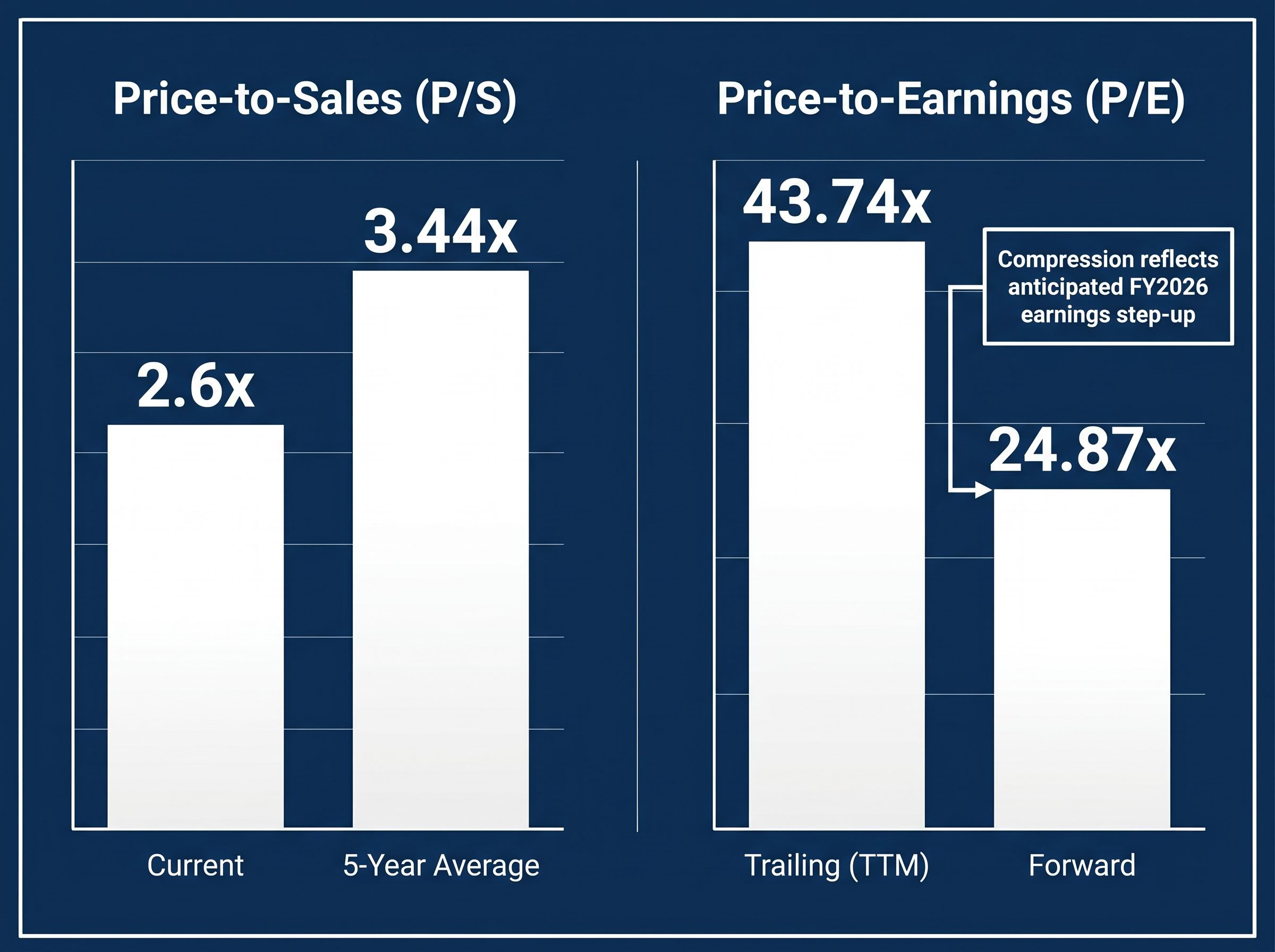

A2 Milk Company shares have shed 31% since the start of 2025, settling at A$6.33 as of 13 May 2026. The decline looks severe on a price chart. The valuation tells a more complicated story: the stock’s price-to-sales ratio of approximately 2.6x sits below its own five-year historical average of 3.44x, and the forward price-to-earnings multiple has compressed to 24.87x from a trailing 43.74x. For ASX investors watching the A2M share price, the question is not whether the stock has fallen. It is whether the price that remains still reflects the risks ahead, or whether the selloff has created an entry point that the business fundamentals can support. This analysis walks through the decline, the business model, the valuation arithmetic, the margin expansion thesis driving bullish forecasts, and the specific risks that could undermine it.

From A$9.97 to A$6.33: what triggered the selloff

The selloff did not arrive in a single session. It unfolded in stages:

- Start of 2025: A2M trading materially higher before the slide began

- March 2026: Share price reached a 52-week high of A$9.97

- May 2026: Shares at A$6.33, representing a 31% decline from the January 2025 starting point

- 52-week low: A$5.89, reached during the cycle’s trough

The FY2025 result itself, released on 18 August 2025, was strong. Revenue rose 13.8% year on year to NZ$1.90B, and net profit after tax climbed 21.1% to NZ$202.89M, materially beating prior consensus expectations. The numbers were not the problem. Management commentary was. Alongside the result, A2 Milk’s leadership flagged slowing category growth in China’s infant formula market, driven by persistently declining birth rates. That warning reframed the stock from a growth compounder to a share-gainer in a shrinking pool.

The April 2026 guidance cut was itself the product of five converging China supply chain disruptions, including Synlait manufacturing backlogs, enhanced cereulide testing requirements, elevated customs inspection rates, and freight capacity constraints tied to Middle East conflict, each compressing A2M’s ability to recognise revenue in FY2026 rather than shifting it into FY2027.

Performance gap: A2M’s one-year total return of -24.1% significantly underperforms both the AU Food sector (-4.6%) and the broader Australian market (+4.4%).

The March 2026 peak of A$9.97 now appears to have been the last gasp of post-result optimism. Market capitalisation has settled at A$4.61B, and investors are left to decide whether the pessimism is overdone or merely catching up with reality.

When big ASX news breaks, our subscribers know first

What A2 Milk actually sells, and why the business model matters for valuation

Investors evaluating A2M’s multiples need to understand why this company trades like a branded growth business rather than a commodity dairy producer. Three structural features explain the premium:

- A2 protein science: a differentiated product claim built on digestibility evidence

- Outsourced manufacturing model: capital-light operations historically reliant on third-party production

- Infant formula focus: a high-margin, high-growth category concentrated in China’s premium segments

The A2 protein story

Most conventional dairy products contain A1 beta-casein protein. A2 Milk, founded in New Zealand in 2000, sources milk exclusively from cows that produce the A2 beta-casein variant. Clinical studies suggest the A2 variant may be easier to digest for consumers who experience discomfort with standard dairy, though the science remains somewhat contested in academic circles. The competitive moat rests as much on brand trust and consumer loyalty as it does on the underlying research. Over 25 certified Australian dairy farms supply the milk, with Synlait Milk serving as the historical key manufacturing partner.

Why infant formula drives the valuation

Infant formula is the segment that commands the valuation premium investors pay for A2M. China’s premium and ultra-premium infant formula tiers, where A2 Milk concentrates its export strategy, carry structurally higher margins than liquid milk or adult nutrition. These premium tiers have also proven more resilient than the mainstream market even as aggregate Chinese birth rates decline. Without this infant formula exposure and the brand differentiation that supports premium pricing, the P/S and P/E multiples discussed below would be difficult to defend.

The valuation question: is 2.6x sales still a premium?

Valuation multiples mean little in isolation. The tension in A2M’s current pricing becomes visible only when each metric is set against its own historical reference point.

| Metric | Current | Historical Reference | Interpretation |

|---|---|---|---|

| P/S ratio | ~2.6x | Five-year average: ~3.44x | Below own history; complicates the “still overvalued” narrative |

| TTM P/E | 43.74x | Elevated for a slowing-category business | Reflects trailing earnings before margin expansion thesis delivers |

| Forward P/E | 24.87x | Near half of TTM P/E | Compression reflects anticipated FY2026 earnings step-up |

| 1-year total return | -24.1% | AU Food: -4.6%; Broader market: +4.4% | Significant underperformance across both benchmarks |

The P/S ratio of approximately 2.6x is calculated from A2M’s current market capitalisation of A$4.61B divided by trailing twelve-month revenue of A$1.77B in AUD. Some analyst sources cite a higher P/S figure (Rask, for instance, references 3.65x), which likely reflects a different measurement date or NZD-to-AUD conversion basis. The directional conclusion remains the same: on a revenue multiple basis, the stock is trading below its own five-year average.

The more revealing tension sits in the earnings multiples. A TTM P/E of 43.74x looks stretched for a company facing structural category headwinds. A forward P/E of 24.87x looks reasonable for a business expected to grow earnings by roughly 33.5% in FY2026. The gap between those two numbers is the margin expansion thesis, distilled into a single ratio. If the thesis delivers, the forward multiple justifies the current price. If it does not, the trailing multiple is the one that matters.

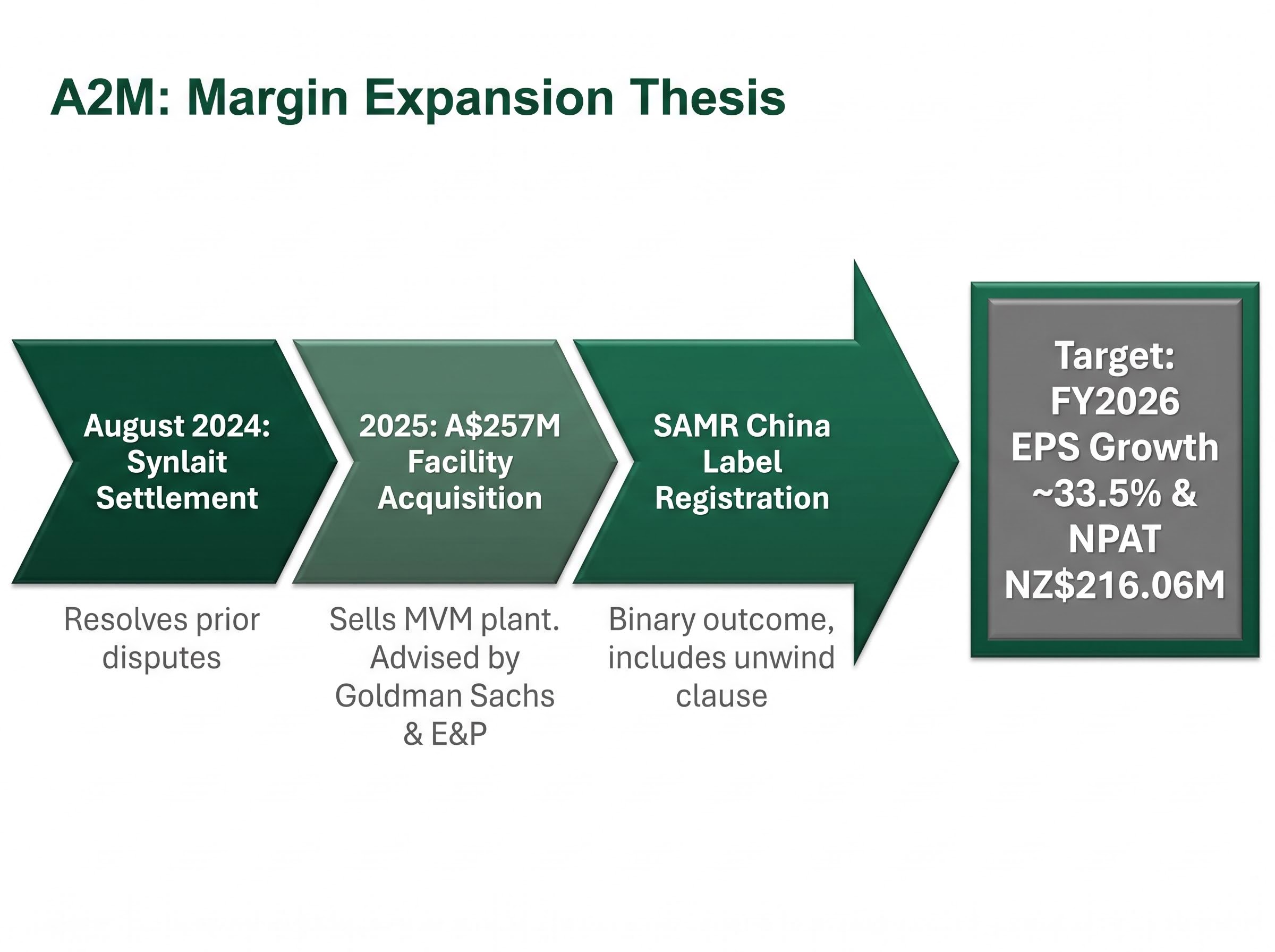

The margin expansion thesis: Synlait, the new facility, and the FY2026 earnings step-up

The bull case for A2M is not a list of positives. It is a cause-and-effect chain, and each link must hold for the earnings step-up to materialise.

- Synlait resolution reduces supply costs and uncertainty. In August 2024, A2M struck a settlement with Synlait Milk that resolved prior contractual disputes, according to reporting by the Australian Financial Review. The deal gave A2M greater control over its manufacturing base, removed a structural overhang that had weighed on the stock for years, and was reflected in a sharp share price re-rating at the time.

- New facility acquisition shifts A2M toward vertical integration. In 2025, A2M acquired a manufacturing facility for approximately A$257M, with Goldman Sachs and E&P advising. Simultaneously, the company sold its Mataura Valley Milk (MVM) plant to recycle capital from a non-core asset. The combined effect is a shift from brand-owner reliant on third-party production toward a model where A2M controls a high-quality, China-aligned facility for its most valuable product lines.

- China label registration unlocks premium volume through owned production. The facility’s strategic value is contingent on securing SAMR (State Administration for Market Regulation) approval for infant formula production. A2M structured the deal to include an unwind clause: it retains the right to reverse the acquisition if China label registration is not obtained, a structure that acknowledges the binary nature of the regulatory risk.

Synlait’s financial position adds a further layer of complexity to A2M’s supply chain thesis: Synlait completed a NZ$307 million North Island asset sale to Abbott in April 2026 and used NZ$200 million to halve its bank debt, but all remaining bank facilities mature on 30 June 2026 and a NZ$130 million shareholder loan falls due days later, meaning A2M’s key historical manufacturer is itself navigating a critical refinancing window.

FY2026 EPS growth forecast of approximately 33.5% is contingent on China label registration being secured for the new facility.

The FY2026 NPAT forecast of NZ$216.06M, according to Intelligent Investor estimates, implies earnings growth materially stronger than the FY2025 result, even if top-line revenue growth does not re-accelerate dramatically. Simply Wall St projects earnings growth of approximately 19.05% per year going forward, roughly double the historical five-year average of 9.7% per year. The company’s balance sheet, rated 6/6 by Simply Wall St’s health scoring system with low debt and total assets of approximately NZ$1.85B, provides the capacity to absorb near-term earnings volatility while the thesis plays out.

Three risks that could keep A2M a value trap

Premium valuations require premium execution. The following three risks are structural and specific, not vague macro concerns.

- China’s birth rate decline is secular, not cyclical. Management confirmed at the FY2025 result that the infant formula category is shrinking in aggregate. The birth rate trajectory is not reversing. A2M must perpetually win share in a declining pool to grow volume, a dynamic that places a permanent ceiling on category-driven upside and demands constant competitive gains simply to stand still.

- SAMR label registration introduces a binary outcome. If the new facility does not receive regulatory approval for China-label infant formula production, the margin expansion thesis is materially impaired. The forward earnings forecasts underpinning the 24.87x forward P/E would require reassessment. A2M’s decision to include an unwind clause in the acquisition deal acknowledges this risk explicitly, but the clause itself does not eliminate the strategic setback a negative outcome would represent.

The SAMR Order No. 80 registration requirements set out by China’s State Administration for Market Regulation cover the full technical review, recipe registration, and on-site inspection process that overseas dairy producers must satisfy before exporting infant formula to China, making regulatory approval a multi-step process with no guaranteed timeline.

- Intensifying competition compresses pricing power. Domestic Chinese brands, including Yili and Feihe, are gaining ground in the premium formula market. Multinationals continue to compete aggressively. Over time, this intensification compresses the pricing power that A2M relies on to justify higher retail prices in the premium and ultra-premium tiers. Brand trust and A2 protein differentiation remain advantages, but they are advantages under pressure.

A2M’s weekly price volatility of approximately 6.4% (versus 5.4% for the Food sector average) and its 52-week range of A$5.89 to A$9.97 illustrate the width of outcomes investors are already pricing. The stock is not trading as a panic liquidation; the market has partially digested these headwinds. The question is whether it has digested enough.

The next major ASX story will hit our subscribers first

A stock in transition: what a fair price requires A2M to deliver

The valuation picture, taken as a whole, is neither a clear bargain nor an obvious warning. A P/S of approximately 2.6x sits below the five-year average. A forward P/E of 24.87x is substantially lower than the trailing 43.74x. Simply Wall St models suggest A2M trades approximately 26-48% below estimated intrinsic value, and analyst consensus implies upside of approximately 35.6% from current levels. Every one of these signals, however, is contingent on execution.

A further legal overhang was removed in April 2026 when A2M reached a class action settlement of A$62 million, fully covered by insurance, with the proceedings originating from the company’s guidance disclosures during the FY21 period; the settlement was reached with no admission of liability and no impact on FY26 earnings, clearing one of the longer-running legal clouds from the investment case.

Three conditions must materialise for the current valuation to be justified:

- SAMR label registration secured for the new manufacturing facility

- Continued share gains in China’s premium and ultra-premium infant formula tiers, offsetting aggregate category decline

- Successful ramp-up of the new production facility to generate the margin uplift embedded in FY2026 forecasts

Simply Wall St models suggest A2M trades approximately 26-48% below estimated intrinsic value, though this range is model-dependent and should not be read as a price target.

The dividend yield of 3.29% (A$0.21 per share, ex-dividend 19 March 2026) provides a modest income component that reduces the holding cost while investors wait for the thesis to play out. It is not, for a growth-oriented stock, a primary investment rationale.

Investors who can articulate what A2M needs to deliver, and who hold a view on the likelihood of each condition being met, are in a materially stronger position than those reacting to the price chart alone.

A2M’s next chapter depends on one regulatory outcome

The selloff has brought A2M’s valuation multiples closer to, and in some measures below, historical averages. The forward earnings case that makes those multiples defensible rests on China label registration and facility ramp-up, both of which remain unresolved as of May 2026.

What distinguishes this situation from a distressed investment is the balance sheet. A2M carries low debt, holds approximately NZ$1.85B in total assets, and scores 6/6 on Simply Wall St’s financial health metric. The company is not in financial jeopardy regardless of the China outcome.

The next material catalyst is the SAMR label registration decision. Investors considering a position, or an addition to an existing one, may benefit from defining in advance what action they would take depending on the outcome. A2M is a monitored thesis, not a concluded one.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including earnings forecasts and analyst estimates referenced in this article, are subject to change based on market developments and company performance.