How to Manage AI Stock Concentration Risk in Your Portfolio

4 hrs ago

From 7:30pm AEST on 12 May 2026, the rules governing how Australians profit from property and shares outside superannuation changed. Treasurer Jim Chalmers’ 2026-27 federal budget introduced two interlocking reforms: restrictions on negative gearing for established residential properties and a replacement of the 50% capital gains tax discount with a new indexation model carrying a 30% minimum tax on real gains. The negative gearing changes apply to purchases made after budget night; the capital gains tax overhaul commences 1 July 2027. Both measures affect individuals, trusts, and partnerships, but leave superannuation funds untouched. The question for Australian investors is no longer whether these capital gains tax changes in Australia matter, but how quickly they can understand what the reforms mean for their own portfolios. This explainer breaks down exactly what changed, who is affected, how the new rules alter after-tax returns across property and equity strategies, and what strategic options investors should be weighing before the 1 July 2027 commencement date.

The 2026-27 budget delivered two distinct but connected reform pillars, each with its own commencement date and scope. Understanding which reform applies to which asset class, and when, is the necessary first step before assessing any personal exposure.

Both measures are confirmed budget announcements, supported by the official government factsheet “Negative Gearing and Capital Gains Tax Reform” and Budget Paper No. 1. However, as of 17 May 2026, no enabling legislation has been tabled in Parliament. The reforms remain announced policy, not yet enacted law. Final rules depend on legislation expected in coming months.

The approximately 13-month window between budget night and 1 July 2027 is both the legislative runway and the strategic planning period for investors.

The reforms carry more weight when measured against the system they replace. Two longstanding concessions, negative gearing and the CGT discount, shaped how Australian investors structured property and equity portfolios for decades. Understanding their mechanics makes the scale of the disruption immediately visible.

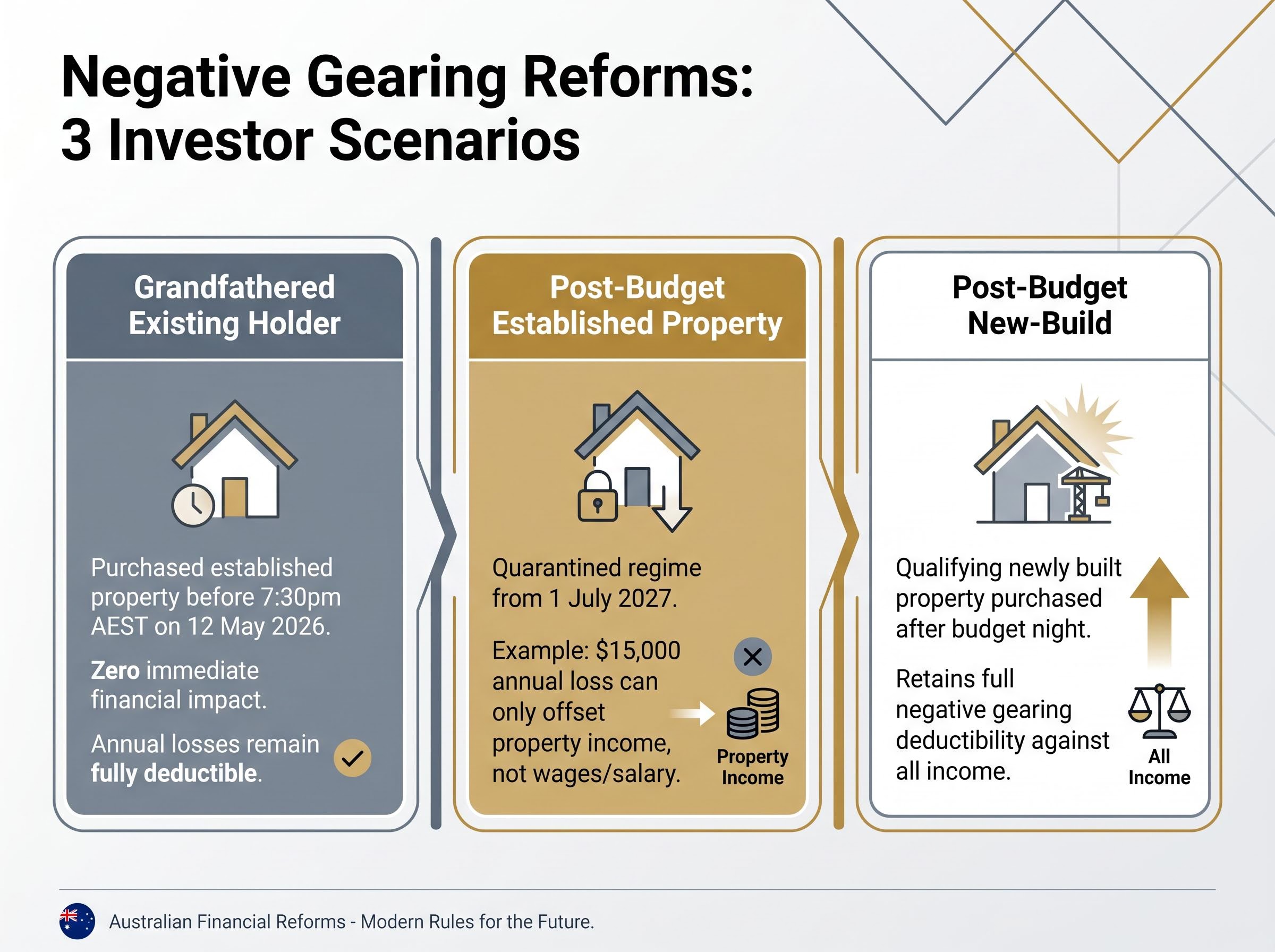

Under the old rules, an investor who borrowed to purchase a rental property could deduct the full shortfall between rental income and holding costs (loan interest, maintenance, depreciation) against all other income, including wages and salary. A high-income earner on a 47% marginal tax rate who generated a $20,000 annual loss on an investment property could reduce their taxable salary income by that same $20,000, producing a meaningful annual tax benefit. This treatment applied equally to established and newly built properties, with no distinction between the two.

When an individual, trust, or partnership sold an asset held for more than 12 months, only half the capital gain was added to assessable income. The remaining 50% was disregarded entirely. For a high-income investor on the top marginal rate, the effective CGT rate was approximately 23.5% rather than 47%. Trusts added a further planning layer: by distributing capital gains to beneficiaries on lower marginal rates, investors could reduce the effective tax burden below even the discounted rate. Superannuation funds operated under a separate regime (a 15% tax rate with a one-third discount for assets held over 12 months), and that regime remains unchanged by this budget.

The government has framed the new approach as more economically neutral, arguing that cost-base indexation taxes only real gains rather than rewarding nominal price increases with a blanket discount.

| Feature | Old rules | New rules (from 1 July 2027) |

|---|---|---|

| Negative gearing (established property) | Losses deductible against all income | Losses quarantined to property income only (post-budget purchases) |

| CGT treatment (individuals, trusts, partnerships) | 50% discount on gains held over 12 months | Cost-base indexation plus 30% minimum tax on real gains |

| Superannuation CGT treatment | 15% tax, one-third discount (assets held over 12 months) | Unchanged |

Policy language becomes practical when applied to real positions. Three investor profiles illustrate how the quarantining mechanic operates in practice, and where it changes nothing at all.

The distinction between contract date and settlement date matters. According to the budget factsheet, the relevant trigger is the contract date, not settlement. Investors who exchanged contracts before 7:30pm AEST on 12 May 2026 fall under the grandfathered regime regardless of when settlement occurs. The exact definitional boundaries of “newly built” are subject to forthcoming legislation, a detail that will be material for investors weighing new-build purchases in the months ahead.

The CGT reform reaches well beyond property. From 1 July 2027, every CGT asset held outside superannuation by an individual, trust, or partnership falls under the new framework. That includes equities, shares, and REITs.

The mechanical shift works in two parts. First, cost-base indexation adjusts the original purchase price of an asset for inflation before the gain is calculated. If an investor bought shares for $100,000 and inflation over the holding period totalled 15%, the indexed cost base becomes $115,000. Only the gain above that indexed cost base is taxable, meaning the tax applies to the real (above-inflation) gain rather than the full nominal gain.

Second, a 30% minimum tax applies to that real gain. Regardless of the investor’s marginal rate or how the gain is distributed through a trust structure, the effective tax rate on the indexed gain cannot fall below 30%.

CGT transitional rules split gains at the 1 July 2027 date, with pre-reform gains still eligible for the 50% discount and only post-reform gains subject to indexation and the new 30% floor, though the precise methodology for calculating this split has not yet been legislated and will significantly affect after-tax outcomes for investors holding assets across the transition date.

KPMG’s Federal Budget 2026 analysis noted that the 30% minimum closes the planning strategy of distributing capital gains to low-tax beneficiaries through trusts, a structure that many Australian investors have relied upon to reduce their effective CGT burden below the discounted rate.

RSM Global’s budget analysis, released three days after the announcement, specifically modelled how the 30% minimum tax floor interacts with trust distribution strategies, confirming that the rate advantage previously available by streaming gains to low-tax beneficiaries is eliminated under the new framework.

For share investors and REIT holders, this is a direct reassessment trigger. An investor who previously paid an effective rate of approximately 23.5% on discounted gains (at the top marginal rate) now faces a 30% floor on real gains, and investors who used trust distributions to reduce the rate further face a larger adjustment.

| Scenario | Old framework (50% discount) | New framework (indexation + 30% min.) |

|---|---|---|

| Nominal gain | $100,000 | $100,000 |

| Inflation adjustment (5 years, ~15%) | Not applicable | Indexed cost base reduces gain to ~$85,000 |

| Taxable gain | $50,000 (after 50% discount) | ~$85,000 (real gain after indexation) |

| Tax at 47% marginal rate | ~$23,500 | ~$25,500 (30% minimum on $85,000) |

Commentary from Stockspot’s CGT calculator (published 12 May 2026) suggested that early modelling points to superannuation becoming relatively more attractive for long-term equity holdings under the new framework. In certain cases, new-build investors may also choose between the old 50% discount rules or the new indexation framework, a transitional concession designed to preserve the new-build incentive.

The reforms create clear winners and losers across Australian investor profiles.

Better positioned after the reforms:

More exposed after the reforms:

Baker McKenzie’s “Budget Bites” analysis (published 12 May 2026) flagged that a trust structure review is now a priority for investors using discretionary trusts for investment properties or share portfolios.

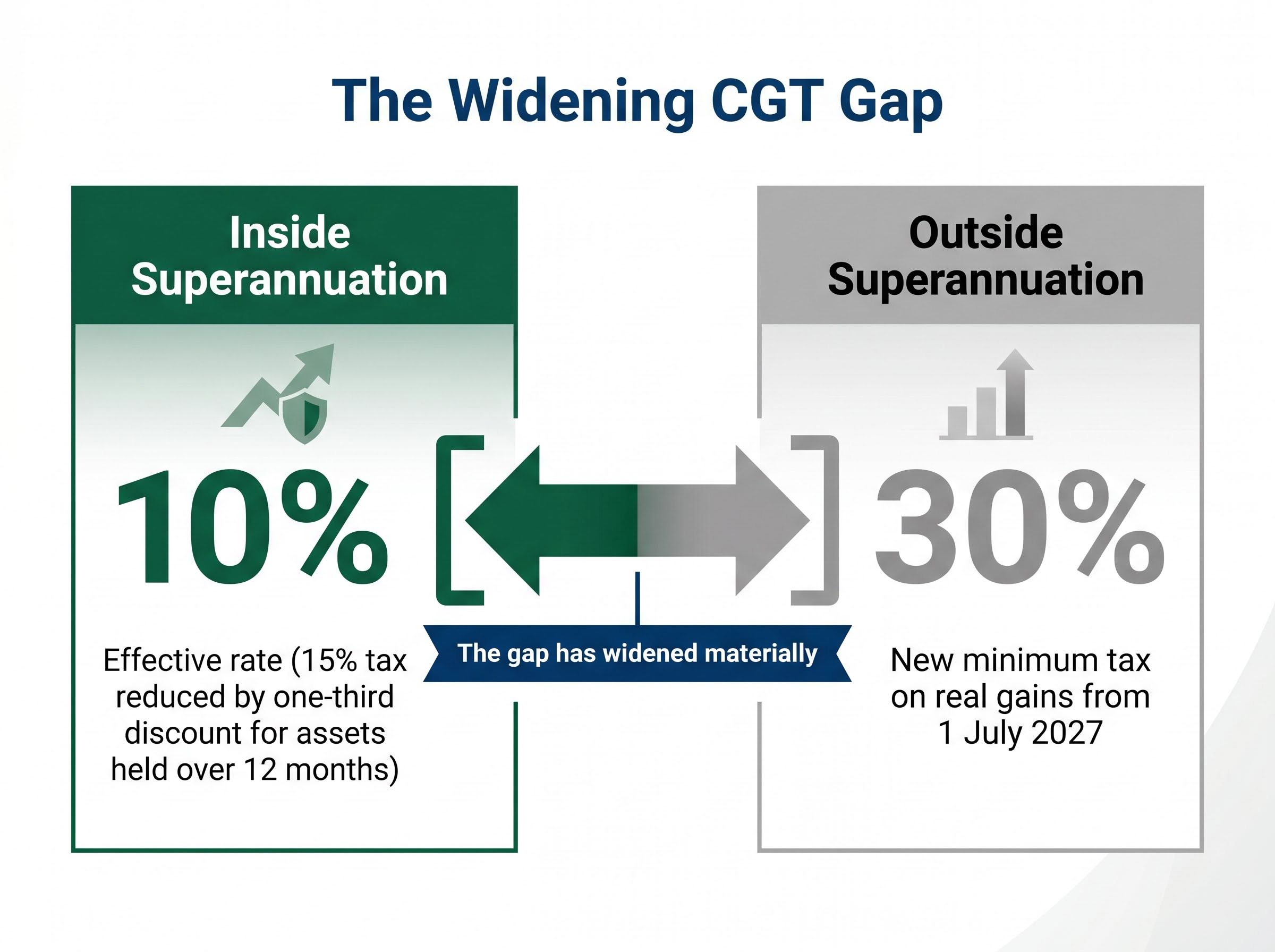

The CGT rate differential between superannuation and non-superannuation holdings has widened materially. Inside super, an investor pays 15% tax on capital gains, reduced by a one-third discount for assets held over 12 months, producing an effective rate of 10%. Outside super, the new minimum is 30% on real gains from 1 July 2027.

That gap, from roughly 10% inside super to 30% outside, is the widest the structural differential has been. Early commentary in the Australian Financial Review and The Guardian identified superannuation as the primary structural beneficiary of the reform package.

The Guardian Australia’s budget coverage, published the day after the announcement, identified superannuation as the primary structural beneficiary of the reform package, a conclusion consistent with the widened CGT rate differential that now separates super holdings from assets held outside the fund.

Contribution caps and access restrictions still apply, making superannuation unsuitable as a sole response. But for investors with capacity to contribute, the after-tax return gap has widened enough to warrant a serious reassessment of where long-term equity and property holdings sit.

The 13-month window between budget night and 1 July 2027 is finite, and the decisions available now may narrow once legislation is finalised. Four strategic levers deserve attention:

A superannuation contribution strategy that uses carry-forward concessional cap space, available to investors with balances below $500,000 who have unused cap room from the prior five years, can allow contributions well above the standard $30,000 annual limit in a single financial year, making the 13-month planning window before 1 July 2027 particularly valuable for mid-career investors with available cap space.

The measures have not yet been enacted. No enabling legislation had been tabled in Parliament as of 17 May 2026, and the precise drafting of definitions, particularly “newly built” and the indexation methodology, will be material to planning decisions. Investors should factor legislative uncertainty into any pre-commencement strategy.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding future tax treatment are based on announced budget policy and are subject to change based on the final form of enabling legislation.

Both reforms are announced policy, not yet law. That distinction matters. It creates a planning window that investors should use actively rather than wait out.

The core asymmetry is straightforward: grandfathered investors face no immediate change to existing holdings, but anyone making new investment decisions, whether in property, equities, or trust structures, now operates under a materially different after-tax return framework.

The 13 months before 1 July 2027 will see legislation drafted, consulted upon, and debated. Definitions will be sharpened. Transitional rules will be finalised. Investors who engage with their tax position now, with qualified advice specific to the new regime, will have more options than those who wait until the rules are already in force.

Investors exploring the precise dollar cost of these changes across different investor profiles will find our full explainer on the after-tax wealth impact, which models the specific reduction in proceeds for a leveraged property investor, a business founder realising a $1 million exit, and the unresolved interaction between the 30% CGT floor and Division 152 small-business concessions that remain the single most consequential unknown for owners approaching succession.

From 1 July 2027, the existing 50% CGT discount for individuals, trusts, and partnerships will be replaced by a cost-base indexation model that taxes only real (inflation-adjusted) gains, with a 30% minimum tax rate applying to those gains. Superannuation funds are not affected by this change.

The negative gearing quarantine applies to established residential properties purchased after 7:30pm AEST on 12 May 2026, with the formal restriction taking effect from 1 July 2027. Losses on these properties can no longer be offset against wages or salary, only against other property income.

Under the new framework, the effective tax rate on indexed capital gains cannot fall below 30%, regardless of how gains are distributed through a discretionary trust to low-tax beneficiaries. This eliminates the rate advantage that many Australian investors previously used to reduce their effective CGT burden below the discounted rate.

Yes, investors who purchase a qualifying newly built residential property after budget night retain full negative gearing deductibility against all income, including wages and salary, identical to the treatment under the old rules. The exact definition of 'newly built' has not yet been legislated and will be clarified in coming months.

Investors have several options in the 13-month window before the new rules commence, including realising unrealised gains before 1 July 2027 under the current 50% discount, reviewing superannuation contribution strategies to take advantage of the now-wider CGT rate differential, and assessing any discretionary trust structures used for property or share portfolios.