Why the Record-Low Consumer Sentiment Reading May Not Mean Recession

33 mins ago

Gaming is the world’s largest entertainment sector by audience. More than 3 billion players worldwide generate a market approaching $192 billion in 2025, according to Newzoo estimates. Yet when Australian investors scan their thematic ETF options, gaming still sits awkwardly alongside sports betting and novelty screens, categorised as discretionary entertainment rather than a structural technology play. The VanEck Video Gaming and Esports ETF (ASX: ESPO) exists to challenge that categorisation, offering ASX-listed exposure to the companies building recurring revenue models that look far more like software subscriptions than movie tickets. This analysis stress-tests the case for ESPO as a long-term holding, examining the structural revenue shifts that underpin the thesis, the specific risks that could derail it, and how ESPO compares against the alternatives available to Australian investors in May 2026.

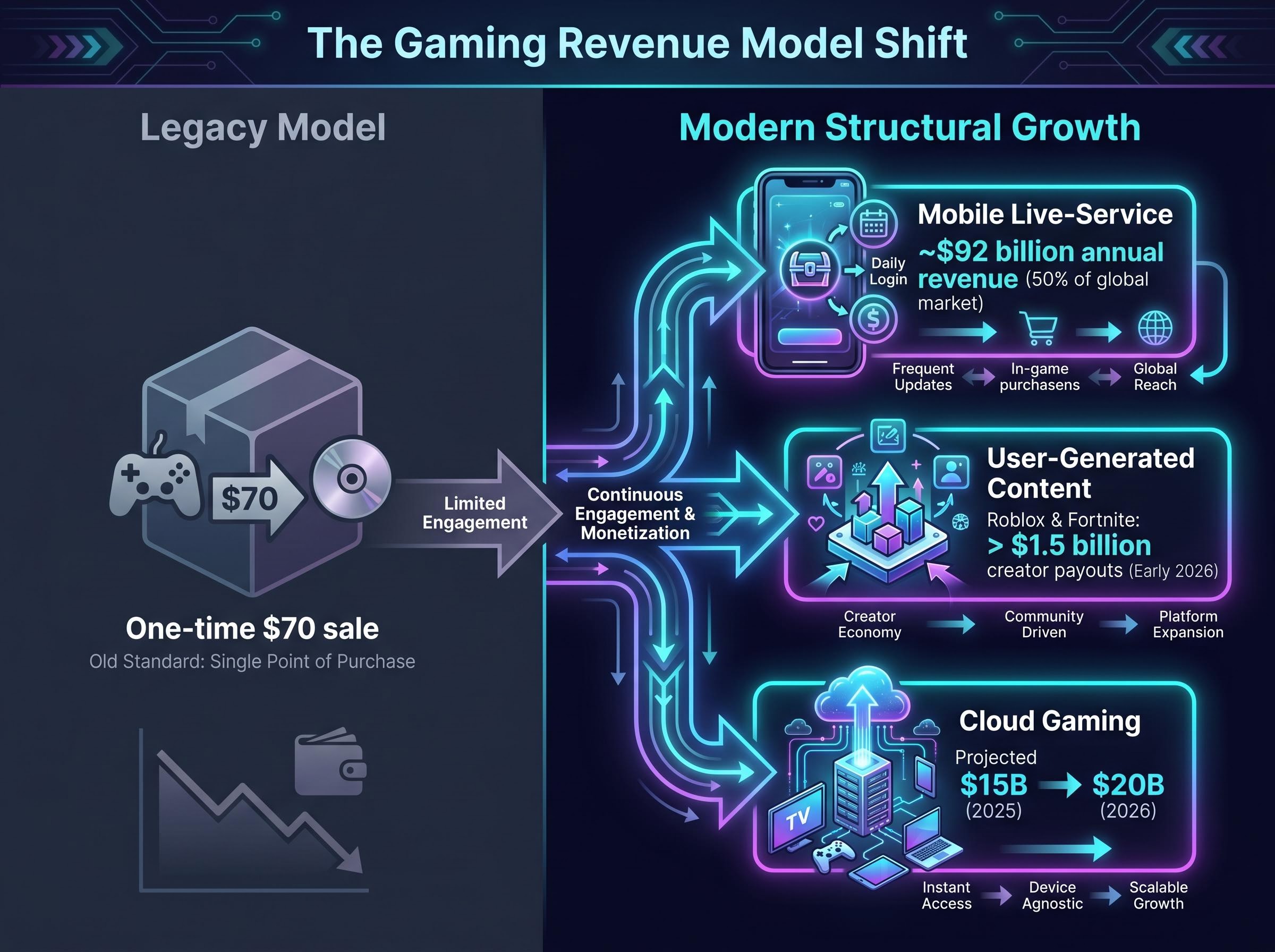

The bias is persistent: gaming looks like entertainment, so investors price it like entertainment. Cyclical, discretionary, dependent on hit-driven product launches. That framing made sense a decade ago. It no longer matches the revenue structure.

The shift underneath the sector has been a migration from one-off game purchases to recurring revenue streams. Three structural changes drive this:

This is not just a growth story. It changes the risk profile. A studio with 70% recurring revenue from live services and licensing is a fundamentally different investment proposition from one dependent on whether its next title ships on time.

A thematic ETF is only as strong as its holdings’ ability to execute on the theme. ESPO’s top three positions, Nintendo (approximately 12%), EA (approximately 10%), and Tencent (approximately 9%), each tell a different part of the structural revenue story.

| Company | Approx. Weight | Key Revenue Driver | One Risk to Watch |

|---|---|---|---|

| Nintendo | ~12% | Switch 2 pre-orders, IP licensing (Super Mario film sequel, cloud streaming partnerships) | Hardware cycle dependency; Switch 2 adoption pace |

| EA | ~10% | Live-service titles (EA Sports FC, Apex Legends); microtransactions up ~15% | Loot box regulatory probes in EU and U.S. |

| Tencent | ~9% | Honor of Kings, PUBG Mobile; cloud gaming infrastructure investment | U.S. investment scrutiny of Chinese tech |

Nintendo reported FY2025 revenue of ¥1.7 trillion and net profit of ¥420 billion, beating estimates on the strength of Switch 2 pre-orders and a Super Mario film sequel announced in Q1 2026. The IP licensing thesis is not theoretical here; it is generating revenue across film, merchandise, and cloud streaming partnerships.

EA posted Q4 FY2025 revenue of $7.6 billion, with microtransaction revenue up approximately 15% and AI development tools reportedly delivering an estimated 20% cost savings. The live-service model is producing durable, recurring income.

Tencent’s gaming segment grew +13% in Q1 2026, led by Honor of Kings and PUBG Mobile, following a year in which China’s game approvals increased approximately 40%. For investors who had written off Tencent under the regulatory overhang, the recovery has been material.

One honest complication: Take-Two Interactive’s GTA VI has been delayed to 2027. ESPO holds exposure to companies where live-service revenue is currently compensating for blockbuster delays, and that compensation has limits. Roblox offers a counterpoint, reporting Q1 2026 bookings up +28%, driven by UGC platform expansion.

At the surface level, the observation is straightforward: gaming now generates more revenue from ongoing engagement than from upfront sales. The mechanism underneath that observation is what matters for investors evaluating whether the shift is durable.

The percentage growth figures are striking. The base is not. Cloud gaming currently represents below 5% of total gaming market share. Latency constraints and broadband access limitations continue to cap near-term adoption, particularly in regions outside dense urban centres.

Tencent and other major ESPO holdings are investing heavily in cloud gaming infrastructure, but this is more accurately framed as a 2027-2029 inflection story rather than a current earnings driver. Investors pricing ESPO on cloud gaming expectations alone would be premature. The broader gaming market is projected to grow at a 5-7% compound annual growth rate (CAGR) through the medium term, according to Newzoo, well below the double-digit rates of the prior decade. Setting expectations accurately matters.

Newzoo’s Global Games Market Report projects the global gaming market at approximately $188.8 billion in 2025, with platform-level breakdowns confirming mobile’s dominance and a 5-7% CAGR through the medium term, providing the quantitative baseline that underpins the structural growth thesis for ESPO’s holdings.

The investment profile, taken together, looks more like software than entertainment: recurring revenue, improving margins through AI cost reduction, and a long-duration infrastructure buildout. That comparison is what supports a patient holding thesis.

Tencent’s geopolitical exposure is the single most significant holding-level risk. China’s game approvals increased approximately 40% in 2025, and that improvement is real. What it does not resolve is the persistent U.S. investment scrutiny of Chinese technology companies, which creates a ceiling on valuation re-rating for Tencent regardless of operating performance. Approximately 25% of gaming executives cite geopolitical risk as a top concern, according to the American Gaming Association’s (AGA) Q1 2026 data. For a fund with Tencent at approximately 9% weighting, this is not a footnote.

Three risk categories warrant attention:

Concentration risk in thematic ETFs behaves differently from concentration risk in individual stock positions: a single holding’s decline is absorbed across the fund, but a sector-wide drawdown affects all holdings simultaneously, which is exactly the scenario ESPO investors faced during the 2022 gaming sector correction.

77% of developers surveyed at GDC expressed optimism about the gaming industry’s long-term trajectory. The risk profile is real, but the industry’s own practitioners are not pricing in a structural decline.

The distinction for ESPO investors: Tencent exposure and mobile monetisation scrutiny are thesis-level risks that could impair specific holdings’ earnings power. Hardware constraints and consumer spending softness are cyclical headwinds that a 5-10 year hold can absorb. Knowing which is which matters for position sizing.

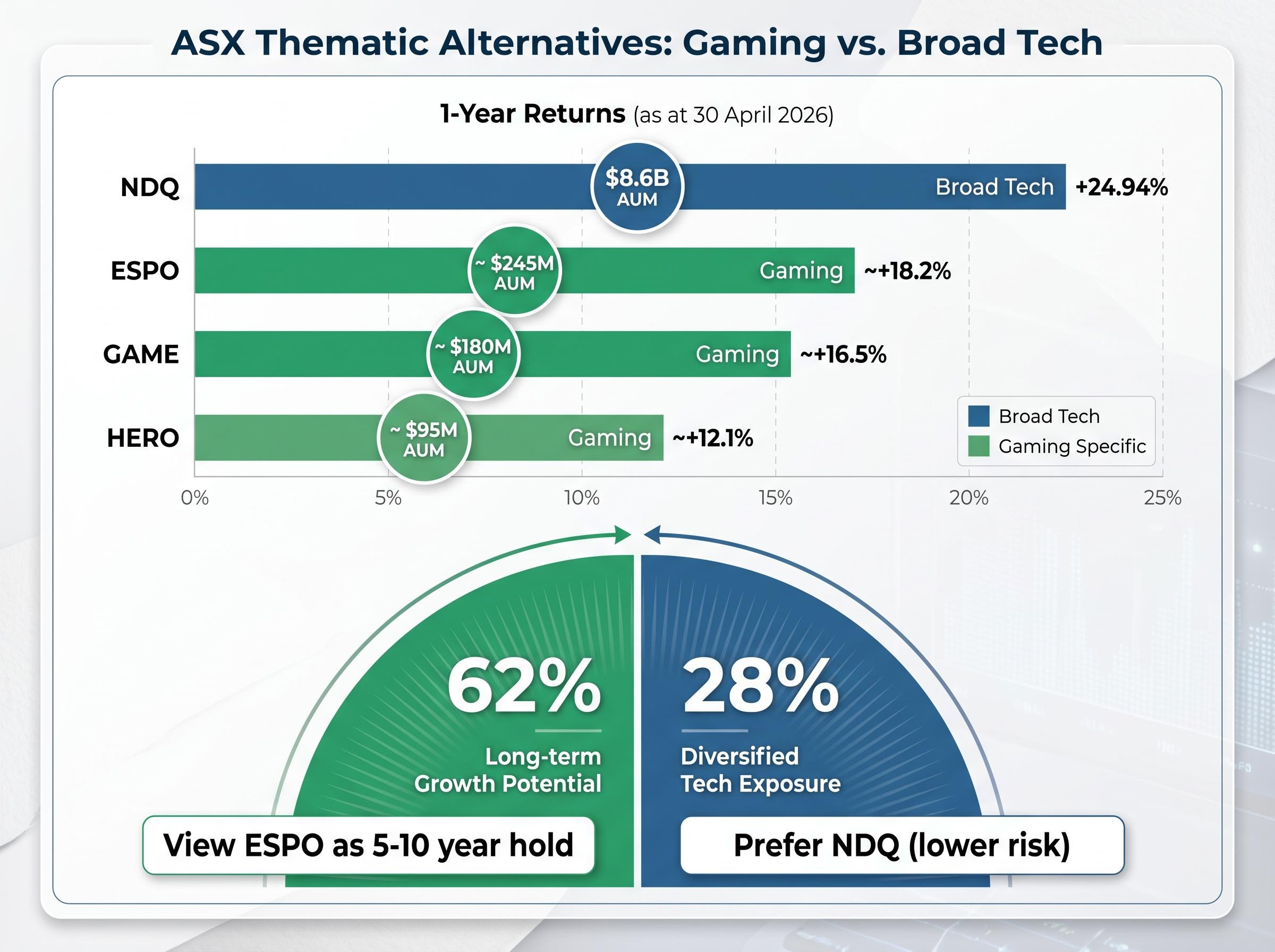

The ASX offers a small but distinct set of alternatives for investors seeking gaming or adjacent technology exposure. The comparison is not just about fees and returns; it is about what type of investor each product is built for.

| ETF | MER | Approx. AUM (AUD) | 1-Year Return | Best Suited For |

|---|---|---|---|---|

| ESPO | 0.55% | ~$245M* | ~+18.2%* | Diversified gaming exposure; Tencent/Nintendo access |

| GAME | 0.67% | ~$180M* | ~+16.5%* | Smaller-cap gaming bias; higher volatility tolerance |

| HERO | N/A | ~$95M* | ~+12.1%* | Esports-heavy allocation; niche conviction |

| NDQ | N/A | $8.6B | +24.94% | Broad tech exposure; lower risk, lower gaming specificity |

*ESPO, GAME, and HERO figures are directional estimates and could not be independently verified at time of writing. NDQ figures verified as at 30 April 2026.

BetaShares NDQ is the legitimate lower-risk alternative that many Australian retail investors are already choosing. Its 1-year return of +24.94% and AUM of $8.6 billion reflect both performance and trust. What NDQ offers is broad technology exposure, including indirect gaming exposure through holdings such as Microsoft and Apple. What it does not offer is concentrated exposure to the live-service and IP monetisation thesis.

The ESPO versus NDQ decision is a conviction question. NDQ is the default for investors who want technology exposure without a sector bet. ESPO is for investors who specifically believe gaming’s structural revenue shift is underpriced by the broader market and worth paying a specialist premium to access. Survey data (directional, sourced from retail investor forums) suggests approximately 62% of respondents view ESPO as a buy-and-hold vehicle for a 5-10 year thesis, while 28% prefer NDQ as the lower-risk path.

Investors exploring how ESPO’s returns compare across the broader ASX thematic ETF landscape will find our deep-dive into top-performing ASX ETFs in 2026, which profiles SEMI, ASIA, and EMXC alongside the concentration risks and volatility profiles that accompany each fund’s outsized year-to-date returns.

Three Australian tax considerations apply directly to ESPO and should be understood before purchasing:

From a portfolio construction standpoint, ESPO’s concentration in gaming means it should function as a satellite holding, typically 5-10% of a diversified portfolio, rather than a core position. Institutional flows favour ESPO specifically for its ASX-accessible exposure to Tencent and Nintendo, which are not easily obtained through domestic or broad-market ETFs.

The core-and-satellite framework, typically built around a broad index ETF foundation with targeted thematic allocations as satellites, is the portfolio construction context in which ESPO fits most naturally; a 5-10% satellite weighting to gaming sits alongside a larger NDQ or broad market core rather than competing with it.

One practical clarification: despite the gaming sector’s surface-level association with gambling, ESPO does not classify as a gambling product under Australian law. It is a thematic equity ETF.

Investors should consult the ESPO product disclosure statement (PDS) and a qualified tax adviser for guidance specific to their circumstances.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections referenced are subject to market conditions and various risk factors.

ESPO’s investment case rests on a genuine structural shift in gaming revenue models: live-service economics, AI-driven cost reduction, and IP monetisation across media verticals. This is not sector hype or post-pandemic momentum extrapolation. The holdings are executing on the thesis, and the post-2024 valuation reset has created a more attractive entry point for patient capital.

ESPO is not for every portfolio. It is a conviction play for investors who believe these revenue model shifts are durable, underappreciated by the broader market, and worth paying a 0.55% MER to access specifically rather than diluting the thesis through a broad technology allocation like NDQ. One final note of caution: data confidence gaps remain across ESPO’s reported AUM, specific holding earnings figures, and competitor ETF metrics. Investors should verify current metrics directly via VanEck Australia factsheets and the ESPO PDS before acting.

ESPO is an ASX-listed thematic ETF that provides diversified exposure to global gaming and esports companies, including top holdings such as Nintendo, EA, and Tencent, with a management expense ratio of 0.55%.

NDQ offers broad technology exposure with a 1-year return of approximately 24.94% and lower sector concentration, while ESPO targets the specific live-service and IP monetisation thesis within gaming, making it a conviction play rather than a general tech allocation.

The key risks include Tencent's exposure to U.S.-China geopolitical tensions, regulatory scrutiny of loot box and microtransaction mechanics in the EU and U.S., and cyclical headwinds such as hardware supply constraints and consumer spending softness.

ESPO units held longer than 12 months qualify for the 50% CGT discount, but distributions do not carry franking credits and U.S.-sourced income may attract 15-30% withholding tax, reducing the net yield for Australian investors.

ESPO is best suited as a satellite holding of around 5-10% of a diversified portfolio, sitting alongside a broader index ETF core such as NDQ rather than serving as a primary position.