What 4 Wall Street Firms See Driving Markets in H2 2026

17 mins ago

Australia’s 2026 Federal Budget confirmed a structural overhaul of capital gains tax that will touch every long-term investor in the country from 1 July 2027. The headline framing, that CPI indexation will replace the 50% CGT discount, understates the real complexity. The proposed reform does not simply swap one concession for another. It layers a reported 30% minimum effective tax floor on top of inflation-indexed cost base adjustments, and it is the interaction between these two elements that determines who gains and who loses under the new regime. With the confirmed implementation date still 13 months away and no exposure draft legislation yet released, investors face a planning window that is already narrowing. What follows unpacks the confirmed mechanics, explains why the floor-and-indexation combination can produce higher effective tax burdens than the old system for many long-term holders, and identifies the decision points worth considering now, before draft legislation closes off options.

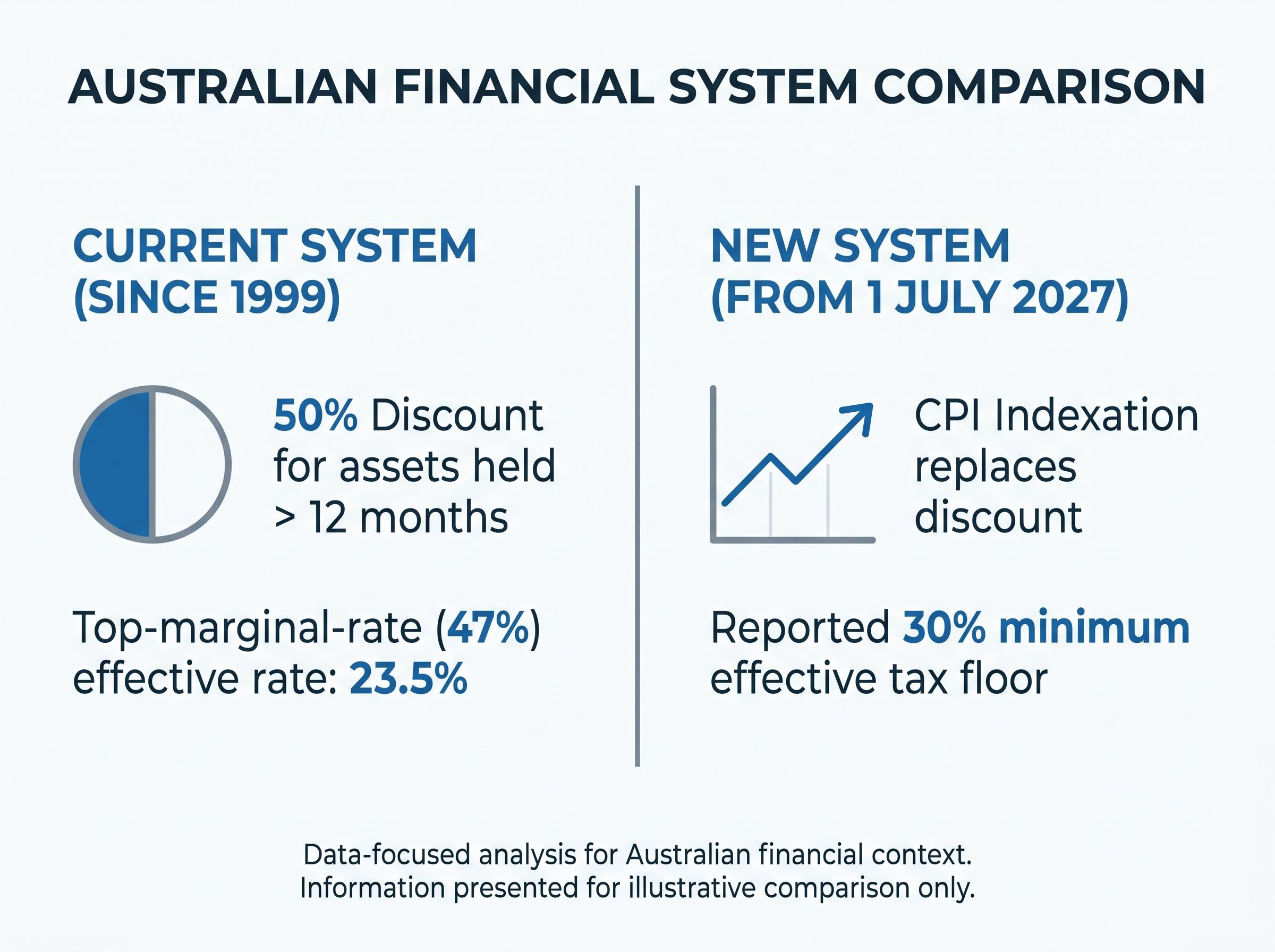

Treasurer Jim Chalmers confirmed in the 2026-27 Budget Speech that the existing 50% CGT discount for assets held more than 12 months will be replaced by CPI indexation of the cost base, effective 1 July 2027. Small business CGT concessions, including the 15-year exemption, retirement exemption, rollover concession, and active asset reduction, are preserved under the new framework.

Beyond those confirmed elements, several reported details remain unverified in primary legislation.

The budget.gov.au CGT and negative gearing factsheet provides the government’s primary published explanation of the capital gains tax changes, including the rationale for replacing the 50% discount with CPI indexation and the policy objectives framing the 2027 transition.

| Reform Element | Status |

|---|---|

| 50% CGT discount replaced by CPI indexation from 1 July 2027 | Confirmed (Budget Speech, ministers.treasury.gov.au) |

| Small business CGT concessions preserved | Confirmed (Budget papers) |

| 30% minimum effective tax floor on real gains | Reported; primary legislative source not publicly available |

| Split-period transitional treatment (pre/post 1 July 2027) | Reported; unverified in primary legislation |

| 12-month grace period under existing rules | Reported; not confirmed by ATO or Treasury |

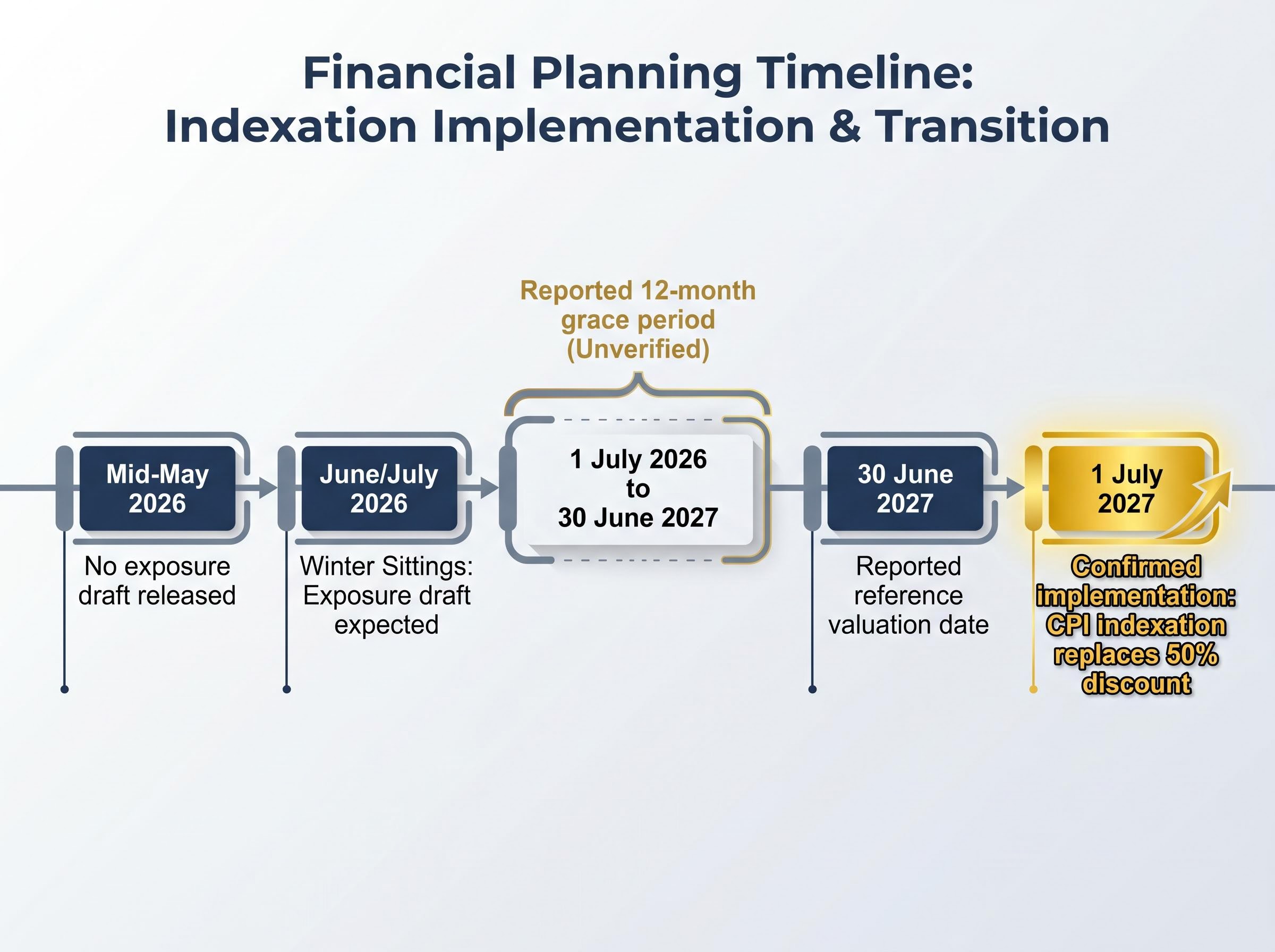

No exposure draft legislation had been released as of mid-May 2026. Parliament introduction is expected during the Winter 2026 sittings (June/July 2026). Until that draft is public, investors and advisers are working with the Budget announcement and industry commentary rather than final law. Monitoring treasury.gov.au and ato.gov.au for the exposure draft release is the most direct way to track progress.

The system in place since 1999 operated as a blunt instrument. Any investor who held an asset for more than 12 months paid tax on exactly half the nominal gain. The benefit was identical whether the asset was held for 13 months or 30 years, and whether inflation ran at 1% or 5%. The concession was fixed, predictable, and indifferent to economic conditions.

The new system replaces that fixed concession with a variable one. Under CPI indexation, the mechanics work differently:

Under the old system, the tax concession was fixed at 50% regardless of inflation. Under the new system, the concession floats with CPI: higher inflation delivers a larger cost base uplift and a smaller taxable gain; lower inflation delivers less protection.

This matters because Australia’s inflation trajectory is heading downward. The RBA’s May 2026 Statement on Monetary Policy shows headline CPI peaking at approximately 4.8% in mid-2026 and underlying inflation (trimmed mean) at approximately 3.7%. The longer-term trajectory points toward the 2-3% target band. In a low-inflation environment returning to that band, the indexation uplift is modest, and the protection it offers may be substantially less than many investors assume.

The RBA inflation trajectory matters for this reform in a direct mechanical sense: the lower CPI falls toward the 2-3% target band, the smaller the cost base uplift an investor receives each year, and the more frequently the 30% floor activates to impose a minimum tax burden that indexation alone cannot reduce.

The reported 30% minimum effective tax floor introduces a mechanism that limits how much indexation can reduce an investor’s tax burden. Even after applying CPI indexation to shrink the taxable gain, the government would impose a floor ensuring the investor pays at least 30% effective tax on the real gain.

The interaction between the floor and indexation is where the reform’s impact concentrates. In a low-inflation environment, the indexed cost base rises slowly. The real gain remains large relative to the nominal gain. And the 30% floor activates because the natural effective rate after indexation falls below that threshold. Industry commentary from the Tax Institute, SMSF Association, and FAAA has identified the floor as the component most likely to disadvantage long-term investors, with reported calls for a 25% floor cap or exemptions for assets held over 15 years.

Under the existing 50% discount, a top-marginal-rate investor paying 47% tax on half the nominal gain faces an effective rate of 23.5%. The reported 30% floor exceeds this, meaning the reform could increase effective tax burdens for high-earning, long-term holders.

The following table illustrates conceptually how the floor interacts with different inflation and holding period assumptions:

| Scenario | Inflation Rate | Holding Period | Indexation Benefit (Conceptual) | Floor Activated? |

|---|---|---|---|---|

| Low inflation, medium hold | 2% | 10 years | Modest cost base uplift; real gain remains large | Likely yes |

| Low inflation, long hold | 2% | 20 years | Greater cumulative uplift, but nominal returns compound faster | Likely yes |

| Moderate inflation, medium hold | 3.5% | 10 years | Meaningful cost base uplift narrows real gain | Less likely |

In reported commentary, the floor is suggested to activate as early as year 6 for equities with nominal returns around 7% and inflation around 2-2.5%. The primary legislative source for these thresholds remains unverified, but the conceptual dynamic is consistent across industry analysis: the cohort most affected is long-term, buy-and-hold investors in a low-inflation environment.

A higher effective tax rate in any single year is manageable. The compounding effect of that higher rate across decades is where the reform reshapes wealth outcomes.

Even a 1-2 percentage point increase in annual effective CGT drag, compounded over 20-30 years on a reinvested portfolio, reduces terminal wealth meaningfully. The lost reinvestment potential on after-tax returns accumulates quietly, year after year, widening the gap between what the old system would have delivered and what the new system produces.

Three cohorts face the greatest cumulative impact:

The scale of that exposure is concrete: modelling cited in coverage of the founder liquidity event scenario estimates a business founder selling a company for $1 million could lose more than $225,000 in after-tax proceeds under the new regime compared with the existing 50% discount, a gap that dwarfs the cost of most professional advisory engagements.

A diversified equity investor can stage realisations across financial years to manage CGT liability. A founder selling a business typically cannot. The bulk of their lifetime return crystallises in a single transaction. Small business CGT concessions remain available, but eligibility conditions (the active asset test, turnover thresholds) are not universally met. For founders who fall outside those concessions, the effective rate at the point of sale determines a significant portion of their lifetime after-tax wealth.

The 2026-27 financial year and first half of 2027 represent the last period during which the existing 50% discount rules apply to the entirety of accrued gains for qualifying assets. That window is finite and already narrowing.

A 12-month grace period (1 July 2026 to 30 June 2027) reportedly allows investors to sell under existing rules. This has not been confirmed by ATO or Treasury primary sources. Similarly, a split-period transitional treatment (pre-2027 gains taxed under old rules, post-2027 gains under the new regime, with 30 June 2027 as the reference valuation date) has been widely reported but not legislated. Reported valuation methods include ASX closing price for shares and independent valuation for property, with a safe harbour reportedly proposed for assets under $500,000.

Given these uncertainties, investors can take the following steps now:

Key transitional details including the grace period and valuation methodology remain unverified in primary legislation as of May 2026. Investors should not act on reported details without professional advice and confirmation of final law.

For investors who hold large unrealised equity positions built up over the post-2022 bull market and are now weighing the timing of realisations before 1 July 2027, our dedicated guide to tax-efficient portfolio rebalancing covers the mechanics of executing rebalances inside superannuation and SMSF structures, where the concessional 15% earnings tax provides a materially more favourable environment than disposing of assets held personally at marginal rates.

Several technical gaps remain unaddressed in verified primary sources:

The political landscape adds a further layer of uncertainty. Three positions are currently in play:

With Labor holding a majority government, outright reversal before 2027 is low probability. Modification of the floor, whether a reduction, phase-in, or exemption for long-term holders, is the more plausible outcome given the volume of industry opposition. That assessment remains speculative until draft legislation and Senate arithmetic are clearer. The exposure draft, expected during the Winter 2026 sittings, will be the first moment investors and advisers see the precise floor rate, transitional mechanics, and valuation rules. Treasury.gov.au and ato.gov.au remain the primary verification sources.

If legislated as reported, the new framework will reduce after-tax returns for many long-term investors relative to the existing system, particularly in a low-inflation environment where the 30% floor activates and indexation provides limited cost base uplift. That is the honest assessment of the reform’s direction.

It is not, however, the only variable in a long-term wealth equation. The compounding effect of remaining invested, diversified, and maintaining low portfolio turnover still dominates the compounding effect of a higher tax drag in most modelled scenarios over 20-30 year horizons. Investment structures that minimise unnecessary realisation events, such as low-turnover index ETF portfolios with buy-only rebalancing, carry increased relative value in a higher CGT environment because deferring realisation preserves the compounding base.

Three actions are available now:

Remaining invested, diversified, and disciplined over a 20-30 year horizon is likely to matter more to final wealth outcomes than the CGT rate structure. That does not make the rate structure irrelevant to planning decisions made now.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding future tax outcomes are speculative and subject to change based on final legislation and market developments.

From 1 July 2027, the existing 50% CGT discount for assets held more than 12 months will be replaced by CPI indexation of the cost base, meaning investors pay tax only on the real (inflation-adjusted) gain rather than half the nominal gain.

The reported 30% floor sets a minimum effective tax rate on real gains, meaning that even after CPI indexation reduces the taxable gain, investors cannot reduce their effective tax burden below 30%, which can exceed the 23.5% effective rate top-marginal investors paid under the old 50% discount.

As of mid-May 2026, no exposure draft legislation had been released; Parliament introduction is expected during the Winter 2026 sittings in June/July 2026, and investors should monitor treasury.gov.au and ato.gov.au for updates.

Small business CGT concessions, including the 15-year exemption, retirement exemption, rollover concession, and active asset reduction, are confirmed as preserved under the new framework announced in the 2026-27 Budget.

Investors can engage a qualified tax adviser to model scenarios using confirmed and reported reform parameters, identify assets with large unrealised gains, review business structure and small business concession eligibility, and monitor treasury.gov.au and ato.gov.au for the exposure draft release.