Aristocrat Leisure has lost roughly 36% of its value from its August 2025 peak of AUD 73.29, yet the same company posted AUD 6.3 billion in full-year FY2025 revenue, up 11% year on year, and normalised profit after tax attributable (NPATA) of AUD 1.6 billion, up 12%. The gap between operating performance and share price trajectory is the tension at the centre of every investment conversation about this stock right now.

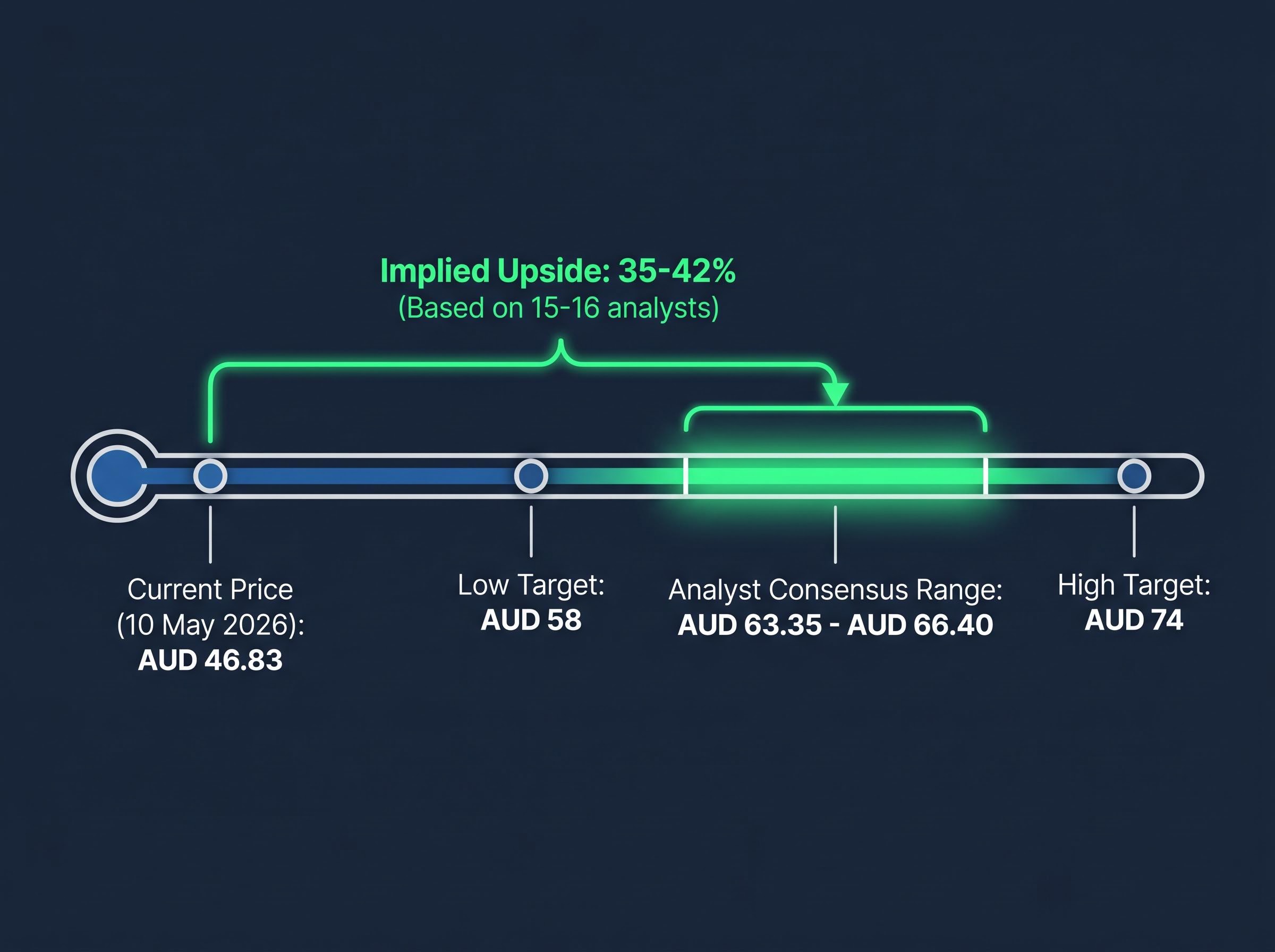

As of 10 May 2026, ALL trades at AUD 46.83, well below an analyst consensus target range of AUD 63.35 to AUD 66.40 drawn from 15 to 16 brokers. For growth investors, that discount raises an immediate question: is the market’s re-rating rational, or has sentiment overshot the fundamentals?

What follows walks through the specific financial metrics that matter for evaluating a growth-oriented company like Aristocrat, examines the strategic transformation underway, and assesses whether the current price represents a genuine entry opportunity or a discount that still carries material downside risk.

What the price chart is actually telling investors

The scale of the decline demands attention. From its 52-week high of AUD 73.29 in August 2025 to a 52-week low of AUD 44.18 in March 2026, Aristocrat shed nearly a third of its market capitalisation in seven months.

AUD 73.29 to AUD 46.83: a decline of approximately 36% from peak to the current price.

That fall did not arrive in a single event. It compounded through a sequence of pressures, each reinforcing the last:

- 14 May 2025: H1 FY2025 results revealed revenue of AUD 3.03 billion, missing the AUD 3.3 billion consensus. The stock fell 12.7% in a single session, from a prior close of AUD 68.13 to AUD 59.49 in morning trade.

- Post-results weeks: Multiple brokers cut price targets. Morgan Stanley removed ALL from its top sector picks.

- Mid-to-late 2025: Strategic divestment announcements (Plarium, Big Fish restructuring) introduced uncertainty about the revenue mix going forward.

Context matters here. In the 12 months prior to May 2025, ALL had gained approximately 55.41%, significantly outperforming the ASX 200’s 7.15% return over the same period. The stock was priced for perfection; the earnings miss punctured that pricing, and everything that followed widened the wound.

Understanding whether this decline reflects genuine fundamental deterioration or a sentiment overshoot is the first analytical step before evaluating any potential entry.

Multiple compression risk is a structural feature of growth stocks priced for perfection: when the market re-rates the earnings multiple downward, the share price can fall sharply even if reported earnings are rising, which is precisely the pattern visible in Aristocrat’s trajectory from its August 2025 peak.

When big ASX news breaks, our subscribers know first

From poker machines to platforms: how Aristocrat’s business has changed

Aristocrat was established in 1953 as a manufacturer and distributor of physical gaming machines, operating through direct sale and revenue-sharing arrangements with casinos and gaming venues. For decades, the investment case was straightforward: a dominant supplier to a regulated, high-margin industry with predictable replacement cycles.

The company that traded at AUD 73 last August looked materially different. Digital gaming had expanded to account for close to half of total revenue at peak exposure, with Plarium Global (casual and mid-core mobile titles) and Big Fish Games sitting alongside the legacy land-based operations.

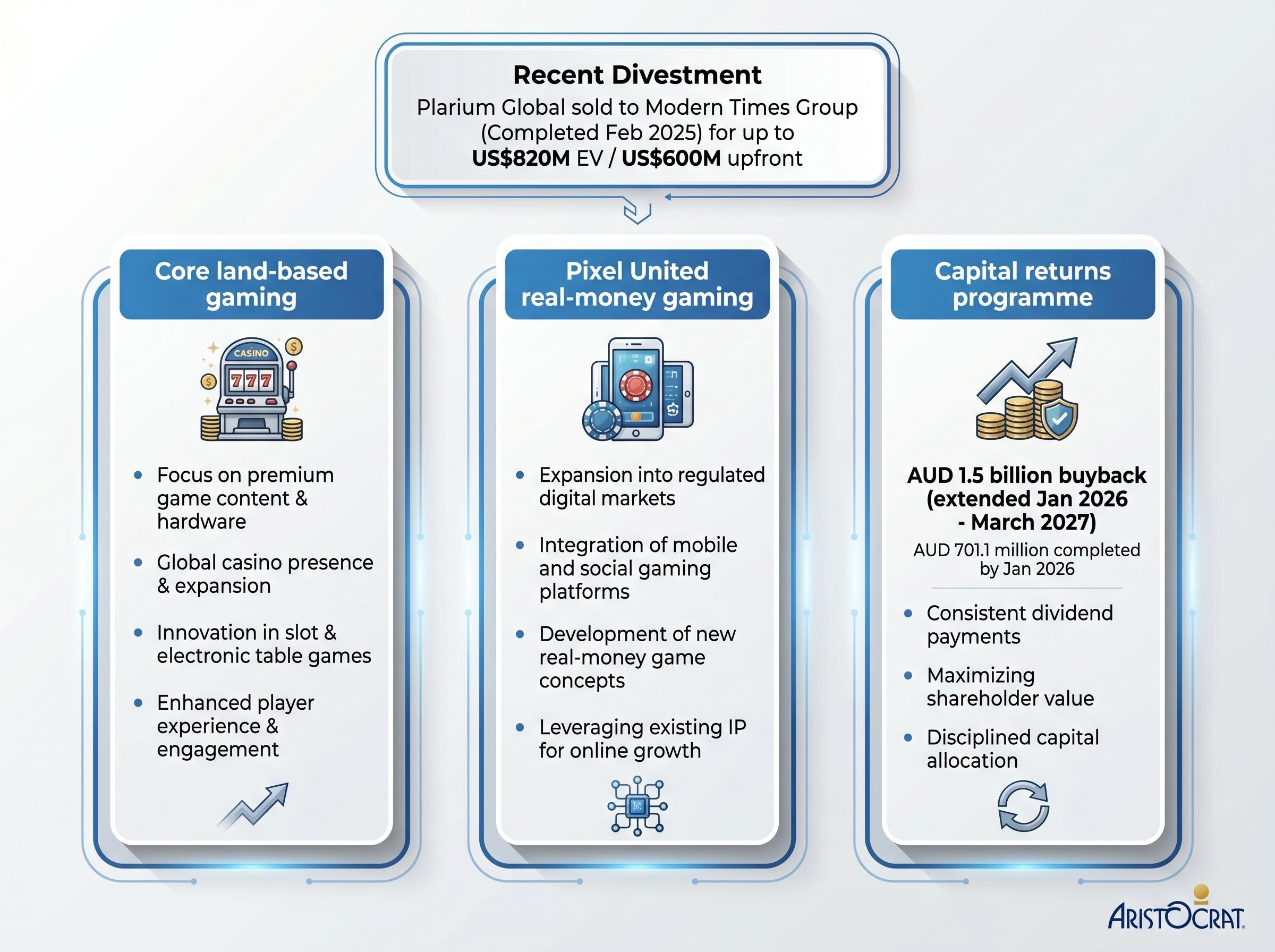

That digital portfolio is now being deliberately dismantled.

Aristocrat sold Plarium Global to Modern Times Group for up to US$820 million in enterprise value (US$600 million upfront), with the transaction completing in February 2025. Big Fish Games was restructured to focus solely on profitable “evergreen” titles, with all new game development halted.

The post-divestment revenue mix

What remains is a narrower, more focused portfolio. The post-divestment business rests on three pillars:

ASX gaming sector dynamics in the current cycle illustrate a consistent pattern: recurring revenue streams provide earnings stability while hardware and equipment sales remain volatile, a dynamic visible in Ainsworth Game Technology’s CY2025 results where recurring revenue of AUD 97.7 million (34% of group revenue) cushioned a 9% decline in underlying profit.

- Core land-based gaming: Machine manufacture, distribution, and revenue-sharing arrangements with casino operators globally.

- Pixel United real-money gaming: The retained digital operations focused on real-money gaming, distinct from the exited casual and mid-core segments.

- Capital returns programme: An AUD 1.5 billion buyback (extended January 2026 through March 2027), with AUD 701.1 million completed by January 2026, signalling management’s preference for returning divestment proceeds to shareholders.

The revenue quality has shifted. Core land-based gaming is more stable and predictable, but potentially slower-growth than the higher-volatility digital assets that were removed. Investors who valued Aristocrat primarily on digital growth runway need to reassess what the company is now, not what it was in 2022.

How to read Aristocrat’s financials as a growth investor

Growth investors evaluate companies differently from income-focused or value-focused investors. Where a mature blue-chip assessment might prioritise dividend yield, debt coverage, and payout ratio stability, growth company analysis centres on three metrics: the rate of revenue expansion, the trajectory of profit growth, and the return on equity (ROE), which measures how effectively a company generates profit from the capital shareholders have left in the business.

Growth investors applying fundamental analysis metrics such as ROE, revenue CAGR, and EBITDA margin to Aristocrat need to interpret each figure in relation to the others: a 20% ROE is a strong signal in isolation, but its meaning shifts considerably depending on how much debt was used to generate it.

Aristocrat’s record on all three is strong. Revenue grew at an average rate of 11.7% per year from FY2021 to FY2024, reaching AUD 6,604 million in FY2024. Net profit expanded from AUD 820 million (FY2021) to AUD 1,303 million over the same period. The most recent full-year results extended that trajectory: FY2025 revenue of AUD 6.3 billion (up 11% year on year), NPATA of AUD 1.6 billion (up 12%), and an EBITDA margin of 41.7%.

| Metric | FY2021 | FY2024/FY2025 | Change |

|---|---|---|---|

| Revenue | ~AUD 4.7B | AUD 6.3B (FY2025) | ~11.7% CAGR |

| Net Profit / NPATA | AUD 820M | AUD 1.6B (FY2025 NPATA) | +12% YoY (FY2025) |

| ROE | — | 20.0% | — |

ROE of 20.0%: This indicates Aristocrat generates 20 cents of profit for every dollar of shareholder equity retained in the business, a level that, according to analyst research, signals strong capacity to compound shareholder value over time.

Analysts have cited a 14% three-year earnings per share (EPS) growth trajectory as a medium-term anchor for the bull case. The numbers here establish whether the business underneath the share price is genuinely compounding value, and on this measure, the evidence is difficult to dismiss.

The valuation gap: what analysts see that the market price does not (yet) reflect

At AUD 46.83, Aristocrat trades at a meaningful discount to every layer of broker consensus. The current target range sits at AUD 63.35 to AUD 66.40 across 15 to 16 analysts, with a high target of AUD 74 and a low of AUD 58. The implied upside from the current price to the consensus midpoint is approximately 35-42%.

That gap is not a static number. The consensus itself has moved. In mid-2025, the average broker target sat at approximately AUD 74.91. The decline to the current AUD 63-66 range shows analysts have already absorbed significant disappointment into their models. They have repriced the stock lower, and they still see material upside.

The question is what the market needs to see before it agrees. Three conditions stand out:

- FY2026 guidance credibility: The next reporting period is expected in mid-May 2026. Forward guidance that confirms the post-divestment business can sustain double-digit growth would be the most direct catalyst for re-rating.

- Evidence of margin improvement: The strategic pivot to higher-margin core operations needs to show up in reported margins, not just in management commentary.

- Buyback-driven EPS accretion: The AUD 1.5 billion programme needs to deliver visible per-share earnings improvement to validate the capital allocation decision.

The ASX Continuous Disclosure rules require listed companies to immediately release any information that a reasonable person would expect to have a material effect on the price or value of their securities, which means FY2026 earnings guidance from Aristocrat, if materially different from market expectations, must be disclosed to the market without delay.

Simply Wall St noted on 9 May 2026 that “sustained ROE strength will drive share price higher,” though the same analysis acknowledged execution risks and the slower pace of the digital pivot.

The stock’s 2026 year-to-date recovery of approximately 3.1% has broadly tracked the ASX 200, suggesting the market is not yet pricing in a re-rating; it is simply no longer pricing in further deterioration.

Risks that growth investors must price in before acting

A 35% discount to analyst consensus does not come free. The risks attached to that discount are specific, and several of them could widen the gap rather than close it.

Earnings execution is the primary concern. The H1 FY2025 miss showed consensus expectations had run ahead of delivery. A repeat in FY2026 reporting, with results due imminently, would likely trigger another de-rating rather than the re-rating bulls are positioned for.

FX dependency is understated in headline numbers. Constant currency revenue growth of approximately 5% in H1 FY2025 sat materially below the reported 8.7%, meaning foreign exchange movements flattered operational performance. Any strengthening of the Australian dollar or softening in the US economy, where Aristocrat generates significant land-based revenue, compounds this risk.

Strategic transition carries its own uncertainty. Removing Plarium and Big Fish takes out higher-growth (if lower-quality) digital revenue. The remaining Pixel United real-money operations and core land-based segment may not grow fast enough to satisfy investors expecting the 11-12% annual compounding the historical record delivered.

The four risk categories that growth investors should stress-test:

- Earnings execution risk: Consensus still ahead of proven delivery capacity

- FX dependency: Reported growth overstates operational momentum

- Strategic transition: Narrower portfolio may constrain growth ceiling

- Further analyst revisions: Consensus has already fallen from AUD 74.91 to AUD 63.35-66.40; further cuts are possible if FY2026 guidance disappoints

Cost pressures flagged in H1 FY2025 results commentary remain a watch item, with rising costs limiting NPAT expansion even as top-line revenue grows.

For investors wanting to assess the FY2026 results themselves when they are released in mid-May 2026, our dedicated guide to analysing earnings reports walks through the reconciliation table, GAAP versus non-GAAP EPS gaps, free cash flow verification, and guidance comparison steps that matter most when a result carries binary re-rating risk.

What the numbers say, and what investors still have to decide

The bull case is grounded in data. Aristocrat’s financial compounding record is real: 11.7% revenue CAGR over four years, a 20% ROE, an EBITDA margin of 41.7%, and a management team willing to return AUD 1.5 billion to shareholders through buybacks. The discount to analyst targets of AUD 63-66 is the widest it has been in the current cycle.

The bear case is equally specific. The strategic pivot removes growth optionality that contributed to the stock’s prior premium. Foreign exchange dynamics have flattered reported numbers. FY2026 results, due imminently, carry meaningful re-rating risk in both directions.

- Bull case: Proven compounding record, significant discount to consensus, buyback signals management conviction

- Bear case: Strategic narrowing reduces growth ceiling, FX flatters fundamentals, next earnings report is a binary event

The metrics covered in this analysis, revenue growth, profit trajectory, ROE, and margin profile, represent a partial analytical picture. A complete valuation requires additional tools including discounted cash flow modelling, peer comparison across global gaming operators, and consideration of qualitative competitive factors such as regulatory positioning and product pipeline strength. Research from Rask Invest highlights these metrics as appropriate for growth company assessment but cautions they should not be used in isolation.

At AUD 46.83, the market has made its near-term judgement. FY2026 reporting will determine whether that judgement holds, or whether the gap between price and fundamentals begins to close.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.