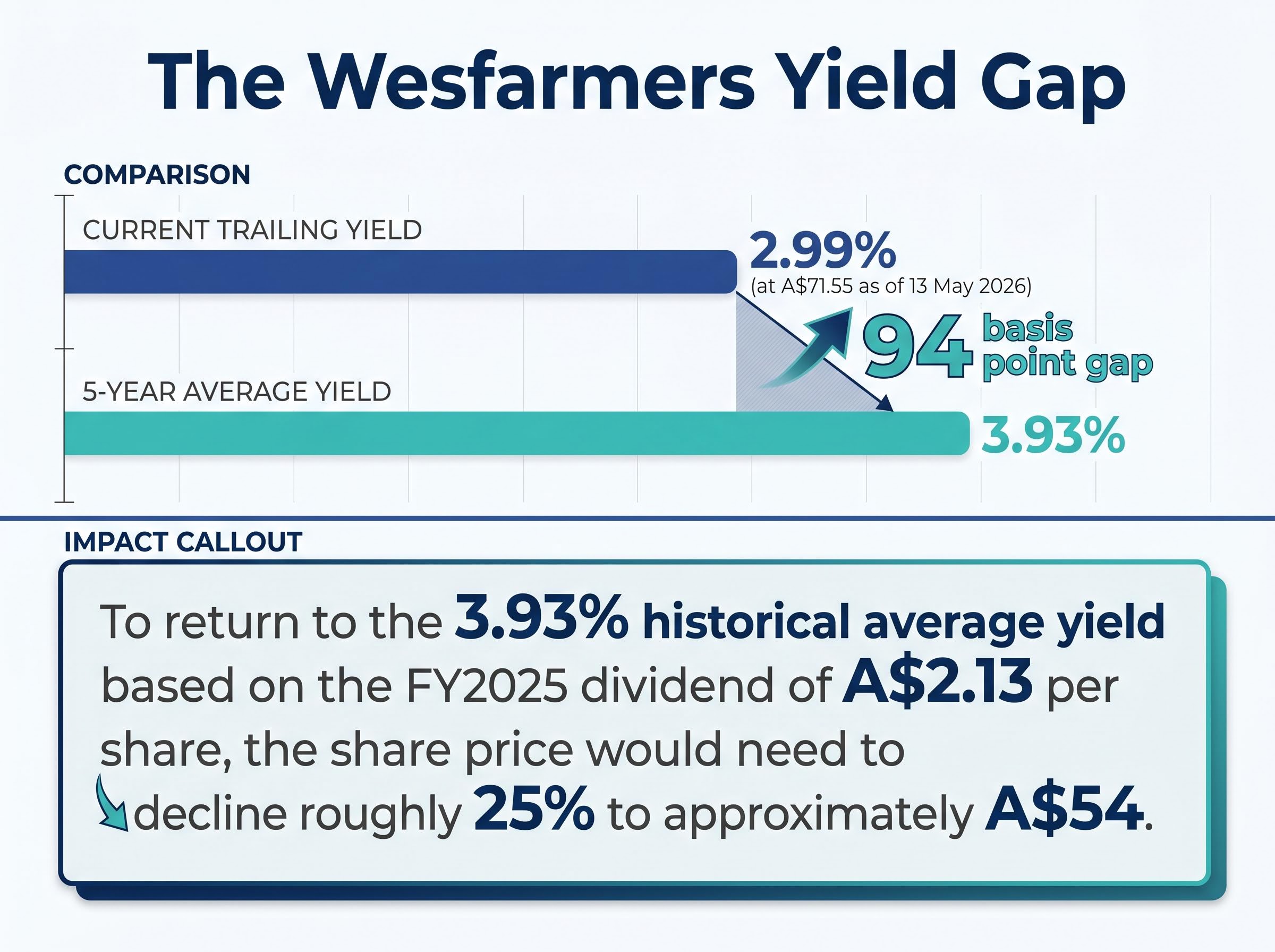

Wesfarmers shares closed at A$71.55 on 13 May 2026, sitting less than 1% above their 52-week low of A$70.87. For many investors, proximity to a multi-year floor signals opportunity. Yet the stock’s trailing dividend yield of 2.99% remains 94 basis points below its five-year average of 3.93%, a gap that dividend yield theory interprets not as cheapness but as a persistent valuation premium. That tension, between a share price near its recent low and a yield that says the stock is historically expensive relative to income, sits at the centre of the valuation question for income-focused investors. What follows is a yield-based analysis of Wesfarmers (ASX: WES), an examination of the business fundamentals behind the premium, and a framework for assessing both the bull and cautionary cases at current levels.

What the dividend yield gap reveals about WES valuation right now

The logic is counterintuitive but straightforward. When a stock’s trailing dividend yield is below its historical average, the share price has outrun income growth. The stock is expensive relative to its own dividend history, not cheap.

Wesfarmers paid approximately A$2.13 per share in fully franked dividends across FY2025. At the current price of A$71.55, that produces a trailing yield of 2.99%. The five-year average yield is 3.93%.

The yield gap: 2.99% current versus 3.93% five-year average. For the trailing yield to return to its historical average on the same dividend, the share price would need to fall to approximately A$54, a decline of roughly 25% from current levels.

That calculation does not predict a share price decline. It illustrates the degree of valuation premium embedded in the current price relative to income history. Proximity to the 52-week low is a relative measure within the past 12 months only; it says nothing about where the stock sits against its longer-term yield profile.

| Metric | Current | Five-Year Average | Implication |

|---|---|---|---|

| Trailing Dividend Yield | 2.99% | 3.93% | Share price elevated relative to income history |

| Full-Year DPS (FY2025) | A$2.13 | Progressive growth track record | Dividend growth has not kept pace with share price re-rating |

| Distance to 52-Week Low | 0.96% | N/A | Near-term floor, not a long-term valuation signal |

A stock can simultaneously trade near its 52-week low and carry a premium on yield terms. Both are true for Wesfarmers in mid-May 2026.

When big ASX news breaks, our subscribers know first

Wesfarmers in plain terms: a conglomerate built on acquiring, compounding, and moving on

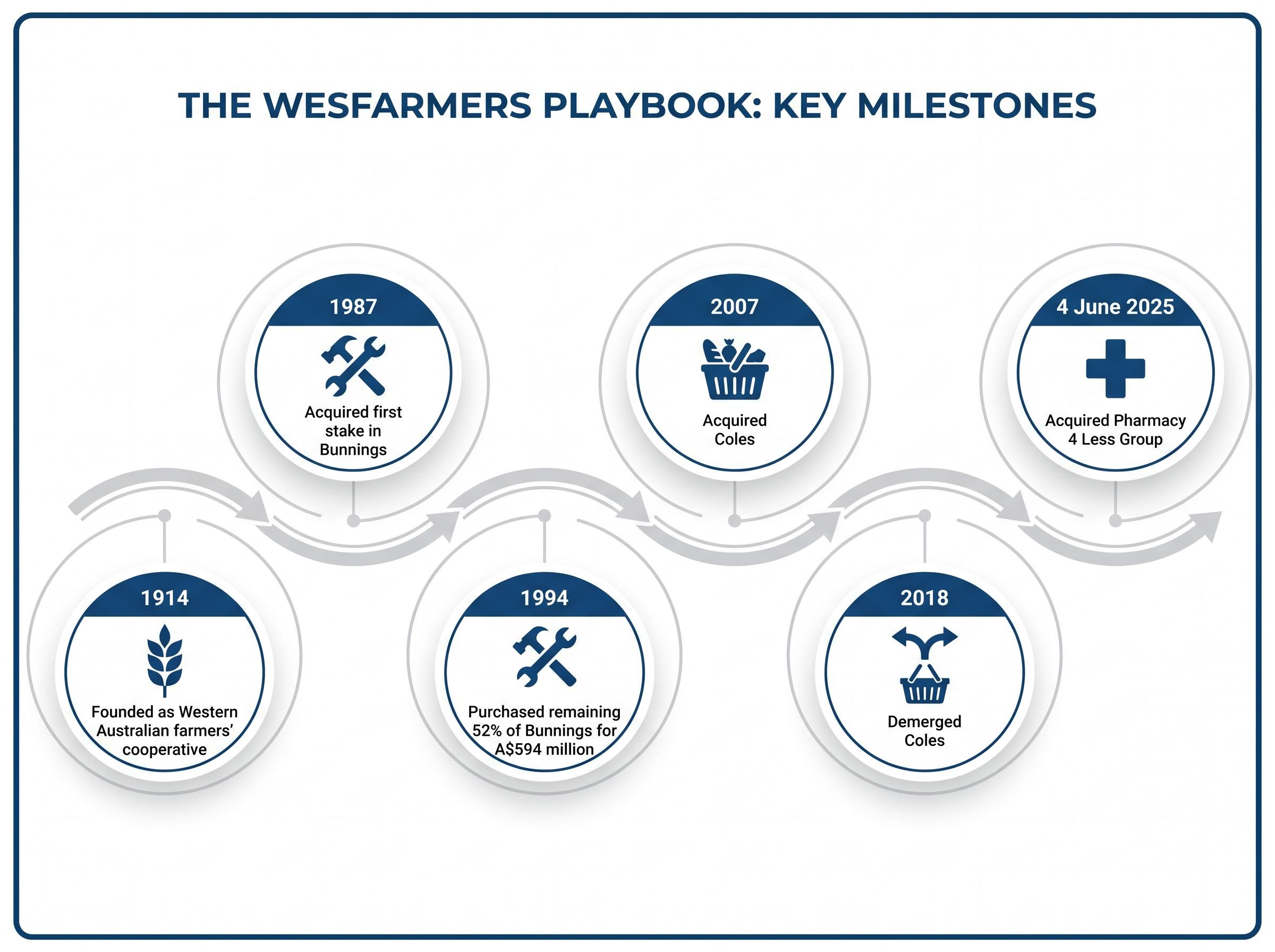

Wesfarmers was founded in 1914 as a Western Australian farmers’ cooperative. More than a century later, it operates as something closer to a listed private equity vehicle than a traditional retailer: acquiring businesses, improving their operations, compounding returns, and divesting when the strategic logic changes.

The pattern is visible in two signature transactions. Wesfarmers acquired its first stake in Bunnings in 1987, then purchased the remaining 52% in 1994 for A$594 million. That single deal became the foundation of the group’s earnings. In 2007, the company acquired Coles, ran it for a decade, then demerged it in 2018 when it judged the supermarket business had reached a natural ceiling under conglomerate ownership.

Today, the group carries a market capitalisation of approximately A$81.2 billion and is headquartered in Perth, Western Australia. The portfolio is broad, but earnings concentration is narrow.

From hardware to healthcare: how the current portfolio took shape

The current divisional structure reflects the latest iteration of the acquisition-and-divestment playbook:

- Bunnings: Australia’s dominant hardware and home improvement retailer, and the group’s primary earnings engine

- Kmart/Target: General merchandise retail, repositioned toward value-focused consumers

- Officeworks: Office and technology supplies, with a growing small business services offering

- Wesfarmers Health: Priceline Pharmacy and, since 4 June 2025, the Pharmacy 4 Less Group, extending the retail pharmacy footprint into the discount chemist segment

- WesCEF: Chemicals, energy, and fertilisers, including a Western Australian lithium operation where a potential capacity doubling is under consideration, with a final decision expected later in 2026

The healthcare acquisitions and the lithium expansion consideration are the newest expressions of the playbook. Whether they compound as effectively as Bunnings remains the open question.

Bunnings carries the group: what the latest earnings show

Three figures from the 1H FY2026 results (half-year to 31 December 2025, reported 19 February 2026) define the current earnings picture:

- Group revenue: A$24,212 million, up 3.1% on the prior corresponding period

- Group EBIT: A$2,493 million, up 8.4%

- Interim dividend: A$1.02 per share, fully franked

EBIT growth of 8.4% in the first half of FY2026 demonstrates that the quality premium in the share price is not entirely unearned.

Bunnings delivered sales growth of 4.0% in the half, consistent with the low-to-mid single-digit trajectory the division has sustained since post-COVID normalisation. Scale advantages with suppliers, tight cost management, and growth in higher-margin categories continue to support margins.

For the full year of FY2025, group revenue reached A$45,700 million (up 3.4%) and total dividends came to approximately A$2.13 per share. The interim dividend of A$1.02 for 1H FY2026 suggests the progressive dividend growth track record remains intact.

The concentration risk is the other side of the same coin. Bunnings is the load-bearing pillar. Any softening in its growth trajectory would disproportionately affect both group earnings and the dividend sustainability assessment that underpins the income case.

The bull case, the cautionary view, and where the valuation consensus lands

| Bull Case | Cautionary View |

|---|---|

| Entry point is materially improved versus recent highs | Trailing yield of 2.99% remains 94 basis points below the five-year average; the stock is not historically cheap on income terms |

| Fully franked dividends with a progressive growth track record | A quality premium to market and sector peers remains embedded in the multiple |

| Bunnings’ structural resilience provides earnings stability through softer consumer environments | Pharmacy 4 Less integration alongside Priceline adds execution complexity; the health segment has not yet reached its targeted return profile |

| Healthcare and lithium provide medium-term growth optionality for future dividend growth | Lithium expansion decision carries capital allocation risk in a depressed commodity price environment |

The sell-side consensus gravitates toward a familiar characterisation: high quality, not cheap on traditional metrics. Fund managers frequently describe Wesfarmers as a core holding suited to buy-on-weakness strategies, and the proximity to the 52-week low has prompted commentary acknowledging improved risk-reward.

That framing stops well short of calling the stock an outright bargain. The valuation still embeds a quality premium, and upside from current levels depends on sustained earnings execution from Bunnings, successful integration of the healthcare portfolio, and disciplined capital allocation on the lithium expansion. For income-oriented investors, WES fits a defensive, long-term allocation that prioritises stability and fully franked income over deep value or high absolute yield.

What dividend yield theory actually tells investors (and what it misses)

Dividend yield as a valuation signal rests on a mean-reversion premise. Over time, a stock’s yield tends to fluctuate around an average. When the yield dips below that average, the share price has risen faster than dividends, implying the stock is expensive relative to its own income history. When the yield rises above the average, the opposite holds.

For Wesfarmers, the current yield of 2.99% versus the five-year average of 3.93% places the stock firmly in the “price has outrun income” camp. The signal is useful as a relative indicator, a way to compare today’s valuation against the stock’s own history, rather than an absolute buy or sell trigger.

Yield analysis works best alongside other tools. Discounted cash flow models, dividend discount models, and earnings-based multiples each capture dimensions that yield alone misses. The risk-free rate context also matters; income investors comparing a 2.99% yield against the RBA cash rate and term deposit alternatives need the full picture.

Key limitations of yield-based valuation:

- It ignores earnings growth potential; a low yield on a fast-growing dividend may still represent good value

- It is sensitive to changes in dividend policy; a payout ratio shift can distort the signal

- It requires a stable payout ratio to be meaningful over time

- It does not account for balance sheet quality or capital allocation optionality

Why franking credits change the income calculation for Australian investors

Fully franked dividends carry embedded tax credits that increase the effective income for Australian resident investors. For a shareholder on a 30% marginal tax rate, Wesfarmers’ fully franked A$2.13 DPS grosses up to approximately A$3.04, producing a grossed-up yield of roughly 4.27% at current prices.

For self-managed super fund (SMSF) investors and retirees in lower tax brackets, the effective improvement is even more pronounced; those paying 0% tax in the pension phase receive the full franking credit as a refund. This franking benefit is a material consideration that headline yield figures alone do not capture.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Upcoming catalysts that could move the valuation dial

Three corporate events will add material new information to the valuation picture over the coming months:

- Strategy Briefing Day (10 June 2026): Expected to cover capital allocation priorities, Bunnings growth plans, and healthcare integration progress, this is the nearest opportunity for management to update the market on strategic direction.

- FY2026 full-year results (expected August 2026): Bunnings’ second-half performance and the final dividend announcement will be the focal points for income investors assessing whether the progressive dividend track record extends another year.

- Lithium expansion decision (expected later in 2026): A potential capacity doubling at the Western Australian mine represents a material capital allocation event that will either reinforce or test the market’s confidence in management’s reinvestment discipline.

Investors should also monitor several ongoing risks:

- Consumer spending pressure weighing on Bunnings and Kmart/Target traffic and basket sizes

- Healthcare integration execution as Pharmacy 4 Less is absorbed alongside the existing Priceline network

- Digital investment returns across all retail banners, which remain long-dated and not yet fully visible in divisional earnings

- Valuation premium compression if earnings growth disappoints or the broader market re-rates

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A quality blue-chip at a quality price: what WES near its 52-week low actually means

The central finding is simple to state and frequently misunderstood. Wesfarmers can trade less than 1% above its 52-week low and still carry a valuation premium on dividend yield terms. Both facts are true simultaneously in mid-May 2026, and recognising the distinction is the first step toward a disciplined income assessment.

For income-focused investors, the realistic options are clear. Accept the quality premium as the cost of owning a structurally resilient, fully franked compounder. Wait for a yield closer to the 3.93% five-year average, which implies a meaningfully lower share price. Or look elsewhere for a higher starting yield and accept different risk characteristics.

The 10 June 2026 Strategy Briefing Day and the FY2026 full-year results expected in August 2026 are the next substantive valuation checkpoints. The lithium expansion decision will test capital allocation discipline. Until those events deliver new information, the yield gap tells the story: quality compounders rarely go on sale, and Wesfarmers is no exception.

These statements are speculative and subject to change based on market developments and company performance.