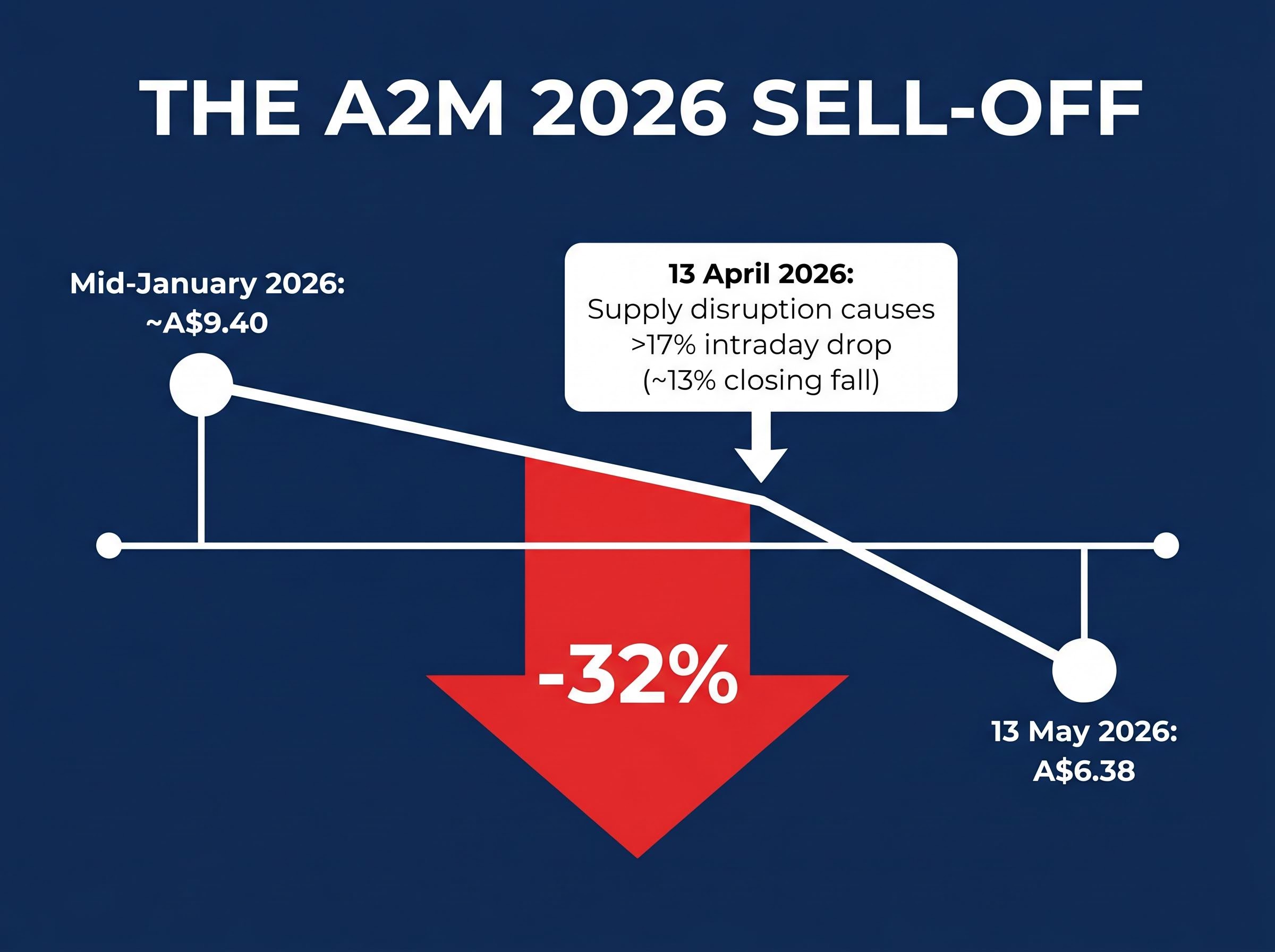

The a2 Milk Company has shed roughly 32% from its mid-January 2026 peak of approximately A$9.40, closing at A$6.38 on 13 May 2026. The slide accelerated in April when the company slashed its profit forecast following a supply chain disruption, triggering a single-day plunge exceeding 17% intraday. The sell-off has compressed the A2M share price to a price-to-sales ratio of roughly 2.99x, approximately 25% below the 10-year median, raising the question every ASX retail investor screening the stock is asking: is this a buying opportunity or a warning sign dressed up as a discount?

What follows unpacks the causes of the decline, what the valuation metrics do and do not reveal, and what the bull and bear cases look like when laid out honestly. The goal is not a verdict. It is a framework for forming one.

How A2M built its business (and why that matters when things go wrong)

The a2 Milk Company is not a manufacturer. It is a brand and intellectual property business, founded in New Zealand in 2000, that outsources production to a network of more than 25 certified dairy farm partners in Australia and to Synlait Milk in New Zealand for its infant formula range. Revenue depends on regulatory positioning and brand premium, not on physical processing assets.

The business model’s structural features are worth holding in mind before evaluating the sell-off:

- Brand-led: Revenue is earned on the A2-protein differentiation claim, not on commodity dairy processing margins

- Outsourced production: Manufacturing is contracted rather than owned, reducing capital intensity but creating supply chain concentration risk

- Regulatory-dependent distribution: Access to the China infant formula market requires ongoing compliance with formula registration and label approval regimes

In 2025, A2M sold its Mataura Valley Milk plant to Open Country Dairy, New Zealand’s second-largest dairy exporter. Chinese regulatory approval for the transaction was received in October 2025. The deal included a strategic manufacturing agreement for ongoing supply and, notably, a retained option for A2M to unwind the transaction within 12 months if Chinese label registration for new formulations is not obtained. That unwind clause is not boilerplate. It signals how tightly A2M’s forward revenue thesis is bound to regulatory outcomes in China.

The A2 protein claim and its eroding edge

The commercial appeal has always rested on the claim that A2-beta-casein protein is easier on digestion than conventional A1-dominant milk, a positioning that resonated strongly with parents seeking premium infant formula. For years, this differentiation commanded a premium multiple.

That edge is narrowing. Large domestic Chinese competitors, including Feihe, Yili, and Junlebao, are now launching their own A2-protein and digestive-health-focused products. A differentiation that once set A2M apart is becoming a category feature rather than a competitive moat.

When big ASX news breaks, our subscribers know first

The anatomy of a 32% drawdown in four months

The proximate trigger arrived on 13 April 2026. A2M disclosed temporary shortfalls in product supply linked to Middle East conflict disrupting its China supply chains and simultaneously cut its profit forecast. Shares fell approximately 13% on the day, with the intraday drop exceeding 17%.

The April announcement that sparked the sharpest single-day move included more than a supply disruption disclosure; the FY26 guidance downgrade cut EBITDA margin expectations from 15.5%-16.0% to 14.0%-14.5% and slashed cash conversion guidance from approximately 80% to 50%, as five converging supply constraints pushed revenue recognition into FY27.

The April shock was the detonator. The structural kindling had been accumulating for months.

A2M’s shares entered 2026 at a P/S ratio of approximately 5.22x, well above the five-year average of roughly 3.44x. The stock was priced for strong execution. When that execution failed to materialise, the re-rating was sharp and fast. Layered beneath the supply disruption sits a demographic reality that no amount of marketing can reverse.

China recorded 7.92 million births in 2025, a 17% decline from 2024 and the lowest figure since 1949. The infant formula market’s total addressable volume is structurally compressing.

| Cause | Date | Share price impact | Type |

|---|---|---|---|

| Elevated valuation unwind (P/S ~5.22x vs 3.44x avg) | January-April 2026 | Gradual compression from ~A$9.40 | Structural |

| Supply disruption and profit forecast cut | 13 April 2026 | ~13% single-day decline; >17% intraday | Event-driven |

| China demographic deterioration | Ongoing (2025 data) | Compressed forward growth expectations | Structural |

| Domestic competitive pressure (Feihe, Yili, Junlebao) | Ongoing | Eroded premium moat and pricing power | Structural |

Separating the event-driven shock from the structural de-rating is not an academic exercise. Investors who collapse these into a single cause risk treating a multi-layered impairment as a temporary dip.

What the valuation metrics actually say (and what they cannot tell you)

The current P/S of approximately 2.99x sits roughly 25% below the 10-year median of 3.98x. On a price-to-sales basis alone, the market has priced in meaningful bad news.

The trailing PE tells a different story. At approximately 28.3x, A2M is still priced for growth, not distress. If China revenue disappoints further in FY26, that multiple offers limited margin of safety.

| Metric | Current value | Historical reference |

|---|---|---|

| Price-to-sales (P/S) | ~2.99x | 10-year median ~3.98x; 5-year avg ~3.44x |

| Trailing PE | ~28.3x | Prices growth, not distress |

| Net cash position | ~NZ$896.88m | Substantial balance sheet buffer |

FY25 net profit after tax came in at approximately NZ$186m, up roughly 21% year-on-year. The business can still grow profitability. The question is whether it can do so at the rate the PE implies.

P/S analysis provides a useful first-pass signal, but it cannot substitute for discounted cash flow or more rigorous intrinsic value methods. Investors screening purely on P/S compression risk mistaking a statistically cheap reading for genuine undervaluation.

For retail investors, the honest framing requires holding both figures simultaneously. The P/S says the bad news may be priced in. The PE says the market still expects growth to deliver. Those two readings are in tension, and that tension is the stock’s defining feature at A$6.38.

The structural headwinds A2M cannot market its way out of

Three interlocking pressures sit beneath the April supply disruption, and each reinforces the others:

- Demographic decline: China’s 7.92 million births in 2025 represent a 17% drop from the prior year. Policy responses, including the three-child policy and subsidies, have produced no meaningful reversal. The total addressable market for infant formula is contracting in volume terms, with only partial offset from premiumisation.

- Domestic competitor strength: Feihe, Yili, and Junlebao have built stronger offline pharmacy and mother-and-baby store networks than imported brands. They deploy localised key opinion leader (KOL) marketing, loyalty programmes, and regulatory alignment advantages to take shelf space. Post-pandemic cross-border e-commerce (CBEC) volumes have normalised, requiring A2M to invest more in promotional activity simply to defend existing share.

- Regulatory binary risk: Chinese label registration is not a formality. It governs which specific products can be legally sold in China-label format, and its outcome creates binary strategic exposure for A2M.

The SAMR label registration outcome represents the single highest-stakes binary for the investment thesis; without confirmed registration for Mataura Valley Milk formulations, the forward earnings growth of approximately 33.5% implied by the current PE multiple becomes structurally unachievable regardless of underlying demand conditions.

The label registration risk and why it matters more than it sounds

The Mataura Valley Milk manufacturing agreement includes A2M’s option to unwind the transaction within 12 months if Chinese label registration for new formulations is not obtained. That clause exists because registration failure would remove a material portion of A2M’s forward China-label revenue capacity.

The China infant formula registration requirements administered by the National Medical Products Administration (NMPA) under SAMR govern which specific formulations can be legally sold in China-label format, with foreign manufacturers required to submit product documentation, factory audits, and formula composition filings before receiving market access approval.

Analysts broadly characterise A2M as a “quality but China-exposed” name. The framing is accurate, but the word “exposed” understates the degree. These are not cyclical headwinds that reverse when sentiment improves. Demographic decline and the rise of well-capitalised domestic competitors represent durable structural shifts that investors must explicitly accept as part of the A2M thesis.

The bull case: what a recovery would need to look like

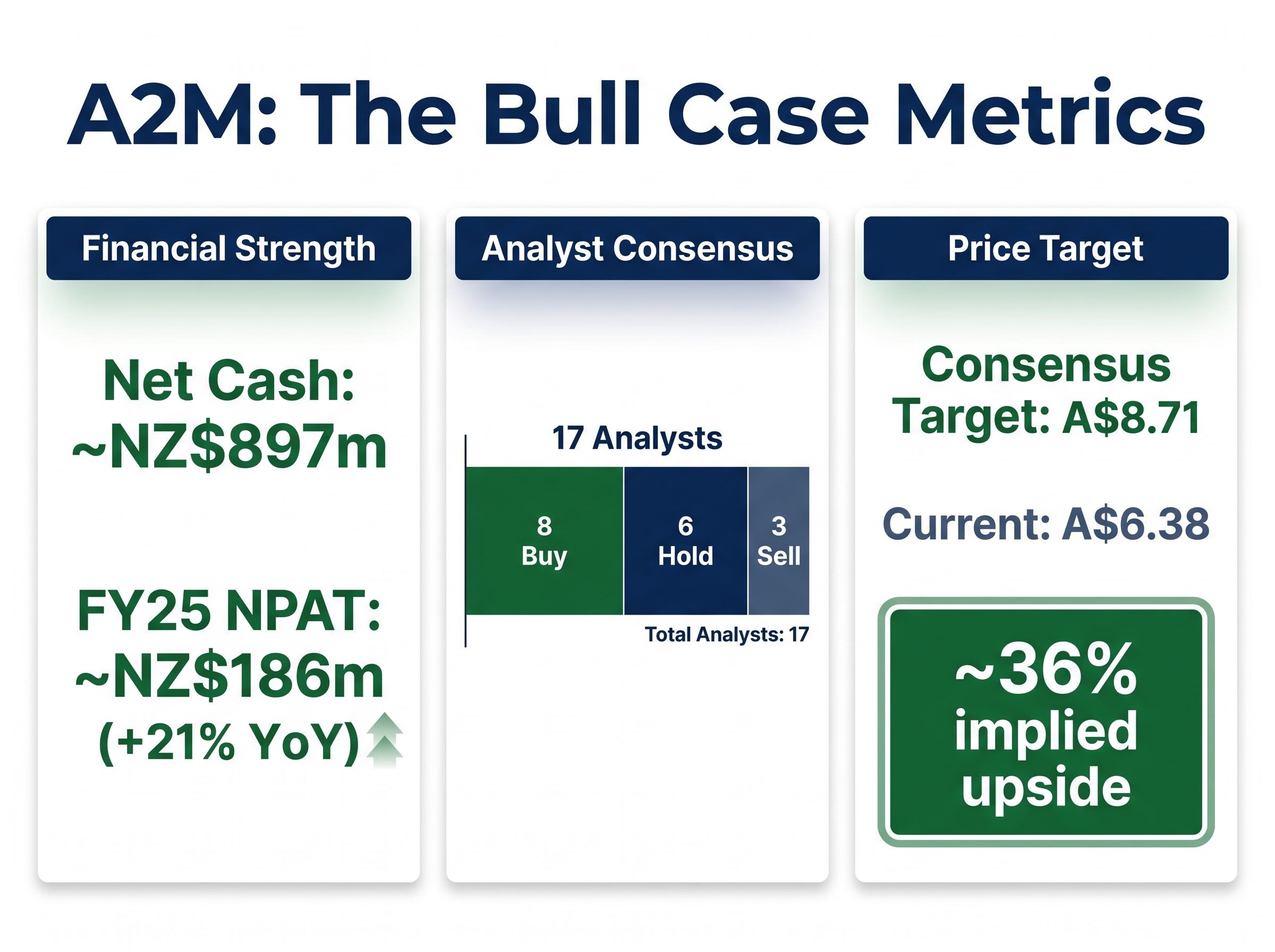

The balance sheet is the starting point, and it is a genuine differentiator. Approximately NZ$897m in net cash is not decorative. It funds marketing investment, product innovation, potential buybacks, and provides operational runway if conditions deteriorate further. Few ASX consumer staples names carry this kind of buffer.

For investors stress-testing the bull case, the free cash flow profile adds a material qualification to the profitability narrative; A2M’s gross margin of 45.8% and net cash balance sheet are genuine strengths, but negative free cash flow of NZ$120 million in FY25 signals that reported NPAT growth does not yet fully translate into distributable cash, limiting the practical capital return optionality that the cash pile appears to offer.

The analyst consensus offers a reference point. Across 17 covering analysts, the breakdown stands at 8 Buy, 6 Hold, and 3 Sell, with a consensus price target of A$8.71.

The average analyst price target of A$8.71 implies approximately 36% upside from the current A$6.38, though consensus targets reflect a range of assumptions about China execution that may or may not prove accurate.

Prior to the April supply disruption, A2M reported strong demand across all product categories and regions in Q3 FY26, supporting the view that the operational shock was event-driven rather than demand-driven. FY25 NPAT growth of approximately 21% year-on-year demonstrates the business can still expand profitability. The P/S sitting roughly 25% below its 10-year median provides valuation support if growth re-emerges.

For the bull thesis to materialise, three conditions would need to hold:

- Regulatory clearance: Chinese label registration confirmed for Mataura Valley Milk formulations, removing the binary overhang

- China execution: FY26 China revenue growth recovered to low-to-mid single digits or better

- Capital deployment: Balance sheet cash directed into buybacks, dividend initiation, or strategic acquisition, rather than simply accumulating

The bull case is not irrational. The question is whether it can survive the structural headwinds outlined above.

The next major ASX story will hit our subscribers first

Opportunity or value trap? What the evidence actually supports

A2M sits in genuinely contested territory. It is not cheap enough to be a deep value play; a PE of 28.3x still prices in meaningful growth. It is not structurally secure enough to be treated as a quality compounder without accepting material China execution risk. The five-year average dividend yield of approximately 0.28% confirms this is not an income stock; investors receive negligible return while waiting for thesis resolution.

Sector context reinforces the point. ASX Consumer Staples returned an average of -1.17% per year over the five years to May 2026, compared with the ASX 200’s 4.21%. Sector tailwinds will not rescue a weak thesis.

Three signals that would strengthen the bull case

Investors monitoring the stock should watch for:

- Chinese label registration confirmed for Mataura Valley Milk formulations (removes the binary regulatory overhang)

- FY26 China revenue growth recovered to low-to-mid single digits or better (validates demand resilience)

- A capital allocation announcement indicating buybacks, dividend initiation, or strategic acquisition (evidence the cash position is being deployed, not accumulated)

A2M rewards investors who are right about China, not investors who simply bought the dip. Position sizing relative to China risk tolerance is the more actionable frame than trying to identify the exact bottom.

A2M at A$6.38: a stock that demands intellectual honesty from investors

The P/S discount to the 10-year median is real and meaningful. The near-NZ$900m cash pile and FY25 profitability growth make this a viable quality-with-risk hold, not a terminal decline story. The PE of 28.3x means investors are still paying for future growth that depends heavily on China execution.

The honest framework is straightforward: understand your China exposure tolerance, monitor the three swing factors (label registration, China FY26 revenue trajectory, and cash deployment), and treat any position as higher-beta Consumer Staples rather than a defensive core holding. A2M at this price is a bet on China execution. The intellectual honesty lies in acknowledging that explicitly before sizing the position.

For readers wanting to understand how the macro backdrop shapes the risk environment for China-exposed ASX names, our full explainer on US-China trade negotiations examines how markets have priced in summit optimism across agricultural and energy purchase commitments that carry very different probability distributions than current equity valuations imply, with direct implications for consumer brands reliant on cross-border e-commerce volumes.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.