Aristocrat Leisure shares surged approximately 10% on 13 May 2026, a striking outperformance on a day when the ASX 200 was tracking down nearly 1% for its fourth consecutive losing session. The move followed the pre-market release of the company’s first-half FY26 results, which showed reported revenue barely moving while constant-currency earnings grew at a materially faster pace. That gap between the headline numbers and the underlying operational momentum is what prompted investors to reassess Aristocrat Leisure’s share price trajectory in a single session. What follows unpacks the specific numbers behind the market’s reaction, what each of Aristocrat’s three business divisions contributed, and what management’s guidance signals for the full year and beyond.

The share price move in context: a 10% surge against a falling market

While the ASX 200 fell approximately 0.92% on 13 May 2026, marking its fourth straight down session, Aristocrat Leisure (ASX: ALL) moved sharply in the opposite direction. The stock had closed in the range of approximately A$45.85 to A$46.38 on 12 May and traded in an approximate intraday range of A$46 to A$52 on results day.

That places the stock well above its 52-week low of approximately A$44.18, which it was approaching before the result, but still considerably below its 52-week high of approximately A$73.29.

The result lands against a backdrop that matters: the stock’s 36% decline from its August 2025 peak to approximately A$46.83 had pushed it toward levels where the gap between the share price and broker consensus targets was widening, compressing the multiple that the market was willing to assign to the underlying earnings quality.

Key share price data points for context:

- Prior close (12 May 2026): approximately A$45.85 to A$46.38

- Intraday trading range (13 May 2026): approximately A$46 to A$52

- 52-week high: approximately A$73.29

- 52-week low: approximately A$44.18

The scale of the move against a weak broader market signals the result cleared a meaningful expectations hurdle. Precise intraday figures should be confirmed via ASX real-time feeds or Bloomberg for exact levels.

When big ASX news breaks, our subscribers know first

Reported numbers versus constant-currency reality: how to read the headline figures

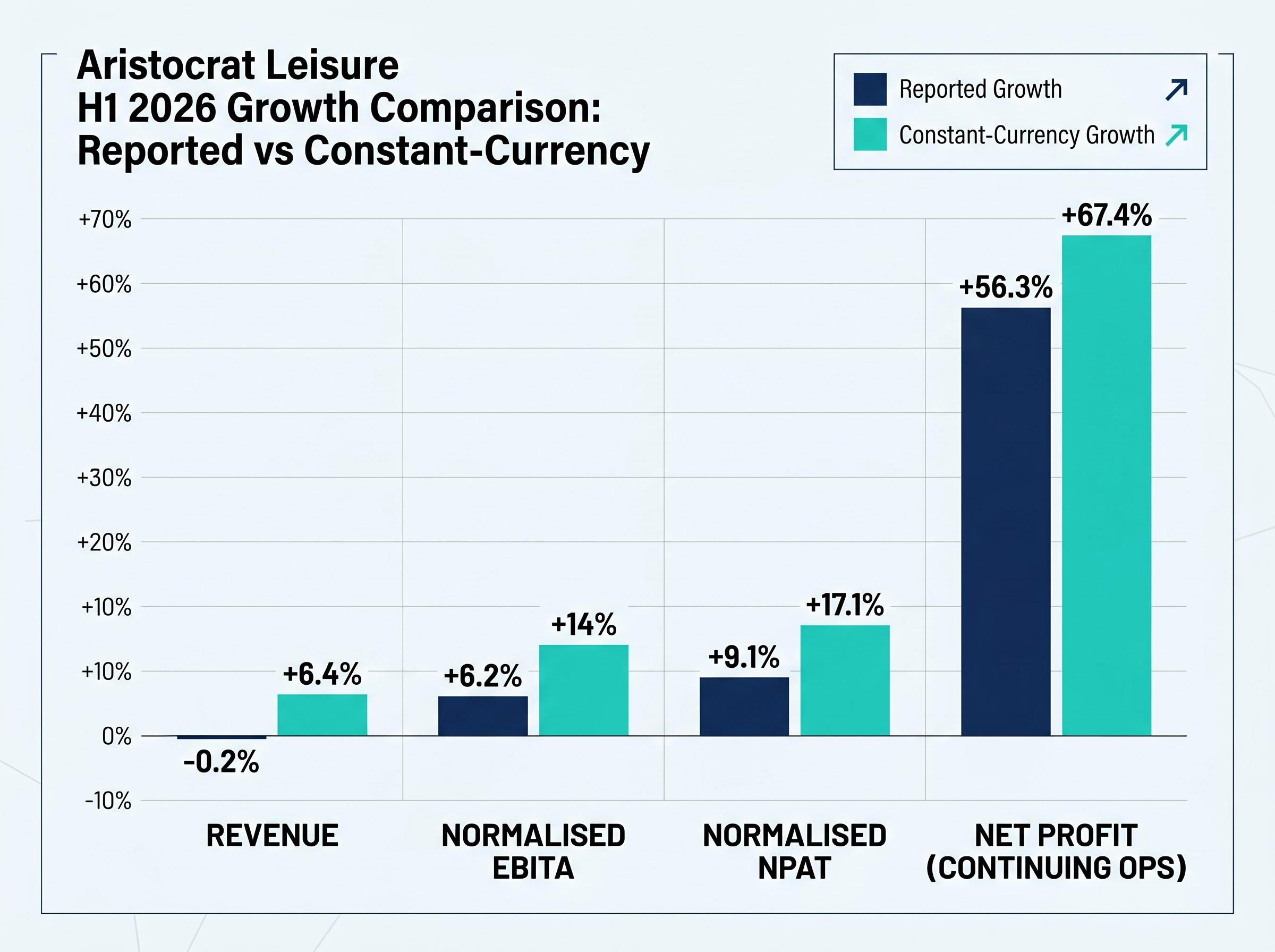

At first glance, Aristocrat’s top line barely moved. Total revenue edged down 0.2% on a reported basis to approximately US$2.2 billion for the six months ending 31 March 2026. That figure alone would not justify a 10% share price jump.

The constant-currency picture tells a different story. Stripping out foreign exchange translation effects, revenue advanced 6.4%, normalised EBITA grew 14% to US$1.12 billion, and normalised net profit after tax rose 17.1%. The standout line was net profit from continuing operations, which reached A$511 million, up 56.3% on a reported basis and 67.4% in constant-currency terms.

| Metric | Reported Value | Reported Growth | Constant-Currency Growth |

|---|---|---|---|

| Revenue | ~US$2.2B | -0.2% | +6.4% |

| Normalised EBITA | US$1.12B | +6.2% | +14% |

| Normalised NPAT | — | +9.1% | +17.1% |

| Net Profit (Continuing Operations) | A$511M | +56.3% | +67.4% |

Why constant-currency metrics matter for Australian investors

Aristocrat earns the majority of its revenue in US dollars while reporting in the same currency. For Australian investors, movements in the AUD/USD exchange rate can significantly distort how translated earnings appear, making the operational performance look stronger or weaker than it actually is. In this half, the translation effect systematically understated the company’s operational momentum, which is why constant-currency figures are the more reliable gauge of underlying performance.

What drove the numbers: a division-by-division breakdown

Aristocrat Gaming

The land-based gaming division remained the strongest performer. Management cited market share gains in both North America and Australia, supported by outright sales strength and continued expansion of the gaming operations installed base.

- North American and Australian outright sales delivered above-market growth

- The gaming operations installed base continued to expand, with full-year net unit growth targeted at the higher end of the 4,000 to 5,000 unit range

- Market share gains were referenced across multiple geographies in management commentary

Product Madness (Social Casino)

Aristocrat’s social casino arm outperformed the broader market in the half, driven by sustained investment in user acquisition and growing direct-to-consumer conversion.

- Revenue growth outpaced the social casino market

- User acquisition spending remained elevated as a deliberate growth investment

- Direct-to-consumer conversion rates improved, supporting higher per-user economics

Aristocrat Interactive

The Interactive segment delivered a more mixed result. iLottery and content performance were strong, but constant-currency revenue growth decelerated to approximately 6.4-6.5% in H1 2026, down sharply from approximately 20% in the prior comparable period.

- iLottery and content business lines delivered positive growth

- The deliberate exit from white-label operations weighed on the segment’s headline revenue; this was a strategic decision, not an operational failure

- The deceleration from approximately 20% to approximately 6.5% constant-currency growth is the single biggest source of ongoing investor caution

The net picture is positive but uneven. Gaming and Social Casino are firing reliably, while Interactive carries execution risk that matters for anyone building a thesis around the segment’s FY29 revenue target.

EBITA margin expansion to 36.9% in HY26, up from 28.6% in FY22, reflects the operating leverage the business has generated as recurring revenue crossed 70% of group revenue, a structural shift that amplifies the earnings impact of each incremental unit of topline growth.

Buyback expansion and dividend increase: reading the board’s confidence signal

Aristocrat did not limit its results-day announcements to earnings. The board expanded the on-market share buyback by A$1 billion to a cumulative total of up to A$2.5 billion, extended through to 12 May 2027. The interim dividend rose 13.6% to A$0.50 per share.

Total capital returned to shareholders via dividends and buybacks in the half: A$981 million.

The three components of the capital return package:

- Interim dividend: A$0.50 per share, up 13.6%

- Buyback expansion: cumulative total increased to up to A$2.5 billion

- Buyback extension: programme now runs through to 12 May 2027

An A$981 million capital return in a single half, combined with a buyback running into mid-2027, reflects management’s confidence in the company’s cash generation capacity and provides a tangible floor for investor sentiment even as the Interactive growth trajectory remains under scrutiny.

Ex-dividend price mechanics mean the A$0.50 per share payout is not additive to shareholder wealth in isolation: the share price adjusts downward by approximately the dividend amount on the ex-dividend date, so the capital return’s real value lies in its signal about management’s confidence in ongoing cash generation rather than in the raw yield figure.

Full-year guidance and the path to US$1 billion in Interactive revenue

Management’s full-year guidance provides a near-term anchor. Aristocrat expects underlying net profit growth for the year ending 30 September 2026 on a constant-currency basis, with all three divisions expected to grow revenue and market share. The gaming operations net unit growth target sits at the higher end of the 4,000 to 5,000 range.

- Aristocrat Gaming: revenue and market share growth expected to continue

- Product Madness: above-market revenue growth anticipated

- Aristocrat Interactive: revenue growth targeted, with Anaxi/NeoGames integration as the primary lever

The longer-range ambition centres on the Interactive segment’s target of at least US$1 billion in annual revenue by FY29. CEO Trevor Croker has expressed conviction on the trajectory.

“Interactive on track for [at least] $1B by FY29 despite macro softness,” Croker stated during the results webcast, citing progress on Anaxi/NeoGames integration and US real-money gaming market share gains as supporting evidence.

Balancing that optimism, management flagged ANZ online gambling regulatory tightening as a headwind for the Interactive segment. Investors watching the stock over the next three years will need to weigh Croker’s conviction against the segment’s recent deceleration and regulatory pressures.

Australia’s online gambling reforms, administered through the Department of Social Services, include a series of consumer protection measures under the National Consumer Protection Framework for Online Wagering that directly constrain how interactive gaming operators can acquire and retain customers in the ANZ market, contributing to the regulatory headwind management flagged for the Interactive segment.

What analysts and investors are watching next

The broker consensus picture heading into the second half offers context for how the market is pricing the result. Available data places the average price target in the range of approximately A$62.88 to A$65.58, though these figures require verification against current Bloomberg data. Notably, Bell Potter cut its price target to A$61.00 in May 2026, contrary to some early reports of an upgrade.

Following the results, FY26 NPAT consensus estimates were revised upward by approximately 1.5%, a modest but directionally positive signal that institutional estimates are adjusting higher.

Two items will determine whether the market’s positive reaction holds:

- Interactive constant-currency revenue growth in H2: whether growth accelerates back toward historical rates or continues to decelerate toward the approximately 6.5% pace recorded in H1

- Buyback execution and price support: whether the expanded programme provides sufficient buying pressure given the stock remains well below its 52-week high of A$73.29

(Broker price targets and consensus figures should be verified against Bloomberg or the investor’s own broker platform before acting on them.)

The gap between current prices and the broker consensus range highlights both the opportunity and the execution risk investors are being asked to accept.

A strong result, but the Interactive question is still being answered

Constant-currency earnings growth of 14% on EBITA and 56.3% on net profit from continuing operations explains the market’s reaction more clearly than any single headline figure. The capital return programme reinforces management’s confidence in the company’s cash generation.

The unresolved tension remains the Interactive segment. A deceleration from approximately 20% to approximately 6.5% constant-currency revenue growth is material, and the market will continue to price that uncertainty in even as Croker reaffirms the FY29 target.

Investors watching ALL from here have two clear markers to track: the H2 FY26 Interactive constant-currency revenue trajectory and the pace of buyback execution. Those are the most meaningful signals of whether the result’s optimism proves durable.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

—