Why a BoJ Rate Hike Hasn’t Stopped the Yen Carry Trade

2 hrs ago

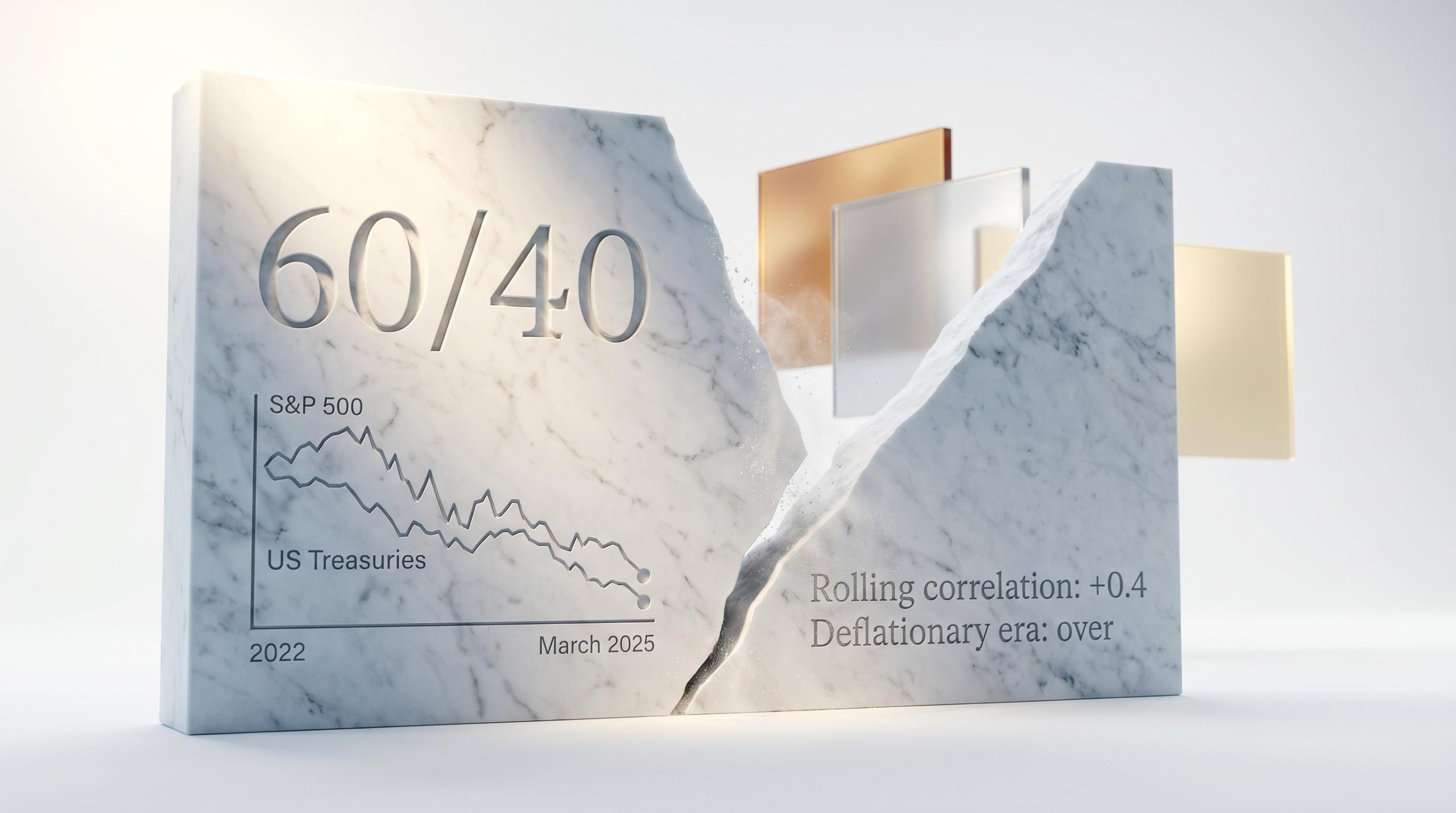

For decades, the assumption underpinning most balanced portfolios was straightforward: when equities fall, bonds rise. That negative correlation between stocks and bonds formed the bedrock of modern portfolio construction, and millions of investors built their retirement savings around it. Then 2022 arrived, and both asset classes declined together. The damage was supposed to be temporary. It was not. During a March 2025 US inflation surprise and yield spike, the S&P 500 and US Treasuries fell simultaneously once more, and rolling correlations turned positive again into early 2025. The hedge that defined a generation of portfolio theory had stopped working.

At the HSBC Global Investment Summit 2026 in Hong Kong, Bob Prince, Co-Chief Investment Officer of Bridgewater Associates (one of the world’s largest hedge funds), named the problem directly. Diversification, he argued, is necessary but no longer sufficient. The structural forces reshaping global markets, from modern mercantilism to AI-driven transformation, demand something more: portfolio agility.

This guide explains why static diversification is under strain, what portfolio agility means in practical terms, and provides a concrete framework any investor can apply to their holdings, regardless of portfolio size.

The logic of the traditional 60/40 portfolio rests on a single assumption: that government bonds provide ballast when equities decline. For roughly two decades, that assumption held. A deflationary global environment kept inflation subdued, central banks accommodative, and the stock-bond correlation reliably negative. Investors who held both asset classes could expect one to cushion the other during stress.

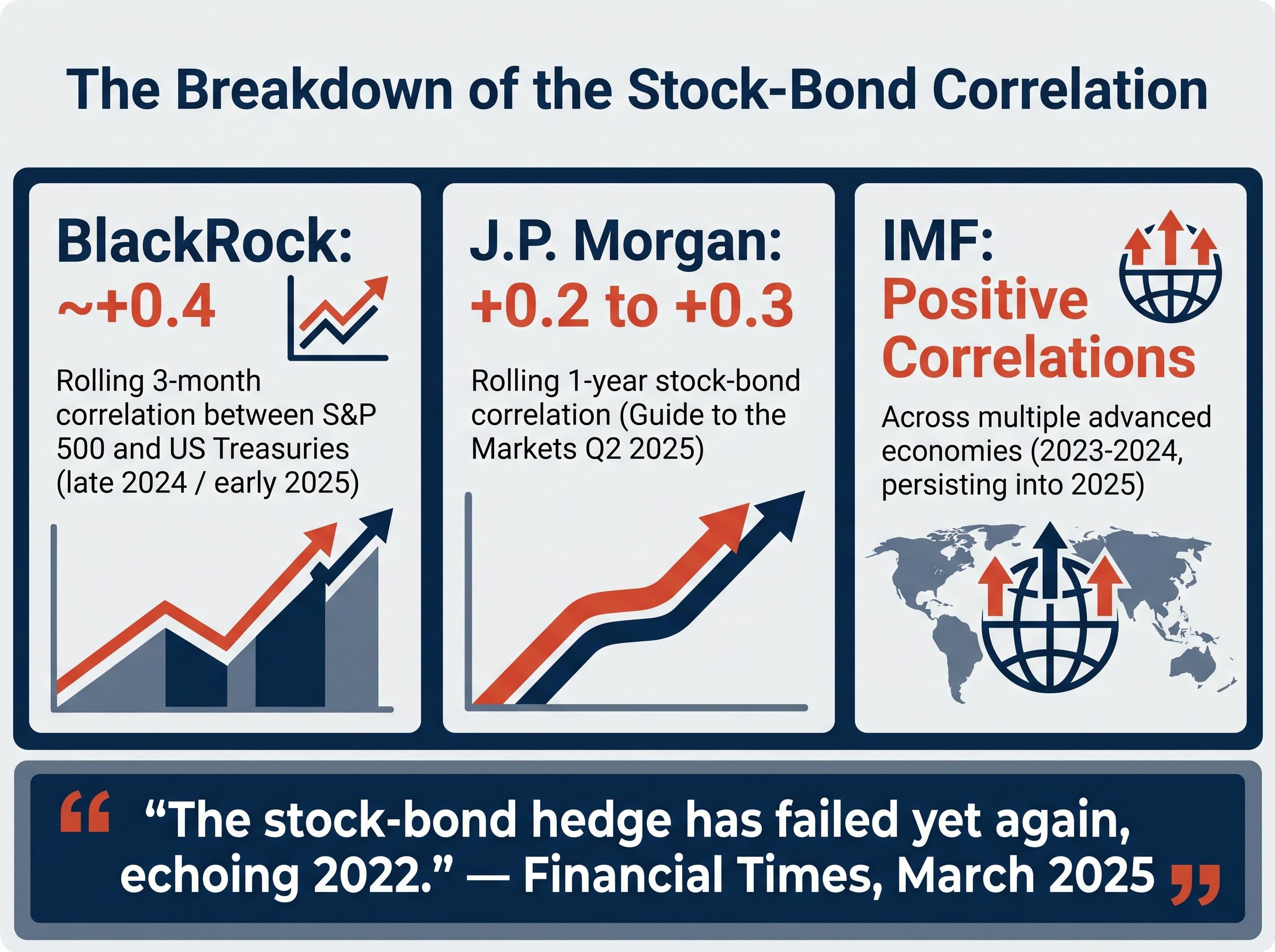

That cushion has developed holes. According to BlackRock, the rolling three-month correlation between the S&P 500 and US Treasuries rose to approximately +0.4 during late 2024 and early 2025 rate-repricing shocks, against a long-term negative baseline. J.P. Morgan’s Guide to the Markets for Q2 2025 showed the rolling one-year stock-bond correlation sitting in the +0.2 to +0.3 range in early 2025. The IMF’s World Economic Outlook in April 2025 documented positive equity-bond correlations across multiple advanced economies during 2023-2024 stress windows, with the pattern persisting intermittently into 2025.

The pattern of stocks and bonds falling simultaneously is not confined to 2022 or early 2025: on 15 May 2026, a coordinated selloff across US Treasuries, global equities, and commodities confirmed that inflation-driven correlation breakdowns are a recurring feature of the current regime rather than an episodic anomaly.

BlackRock’s analysis of post-60/40 allocation concludes that bond exposure has become a less reliable equity diversifier as correlations have turned more persistently positive, and that investors need a broader, more layered approach to ensure portfolio stability across different market regimes.

“The stock-bond hedge has failed yet again, echoing 2022.” — Financial Times, citing State Street data, March 2025

The correlation breakdown is not a one-off. Three structural forces are driving it:

If the hedge that “balanced” portfolios have relied on for decades is structurally impaired, the risk embedded in those portfolios is materially higher than the label suggests. Recognising this is the prerequisite for everything that follows.

Prince’s argument at the HSBC Global Investment Summit was not a tactical trade call. In dialogue with Ida Liu, CEO of HSBC Private Bank, he identified two concurrent structural forces reshaping global markets: modern mercantilism (the rise of industrial policy, tariffs, and strategic competition between nations) and AI-driven market transformation. Together, these forces are compressing the time between regime shifts and making static positioning increasingly costly.

Prince’s identification of mercantilism and AI as structural forces reshaping macro investing sits within a broader Bridgewater thesis: that tariff-driven sticky inflation, compressed policy space, and AI capital concentration are creating a new regime where passive allocation defaults consistently underperform active regime-aware construction.

The distinction Prince drew is worth pausing on. He was not arguing against diversification. He was arguing that diversification defined by asset-class labels alone, holding equities and bonds and assuming the job is done, is no longer adequate.

Bridgewater’s framing centres on what they call “diversification across environments,” meaning building portfolios that hold assets performing in growth environments, inflation environments, and risk-off environments, rather than simply holding a mix of equities and bonds.

Bridgewater’s reframe: Diversification across environments (inflation, growth, and policy regimes) rather than diversification across asset-class labels alone.

This is a meaningful conceptual upgrade. A portfolio holding global equities and government bonds may look diversified by label, but if both asset classes respond the same way to an inflation shock, the portfolio has only one bet on, not two. The shift is from asking “do I hold different asset types?” to asking “does my portfolio have coverage across different economic conditions?”

Ben Inker at GMO reinforced this view in March 2025, arguing that structural regime shifts make “long backward-looking correlations unreliable.” Bridgewater’s published research from April 2025 was equally direct, concluding that “the deflationary era is over” and that rising nominal and real yields have increased the probability that equities and bonds decline together when inflation fears re-emerge.

Prince is reframing the underlying architecture investors use to build portfolios. Grasping that distinction helps readers separate this structural argument from the noise of short-term market commentary.

Portfolio agility, at its simplest, is the capacity to adjust exposures in a disciplined, rules-based way as market conditions or economic regimes shift. It is not reactive trading. It is not checking a brokerage app every morning and rotating into whatever sector is up that week. Agility is a structured process, closer to a fire drill than a fire.

The concept operates on a spectrum. At one end sits a portfolio that never changes, the “set and forget” allocation reviewed once a decade. At the other sits an institutional trading desk making intraday adjustments. Most individual investors sit, or should sit, somewhere in the middle.

Four levels of agility exist, in ascending order of complexity:

The institutional world is already moving. A State Street Global Advisors survey from 2025 found that over 60% of institutions plan to increase dynamic asset allocation over the next three years, and nearly half have already shortened their risk-review cycle from quarterly to monthly since 2020. According to BlackRock’s 2025 Global Family Office Report, family offices have increased alternatives to an average 51% of portfolios, with over 70% using tactical tilts or opportunistic capital deployment.

Retail investors are shifting too. Morningstar’s 2024-2025 fund flow data shows a significant move into short-term bond funds, multi-asset tactical allocation funds, and liquid alternatives. Charles Schwab’s 2025 ETF Investor Study found that a majority of self-directed investors now use sector or thematic ETFs for short-to-medium-term tactical views.

The following comparison illustrates what separates a static approach from an adaptive one:

| Dimension | Static portfolio | Adaptive portfolio |

|---|---|---|

| Rebalancing frequency | Annual or ad hoc | Quarterly, or triggered by drift threshold |

| Allocation flexibility | Fixed target weights | Range bands (e.g., equities 50-70%) |

| Instrument range | Core index funds and bonds | Core funds plus sector, factor, and regional ETFs |

| Typical review trigger | Calendar date | Allocation drift, regime change signal, or valuation shift |

Agility is not the exclusive domain of hedge funds. The tools are increasingly available to any investor willing to define a process and follow it.

Prince’s specific mention of Asia at the summit was not incidental. The region provides perhaps the clearest illustration of why agility, and specifically selectivity, matters in practice.

A static “emerging markets” allocation treats Asia as a single trade. The reality is sharply different. China is decelerating. India and several ASEAN economies are accelerating on the back of supply-chain diversification, manufacturing capex cycles, and demographic tailwinds. North Asia, particularly South Korea and Taiwan, occupies a distinct position driven by semiconductor and AI hardware demand.

Semiconductor and AI hardware demand has become the defining capital flow theme of 2026, with the SOXX ETF posting a 40.4% gain in April 2026 alone, a concentration of returns so extreme that it forces investors to decide not just whether to hold North Asia tech but how much of a single-cycle bet they are willing to make.

The IMF emphasised at its Spring Meetings in 2026 that “Asia will continue to account for the majority of global growth in the medium term,” with India and ASEAN outpacing China.

Goldman Sachs reported in October 2025 that multinationals are increasing capital expenditure in India and ASEAN as part of supply-chain resilience strategies, driving multi-year investment cycles in industrial parks, logistics, and power infrastructure. HSBC Global Research’s March 2025 analysis highlighted India, Vietnam, Indonesia, and Taiwan/South Korea as specific beneficiaries of friend-shoring and semiconductor supply-chain repositioning. BlackRock noted in June 2025 that local currency Asian bonds offer diversification benefits and higher yields, though foreign exchange risk management remains a requirement.

| Sub-region | Structural driver | Opportunity type | Primary risk |

|---|---|---|---|

| India / ASEAN manufacturing | China+1 supply-chain diversification, demographic growth | Industrial capex, consumer demand, infrastructure | Regulatory fragmentation, execution risk on reforms |

| North Asia tech (Korea, Taiwan) | AI hardware cycle, semiconductor foundry demand | Technology equities, hardware supply-chain exposure | Geopolitical tension, concentration in a few firms |

| Broad China | Domestic consumption, policy stimulus | Selective sector exposure (consumer, green energy) | Slower structural growth, property sector overhang |

The move from “allocate to emerging markets” to “allocate selectively to India’s consumer economy, ASEAN manufacturing, or North Asia semiconductors” is itself an act of portfolio agility. Investors who treat Asia as a monolith leave both risk management and return potential on the table.

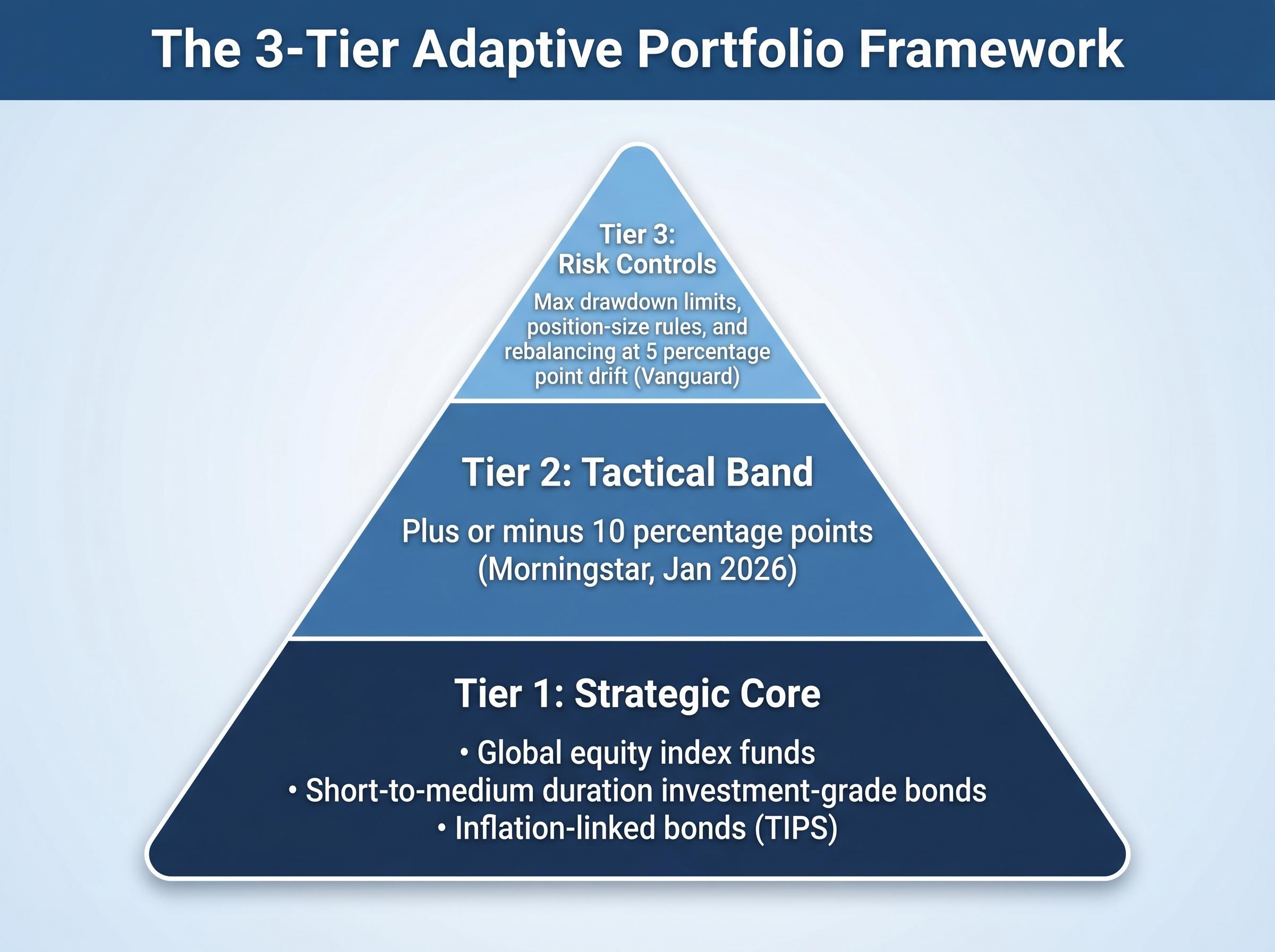

The institutional language of agility translates into a straightforward tiered framework that individual investors can apply immediately. Research from Morningstar, Vanguard, and BlackRock converges on the same core architecture, differing in labels but agreeing in structure.

The framework operates across three tiers, each building on the last:

BlackRock iShares’ three-bucket framework from March 2026 offers a complementary lens: a safety and liquidity bucket (cash, short-duration bonds), a growth bucket (global equities with regional and sector diversity), and a diversifier bucket (inflation-linked bonds, commodities, and select alternatives).

ETFs have become the primary instrument for tactical tilts. Sector ETFs, regional ETFs (India-focused or ASEAN-focused), and factor ETFs (value, quality) allow investors to adjust exposures without selling core positions. Automatic rebalancing platforms and managed account structures provide mechanical agility for investors who prefer not to make active decisions.

A shared caution runs through the research. Fidelity’s April 2026 guidance warns against over-trading, recommending semi-annual check-ins and small incremental tilts rather than large market calls. The goal is measured, rules-based adjustment, not responsiveness to every headline.

The concept of pre-committed rules is worth emphasising. Defining in advance the conditions that would trigger a rebalancing move (a 5-percentage-point drift from target, a material change in inflation regime, a valuation threshold being breached) turns agility from an abstract idea into a repeatable process. The decision is made in advance; only the execution happens in real time.

Investors wanting to put the drift-threshold and tax-efficiency considerations into practice will find our comprehensive walkthrough of portfolio rebalancing mechanics covers the specific execution steps for super, SMSF, and taxable account structures, including how to sequence trimming decisions and which alternative asset destinations are most appropriate for displaced equity capital in the current rate environment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Prince’s argument at the HSBC summit was not about the next quarter. It was about the next decade. Diversification remains necessary, but the correlation breakdown between equities and bonds is structural, not cyclical. The deflationary era that made the 60/40 portfolio reliable has ended, and the forces replacing it, de-globalisation, fiscal activism, and persistent inflation uncertainty, are not reversing soon.

Portfolio agility is the complementary capacity that fills the gap. It is not a hedge fund privilege. The tools, from sector ETFs to rules-based rebalancing platforms, are available to any investor willing to define a process and commit to it. Asia’s internal divergence provides a live illustration: the difference between a static emerging-markets allocation and a selective one, distinguishing India from ASEAN from North Asia, is itself agility in practice.

No framework eliminates uncertainty. The value of agility is not in predicting the next regime shift; it is in building a portfolio structure that can respond when the shift arrives, rather than one locked into assumptions formed in a different era.

Three questions serve as a starting point: does the strategic core cover multiple economic environments? Is there a pre-defined tactical band with rules for adjustment? Are risk controls explicit and written down? Investors who can answer yes to all three have already begun building the adaptive portfolio this environment demands.

Portfolio resilience is the ability of a portfolio to withstand losses across different economic regimes, including inflation shocks, growth slowdowns, and policy shifts. It matters now because the traditional stock-bond negative correlation that protected balanced portfolios for decades has broken down, meaning investors need broader diversification across economic environments rather than just asset-class labels.

The 60/40 portfolio relied on bonds rising when equities fell, but persistent inflation has caused both to decline simultaneously, with BlackRock data showing the rolling three-month stock-bond correlation rising to approximately +0.4 during 2024-2025 rate-repricing shocks. Structural forces including de-globalisation, fiscal activism, and the end of the deflationary era mean this correlation breakdown is unlikely to fully reverse.

Portfolio agility means having a structured, rules-based process to adjust exposures as market conditions change, rather than reacting to daily headlines. In practice it involves four levels: structured rebalancing on a schedule or drift threshold, allocation range bands (such as equities between 50% and 70%), tactical tilts via sector or regional ETFs, and the addition of alternatives like inflation-linked bonds or commodities.

Instead of treating Asia as a single emerging-markets allocation, agility-driven investors distinguish between India and ASEAN (benefiting from supply-chain diversification and demographic growth), North Asia tech in South Korea and Taiwan (driven by AI hardware and semiconductor demand), and China (offering selective consumer and green energy exposure with slower structural growth). This selectivity is itself an act of portfolio agility that improves both risk management and return potential.

The three-tier framework starts with a strategic core covering multiple economic environments through global equities, short-to-medium duration bonds, and inflation-linked bonds. Around that sits a tactical band allowing pre-defined adjustments of plus or minus 10 percentage points based on valuations or macro signals. The third tier is explicit risk controls, including maximum drawdown rules, position-size limits, and rules-based rebalancing triggered when allocations drift by more than 5 percentage points.