Why a Rising AUD Is Quietly Eroding Your International ETF Returns

3 hrs ago

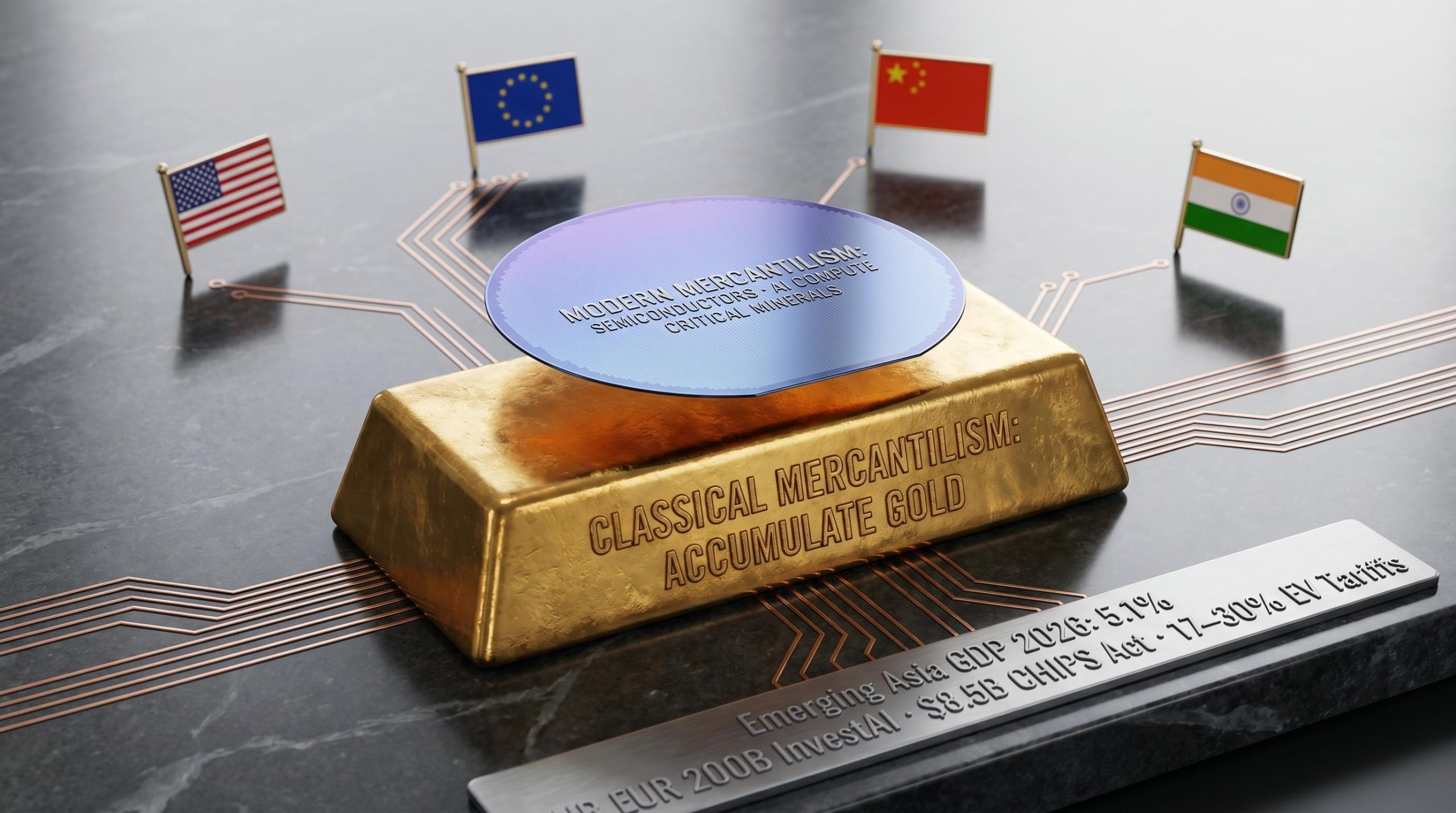

In the 17th century, nations fought wars over gold and spice routes. In 2026, the battles are over semiconductor fab capacity, AI compute, and battery chemistry. Bob Prince, Co-CIO of Bridgewater Associates, told the HSBC Global Investment Summit in Hong Kong that modern mercantilism is now one of the central structural forces reshaping global financial markets. The language has changed, the weapons have changed, but the competitive logic of states manoeuvring for economic supremacy has not.

A major intellectual and policy shift is underway. Governments in Washington, Brussels, Beijing, and New Delhi are increasingly prioritising domestic production, strategic supply chains, and economic nationalism over the free-trade consensus that shaped the post-Cold War era. The US CHIPS Act, EU anti-subsidy tariffs on Chinese electric vehicles, China’s self-reliance drive in semiconductors, and India’s production-linked incentive schemes all reflect the same impulse: state power deployed to win the industries that will define the next decade.

What follows is a precise explanation of what modern mercantilism actually means, how it differs from the history-book version, which policy tools governments are using right now, and what this structural shift means for portfolio construction in 2026 and beyond.

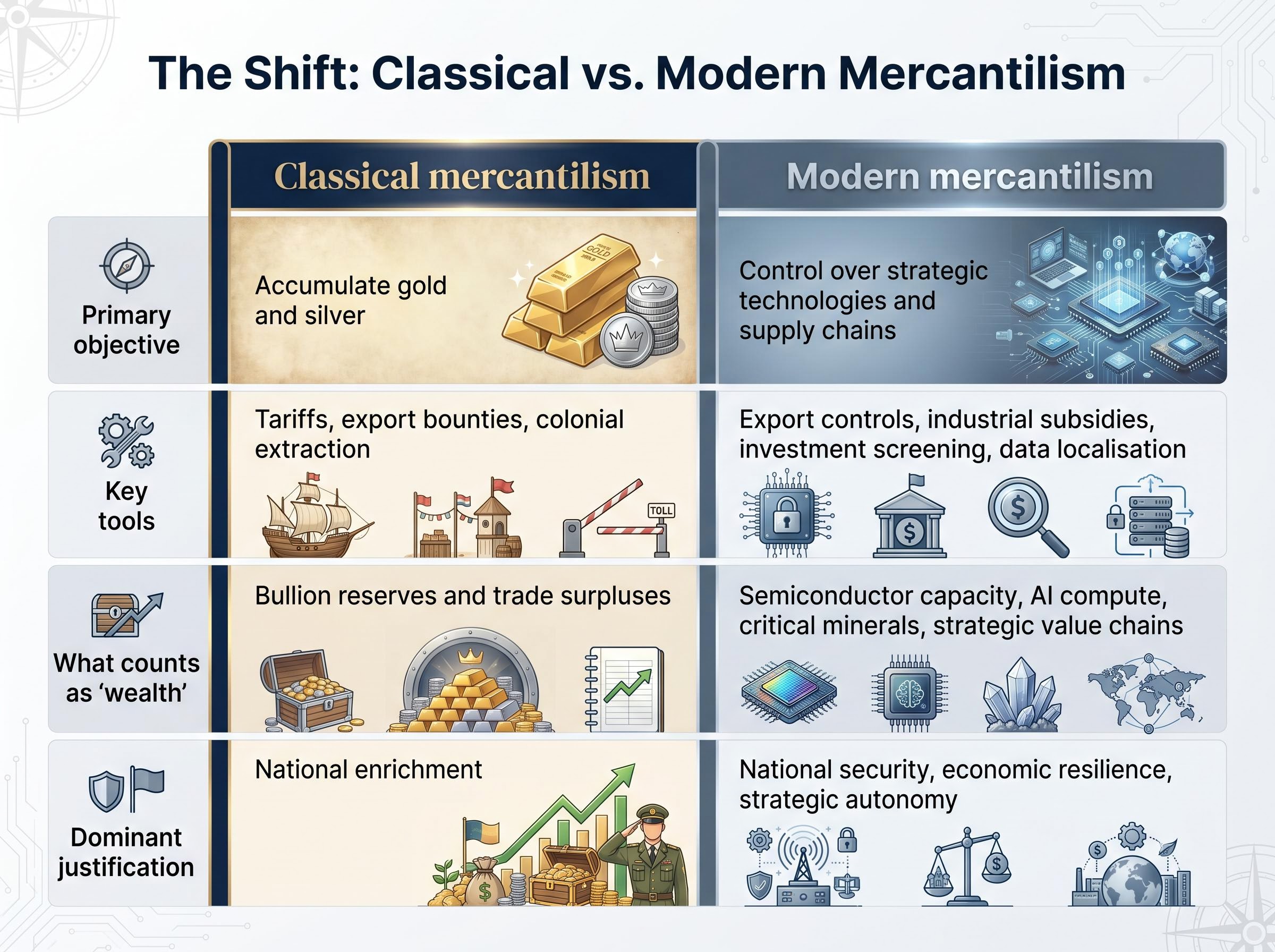

The version most readers carry from school is straightforward. Classical mercantilism, dominant in the 17th and 18th centuries, treated national wealth as a fixed stock of gold and silver. Trade was zero-sum: one nation’s surplus was another’s deficit. Governments enforced this logic through tariffs, export bounties, and colonial extraction, all aimed at hoarding bullion.

The modern version shares the competitive, state-first logic but has fundamentally different targets and tools.

The WTO World Trade Report 2024 describes a “new era of trade policy interventionism” that is “less about accumulating monetary reserves and more about securing control over key technologies, critical minerals, and strategic value chains.” Adam Posen of the Peterson Institute for International Economics characterises modern mercantilism as “the pursuit of national advantage through targeted protectionism, state direction of credit, and discrimination against foreign firms in strategic sectors.” Martin Wolf, writing in the Financial Times in March 2025, argues that governments now seek “strategic surpluses in critical goods, not just in current accounts.”

The assumption that trade creates winners and losers persists. So does the willingness to use government power to tilt outcomes. What has changed is the prize: not gold, but semiconductors, AI models, and lithium supply chains.

| Dimension | Classical mercantilism | Modern mercantilism |

|---|---|---|

| Primary objective | Accumulate gold and silver | Control over strategic technologies and supply chains |

| Key tools | Tariffs, export bounties, colonial extraction | Export controls, industrial subsidies, investment screening, data localisation |

| What counts as “wealth” | Bullion reserves and trade surpluses | Semiconductor capacity, AI compute, critical minerals, strategic value chains |

| Dominant justification | National enrichment | National security, economic resilience, strategic autonomy |

Investors who conflate modern mercantilism with old-fashioned tariff wars will misread both the nature and the durability of the shift. The distinction is not academic; it is the conceptual foundation for everything that follows.

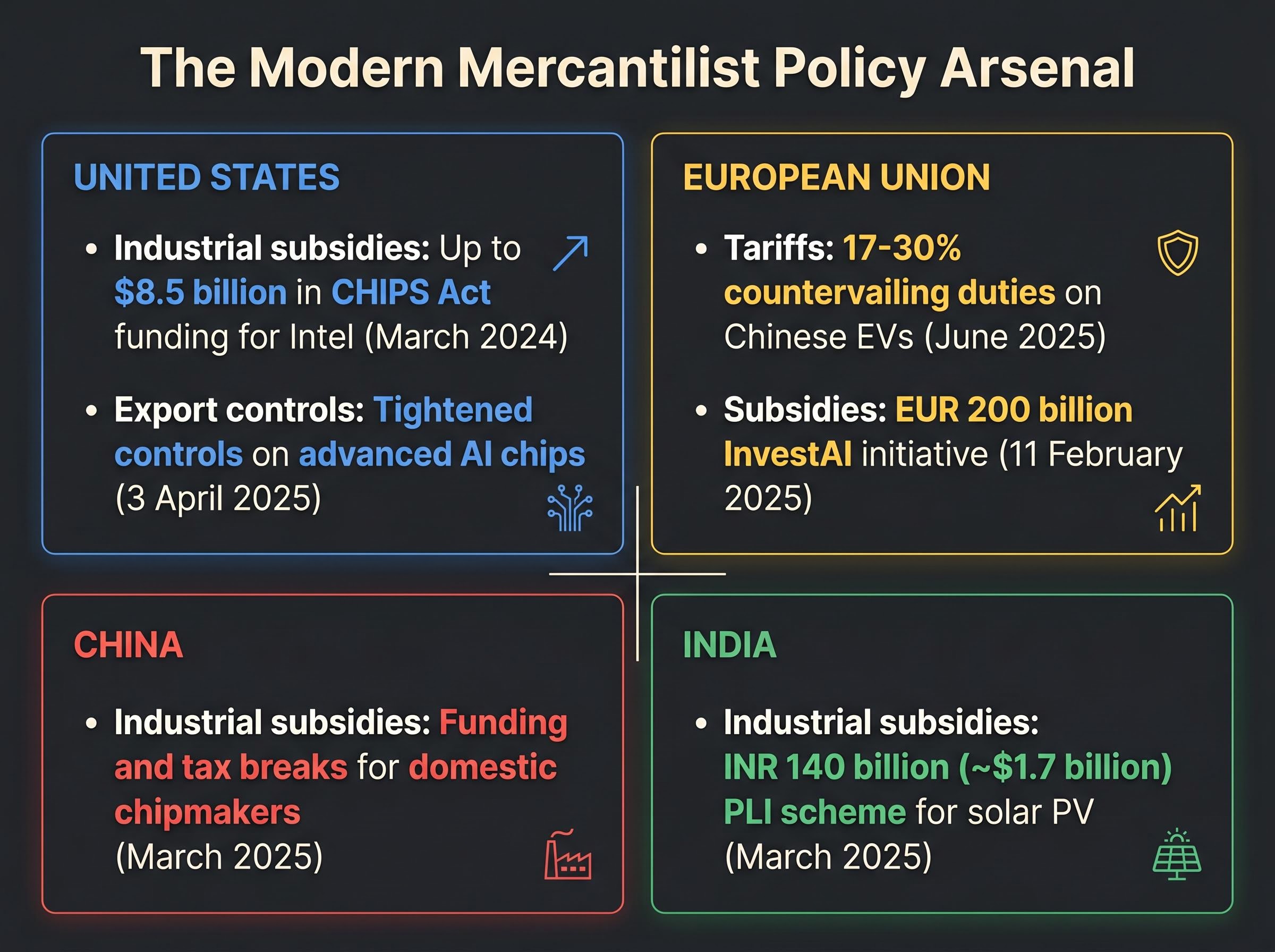

The concept becomes concrete when measured by the policy instruments in use today. Four main categories define the modern mercantilist toolkit: export controls and investment screening, industrial subsidies and local-content rules, tariffs and countervailing duties, and data and technology localisation mandates. What makes the current moment structural rather than episodic is that the US, EU, China, and India are all deploying versions of these tools simultaneously.

The WTO World Trade Report 2024 documents the cross-jurisdictional scale of industrial policy expansion, providing the empirical baseline against which the simultaneous deployment of mercantilist tools by the US, EU, China, and India can be assessed.

The WTO’s World Trade Report 2024 describes a “new era of trade policy interventionism,” a framing that captures the cross-jurisdictional scale of the shift.

United States:

European Union:

China:

India:

Knowing which instruments are being deployed, and where, tells investors which sectors and supply-chain configurations are being structurally advantaged or disadvantaged.

Legal constraints on tariff authority have introduced a new variable into the mercantilist policy calculus: two federal courts struck down the broadest IEEPA-based and Section 122-based duties within three months in 2026, shifting the effective toolkit toward Section 232 national security justifications and legislative channels, which are slower and more predictable for markets to price than executive unilateral action.

AI is not a separate trend from mercantilism. It is its most advanced expression. Governments are treating compute, data, and algorithmic capability as strategic national assets in the same way earlier generations treated coal, oil, or steel capacity.

The mercantilist tools being deployed in AI fall into three categories:

According to The Economist (September 2025), governments are “hoarding compute, subsidising chip fabs and national champions, and ring-fencing data behind sovereignty rules.”

The Brookings Institution argued in May 2025 that AI has become “a central theatre for mercantilist competition,” with policies risking fragmentation into regional AI blocs. A CSIS report described the emerging outcome: a “bifurcated AI hardware and software stack” between US-aligned and China-aligned blocs, with cost and interoperability implications for globally integrated businesses.

For investors, AI mercantilism means the sector’s returns will increasingly depend on which geopolitical bloc a company operates within, not simply on its technological capability. That is a reframe of how to evaluate AI-exposed equities, moving the analysis from product quality to jurisdictional positioning.

The Asian semiconductor beneficiaries of this AI compute competition are already delivering earnings validation at scale: Samsung reported more than an eightfold surge in Q1 2026 operating profit, SK Hynix confirmed strong AI-linked demand, and the MSCI AC Asia Pacific IT Index was trading at approximately half the forward P/E multiple of the Nasdaq 100 despite earnings growth forecasts running nearly three times faster, a valuation gap that mercantilist capex concentration is actively narrowing.

The asymmetric economic outcomes of mercantilist competition are already visible in the growth data. Asia, particularly India and ASEAN, is growing at a structurally faster rate than the US or Europe, and mercantilist supply-chain re-routing is amplifying the divergence rather than reducing it.

Regional growth divergence is not a forecast but a present reality in the data: the April 2026 composite PMI collapsed to 47.6 in eurozone services while US nonfarm payrolls beat consensus at 115,000, a split that maps directly onto the asymmetric capital flow patterns that mercantilist supply-chain rerouting is amplifying.

| Region | 2025 GDP growth | 2026 GDP growth |

|---|---|---|

| Emerging and Developing Asia | 5.3% | 5.1% |

| United States | 2.1% | 1.9% |

| Euro area | 1.4% | 1.6% |

Source: IMF World Economic Outlook Update, January 2026

Friend-shoring and supply-chain diversification away from China are directing incremental investment toward specific economies. HSBC Global Research identified “under-ownership of Asia in global portfolios relative to its growing share of world GDP and capex” in October 2025. Amundi’s 2026 outlook expressed a preference for Asia-centric regional value chains, naming specific beneficiaries:

BlackRock’s Midyear 2025 outlook adopted a position of modestly overweight US and Asia ex-Japan equities, while underweight on the euro area, citing better earnings growth and industrial-policy tailwinds. IIF Capital Flows Tracker data from March 2026 showed robust non-resident portfolio flows into EM Asia versus more volatile flows into EM Europe and Latin America.

Europe faces specific headwinds: elevated energy costs, weaker industrial policy relative to the US, demographic constraints, and exposure to export-dependent manufacturing sectors now confronting tariff and subsidy competition from multiple directions.

Regional divergence is where mercantilism translates most directly into differential equity returns, currency dynamics, and capital flow patterns.

At the HSBC Global Investment Summit, Bridgewater’s Bob Prince identified two portfolio qualities as responses to a changing, less predictable global order: diversification and agility. In a mercantilist world, both mean something different from what they meant in the free-trade era.

Conventional diversification spread capital across stocks, bonds, and alternatives. Mercantilist fragmentation demands an additional dimension: diversification across geopolitical blocs, supply-chain configurations, and currency systems.

Bridgewater argued in March 2026 that “neutral” benchmarks underweight real assets and Asia relative to where future nominal growth is likely to be, recommending “balanced exposures across competing blocs.” State Street Global Advisors’ 2026 outlook recommended diversifying funding currencies beyond the dollar and euro, identifying selective opportunities in Asia ex-Japan foreign exchange tied to re-shoring.

Bridgewater (March 2026): Investors should hold “balanced exposures across competing blocs” rather than assuming US-centric diversification suffices.

Agility means the capacity to reposition as mercantilist policies shift. JPMorgan Asset Management’s 2026 Long-Term Capital Market Assumptions noted that trade fragmentation raises capex in North America and parts of Asia (positive for industrials) while pressuring margins for globally integrated supply-chain businesses, expecting “wider dispersion of equity valuations across regions and sectors.”

Vanguard advised investors in January 2025 to “stress-test exposures to concentrated supply-chain or sanction risks.”

Four questions an investor can ask of their current portfolio:

These are not stock tips. They are stress-test prompts for an environment where the rules of capital allocation are being rewritten by governments, not markets.

Investors wanting to translate the mercantilist framework into specific allocation changes will find our full explainer on regime-aware portfolio construction, which covers the structural challenges facing the traditional 60/40 model under tariff-driven sticky inflation, the case for real assets and alternatives, active currency hedging approaches, and country-level precision across Japan, India, China, and Southeast Asia rather than a single regional allocation.

Modern mercantilism is not a temporary political weather pattern. Its simultaneity across the US, EU, China, and India, and the depth of the policy commitments involved, confirm a structural regime shift. Zoltan Pozsar has described the destination as a “commodity-anchored, multipolar system” shaped by “state-driven mercantilism in commodities and technology.” Dani Rodrik’s “productivist paradigm” offers a complementary frame, emphasising domestic productive capacity and good jobs as the real objectives, complicating any simple “trade war” narrative.

Genuine uncertainty remains. The pace of further fragmentation, whether regional blocs will harden or partially re-integrate, and the degree to which AI mercantilism will bifurcate technology markets are open questions. As Bob Prince emphasised at the HSBC summit, both modern mercantilism and AI are structural forces, not cyclical ones, requiring a structural rather than tactical response.

Investors who update their mental models from “efficient global markets” to “competing mercantilist blocs generating asymmetric returns” will be better positioned to identify the winners and losers that this environment is continuously creating. The free-trade playbook served well for three decades. The world it described no longer exists.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding policy developments and market positioning are speculative and subject to change based on geopolitical developments and government actions.

Modern mercantilism is the pursuit of national advantage through targeted protectionism, state-directed credit, and discrimination against foreign firms in strategic sectors. Unlike classical mercantilism, which focused on accumulating gold and silver, modern mercantilism targets control over semiconductors, AI compute, and critical mineral supply chains.

Governments are deploying four main categories of tools: export controls and investment screening, industrial subsidies and local-content rules, tariffs and countervailing duties, and data and technology localisation mandates. Examples include the US CHIPS Act, EU countervailing duties on Chinese electric vehicles, and India's production-linked incentive schemes.

According to Brookings Institution analysis from May 2025, AI has become a central theatre for mercantilist competition, with policies risking fragmentation into regional AI blocs. This means AI sector returns will increasingly depend on which geopolitical bloc a company operates within, shifting analysis from product quality to jurisdictional positioning.

Emerging and Developing Asia is growing at 5.1%-5.3% annually versus 1.6%-1.9% for the euro area, with India, Vietnam, Malaysia, and Indonesia specifically identified by Amundi as beneficiaries of friend-shoring and supply-chain diversification away from China.

Investors should assess whether geographic exposure is diversified across competing mercantilist blocs, whether holdings depend on globally integrated supply chains vulnerable to export controls, and whether currency exposure extends beyond the US dollar and euro to reflect where incremental nominal growth is occurring.