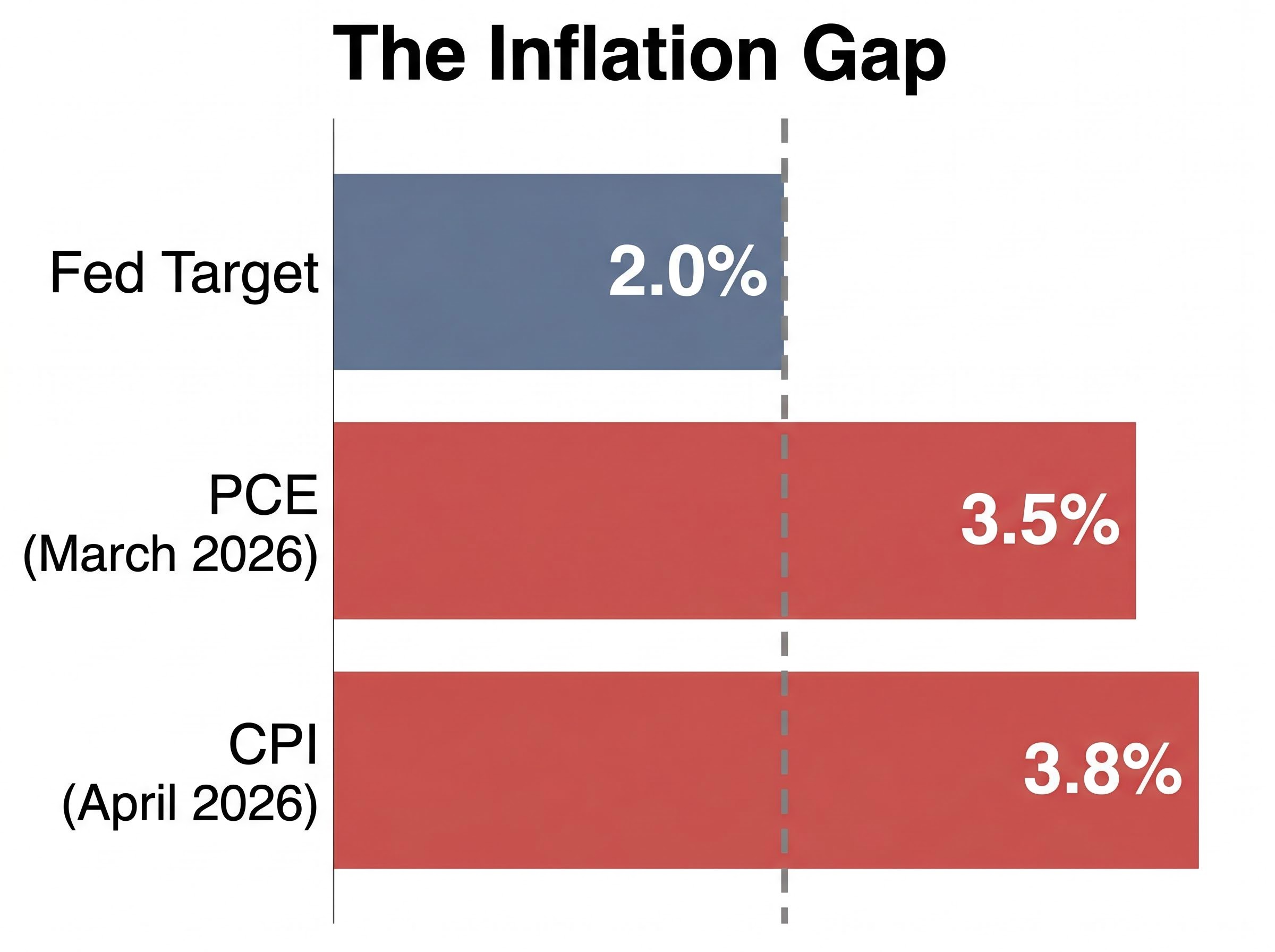

The U.S. Senate confirmed Kevin Warsh as Federal Reserve Chair on 13 May 2026, by a 54-45 vote, handing the nation’s most consequential monetary policy role to a 56-year-old lawyer-financier who has pledged to shrink the Fed’s $6.7 trillion balance sheet and hold an uncompromising line on inflation. The confirmation arrived with consumer prices running at 3.8% year-over-year and the Fed’s preferred inflation gauge at 3.5%, both well above the 2% target. Warsh replaces Jerome Powell, whose chairmanship expires on 15 May 2026. What follows breaks down the contested confirmation process, the independence debate that divided the Senate, and what Warsh’s two stated policy priorities mean for interest rates, the Fed’s bond portfolio, and investors operating in an already-stressed inflationary environment.

A two-day Senate process puts Warsh at the Fed’s helm

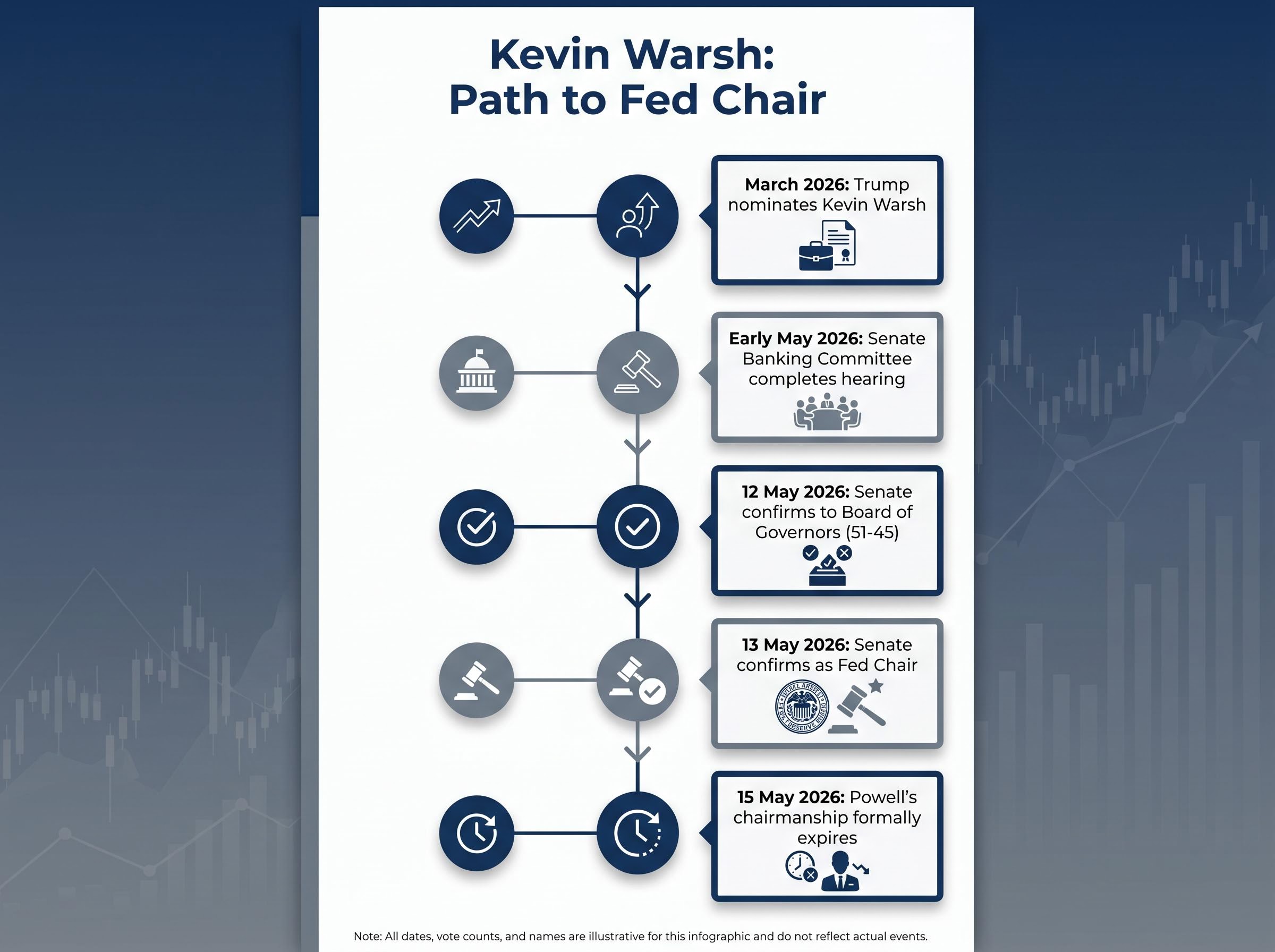

The path to confirmation was a two-step procedure, and neither step was smooth. President Trump nominated Warsh in March 2026. The Senate Banking Committee, chaired by Sen. Tim Scott, completed its confirmation hearing and moved both votes to the floor.

- March 2026: Trump nominates Kevin Warsh for Fed Chair

- Early May 2026: Senate Banking Committee completes confirmation hearing

- 12 May 2026: Senate confirms Warsh to the Board of Governors, 51-45

- 13 May 2026: Senate confirms Warsh as Fed Chair, 54-45

- 15 May 2026: Powell’s chairmanship formally expires

Two separate votes were required because the Fed Chair must first hold a seat on the seven-member Board of Governors. The Governor vote on 12 May cleared that prerequisite; the Chair vote the following day was a distinct confirmation of the leadership role itself.

The process nearly stalled. Sen. Thom Tillis placed a hold on proceedings before withdrawing it after the Department of Justice closed a criminal investigation into Jerome Powell over Fed building renovation cost overruns. The hold’s withdrawal cleared the procedural path, but the episode underscored how politically charged the appointment had become.

Powell stays on; Miran steps aside

Powell is not leaving the institution. In an uncommon step, the outgoing chair has opted to remain as a member of the Board of Governors after vacating the leadership seat. Fed Governor Stephen Miran departed the Board to create the vacancy Warsh now fills. The seven-member Board sets the upper bound of the Fed’s decision-making body, and the composition shift, Warsh in, Miran out, Powell staying, reshapes its internal dynamics from day one.

When big ASX news breaks, our subscribers know first

Why so many Democrats voted no, and why it matters for Fed credibility

The opposition was pointed. The majority of Democratic senators voted against Warsh on both ballots, and their stated concern centred on a single question: whether Warsh would protect the Fed’s independence on monetary policy from Trump administration pressure.

Warsh’s own position draws a deliberate line. During confirmation hearings, he committed to strict autonomy on interest rate decisions while signalling openness to coordination with the administration on non-monetary matters such as regulatory scope. That distinction satisfied enough Republican senators to secure confirmation. It did not satisfy Democrats, who argued the line would blur under sustained political pressure from a president who has not been shy about expressing rate preferences publicly.

According to Morningstar and MarketWatch, defending Fed independence is the “day one test” that will determine whether markets treat Warsh as a credible autonomous actor or price in a political discount from the outset.

The picture is not one-sided. The Economist argued in an April 2026 analysis that Warsh “could save the Federal Reserve” precisely because his track record and stated commitments suggest a more independent posture than his critics anticipate. Analysis published in The Conversation reached a similar conclusion. Whether that independent streak holds under real-world pressure remains the unresolved question, and it is one markets will answer through bond yields and dollar pricing, not op-eds.

The FOMC’s internal fracture predates Warsh’s arrival: the 8-4 dissenting bloc recorded in early May 2026 was the largest since 1992, with inflation running above the 2% target for five consecutive years, a structural persistence that makes the committee’s divisions about more than any single meeting outcome.

Brookings research on central bank independence and inflation finds that sustained political pressure on central banks raises long-run inflation expectations unless offset by credibly independent monetary governance, a finding that frames the Democratic opposition’s concerns as economically grounded rather than purely partisan.

What the Fed’s balance sheet actually is, and why Warsh wants to shrink it

The Federal Reserve’s balance sheet sits at approximately $6.7 trillion as of May 2026. That figure represents the total value of financial assets the Fed holds, accumulated primarily through successive rounds of quantitative easing (QE), a programme in which the central bank purchased bonds to push down interest rates and stimulate the economy during periods of stress.

The balance sheet’s main components are:

- U.S. Treasury securities: Government bonds of various maturities

- Mortgage-backed securities (MBS): Bundles of home loans packaged as tradeable bonds

- Other assets: Including lending facilities and foreign currency holdings

The balance sheet expanded significantly from pre-pandemic levels through QE programmes launched during the 2008 financial crisis and again during the COVID-19 pandemic. Warsh has characterised this bond portfolio as functioning more like fiscal policy (government spending decisions) than monetary policy (interest rate management), and that framing underpins his push for aggressive reduction.

Warsh’s balance sheet reduction philosophy frames the $6.7 trillion portfolio not as a monetary policy residual but as an active fiscal intrusion, a distinction that explains why accelerating quantitative tightening ranks higher in his stated priorities than adjusting the federal funds rate itself.

Quantitative tightening (QT) is the reverse process. Rather than buying new bonds, the Fed allows existing holdings to mature without reinvesting the proceeds. The effect is straightforward: money that would otherwise circulate in the financial system is withdrawn, tightening financial conditions and putting upward pressure on longer-term Treasury yields.

| Policy Tool | What It Does | Warsh’s Stated Direction | Market Effect |

|---|---|---|---|

| Federal funds rate | Sets overnight borrowing cost between banks | Hold or raise; no cuts while inflation persists | Higher short-term borrowing costs across the economy |

| Balance sheet (QT) | Reduces Fed bond holdings by not reinvesting maturing securities | Accelerate reduction of $6.7 trillion portfolio | Upward pressure on longer-term Treasury yields; tighter financial conditions |

For investors, an accelerated QT programme means higher borrowing costs across mortgages, corporate debt, and government financing, making this the single most consequential near-term policy variable Warsh controls beyond the federal funds rate itself.

The inflation problem Warsh is inheriting, and what a hawkish chair could do about it

The numbers facing Warsh on his first day leave little room for ambiguity:

The BLS April 2026 CPI release confirms the all-items index rose 3.8 percent over the prior 12 months, providing the official benchmark against which Warsh’s inflation mandate will be measured from his first day in the role.

- CPI (April 2026): 3.8% year-over-year

- PCE (March 2026): 3.5% year-over-year

- Core PCE (March 2026): Index level 129.279

Some Fed policymakers see inflation broadening beyond tariffs and Iran-conflict-linked energy prices into services and shelter categories that are harder to reverse. Gold closed at approximately $4,698.15 per troy ounce on 13 May (down 0.36%), while the U.S. Dollar Index stood at 98.53 (up 0.24%), a pairing that suggests markets are pricing persistent inflation alongside marginal dollar strength tied to hawkish expectations.

Oil-driven inflation pressures complicate Warsh’s inherited data picture considerably: Brent crude at $106 per barrel is contributing an estimated 40-60% pass-through into core CPI over a 3-6 month lag, meaning the June and July inflation prints carry more policy weight than the April figures Warsh sees on day one.

Warsh has stated the Fed will focus on price stability “without excuse,” signalling he may resist rate cuts even if economic growth softens.

That framing carries weight. A chair who has publicly committed to an uncompromising inflation stance inherits a data picture that may require him to follow through.

Could rates go higher, not just stay higher?

The internal Fed debate has moved beyond the question of when to cut rates. Some officials have been openly discussing rate increases rather than merely holding steady, given broadening price pressures. Under Warsh’s stated framework, a rate hike would become more likely if inflation fails to decelerate over the next two quarters while the labour market remains tight. The distinction matters: “higher for longer” and “higher still” produce very different outcomes for bond portfolios and equity valuations.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding monetary policy are speculative and subject to change based on economic conditions and Fed decision-making.

What Warsh’s ascent signals for investors over the next 12 months

The two policy priorities, aggressive balance sheet reduction and an uncompromising inflation stance, converge on a single directional message: the rate and liquidity environment under Warsh is likely to be tighter than the final stretch of the Powell era.

According to Morningstar and MarketWatch’s “five tests” framework published on 13 May 2026, analysts are watching independence credibility, inflation response, balance sheet pace, forward guidance reform, and communication clarity as the metrics that will define Warsh’s first year.

| Asset Class | Warsh Policy Driver | Likely Direction | Key Risk to Watch |

|---|---|---|---|

| Long-duration Treasuries | Accelerated QT withdrawing demand | Yields higher | QT pace exceeds market absorption capacity |

| Mortgage markets | MBS runoff plus elevated rates | Financing costs rise | Housing market stress if rates spike |

| Growth equities | Higher discount rates compress multiples | Valuation pressure | Earnings growth insufficient to offset rate drag |

| U.S. dollar | Hawkish stance supports yield differential | Moderate strengthening | Independence concerns trigger credibility discount |

Two unknowns could shift the picture materially. First, whether Warsh’s stated plans to overhaul forward guidance and inflation measurement methodology produce actual changes; such reforms could themselves move markets. Second, whether inflation moderates on its own before forcing a rate decision, giving Warsh room to focus on institutional reform rather than the blunt instrument of rate hikes.

For investors wanting to translate the directional signals in the asset class table into concrete portfolio adjustments, our dedicated guide to investing during rate hikes covers sector rotation toward high-margin low-debt equities, dollar-cost averaging frameworks for volatile entry conditions, and the specific leverage exposure metrics to monitor when financing costs are rising.

The Fed chair who could redefine the institution, for better or worse

Warsh enters the role having publicly criticised the Fed’s own practices on forward guidance and inflation measurement. He has a stated mandate to restructure how the institution communicates with markets, a mandate that, if executed, would represent the most significant operational reform at the Fed in over a decade.

The Economist argued in April 2026 that Warsh “could save the Federal Reserve” by restoring institutional discipline. The Democratic opposition’s 45 votes against his confirmation suggest an equal number of senators believe he could do the opposite.

The partisan confirmation margins mean scrutiny of every rate decision will be elevated. Warsh will need to demonstrate separation from the Trump administration through actions, not statements. Powell’s chairmanship expires on 15 May, making the transition official within 48 hours of the 54-45 vote. Warsh’s first FOMC meeting will be the first concrete test of whether his stated framework survives contact with the political and economic pressures of the role.

The next 90 days will reveal whether the reform agenda and independence commitments hold. Markets are not waiting for the answer; they are already pricing the question.