Who Is Actually Driving Nvidia’s AI Revenue Now

44 mins ago

Australia’s first space-focused exchange-traded fund began trading on the ASX this morning. BetaShares’ RCKT opened at $14.00 per unit, tracking the S&P Kensho Space Index, a benchmark that returned 167% in the 12 months to 30 April 2026 but has also recorded a 40% maximum drawdown over its history. The fund gives Australian retail investors and self-managed super funds their first ASX-listed route into the commercial space economy, a sector projected to grow from US$626 billion today to US$1.8 trillion by 2035. Until now, gaining meaningful exposure required purchasing individual US-listed stocks or using international brokerage platforms. This analysis breaks down what RCKT holds, what it costs, how it compares to thematic ETF peers on the ASX, and what the concentration and currency risks mean for investors deciding how to size a position.

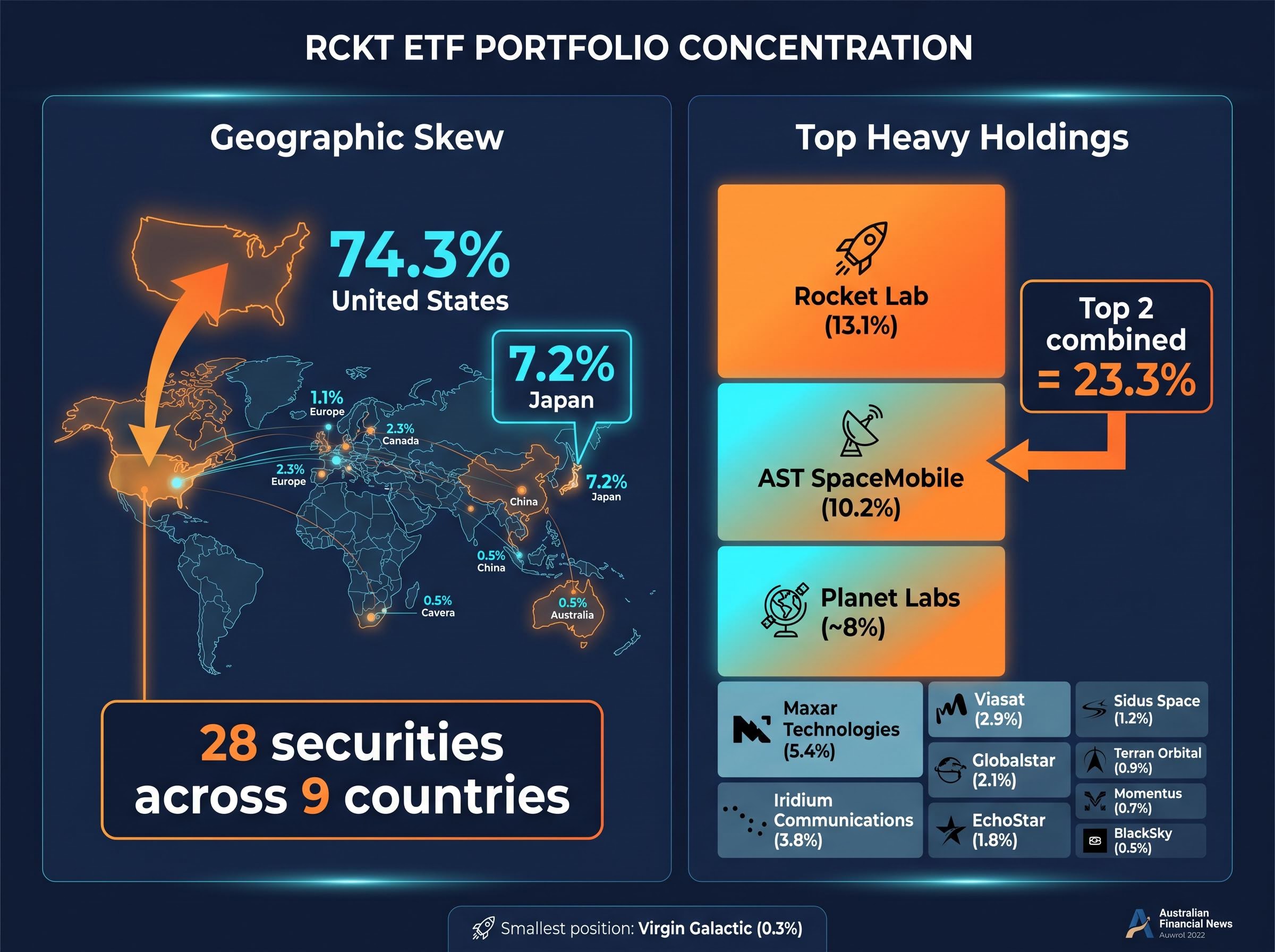

The label says “space.” The portfolio tells a more specific story. RCKT holds 28 securities across nine countries, selected by the S&P Kensho Space Index based on their revenue exposure to commercial and government space activities. The index applies a global mandate, but the geographic reality skews heavily toward a single market.

US-listed equities account for 74.3% of the fund. The remaining allocation is spread thinly across eight countries:

Non-US exposure provides limited diversification. In practice, RCKT functions as a US space sector vehicle with modest international representation.

The fund’s five largest positions reveal a portfolio spanning launch vehicles, satellite broadband, and Earth observation.

| Ticker | Company | Weighting |

|---|---|---|

| RKLB | Rocket Lab USA (launch vehicles, spacecraft manufacturing) | 13.1% |

| ASTS | AST SpaceMobile (satellite-direct-to-cellular broadband) | 10.2% |

| PL | Planet Labs (Earth observation satellites, defence analytics) | ~8% |

| VSAT | Viasat (satellite communications) | Lower weighting |

| SATS | EchoStar (satellite broadband, video services) | Lower weighting |

Rocket Lab and AST SpaceMobile together represent 23.3% of the fund, meaning nearly a quarter of RCKT’s performance rests on two companies operating in different sub-sectors: orbital launch and satellite broadband, respectively. At the other end of the spectrum, Virgin Galactic sits at 0.3%, the smallest position. The BetaShares PDS caps any single stock at 30%.

RCKT’s thematic case rests on a sector where government budgets and private capital are both accelerating.

The global space economy reached approximately US$626 billion in 2025 and is projected to grow to US$1.8 trillion by 2035, according to industry estimates.

That trajectory is not speculative. Measurable capital flows and operational milestones are already visible across 2025 and 2026:

These are not projected catalysts. They are capital already deployed and regulatory barriers already removed.

The fund’s three largest positions each reported earnings within the past quarter, offering a factual basis for the valuations embedded in today’s listing price.

Rocket Lab (RKLB, 13.1%) reported Q1 2026 revenue of US$122 million, a 45% year-on-year increase driven by 14 Electron launches (up from 9 in Q1 2025). In February 2026, NASA awarded the company a lunar lander contract worth US$250 million, and its Neutron rocket test succeeded in March 2026. RKLB closed at approximately US$105.47 on 11 May 2026, below its 52-week high of US$123.94.

AST SpaceMobile (ASTS, 10.2%) reported Q4 2025 revenue of US$18 million, representing approximately 300% year-on-year growth. The first BlueBird satellite block launched in December 2025 via SpaceX. A Vodafone partnership expansion in January 2026 for European and Asian coverage and FCC approval for US testing in April 2026 followed. ASTS was trading at approximately US$82.55 on 11 May 2026.

Planet Labs (PL, approximately 8%) delivered FY Q3 2026 revenue of US$62 million, an 18% year-on-year increase, supported by more than 300 defence contracts and the Pentagon’s US$100 million Tanager mission. PL closed at approximately US$41.84 on 11 May 2026.

| Company | Weighting | Recent Revenue Growth | Key Milestone |

|---|---|---|---|

| Rocket Lab | 13.1% | +45% YoY (Q1 2026) | US$250m NASA lunar lander contract |

| AST SpaceMobile | 10.2% | ~300% YoY (Q4 2025) | FCC approval for US testing (April 2026) |

| Planet Labs | ~8% | +18% YoY (FY Q3 2026) | US$100m Pentagon Tanager mission |

All three holdings are showing operational momentum. The question for investors is how much of that momentum is already reflected in share prices that have appreciated substantially over the past 12 months.

Orbital launch and satellite broadband stocks have been among the strongest-performing segments of the public equity market over the past 12 months, with the same companies anchoring RCKT’s portfolio delivering individual returns well above the index’s 167% aggregate figure, a gap that reflects the outsized contribution of two or three names rather than broad-based sector appreciation.

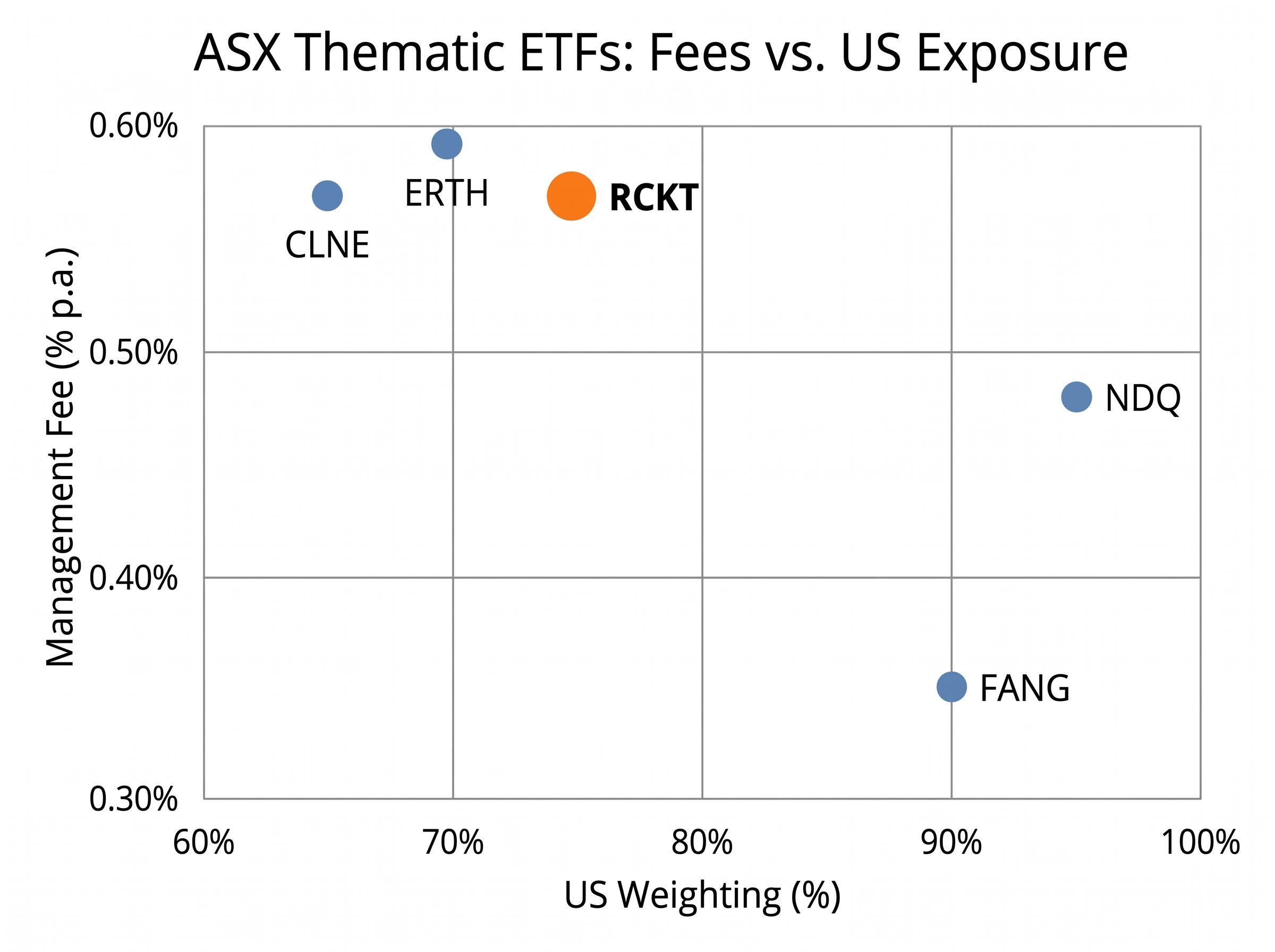

RCKT’s management fee of 0.57% per annum sits in the middle of the ASX thematic ETF range, according to Morningstar Australia, which described it as “mid-pack for thematics” in an April 2026 assessment. The fee is meaningfully higher than broad-market products like VAS at 0.10%, but comparable to VanEck’s CLNE at 0.57% and lower than BetaShares’ ERTH at 0.59%.

| Ticker | Theme | Fee (% p.a.) | AUM | US Weighting |

|---|---|---|---|---|

| RCKT | Space | 0.57% | ~A$40m (Day 1) | 74.3% |

| ERTH | Sustainability | 0.59% | ~A$86m | ~70% |

| NDQ | Nasdaq 100 | 0.48% | A$8.57b | ~95% |

| FANG | Tech/Disruptive | 0.35% | Not verified | ~90% |

| CLNE | Clean Energy | 0.57% | Not verified | ~65% |

The benchmark’s historical performance demands context.

The S&P Kensho Space Index returned 167.25% in the 12 months to 30 April 2026 and 20.46% annualised over five years. It has also recorded a 40% maximum drawdown. Both figures belong in the same evaluation.

VanEck’s Dino Cantinas, writing in the Australian Financial Review on 7 May 2026, noted “thematic fatigue post-2024 AI boom” but argued that the space sector’s total addressable market warrants paying the premium. According to FNArena data as of 9 May 2026, 7 of 12 brokers gave a buy rating, representing a 65% buy consensus. RCKT has no live fund performance track record; all return data references the underlying index.

ASIC Regulatory Guide 282 for exchange-traded products sets out the disclosure, compliance, and market integrity obligations that govern ASX-listed ETFs in Australia, including the product disclosure statement requirements that investors should review before transacting in funds like RCKT.

The shift from opportunity to risk begins with structure. Four categories of risk warrant attention:

UBS Australia (10 May 2026) recommended a position of less than 5% of portfolio for RCKT, citing the ARKX drawdown parallel and the fund’s unhedged US concentration.

Thematic ETF drawdowns of 25% or more occurred across technology-themed ASX products in 2026 even as the broader market captured gains from the resources and energy rotation, a pattern that reinforces why UBS Australia recommended capping RCKT exposure below 5% rather than treating the fund’s 167% index return as a forward performance guide.

Morningstar Australia assigned RCKT a Silver rating but attached a “high risk” designation for conservative portfolios, estimating annualised volatility at 28% (as of 11 May 2026). According to FNArena’s analysis on 9 May 2026, 7 of 12 brokers cited top-heavy concentration as a primary risk, expressing a preference for diversified global equity exposure over single-theme vehicles.

A Financial Standard survey of 150 advisers (published 10 May 2026) found that 62% classified thematic ETFs as high-risk satellite positions, recommending 5-10% portfolio allocations for retail investors within a core-satellite framework.

BetaShares reported A$25 million in pre-launch subscriptions, with AUM reaching approximately A$35 million at listing and an estimated A$40 million by midday. The demand was real. The question is whether it matches the fund’s risk profile for each investor.

UBS Australia noted “enthusiasm from growth-oriented SMSFs,” but the fund’s unhedged currency structure carries particular implications for retirees drawing income in Australian dollars. Financial Standard’s adviser survey indicated a preference for positioning RCKT-style funds as growth exposure for younger investors within a core-satellite construction.

Core-satellite portfolio construction, the framework most commonly cited by advisers evaluating RCKT, typically anchors 75% or more of a portfolio in broad index ETFs before allocating a constrained satellite slice to high-conviction thematic positions, which limits the damage from a single-theme drawdown without eliminating the upside exposure.

Several information gaps remain on day one:

These gaps do not disqualify the fund. They do give investors a legitimate reason to monitor the first few months before committing capital.

Investors exploring whether to complement an RCKT position with direct holdings in individual companies will find our deep-dive into public space equities covers Rocket Lab, AST SpaceMobile, and Intuitive Machines with company-level contract data, analyst price targets, and the specific downside scenarios flagged for 2026, allowing a more granular assessment of the same names embedded in RCKT’s top holdings.

The 167% 12-month index return is real. So is the 40% maximum drawdown. Both figures describe the same benchmark, and both belong in any investor’s assessment of RCKT.

The pre-launch subscription interest of A$25 million and steady debut trading suggest the market has already formed a view: RCKT is a high-conviction satellite position, not a core holding. The analyst consensus supports that framing, with UBS recommending less than 5% of portfolio and Financial Standard’s adviser survey pointing to 5-10% as the appropriate thematic allocation range.

The information gaps at launch, particularly around tax treatment and broker platform access, mean investors have a reasonable basis for monitoring the fund’s early months before transacting. Investors considering RCKT should review the BetaShares PDS in full, confirm platform availability with their broker, and consider how the fund’s 74.3% US weighting interacts with any existing USD or US technology exposure already in their portfolio.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

BetaShares RCKT is Australia's first space-focused exchange-traded fund, listed on the ASX and tracking the S&P Kensho Space Index, which provides exposure to 28 companies across nine countries involved in commercial and government space activities.

RCKT holds 28 securities spanning launch vehicles, satellite broadband, and Earth observation, with its two largest positions being Rocket Lab USA (13.1%) and AST SpaceMobile (10.2%), together representing 23.3% of the fund.

Key risks include unhedged currency exposure to the US dollar (74.3% of holdings are US-denominated), high single-stock concentration with Morningstar citing a significantly elevated Herfindahl index, a 40% historical maximum drawdown on the underlying index, and geopolitical risk tied to US trade policy.

RCKT charges a management fee of 0.57% per annum, which Morningstar Australia described as mid-pack for thematic ETFs, comparable to VanEck's CLNE at 0.57% and slightly lower than BetaShares' own ERTH at 0.59%.

UBS Australia recommended capping RCKT at less than 5% of a portfolio, citing the fund's unhedged US concentration and a parallel to ARKX's approximately 60% drawdown in 2021, while a Financial Standard adviser survey pointed to 5-10% as the appropriate range for thematic satellite positions.