Finfluencer Rules Won’t Work Until the Penalty Beats the Profit

2 hrs ago

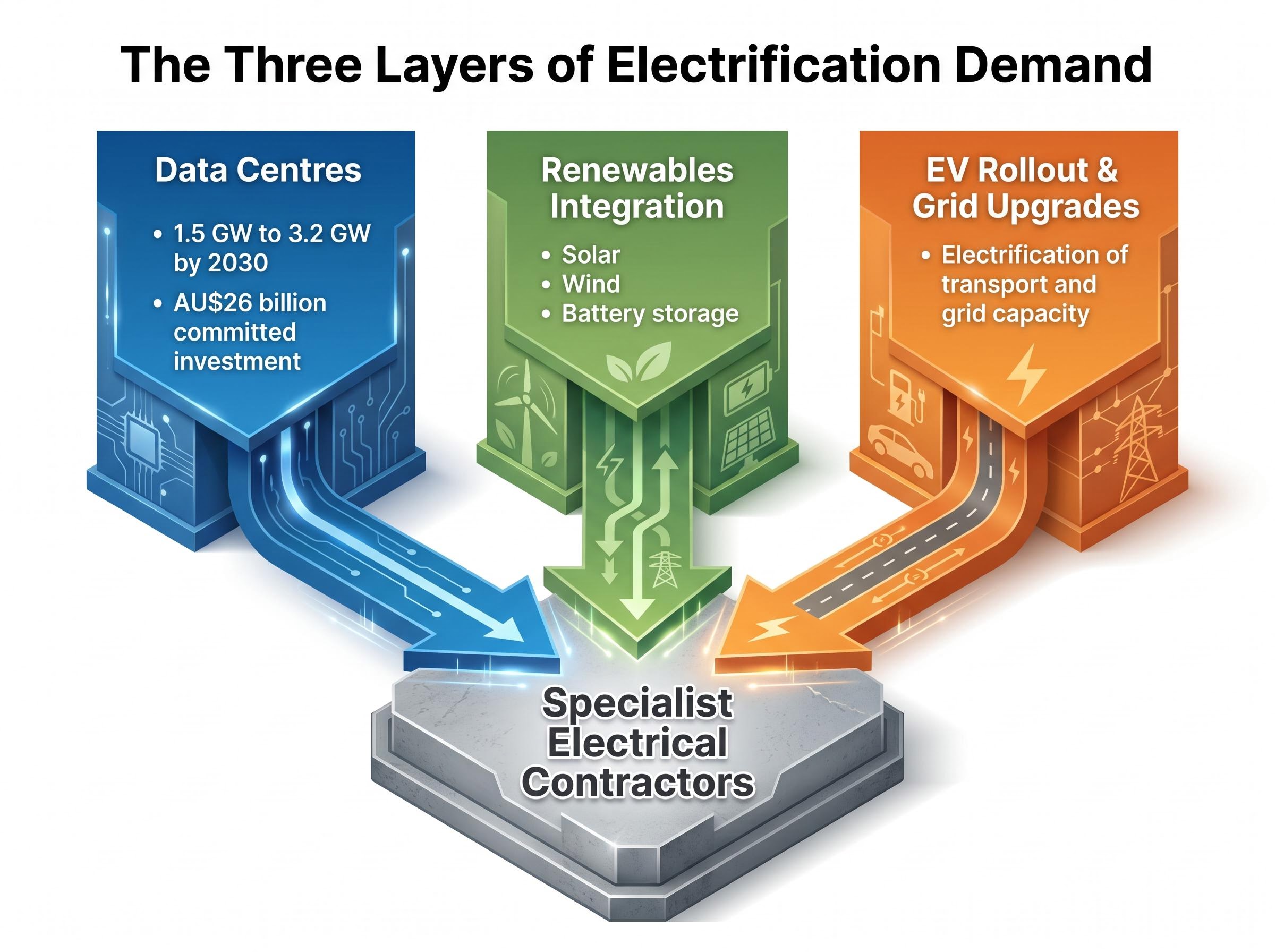

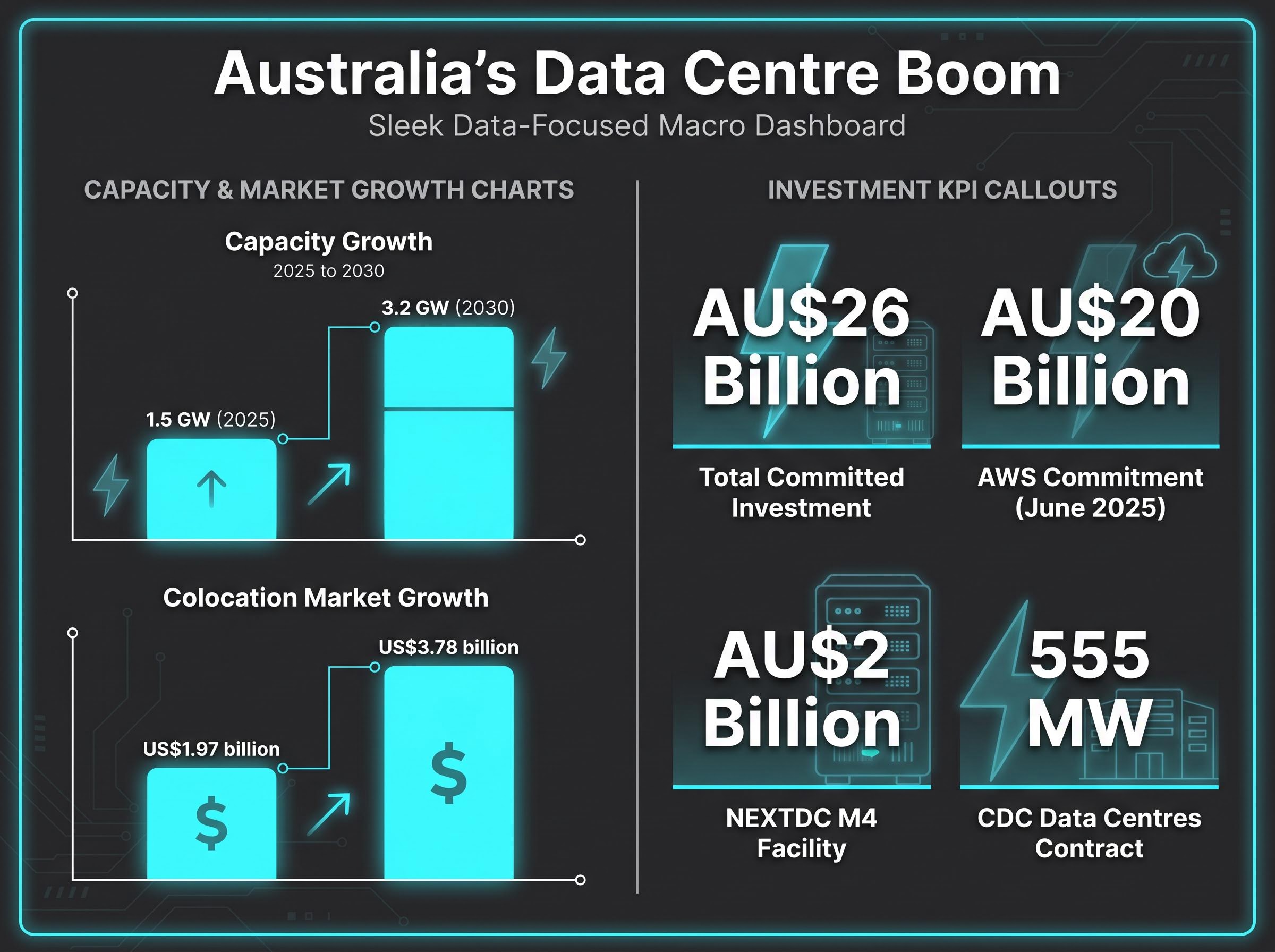

Australia’s data centre capacity is on track to double from 1.5 GW to 3.2 GW by 2030, underpinned by AU$26 billion in committed investment. The hyperscalers, colocation operators, and institutional capital backing that buildout have attracted enormous investor attention. Yet the specialist electrical contractors physically wiring these facilities, the companies without whom no data centre powers on, remain largely absent from mainstream coverage.

These businesses sit in the ASX small-cap space. Analyst coverage is thin. In several cases, earnings growth is accelerating at rates that larger-cap peers in the same supply chain have not matched. The convergence of data centre construction, renewables integration, and broader electrification is creating a multi-layered demand cycle for a handful of ASX-listed electrical engineering firms, and the structural independence of those demand layers is what separates this cycle from previous infrastructure booms.

What follows identifies the forces driving that demand, profiles the ASX small-cap electrical infrastructure stocks with the strongest recent evidence, explains how to evaluate picks-and-shovels plays in this space, and outlines the risks retail investors should weigh before entering.

Infrastructure spending cycles come and go. A mining boom lifts construction, then contracts. A government stimulus programme generates a burst of activity, then fades. Retail investors have seen this pattern enough times to treat any “super-cycle” narrative with scepticism.

This cycle has a structural difference: three independent demand drivers are accelerating simultaneously, and weakness in one does not collapse the thesis for the other two.

AWS committed AU$20 billion to Australian data centre infrastructure in June 2025, described as the largest investment in Australian technology history.

Grid constraints, often cited as a risk to the data centre pipeline, actually extend the cycle. Every grid upgrade required to unlock new capacity is itself a project that demands additional electrical engineering work. Eaton’s 2025 annual report identified data centre growth as the primary spur for grid investment, with the company committing US$13 billion in acquisitions targeting electrification technology. NEXTDC’s forward order book reached 544 MW as of March 2026, an 83% increase from prior periods.

The scale of hyperscaler capital expenditure is the structural ceiling against which Australian contractor pipelines should be measured: Amazon, Microsoft, Alphabet, and Meta collectively spent $130 billion in Q1 2026 alone, with full-year 2026 combined guidance reaching approximately $725 billion and a $1 trillion annual run rate targeted for 2027.

The result is a demand environment where three structurally independent forces reinforce one another rather than competing for the same capital pool.

The “picks and shovels” investment thesis is straightforward: during a gold rush, the most reliable profits often flow to the companies selling tools to miners rather than to the miners themselves. Applied to Australia’s data centre buildout, the equivalent is the specialist electrical contractors whose work sits between the concrete shell and the computing hardware.

These firms design, install, and commission the high-voltage and low-voltage electrical systems that allow a data centre to operate. That includes switchboards, power distribution units, backup generation systems, and increasingly, the liquid-cooling infrastructure required by AI-focused deployments. NEXTDC’s M4 facility in Melbourne, a AU$2 billion “AI Factory” designed for liquid-cooled Nvidia workloads, illustrates the technical complexity involved.

SXE brings more than 20 years of data centre sector-specific experience. That tenure matters because data centre developers do not select electrical contractors primarily on price.

The consequences of electrical installation failure in a data centre extend far beyond the contractor’s fee. Hyperscalers and colocation operators face several constraints that narrow their field of qualified partners:

GNX’s $2.6 billion tender pipeline offers a direct measure of forward visibility in this market. For incumbents with proven track records, the combination of technical complexity and failure consequences creates contract stickiness that insulates them from pure price competition.

Four ASX-listed electrical services businesses have reported results that confirm accelerating exposure to this theme. Each occupies a differentiated position within the supply chain.

Genus Plus (GNX) delivered H1 FY26 revenue of $535.4 million, up 61% year-on-year, with normalised EBITDA growth of 69%.

| Company | ASX Code | H1 FY26 Key Metric | Pipeline / Forward Visibility | Primary Market Focus |

|---|---|---|---|---|

| Southern Cross Electrical | SXE | Underlying EBITDA $35.4M (+30.8% YoY) | FY26 EBITDA guidance $65-68M (18-24% growth) | Data centres, renewables, commercial |

| Genus Plus | GNX | Revenue $535.4M (+61% YoY); EBITDA $46.3M (+69%) | $2.6B tender pipeline; recurring revenue +20% FY26 | Electrical infrastructure, utilities |

| SKS Technologies | SKS | Data centres and tech: 61.3% of total work on hand (H1 FY25) | Growing concentration in high-growth infrastructure | Data centres, AV/IT, electrical |

| IPD Group | IPD | Record H1 FY26 results (reported February 2026) | Diversified across EV, renewables, decarbonisation | Data centres, EV, renewables, decarbonisation |

SXE represents the most established data centre specialist, with its FY26 guidance midpoint of $66.5 million EBITDA reflecting a business that has successfully diversified from its mining heritage. GNX has delivered the most dramatic revenue acceleration, with its $2.6 billion tender pipeline providing the strongest forward visibility of the group.

SKS and IPD sit at an earlier growth stage with thinner analyst coverage. SKS has concentrated 61.3% of its work on hand in data centres and technology, suggesting a deliberate pivot toward the highest-growth segment. IPD, operating through subsidiaries including CMI Electrical with an estimated 501-1,000 staff as of 2026, offers broader exposure across EV infrastructure, renewables, and decarbonisation alongside data centres.

The risk-return profile varies. SXE and GNX offer more established earnings trajectories with greater analyst coverage. SKS and IPD carry more execution risk but also more upside if the structural demand thesis plays out as the pipeline data suggests.

Data centre switchboard contracts are now reaching individual deal sizes that were rare for small-cap electrical manufacturers twelve months ago: Mayfield Group’s $15.7 million single switchboard order, the largest in the company’s FY2026 history, reflects both the power density requirements of hyperscale AI facilities and the concentration of manufacturing capability in a small number of qualified Australian suppliers.

The four companies above are visible now. The more useful question for retail investors is how to evaluate the next wave of small-cap electrical infrastructure beneficiaries before institutional coverage arrives.

Thin analyst coverage in this context is an opportunity signal rather than a warning, provided the underlying demand metrics are independently verifiable. Hyperscaler capital expenditure announcements, government project awards, and colocation operator order books are all publicly available data points that confirm demand without requiring sell-side endorsement.

A practical evaluation framework, applied in logical sequence:

Investment criteria used by specialist emerging-company funds, such as the LSN Emerging Companies framework, reinforce these filters: multi-year revenue growth potential, strong returns on capital, healthy margins, experienced management, solid balance sheets, and reasonable valuations.

Portfolio construction logic matters here. These are high-upside, execution-dependent positions suited to modest allocation within a diversified portfolio rather than concentrated bets.

SXE’s approach to multi-sector contract diversification, spanning data centres, government infrastructure, resources, and logistics across three states, is directly relevant to the red flag framework: clients and sectors are spread broadly enough that no single customer relationship approaches the 40-50% concentration threshold that would create binary execution risk.

No structural thesis is without execution risk. The relevant distinction for retail investors is between risks that affect the pace of delivery and risks that undermine the demand itself.

Execution timing risks:

Structural demand risks:

The dominant analyst and industry view characterises current constraints as execution timing risks rather than structural demand risks.

Current evidence points overwhelmingly toward the former category. The demand itself continues to accelerate, with every major operator expanding pipeline commitments through the first half of 2026. Regulatory and policy shifts could alter delivery timelines without eliminating the multi-year demand backlog already contracted.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The demand signal is arriving simultaneously from both directions. From the top down, hyperscaler capital expenditure commitments totalling AU$26 billion confirm the pipeline. From the bottom up, contractor revenue acceleration, GNX at 61% revenue growth, SXE at 30.8% EBITDA growth, confirms that the spending is reaching the companies doing the physical work.

Australia’s data centre capacity trajectory from 1.5 GW to 3.2 GW by 2030, combined with a colocation market projected to grow from US$1.97 billion to US$3.78 billion over the same period, positions this as an early-to-mid acceleration phase rather than a late-cycle environment. GNX forecasts 20% recurring revenue growth in FY26. SXE’s guidance midpoint of $66.5 million EBITDA reflects a business still scaling into a widening opportunity.

CDC Data Centres’ 555 MW contract, described as the largest data centre deal in Australian history, confirms that hyperscaler appetite is intensifying rather than plateauing.

CDC’s 555 MW contract with a US investment-grade hyperscaler, the largest data centre deal in Australian history, pushed CDC’s total contracted capacity past 1 GW and provides a concrete measure of the deal sizes now moving through the Australian market, with Infratil projecting FY28 EBITDAF exceeding A$1 billion as a direct result.

For retail investors evaluating entry timing, the structural case remains intact. The primary return driver for these small-cap electrical services businesses over the coming years is likely to be earnings growth rather than multiple expansion, a profile that rewards patient capital positioned ahead of broader market recognition.

ASX electrical infrastructure stocks are small-cap companies listed on the Australian Securities Exchange that design, install, and commission electrical systems for data centres, renewables projects, and grid upgrades. Examples include Southern Cross Electrical (SXE), Genus Plus (GNX), SKS Technologies (SKS), and IPD Group (IPD).

Specialist electrical contractors are the primary beneficiaries because electrical work is the single largest construction cost component in a data centre build, and hyperscalers cannot use generalist contractors due to strict safety accreditations, timeline requirements, and the technical complexity of high-density power and liquid-cooling systems.

Genus Plus (GNX) reported H1 FY26 revenue of $535.4 million, up 61% year-on-year, with normalised EBITDA growth of 69%, and holds a $2.6 billion tender pipeline alongside forecast recurring revenue growth of 20% for FY26.

Key red flags include margin compression across consecutive reporting periods, customer concentration above 40-50% in a single client or sector, and debt-funded workload growth without corresponding improvement in cash conversion, which can mask deteriorating unit economics.

The picks-and-shovels thesis argues that the most reliable returns during a construction boom often flow to the suppliers of essential tools and services rather than the end operators; in the context of Australian data centres, this means specialist electrical contractors whose work is required before any facility can power on.