CSL Shares at a 9.5-Year Low: Is the Selloff Justified?

24 mins ago

CSL Limited (ASX: CSL) has disclosed approximately $5 billion in pre-tax impairment charges expected across FY26 and FY27, while simultaneously cutting its full-year revenue forecast to approximately $15.2 billion. The announcement, made on 11 May 2026, represents a material escalation beyond the US$1.1 billion in non-restructuring impairments disclosed at the February half-year result. CSL shares were already trading at approximately $119.88, approximately 50% below prior highs, before today’s update landed. What follows is a breakdown of the impairment charges, the specific revenue shortfalls driving the guidance downgrade, what the numbers mean for FY26 profitability, and how the second half of the year is expected to shape up.

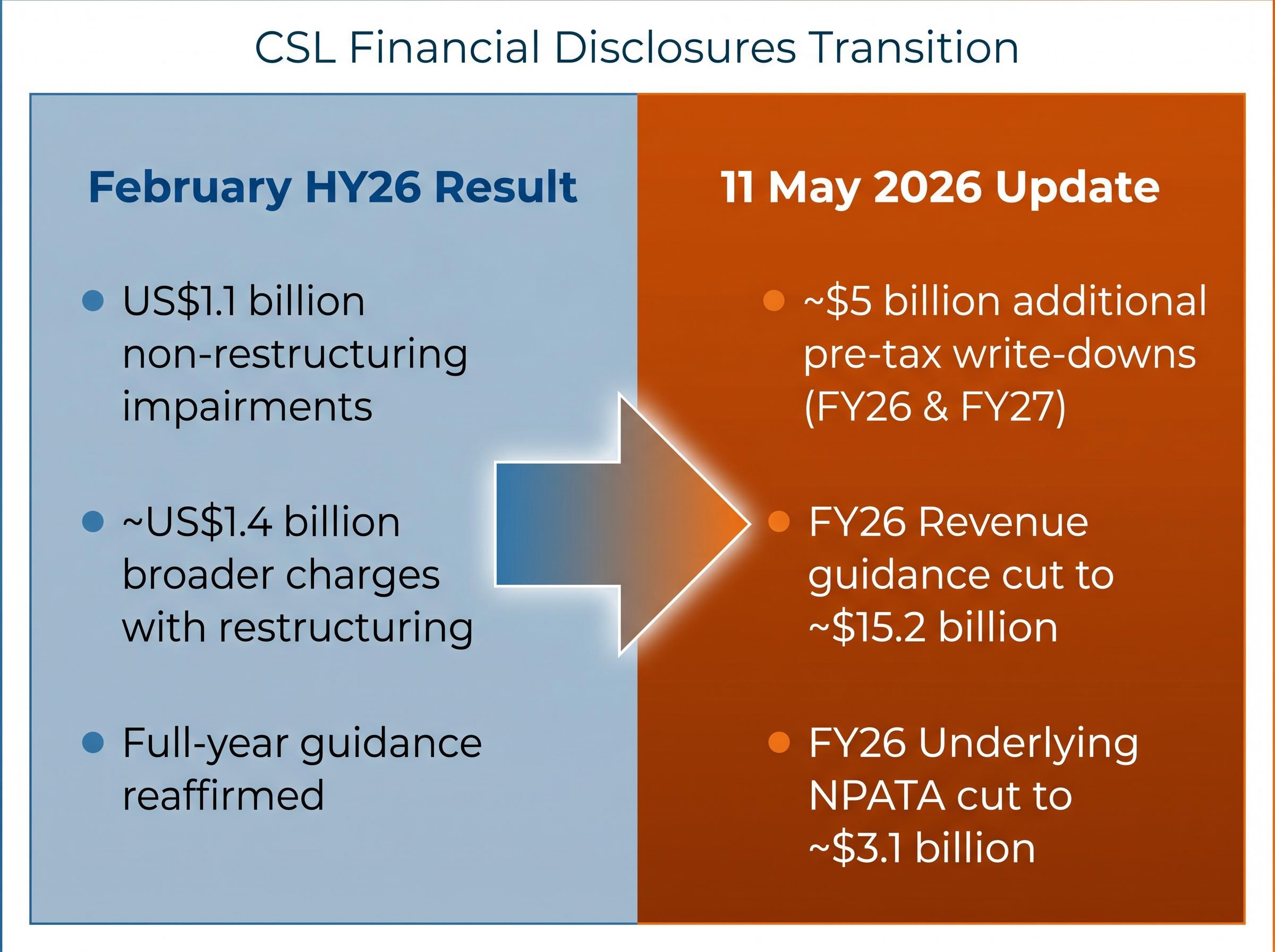

The scale of today’s announcement sits on top of what was already a difficult half-year result. In February, CSL disclosed US$1.1 billion in non-restructuring impairments across its Vifor and Seqirus divisions, with broader charges including restructuring reaching approximately US$1.4 billion. Full-year guidance was reaffirmed at that point.

Three months later, the picture has worsened considerably. CSL now anticipates approximately $5 billion in additional pre-tax write-downs spanning FY26 and FY27.

CSL anticipates approximately $5 billion in pre-tax write-downs across FY26 and FY27, beyond what was disclosed at the February half-year result.

The impairments fall across two asset categories:

The announced figures remain subject to further analysis, business developments, independent auditing, and board sign-off. Final numbers could shift in either direction.

The ASX continuous disclosure obligations set out in Listing Rule 3.1 require listed entities to immediately disclose information that a reasonable person would expect to have a material effect on the price or value of the entity’s securities, which is the framework governing why CSL’s impairment estimates and guidance revision required prompt market announcement despite the figures remaining subject to further audit and board sign-off.

The revised FY26 guidance tells a clear story when placed alongside what CSL was projecting just three months ago.

| Metric | Prior Guidance Status | Updated FY26 Guidance |

|---|---|---|

| Total Revenue | Reaffirmed at February HY26 result | ~$15.2 billion (constant currency) |

| Underlying NPATA | Reaffirmed at February HY26 result | ~$3.1 billion (constant currency, excl. restructuring and impairments) |

The gap between reaffirmed guidance in February and today’s downgrade is the detail that carries the weight. CSL told the market three months ago that its full-year targets remained intact. Those targets have now been cut.

Both figures are presented on a constant currency basis, stripping out foreign exchange movements. The underlying NPATA figure also excludes restructuring costs and impairment charges. This means the $3.1 billion earnings figure does not reflect the $5 billion in write-downs; it represents CSL’s view of its operational earnings power. Investors comparing this to broker consensus estimates should note that most analyst models use a similar clean-earnings basis.

The guidance downgrade is not the result of a single problem. Four distinct headwinds, totalling approximately $650 million in revenue impact, drove the miss.

| Segment or Issue | Estimated Revenue Impact | Nature of Headwind |

|---|---|---|

| US immunoglobulin channel inventory normalisation | ~$300 million | Cyclical (channel/distribution) |

| Chinese albumin market price deterioration | ~$200 million | Structural (market pricing) |

| Middle East conflict exposure | ~$150 million (combined) | Mixed |

| Revised HEMGENIX growth projections | Structural (product adoption) | |

| Heightened iron therapy competition | Structural (competitive) |

The US immunoglobulin shortfall is the largest single item at approximately $300 million. Underlying patient demand continues to grow at mid-to-high single-digit rates. The issue is channel inventory normalisation, where distributors are drawing down existing stock rather than placing new orders. This is a timing and distribution problem, not a demand collapse.

The Chinese albumin shortfall of approximately $200 million tells a different story. CSL’s market share in China actually grew, and volumes stabilised. Falling market prices drove the miss, a dynamic that is harder to reverse through operational execution alone.

The remaining $150 million combines geopolitical exposure in the Middle East, slower-than-expected uptake of HEMGENIX (CSL’s gene therapy for haemophilia B), and increased competition in iron therapy products. Each carries a different risk profile, but together they compound the pressure on CSL Vifor and CSL Behring.

CSL completed the acquisition of Vifor Pharma in 2022 for approximately US$11.7 billion. The deal was designed to add a third growth engine alongside CSL Behring (plasma therapies) and CSL Seqirus (vaccines), giving the company exposure to iron deficiency and nephrology markets. Products acquired included Ferinject, a leading intravenous iron therapy, and Veltassa, a treatment for hyperkalaemia (elevated potassium levels in the blood).

At that price, CSL was paying for growth that had not yet been delivered. A significant portion of the purchase price was recorded as intangible assets, representing the expected future value of Vifor’s product portfolio.

When expected future value fails to materialise, the accounting consequence is an impairment. The factors contributing to the Vifor intangibles write-down include:

The physical assets being impaired, including property, plant and equipment, reflect underutilisation as revenue expectations have been scaled back.

The forward picture contains a partial offset, though it is modest relative to the scale of the shortfall.

CSL Behring is expected to deliver revenue growth in the second half of FY26, supported by underlying patient demand trends and benefits from ongoing operational and transformation programmes. The immunoglobulin channel normalisation is, by its nature, a temporary dynamic, and the recovery in ordering patterns would support a stronger second half.

CSL Behring’s second-half recovery thesis rests partly on a US plasma therapy tariff exemption secured under the Section 232 pharmaceutical proclamation, which protects the company’s highest-value US revenue stream from import duties effective September 2026 and removes a risk that had been weighing on forward earnings models.

CSL Seqirus is forecast to perform somewhat better than previously anticipated, providing an additional, if limited, positive offset.

The financial developments arrive during a period of leadership change:

The simultaneous departure of the CCO alongside an ongoing CEO search adds a layer of management continuity risk during a period when operational execution is under heightened scrutiny.

The Gordon Naylor interim CEO appointment in February 2026 was framed by the board as a continuity play, with Naylor’s 33 years at CSL and prior turnaround experience at Seqirus cited as directly relevant credentials for the transformation period ahead.

The announcement arrives with CSL shares already under sustained pressure.

The 11 February 2026 half-year result triggered an approximately 14% single-day fall, from roughly $181.90 to $156.01. The stock has continued to decline since.

12 of 18 analysts rated CSL buy or strong buy heading into today’s announcement, with a consensus price target of approximately A$195.41, more than 60% above where the stock was already trading.

As of 4 May 2026, the highest broker price target sat at A$267.60. That consensus picture was formed before today’s impairment disclosure and guidance cut, and will almost certainly be revised in the coming sessions.

The pattern is difficult to overlook. In February, CSL reported US$1.1 billion in non-restructuring impairments, a 14% single-day share price fall, and reaffirmed its full-year guidance. Three months later, that guidance has been cut, and a further $5 billion in write-downs has been flagged.

The financial question is whether the revenue headwinds are cyclical (US immunoglobulin channel normalisation) or structural (Chinese albumin pricing, iron therapy competition). The harder question is whether CSL’s management can credibly guide the market forward, particularly with a CEO search still underway and a new CCO appointment in CSL Behring.

CSL Seqirus performing somewhat better than prior expectations is the single positive offset in today’s update. It is a narrow foundation on which to build a recovery narrative.

Investors will now wait for board sign-off on final impairment figures, updated broker price targets, and H2 FY26 divisional results to determine whether today’s guidance floor holds.

Investors wanting to understand the financial recovery thesis in full will find our full explainer on CSL’s $500 million savings programme, which covers the transformation targets, the FY28 timeline for annualised savings delivery, and how management has characterised the revenue headwinds as distinct from underlying demand deterioration.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

An impairment charge is an accounting write-down recorded when the carrying value of an asset exceeds its recoverable future value. CSL disclosed approximately $5 billion in pre-tax impairment charges across FY26 and FY27 primarily because the expected future value of CSL Vifor's acquired intangible assets, including products like Ferinject and Veltassa, has not materialised due to heightened competition, pricing pressure, and slower product adoption.

CSL revised its FY26 revenue guidance to approximately $15.2 billion (constant currency) due to four headwinds totalling around $650 million: US immunoglobulin channel inventory normalisation (approximately $300 million), Chinese albumin market price deterioration (approximately $200 million), and a combined $150 million from Middle East conflict exposure, revised HEMGENIX growth projections, and increased iron therapy competition.

CSL's updated underlying NPATA guidance of approximately $3.1 billion is presented on a constant currency basis and excludes both restructuring costs and impairment charges, meaning it represents the company's view of its core operational earnings power and does not reflect the $5 billion in write-downs announced on 11 May 2026.

US immunoglobulin channel normalisation refers to distributors drawing down existing inventory rather than placing new orders with CSL, creating a temporary revenue shortfall of approximately $300 million. Underlying patient demand continues to grow at mid-to-high single-digit rates, meaning this is a timing and distribution issue rather than a collapse in end-market demand.

CSL is currently operating under interim CEO Gordon Naylor, appointed in February 2026, who brings 33 years of experience at CSL including a prior turnaround at Seqirus. Outgoing CEO Paul Naylor will remain on the board as a non-executive director, while Diego Sacristan has been appointed as the new Chief Commercial Officer of CSL Behring following Andy Schmeltz's departure for personal reasons.