that accrued before 1 July 2027 on assets already held continue to be assessed under the current 50% discount rules. The new indexation method applies only to gains accruing from 1 July 2027 onward on those same assets.

The complication is in the execution. Investors who acquired an asset before 1 July 2027 and sell it after that date must perform a dual calculation, apportioning the total gain between two periods and applying different treatment to each. The steps are:

As of 16 May 2026, the ATO has not released any draft guidance, Practical Compliance Guideline, or Law Companion Ruling on the methodology for this dual calculation. Professional commentary from KPMG, Baker McKenzie, and EY has identified the dual-calculation requirement as a significant compliance burden for both advisers and individual investors. The ATO’s existing CGT pages reflect current law only.

CPI indexation requires two verified inputs: the original cost base and the acquisition date. These are the numbers that determine the indexation factor, and without them the calculation cannot be performed.

For assets acquired many years ago, records may be incomplete or informal. A share parcel purchased through a broker in 2005 may have a clear contract note on file; a property inherited in 1998 may not. The shift to indexation raises the stakes for record accuracy because the cost base is no longer simply halved. It is adjusted by a precise multiplier that depends on the documented purchase price.

The ATO’s existing CGT record-keeping guidance remains available at ato.gov.au, but it has not yet been updated for the new regime.

Several elements of the CGT framework are confirmed as unchanged. The main residence CGT exemption continues to apply. Superannuation funds retain their existing concessional CGT regime and are not subject to the new rules.

A transitional election for new residential properties allows investors to choose between the old 50% discount treatment and the new indexation plus 30% minimum. The precise mechanics of this election, including the form, timing, and whether it is irrevocable, had not been released as of 16 May 2026.

The material unknowns extend well beyond the residential election. The following issues remain outstanding and are expected to be addressed in forthcoming Treasury consultation papers and draft legislation:

| Unresolved Issue | Expected Resolution Path |

|---|---|

| Specific CPI series for indexation | Treasury consultation paper or draft legislation |

| Dual-calculation methodology guidance | ATO Practical Compliance Guideline or Law Companion Ruling |

| Residential property transitional election mechanics | Draft legislation and explanatory memorandum |

| Interaction with superannuation fund CGT concessions | Treasury consultation paper and draft legislation |

| Interaction with welfare means-testing (JobSeeker, Age Pension) | Treasury consultation paper and cross-agency guidance |

| Draft legislation and explanatory memorandum | Parliament bills list (aph.gov.au) and Federal Register of Legislation |

Knowing which elements are settled and which remain open prevents investors from making premature decisions based on incomplete information. This table also serves as a practical checklist for monitoring forthcoming guidance.

The gap between the Budget announcement and the 1 July 2027 commencement date is more than 14 months. That is meaningful time, but only if it is used deliberately. Three actions can be taken now, without waiting for ATO guidance:

For investors who have identified assets where pre-2027 timing may be worth reviewing, our comprehensive walkthrough of CGT planning strategies for 2027 covers low-turnover ETF structures, superannuation contribution capacity, and terminal wealth modelling over a 30-year horizon that quantifies the compounding cost of the new 30% minimum floor.

This reform is Budget-announced policy only. It has not been legislated. Draft legislation had not been released as of 16 May 2026, and further amendment remains possible before any law passes through Parliament.

Investors considering disposal or restructuring decisions should engage a qualified tax adviser before acting on the proposed changes. Major advisory firms including KPMG, Baker McKenzie, and EY have published initial Budget analysis that may be useful for understanding the reform’s direction.

The move from a flat percentage discount to real-gains taxation is structurally different because the tax outcome now depends on both inflation and asset growth, not simply the holding period and the nominal gain. That is a more precise system, but also a more complex one.

Major mechanical details remain unresolved. Investors relying on early estimates, including the worked examples in this article, should treat them as directional rather than definitive until draft legislation is released and ATO guidance follows.

What is clear is that this reform rewards informed preparation. Record-keeping, adviser engagement, and monitoring of the legislative process are the three areas where the time between now and July 2027 is most valuable. Bookmarking the ATO consultation page and the Parliament bills list provides a direct line to material updates as they are released.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. The CGT reform discussed has been announced as Budget policy but has not been legislated. Further amendment remains possible, and all calculations are based on announced parameters as of 16 May 2026.

—

From 1 July 2027, the existing 50% CGT discount will be replaced by a system that indexes the cost base of an asset to CPI and taxes only the inflation-adjusted gain, with a 30% minimum tax rate applied to that real gain for assets held more than 12 months.

The original purchase price of an asset is multiplied by the change in the Consumer Price Index between the acquisition date and the disposal date, producing an inflation-adjusted cost base; only the amount by which the sale price exceeds this indexed figure is treated as a taxable capital gain.

Gains that accrued before 1 July 2027 on assets already held will continue to be assessed under the current 50% discount rules, but gains accruing after that date on the same assets will be subject to CPI indexation and the 30% minimum tax, requiring investors to perform a dual calculation when they eventually sell.

No, superannuation funds are excluded from the new regime and retain their existing concessional CGT treatment; the reform applies to individuals and trusts only.

Investors should audit and verify acquisition records and original cost bases for all CGT assets, consider discussing pre-2027 disposal timing with a qualified tax adviser, and monitor ATO consultation updates and the Parliament bills list at aph.gov.au for forthcoming draft legislation and guidance.