SK Hynix’s $26.5B Nasdaq Listing Shatters ADR Demand Records

9 hrs ago

Metcash shares surged 5.84% on 11 May 2026, closing at A$2.90, after the wholesale distributor lodged an FY26 trading update projecting underlying net profit after tax (NPAT) of A$268-270 million across its food, liquor, and hardware divisions. The single-day gain pushed the stock to an intraday high of A$3.03, but the rally still leaves Metcash roughly 26% below where it traded six months ago. That gap between a strong day and a weak half-year frames the question investors need to answer: does this update mark a turning point, or simply a less-bad result in a stock that has been repriced lower for reasons the guidance alone does not resolve? What follows unpacks the segment-level detail, the forward-looking cost programme, and the sector backdrop that together determine where the Metcash share price goes from here.

The headline figure is concrete. Metcash guided to FY26 underlying NPAT of A$268-270 million, clearing prior market consensus and giving investors a firm anchor ahead of the formal full-year result.

FY26 NPAT Guidance: A$268-270 million

The share price responded accordingly. MTS closed at A$2.90, up A$0.16 (5.84%), after touching an intraday high of A$3.03 and a low of A$2.86. The ASX announcement was lodged at 4:02 PM AEST, with an investor webcast following at 5:30 PM AEST, meaning the bulk of the price reaction occurred in late-session and after-hours trading.

Yet the context reshapes the relief. A 26% decline over the preceding six months means the stock had already been marked down substantially before this update landed. The day’s move narrowed the gap; it did not close it.

The guidance beat confirms that earnings held up better than the share price had been suggesting. Whether that repricing was overdone is the question the segment detail begins to answer.

FY26 guidance revisions have not been uniformly positive across the consumer staples peer group: McPherson’s moved in the opposite direction in April 2026, abandoning its growth target as operating model disruption and supplier surcharges compressed earnings, a contrast that makes Metcash’s guidance beat more meaningful in context.

The NPAT headline smooths over three distinct stories. Breaking the result into its components reveals where the earnings stability sits, and where the uncertainty remains.

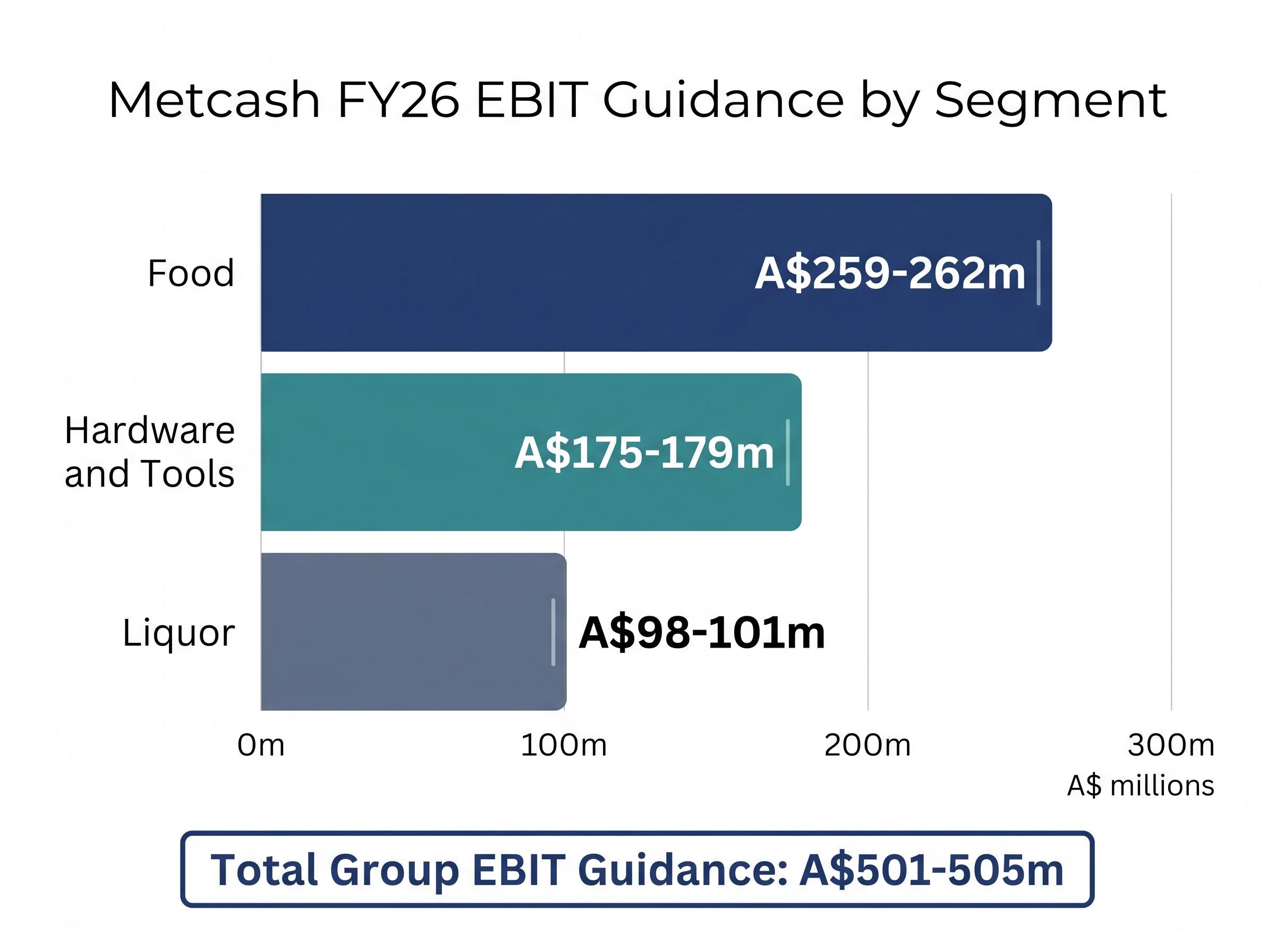

| Segment | FY26 EBIT Guidance (A$m) | Key Operating Conditions |

|---|---|---|

| Food | $259-262m | Stable YoY; IGA network resilient; competitive promotional activity |

| Liquor | $98-101m | H2 margin recovery; independent retailers gained market share |

| Hardware and Tools | $175-179m | H1 sales +2.4%; trade market conditions soft; recovery timeline extended |

The Food division’s EBIT guidance of A$259-262 million reflects stable year-on-year performance. The IGA supermarket network held its ground in a competitive environment where promotional intensity among major chains has been elevated. The foodservice and convenience channel delivered strong volume growth from an expanding customer base, adding a distinct growth avenue within the food pillar.

Coles supermarkets EBIT growth of 14.6% in 1H FY26, driven by automation benefits and strategic sourcing rather than volume uplift, illustrates the margin expansion available to larger integrated chains, a dynamic that directly shapes the promotional intensity IGA independents face when competing for the same household grocery spend.

Liquor guided to EBIT of A$98-101 million, supported by a margin recovery in the second half of FY26. Independent liquor retailers continued to gain market share, and the on-premise trade recovered during H2, contributing to the improved result.

Hardware and Tools guided to EBIT of A$175-179 million. First-half hardware sales grew 2.4%, and momentum improved in H2 through pricing and product ranging initiatives across Mitre 10, Total Tools, and Home Hardware.

The qualification matters. Trade market conditions remained soft, and the recovery timeline extended beyond earlier expectations. This is the segment where the gap between improving indicators and confirmed earnings delivery is widest, and it is the variable that will shape how investors read the full-year result when it arrives.

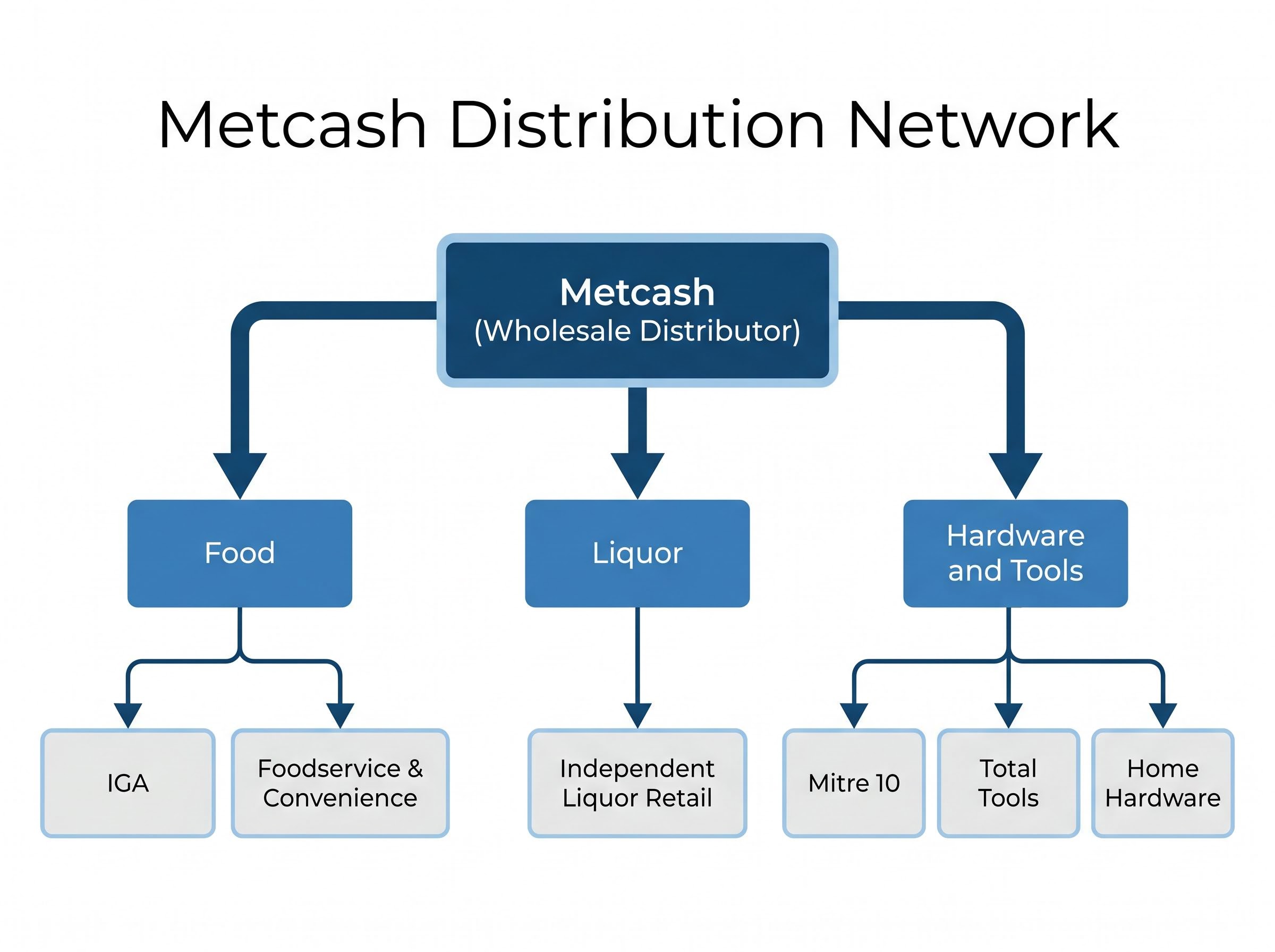

Metcash is a wholesale distributor, not a retailer. The company supplies independent operators rather than owning the stores that carry its brands. This structural distinction shapes how its earnings respond to competitive and consumer dynamics.

The network spans three segments:

Because Metcash sits between producers and independent retailers, its earnings are tied to the health and competitiveness of those independents, not to direct consumer transactions. When IGA stores compete effectively against Woolworths and Coles, Metcash’s food volumes hold. When independent hardware operators lose share to Bunnings, Metcash’s hardware earnings compress.

This model also means that cost efficiencies within Metcash’s own distribution operations, rather than store-level performance, represent one of the levers management can pull directly. CEO Doug Jones has positioned the company’s wholesale infrastructure as the platform from which independent retailers can compete, a framing that makes the FY27 cost programme (discussed below) particularly relevant.

The FY26 trading update included a forward-looking element that sits apart from the segment results: a targeted annualised cost savings programme of at least approximately A$25 million from FY27 onward.

Targeted annualised cost savings from FY27: at least approximately A$25 million

The composition is specific:

This is not a vague efficiency aspiration. The breakdown into two quantified categories, with a defined FY27 realisation timeline, gives investors a tangible earnings catalyst that operates independently of top-line volume recovery.

The distinction matters because the hardware segment’s extended recovery timeline means revenue-driven earnings growth in that division remains uncertain. A cost programme that delivers margin improvement regardless of whether trade conditions improve on schedule introduces a structural floor under forward earnings. Metcash also noted strong cash generation and disciplined working capital management during FY26, suggesting the balance sheet supports execution of the programme without incremental funding pressure.

These statements regarding cost savings are forward-looking and subject to change based on market developments and company performance.

The hardware segment’s soft trade conditions did not occur in isolation. The broader Australian housing construction cycle provides context for whether the extended recovery timeline reflects a company-specific issue or a sector-wide delay.

| Indicator | Figure | Relevance to Metcash |

|---|---|---|

| Housing starts (12 months to Sep 2025) | +11.2% | Improving upstream demand for trade hardware |

| Housing starts (Dec 2025 quarter) | +8% | Continued momentum in residential construction |

| Bunnings FY25 comparable sales growth | +3.5% | Broader hardware market not in structural decline |

| S&P/ASX 200 Consumer Staples (1-year) | -7.83% | Sector-wide underperformance contextualises MTS decline |

| S&P/ASX 200 Consumer Staples (YTD) | +1.14% | Modest sector stabilisation in 2026 |

Housing starts grew 11.2% in the 12 months to September 2025 and 8% in the December 2025 quarter, according to HIA and ABS data. Bunnings (owned by Wesfarmers) reported FY25 comparable sales growth of 3.5% and revenue growth of 3.3%, confirming that the broader hardware retail category was expanding rather than contracting.

The competitive dynamics in independent hardware distribution are shifting: Stealth Group’s HBT acquisition positioned it as a scaled alternative to both Wesfarmers and Metcash in a market valued at approximately $93 billion, adding a third participant to a segment where Metcash’s Mitre 10 and Total Tools networks have historically competed primarily against Bunnings.

The ABS Building Activity data for the December 2025 quarter confirmed total dwelling commencements rose 8.0%, while the September 2025 annual figure showed an 11.2% increase, providing independent verification that upstream construction demand supporting trade hardware volumes was genuine rather than estimated.

This positions Metcash’s hardware softness as a trade market timing issue. The demand is building upstream; the question is when it flows through to the independent trade operators that Metcash supplies. The consumer staples sector’s 7.83% decline over the past year provides additional context: Metcash’s NPAT guidance beat occurred against a weak sector backdrop, making the result more notable than the headline figure alone might suggest.

The consensus analyst 12-month price target for MTS sits at approximately A$3.43-A$3.68, according to aggregated broker coverage. Against the 11 May closing price of A$2.90, that implies 18-27% upside, a gap that the market has acknowledged but not yet awarded.

Even after the 5.84% gain, the stock remains approximately 26% below its level six months prior. The guidance beat has narrowed the distance between the current price and prior expectations. It has not closed it.

ASX market breadth deteriorated sharply in the week ending 1 May 2026, with 22 index constituents hitting 52-week lows against a headline index fall of just 0.65%, a divergence that reflects concentrated stress in consumer-facing sectors including the consumer staples names that make up Metcash’s peer group.

The combination of a confirmed NPAT beat, a quantified cost savings programme, and improving macro conditions for the housing construction cycle creates a scenario where earnings growth is possible. Investors weighing this against the current valuation should hold three open variables in mind:

The low price-to-earnings context reflects a market that is pricing in the risk of these variables resolving unfavourably, while the analyst target range reflects a view that they resolve in Metcash’s favour.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

The FY26 trading update confirmed what the headline NPAT figure suggested: the core food and liquor divisions are stable, the cost base is being actively restructured with a quantified A$25 million FY27 savings target, and cash generation remains strong.

The primary unresolved variable is hardware. Trade market conditions remained soft through FY26 despite improving housing construction data, and the recovery timeline has already extended beyond earlier expectations. Whether that timeline compresses from here, and whether the cost programme delivers at the indicated scale, will determine whether the 11 May share price reaction marks a turning point or a temporary reprieve.

The formal FY26 full-year results represent the next material disclosure point. The guidance has set the baseline. The execution is what comes next.

Metcash is an Australian wholesale distributor that supplies independent retailers across three segments: food (IGA supermarkets), liquor (independent outlets), and hardware (Mitre 10, Total Tools, and Home Hardware). Its earnings are tied to the health and competitiveness of those independent retailers rather than direct consumer sales.

Metcash guided to FY26 underlying NPAT of A$268-270 million and group EBIT of A$501-505 million, clearing prior market consensus. Group revenue grew 0.7% overall and 3.8% excluding tobacco, with food and liquor divisions stable and hardware showing improvement but facing an extended recovery timeline.

Metcash announced a targeted annualised cost savings programme of at least approximately A$25 million from FY27 onward, comprising around A$15 million in labour cost reductions and approximately A$10 million in non-trade procurement savings, with further initiatives noted as in progress.

Despite the 5.84% single-day gain on 11 May 2026, Metcash shares remained approximately 26% below their level six months prior, reflecting soft hardware trade market conditions, an extended recovery timeline in that segment, and broader consumer staples sector underperformance of 7.83% over the past year.

Aggregated broker coverage places the consensus 12-month analyst price target for MTS at approximately A$3.43-A$3.68, implying 18-27% upside from the 11 May 2026 closing price of A$2.90.