Electro Optic Systems (ASX: EOS) jumped more than 4% in Friday trade after acquisition target MARSS secured a €102 million (approximately A$165 million) counter-drone contract with an undisclosed Middle Eastern national defence force. The deal lifts the combined pro forma order backlog to approximately A$726 million once the acquisition completes, a figure large enough to reframe the near-term growth story for a company mid-way through a strategic pivot from hardware manufacturer to integrated counter-drone solutions provider.

The share price reaction landed on the same day EOS confirmed revised earnout terms on the MARSS acquisition, raising the ceiling from €100 million to €140 million. For Australian investors tracking EOS, the contract win, the revised deal economics, and the backlog arithmetic together form a single question: is the acquisition thesis playing out faster than the original structure anticipated, and what does that mean for risk?

MARSS Secures €102 Million Counter-Drone Deal, Driving EOS Share Price Higher

EOS shares climbed more than 4% on Friday 15 May 2026, according to TradingView market data, with the catalyst traced directly to MARSS’s counter-drone contract announcement.

Electro Optic Systems (ASX: EOS) jumped more than 4% in Friday trade following news that acquisition target MARSS secured a €102 million counter-drone contract in the Middle East, lifting the combined order backlog to roughly A$726 million once the deal completes.

The contract, valued at €102 million (approximately A$165 million), was struck with a national defence force of an undisclosed Middle Eastern country. Its scope covers expansion of MARSS installations to provide nationwide drone detection and neutralisation capability, a scale that signals multi-site deployment rather than a pilot programme.

Because the MARSS acquisition has not yet completed and MARSS remains a legally separate entity, the contract was reported via market commentary platforms rather than through a formal EOS ASX announcement. The distinction matters: EOS is not yet the contracting party, but the market is already pricing MARSS’s commercial momentum into EOS’s equity.

The ASX continuous disclosure obligations under Listing Rules 3.1, 3.1A, and 3.1B define when information is considered market sensitive and must be released immediately, which explains why the MARSS contract appeared via market commentary platforms rather than a formal EOS announcement while the acquisition remains legally incomplete.

When big ASX news breaks, our subscribers know first

What the deal does to EOS’s order book, and why the A$726 million figure matters

The A$726 million combined backlog is built from three components, and the arithmetic is worth walking through.

| Entity | Component | Value (AUD approx.) | Notes |

|---|---|---|---|

| EOS standalone | Existing order book | A$509 million | Includes US$42M Slinger and US$3M US integration orders |

| MARSS (pre-contract) | Existing order book | A$217 million | Prior to €102M Middle East contract |

| MARSS | New Middle East contract | A$165 million | €102M; undisclosed national defence force |

| Combined pro forma | Total backlog | ~A$726 million | Indicative; contingent on acquisition completion |

The A$726 million figure is a market estimate based on company disclosures and MARSS contract wins. It is contingent on the acquisition completing and should be treated as indicative.

EOS has also flagged that MARSS holds several prospective contract opportunities each exceeding A$100 million in value. If even one or two of those convert, the combined backlog could expand further before the acquisition formally closes. For a company with EOS’s revenue base, the backlog-to-revenue ratio is now at a level that frames the scale of potential revenue conversion over the next two to three years.

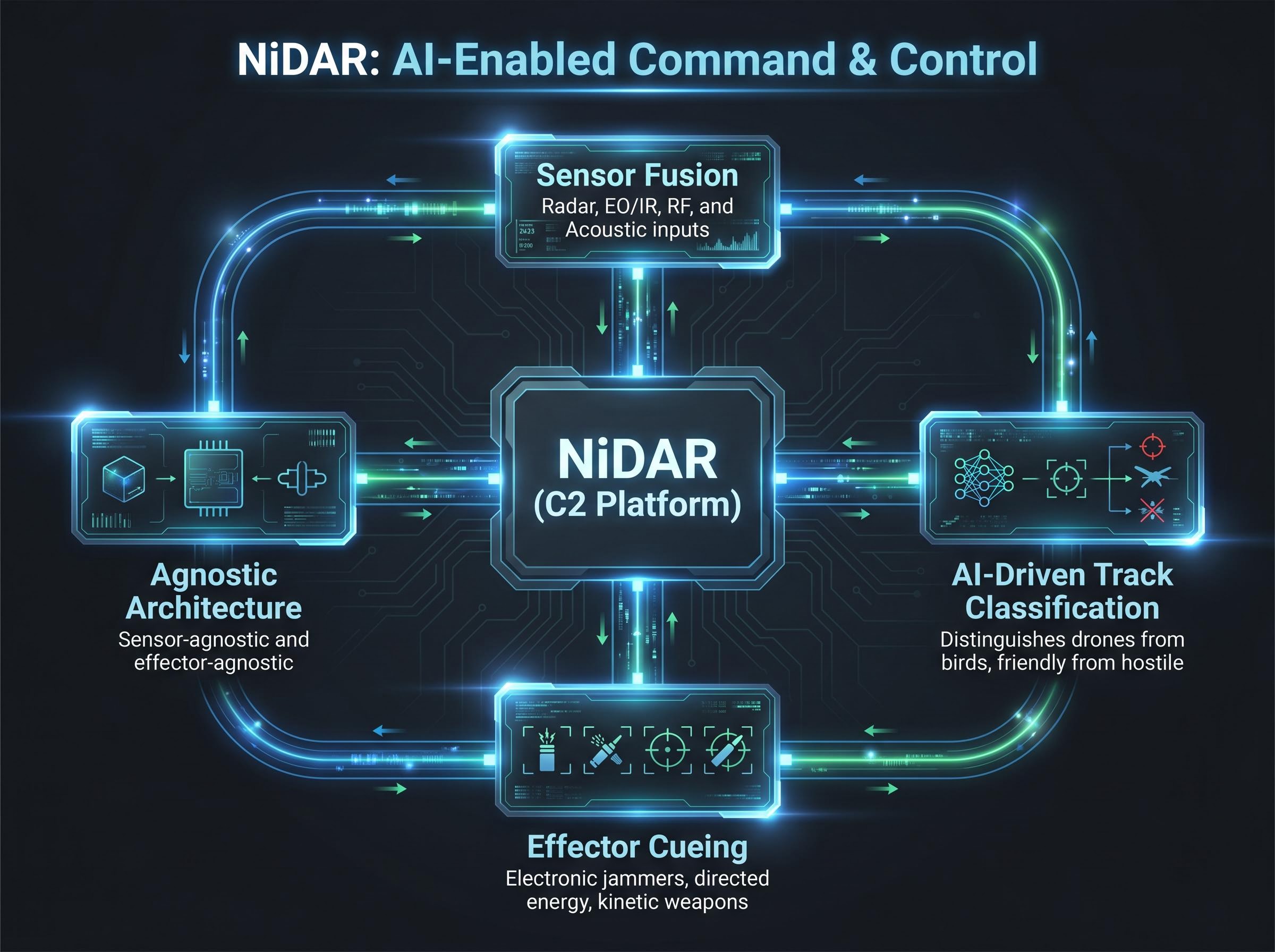

How NiDAR became a A$165 million proposition: what the system does and why Middle Eastern defence forces are buying it

NiDAR is MARSS’s AI-enabled command and control (C2) platform. In practical terms, it is the system that sits at the centre of a counter-drone deployment, pulling together data from multiple sensor types, deciding what is a threat, and telling the right weapon or jammer to respond. Its core capabilities include:

- Sensor fusion across radar, electro-optical/infrared (EO/IR), radio frequency (RF), and acoustic inputs

- AI-driven track classification, distinguishing drones from birds, friendly assets from hostile ones

- Effector cueing across electronic jammers, directed energy systems, or kinetic weapons

- Sensor-agnostic and effector-agnostic architecture, allowing integration with legacy equipment or third-party systems

NiDAR’s operational track record in the Middle East already includes protection of critical infrastructure, with multiple Shahed drone and missile attacks reported as having been neutralised. That track record is what converts a capability demonstration into a A$165 million contract.

The macro driver is straightforward. Lessons from Ukraine and the rapid proliferation of cheap commercial and military-grade drones have made integrated counter-unmanned aerial system (CUAS) procurement a non-discretionary priority across Gulf and broader Middle Eastern defence forces. Protection of oil and gas infrastructure, ports, and urban centres sits at the top of the spending queue. Major consultancies and defence think-tanks including Deloitte, Frost and Sullivan, and Janes forecast CUAS spending growing at mid-teens to above 20% CAGR through the late 2020s.

A €102 million contract with a national defence force is consistent with that urgency. It is not a trial; it is a nationwide deployment.

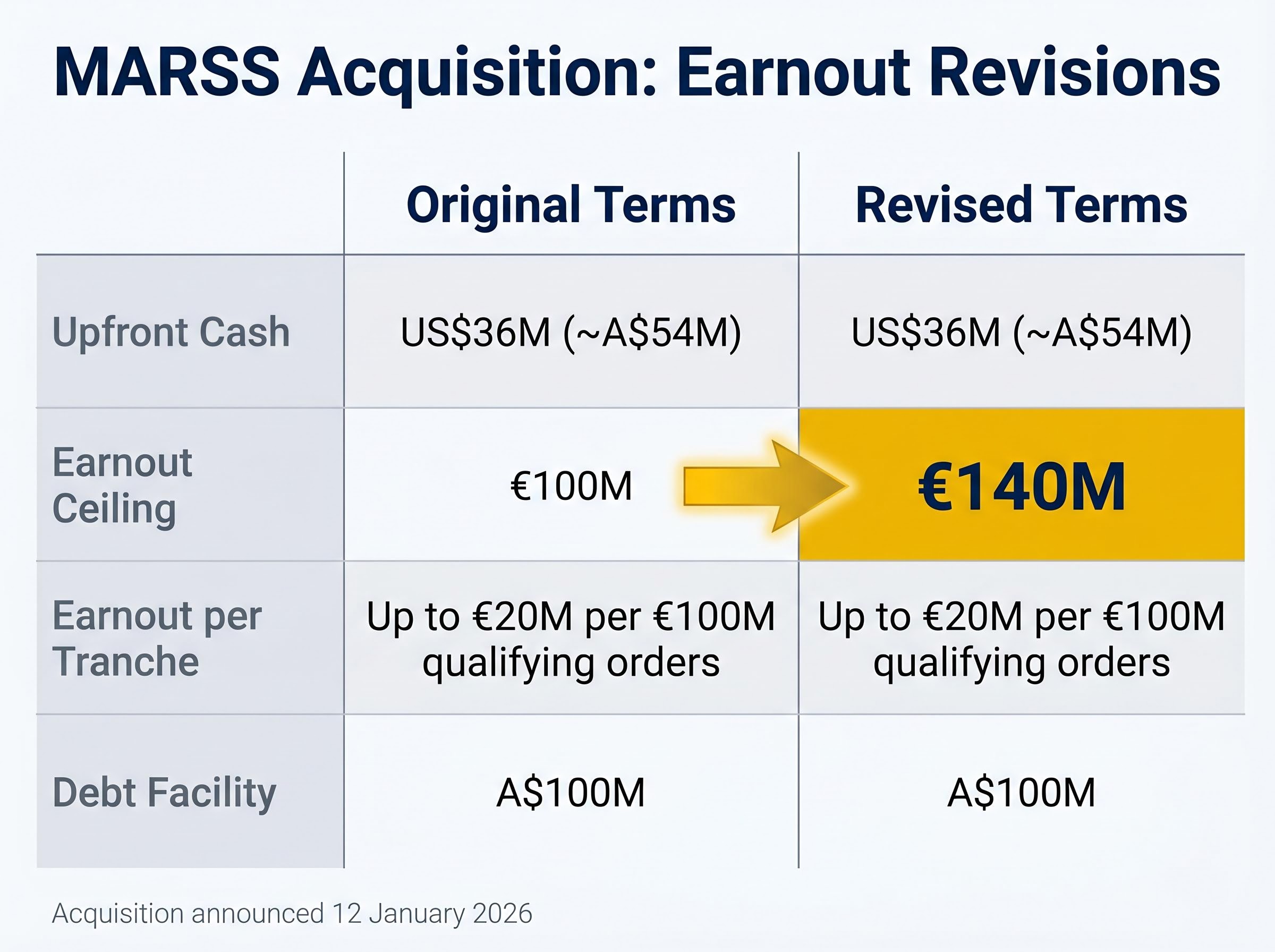

Key Changes to the MARSS Acquisition: Earnout Revisions Explained

EOS announced the MARSS acquisition on 12 January 2026. The original terms set an upfront cash consideration of US$36 million (approximately A$54 million), funded from EOS’s existing cash (approximately A$107 million as at 31 December 2025) and a A$100 million debt facility, of which A$70 million has been drawn down with A$50 million earmarked for the upfront payment.

The earnout structure pays MARSS up to €20 million for each €100 million (or part thereof) of qualifying new third-party orders, in a combination of cash (capped at €20 million per tranche) and EOS shares. The ceiling on total earnout obligations has been revised upward.

The A$100 million debt facility carries a 14.75% average interest rate and a covenant-free structure, terms that provide operational flexibility during the MARSS integration period but also represent a meaningful fixed-cost obligation at a time when the company is absorbing acquisition complexity across multiple jurisdictions.

| Item | Original terms | Revised terms | Notes |

|---|---|---|---|

| Upfront cash | US$36M (~A$54M) | Unchanged | Funded from cash and debt facility |

| Earnout ceiling | €100M | €140M | Revised late January 2026 |

| Earnout per tranche | Up to €20M per €100M of qualifying orders | Unchanged | Cash capped at €20M per tranche; balance in EOS shares |

| Debt facility | A$100M | Unchanged | A$70M drawn; A$50M earmarked for upfront payment |

EOS attributed the revised ceiling to growing customer enquiries and MARSS’s expanded market presence.

EOS has acknowledged there is no guarantee further contracts will be executed. The acquisition remains subject to customer, regulatory, and other approvals, with completion expected during 2026. The financial impact has been described as broadly neutral to earnings and operating cash flow in 2026.

The earnout revision is both a signal and a cost. It signals that MARSS’s pipeline is stronger than expected at the time of the original deal. It also means EOS’s total obligation could reach €140 million if MARSS continues winning at this pace, with a portion of that obligation settled in EOS shares, creating potential dilution for existing shareholders.

Growth trajectory and the risks EOS investors should keep in view

What the bulls are pointing to

The combination of backlog scale, product differentiation, and market tailwinds has drawn constructive commentary from both retail investors and sell-side platforms.

- A pro forma backlog of approximately A$726 million is now large relative to EOS’s current market capitalisation, supporting an order-book multiples argument

- NiDAR’s operational track record, including neutralisation of Shahed drone attacks, demonstrates commercial traction in competitive markets

- CUAS spending is growing at mid-teens to above 20% CAGR through the late 2020s, and government procurement in this category is increasingly treated as non-discretionary

- EOS plans to embed NiDAR directly into its remote weapon systems, creating mesh-networked CUAS nodes; this integration roadmap moves EOS from hardware supplier to integrated solutions provider

EOS’s own recent contract wins reinforce the momentum: a US$42 million Slinger order for a Middle Eastern customer and US$3 million in US integration orders, both with delivery expected during 2026.

EOS’s Middle East procurement pipeline extends well beyond the MARSS contract, with active discussions across Slinger RWS, APOLLO High-Energy Laser Weapons, and infrastructure protection products, alongside a separate conditional US$80 million Goldrone contract and early-stage UAE manufacturing discussions that could establish recurring production revenue streams.

Risks that remain on the table

TipRanks and Streetwise Reports both treat EOS as a higher-risk defence technology name, and the key debate among analysts has shifted from demand risk to execution and conversion risk.

- Earnout obligations capped at €140 million could become material if MARSS continues winning large contracts, creating a growing financial commitment alongside potential share dilution from earnout tranches

- The A$100 million debt facility adds balance-sheet leverage at a time when the company is also absorbing an acquisition across multiple jurisdictions

- Defence primes and technology players have historically struggled to convert large order books into profitable, on-time delivery; execution and integration risk across jurisdictions, cultures, and regulatory environments is real

- The gap between a A$726 million backlog and realised revenue remains wide until delivery milestones are met and margin performance is demonstrated

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

EOS’s counter-drone pivot: a long-term bet that is starting to show its shape

The A$165 million MARSS contract and the revised earnout terms confirm that EOS’s acquisition thesis is playing out faster than the original deal structure anticipated. The combined backlog sits at approximately A$726 million before the acquisition is even complete.

The key watch items remain unchanged: acquisition completion (subject to regulatory and customer approvals), the exact terms and covenants of the A$100 million debt facility, and whether MARSS’s pipeline converts into additional earnout-qualifying contracts that push toward the €140 million ceiling.

2026 is the integration and delivery year. The strategic and financial payoff for investors, if it arrives, is framed as a 2027-and-beyond story, as integrated NiDAR-plus-EOS systems begin to be fielded and backlog starts converting into recognised revenue and margin. Until then, the thesis is compelling on paper. The execution is what will determine whether it holds.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—