Finfluencer Rules Won’t Work Until the Penalty Beats the Profit

1 hr ago

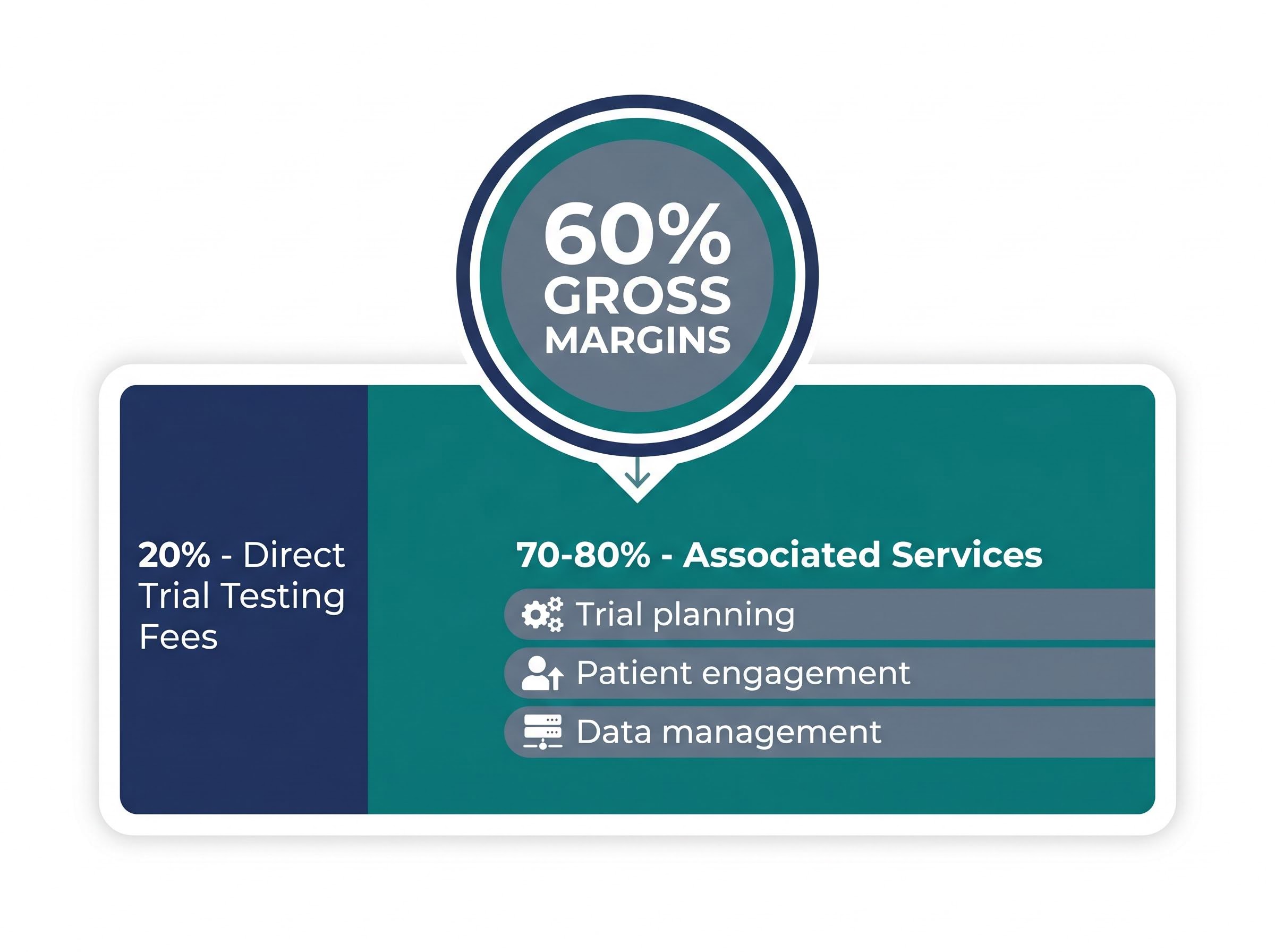

A single cognitive testing vendor embedded in a USD 1 billion Eli Lilly Alzheimer’s trial, capturing roughly 2% of that budget. That positioning explains how a A$400 million ASX small-cap generates 60% gross margins without ever needing to raise capital.

Cogstate (ASX:CGS) sits at the intersection of two durable structural forces: the global Alzheimer’s drug development pipeline and the regulatory requirement for independent third-party cognitive assessment in central nervous system (CNS) trials. With FY25 revenue up 22% and profit before tax nearly doubling, the company has graduated from early-stage promise to profitable compounder territory, yet it remains well below the ASX top 100 radar.

What follows is a detailed assessment of the Cogstate investment case for Australian retail investors, covering the business model, the financial profile, the valuation picture, and the specific risks that could undermine the thesis, so readers can form a considered view of whether the stock belongs in a small-cap portfolio.

Dementia now accounts for close to 10% of all recorded deaths in Australia, having surpassed cardiovascular disease as the primary cause of death. Across developed nations, it ranks among the top five killers. That epidemiological reality has driven sustained pharmaceutical investment into CNS drug development, and the spending is accelerating.

Large pharma firms cannot self-assess cognitive endpoints in the trials they sponsor. Regulatory frameworks require independent third-party vendors to administer and validate cognitive testing, creating a layer of non-discretionary demand that persists regardless of broader clinical trial budget cycles.

The FDA guidance on early Alzheimer’s drug development explicitly requires well-defined outcome measures and objective cognitive tests in clinical trials, a regulatory standard that makes independent third-party vendors like Cogstate a structural necessity rather than an optional line item in trial budgets.

The commercial logic runs deeper than compliance. A single testing error in a multi-hundred-million-dollar trial triggers field verification, physician callouts, and timeline delays that can cost sponsors weeks and millions. Established vendors with validated datasets are preferred over cheaper alternatives precisely because the cost of failure dwarfs the cost of the testing itself.

The global CNS clinical trial testing market is currently valued at approximately USD 600-700 million, with forecasts projecting expansion to USD 1.2-1.3 billion by 2030.

That market expansion, underpinned by regulatory structure rather than discretionary spend, is the foundation of the Cogstate revenue case.

The depth of the Alzheimer’s drug pipeline across ASX-listed companies illustrates why Cogstate’s addressable market extends well beyond a single sponsor; programmes using novel mechanisms such as GLP-1 receptor agonists and cortisol-targeting compounds are generating new Phase 2 and Phase 3 activity that requires independent cognitive endpoint measurement across multiple concurrent trials.

Cogstate’s revenue does not come from a single product line. Approximately 20% derives from direct trial testing fees, the cognitive assessments administered during clinical studies. The remaining 70-80% flows from broader associated services, including trial planning, patient engagement, and data management. This split matters because it means Cogstate captures value across the full trial lifecycle rather than billing for a narrow deliverable.

The result is a business with 60% gross margins that look less surprising once the revenue structure is understood. When the majority of revenue comes from high-touch services layered around a proprietary technology platform, the margin profile reflects intellectual property leverage rather than pricing power alone.

Three elements form the competitive moat:

Cogstate competes primarily against Clario (private) and Cambridge Cognition (smaller, LSE-listed). It is the only ASX-listed player in a three-firm oligopoly, a market structure that limits price competition and raises barriers to entry for new vendors.

Medidata, part of Dassault Systèmes, provides technical platform infrastructure for clinical trials. Cogstate contributes cognitive testing expertise. The combination is offered as an integrated solution to pharma clients, meaning trial sponsors can access Cogstate’s assessments through a platform they already use.

This arrangement reduces Cogstate’s sales and marketing expenditure relative to what an independent vendor would need to spend to maintain equivalent global reach. Medidata effectively functions as an outsourced global sales force. The partnership’s visibility was reinforced by Medidata’s attendance at Cogstate’s investor day, signalling an active commercial relationship rather than a passive licensing arrangement.

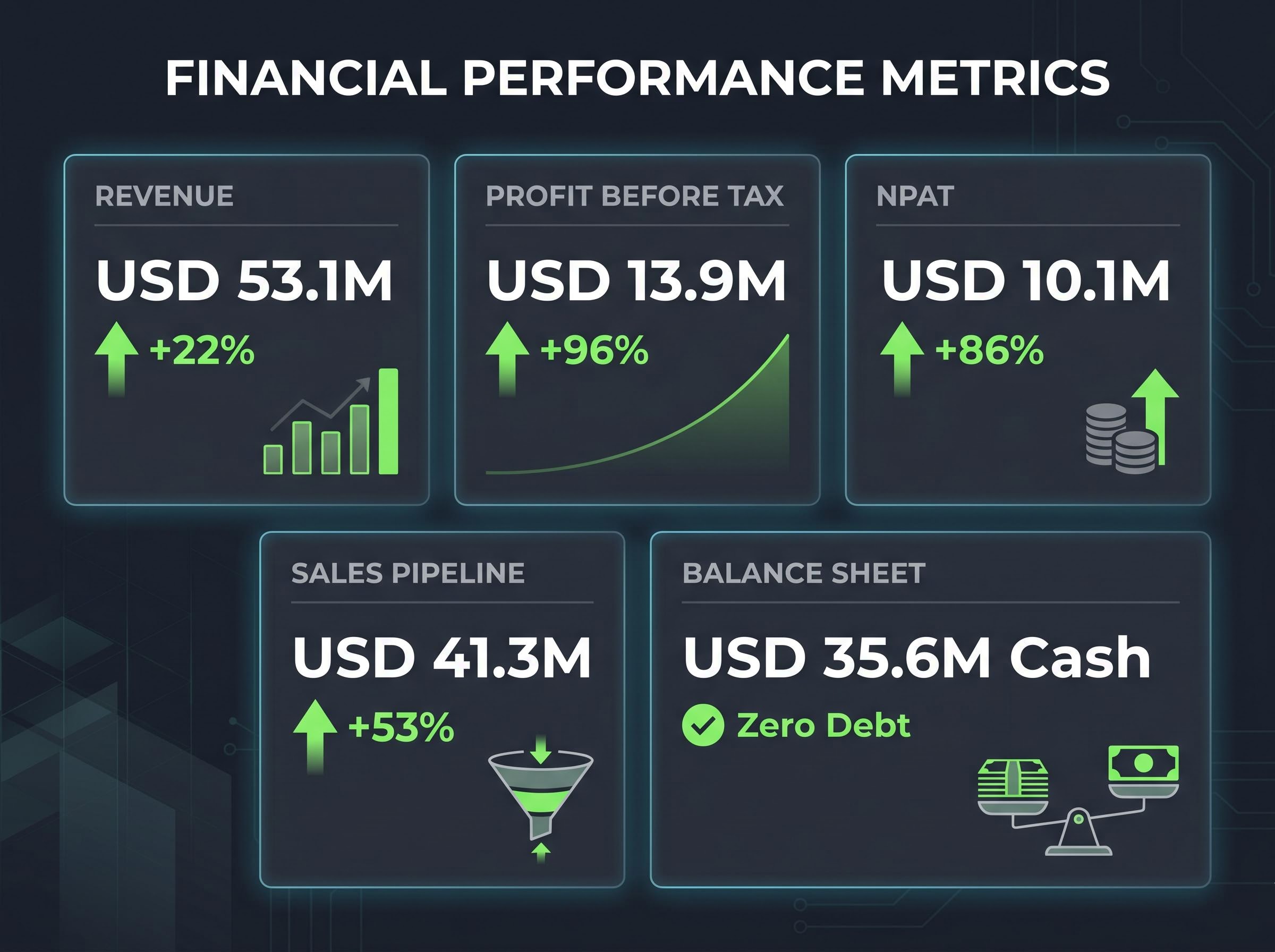

FY25 marked a step-change year. Revenue reached USD 53.1 million, up 22% year on year, with clinical trials revenue of USD 50.6 million growing 28%. Profit before tax hit USD 13.9 million, a 96% increase. Net profit after tax came in at USD 10.1 million, up 86%. The sales contracts pipeline expanded 53% to USD 41.3 million.

Each figure is independently notable. In combination, they describe a business where revenue growth is pulling operating leverage through the income statement while simultaneously building forward visibility through a growing contracted pipeline.

“Profit before tax nearly doubled year on year, rising 96% to USD 13.9 million in FY25.”

The 1H FY26 results, released on 19 February 2026, extended the pattern. Revenue of USD 26.9 million exceeded the USD 25-26 million guidance range. Earnings per share grew 17% year on year to USD 0.027, compared with USD 0.023 in the prior corresponding period. The beat reinforced a pattern of management under-promising and over-delivering on near-term guidance.

Balance sheet quality completes the picture. Cogstate held USD 35.6 million in cash with zero debt, declared a maiden fully franked dividend of A$0.02 per share, and stated its ability to fund all growth internally without capital raises.

| Metric | FY25 | 1H FY26 |

|---|---|---|

| Revenue | USD 53.1M (+22% YoY) | USD 26.9M (+12% YoY) |

| NPAT | USD 10.1M (+86% YoY) | USD 4.53M (+16% YoY) |

| EPS | n/a | USD 0.027 |

| Cash | USD 35.6M | USD 35.6M |

| Pipeline | USD 41.3M (+53% YoY) | n/a |

This is not a growth-at-all-costs story. It is a self-funding, cash-generative business with operating leverage, a materially different risk profile from most ASX small-cap technology names.

The bull case is straightforward on earnings multiples. At A$2.37 (as of May 2026), the stock trades at a 12-month forward PE of 19.93x with a PEG ratio of 1.3x. Consensus analyst price targets sit in the A$3.18-A$3.24 range, implying upside of roughly 35%. LSN Emerging Companies projects EPS growth of up to 50% in FY27, and consensus forecasts three-year EPS growth of 24.6% per annum. On mid-teens forward P/E estimates, that growth trajectory implies a meaningful re-rating case.

The tension arrives through free cash flow. The Price/FCF ratio of 77.99x is exceptionally elevated for a company at this stage.

The Price/FCF ratio of 77.99x requires the FY27 earnings growth forecast to be largely realised to justify the current valuation on a cash-generation basis.

Simply Wall St revised its price target down to A$2.41 in April 2026 (from A$2.60), reflecting margin compression concerns after FY26 guidance explicitly flagged a 0-3 percentage point margin headwind. That revised target sits only marginally above the current share price, leaving limited margin of safety on a DCF basis.

| Multiple | Value |

|---|---|

| Forward PE (12-month) | 19.93x |

| PEG Ratio | 1.3x |

| EV/EBITDA | 14.62x |

| Price/FCF | 77.99x |

| Price/Sales | 4.72x |

| Price/Book | 5.13x |

| Dividend Yield (forecast) | 1.92% |

The earnings-based multiples suggest the growth is not egregiously overpriced. The FCF-based metric suggests it could be. Retail investors benefit from holding both frameworks simultaneously rather than anchoring to a single headline number.

December 2025 provided the clearest illustration of what goes wrong when a high-multiple stock misses on timing. Cogstate shares fell approximately 22%, attributed to delayed revenue recognition rather than a deterioration in the underlying business. The sell-off was sharp and concentrated, and it demonstrated the mechanism through which elevated FCF multiples amplify downside: when the market is pricing in sustained execution, even a timing miss triggers a re-pricing.

FY26 guidance reinforced the near-term caution. Management explicitly flagged a 0-3 percentage point margin headwind from rising direct and operating costs. With only approximately three analysts covering the stock, there is limited independent scrutiny challenging the assumptions embedded in that guidance.

Four material risks warrant ongoing monitoring:

The structural risks to ASX healthcare extend beyond any single company, with FDA staffing reductions since 2025 creating approval backlogs that could delay trial timelines regardless of how well a vendor like Cogstate executes its own programme; companies whose revenue depends on active Phase 3 programmes face indirect exposure to regulatory capacity constraints that are not priced into most small-cap models.

The customer concentration gap is a genuine due-diligence hole. No public breakdown of revenue by pharma client is available in ASX filings, making it impossible for external investors to quantify single-client dependency. For a company where the top 20 shareholders control approximately 80% of shares outstanding, register concentration already narrows the liquidity profile; adding unquantified customer concentration compounds the risk.

Low analyst coverage cuts both ways. It creates potential for upside re-rating as institutional awareness grows, but it also means fewer independent voices challenging management’s guidance assumptions. The AI internalisation scenario remains theoretical for now, constrained by the same regulatory independence requirements that created Cogstate’s moat, but the 5-10 year horizon risk is worth monitoring as AI tools become more capable in clinical settings.

Cogstate occupies an unusual position in the ASX small-cap universe. 60% gross margins, self-funded growth, zero debt, a maiden fully franked dividend, and a contracted pipeline that grew 53% in FY25 are characteristics more commonly associated with mature mid-caps than with A$400 million companies operating at the lower boundary of the institutional investable universe.

Neuren Pharmaceuticals offers a comparable reference point for how a royalty-based CNS model can generate high-margin recurring revenue without the capital requirements of traditional drug development, demonstrating that the ASX small-cap universe contains more than one example of a CNS-adjacent business achieving profitable compounding at sub-institutional scale.

Consensus three-year forecasts project earnings growth of 24.5% per annum, revenue growth of 14.9% per annum, and return on equity of 25.4%. LSN Emerging Companies allocated an initial portfolio weighting of approximately 2%, consistent with a position size for a company at the smaller end of a concentrated fund’s range.

The investment case is neither a clear buy nor an obvious pass. It is a quality business with structural tailwinds, a contested valuation, and identifiable risks that are monitorable. For investors considering whether Cogstate warrants further research, four indicators deserve tracking over the next 12-24 months:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Cogstate is an ASX-listed company that provides independent cognitive testing services for pharmaceutical clinical trials, particularly in Alzheimer's and CNS drug development. Roughly 20% of its revenue comes from direct trial testing fees, with the remaining 70-80% flowing from broader services including trial planning, patient engagement, and data management.

Regulatory frameworks require pharmaceutical companies to use independent third-party vendors to administer and validate cognitive testing in clinical trials they sponsor, making Cogstate a non-discretionary necessity rather than an optional budget item. As the global Alzheimer's drug pipeline expands, demand for Cogstate's services grows alongside it regardless of broader clinical trial budget cycles.

In FY25, Cogstate reported revenue of USD 53.1 million (up 22%), profit before tax of USD 13.9 million (up 96%), and net profit after tax of USD 10.1 million (up 86%), while holding USD 35.6 million in cash with zero debt. First-half FY26 results released in February 2026 showed revenue of USD 26.9 million, beating the USD 25-26 million guidance range, with EPS growing 17% year on year.

Key risks include revenue timing sensitivity (a December 2025 sell-off of around 22% was triggered by delayed revenue recognition), unquantified customer concentration given no public breakdown of revenue by pharma client, exposure to Alzheimer's trial delays or Phase 3 failures at major sponsors, and a longer-term theoretical risk that AI tools could reduce demand for third-party cognitive testing. Management also flagged a 0-3 percentage point margin headwind for FY26 from rising direct and operating costs.

Medidata, part of Dassault Systemes, integrates Cogstate's cognitive testing into its widely used clinical trial platform, allowing pharma clients to access Cogstate's assessments through infrastructure they already use. This effectively provides Cogstate with an outsourced global sales force, reducing the sales and marketing expenditure the company would otherwise need to maintain equivalent international reach.