Stock-Bond Correlation Hits 30-Year Extreme, Rattling 60/40 Investors

10 hrs ago

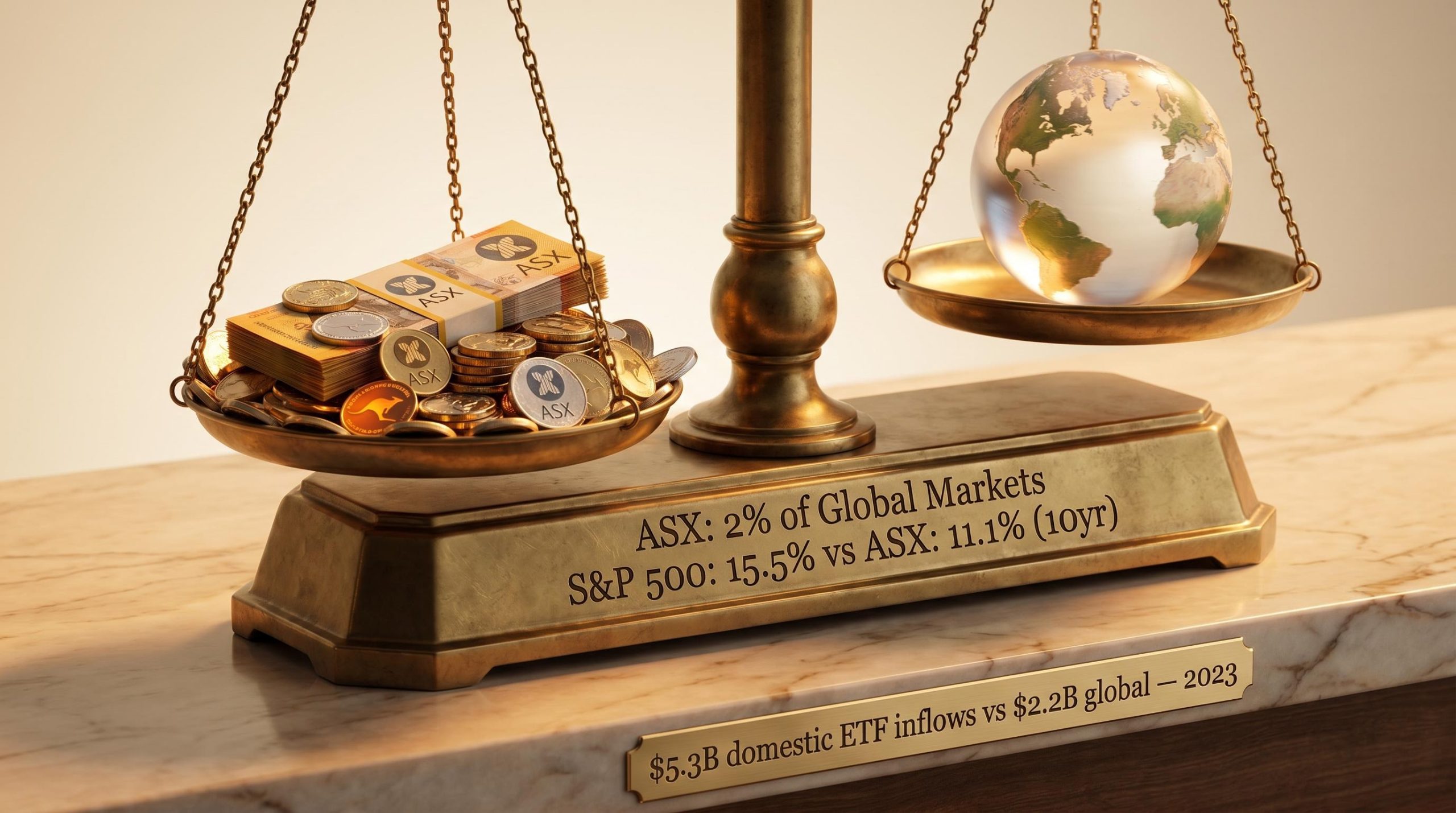

A portfolio with 60% allocated to the ASX 300 gives an investor a larger position in Commonwealth Bank of Australia than in all emerging market equities combined, despite those markets representing roughly 40% of global GDP. The imbalance sounds extreme, yet it describes the structural reality of how most Australian investors are positioned. The ASX represents approximately 2% of global equity market capitalisation. Australian superannuation funds have historically allocated 45-55% of their equities exposure to domestic stocks, and retail investors have been reinforcing that tilt: in 2023, Australian equity ETFs attracted $5.3 billion in inflows while global equity ETFs received just $2.2 billion. The pattern is not fringe behaviour. It is embedded in default fund design, reinforced by familiarity, and carrying a measurable return cost that has compounded over the past decade. What follows is a detailed examination of why the intuitive case for domestic overweighting is weaker than it appears, what the data shows about performance gaps, and how to evaluate rebalancing toward global exposure without abandoning the genuine benefits Australia’s market offers.

Start with the numbers that define the puzzle. The ASX had 1,989 listed companies at end-2024, according to ASIC market structure data. Those listings collectively represent approximately 2% of global equity market capitalisation. A fully market-cap-weighted global investor would hold just 2 cents of every equity dollar in Australian stocks.

Actual allocations look nothing like that. Super funds have historically placed 45-55% of their equities exposure in domestic stocks, an overweight of roughly 20-25 times the ASX’s natural global weight.

APRA’s quarterly superannuation industry data tracks asset allocation across the full superannuation sector, including the split between domestic and international equities, and provides the official regulatory baseline against which fund-level domestic overweighting can be measured.

| Metric | Figure |

|---|---|

| ASX weight in global equity market | ~2% |

| Typical super fund domestic equity allocation | ~45-55% |

| Implied overweight multiple | ~20-25x |

Retail behaviour is heading in the same direction. 2023 ETF flow data showed Australian equity ETFs receiving $5.3 billion (up 20% year-on-year) while global equity ETFs received $2.2 billion (down 15% year-on-year), according to Vanguard data reported by Money Management in January 2024. Domestic preference was strengthening at precisely the moment global equities were rebounding.

Vanguard’s Adam DeSanctis has described home bias as “costly,” identifying familiarity and offshore risk perception as the primary behavioural drivers pushing Australian investors toward domestic overweighting.

This is not irrational in the psychiatric sense. Familiarity reduces perceived risk. Australia’s equity market outperformed many global peers through the 2000s, creating a recency anchor that has persisted well beyond the data that supported it. The question is whether the comfort of the familiar is worth the price that has since attached to it.

The headline comparison is straightforward. Over the 10 years to June 2025, the ASX 200/300 delivered annualised returns of 11.1% including estimated franking credits. The MSCI World returned 12.5%. The S&P 500 returned 15.5%. The data comes from Morningstar Australia, published March 2026.

| Index | 10-Year Annualised Return | 20-Year Annualised Return | Notes |

|---|---|---|---|

| ASX 200/300 (franking-adjusted) | 11.1% | ~11.3% | Includes estimated franking credits (Morningstar/Vanguard) |

| MSCI World | 12.5% | Below ASX ex-US, above ex-franking | Broad global share market (Morningstar) |

| S&P 500 | 15.5% | Ahead across all periods | Technology-driven outperformance (Morningstar) |

The first escape route investors reach for is franking credits. Morningstar addressed this directly.

Morningstar found that “even generous franking treatment would not close the gap” over the 10-year period to June 2025.

The second escape route is timeframe selection. Over 20 years, ASX returns on a franking-adjusted basis (approximately 11.3%) did edge ahead of international ex-US markets, according to Vanguard data reported by Money Management. This is legitimate. The 20-year window captures the 2000s commodity boom and a period of strong Australian bank earnings, both of which rewarded domestic holders. The honesty of this acknowledgement matters: the case against home bias does not require pretending Australia has never outperformed.

It does require recognising that the most recent decade, the one that reflects the market structure investors actually face today, tells a different story.

A 15-year view of ASX market performance makes the structural case even more starkly: Morningstar’s analysis found the ASX 300 compounded at 8.62% per year against the S&P 500’s 16.03% in Australian dollar terms, a gap so large that it compounds into dramatically different terminal wealth outcomes for investors who held the domestic overweight throughout the period.

Calendar year 2024 offered a further data point. The ASX delivered a total return of approximately 11%, solid in isolation. Maple-Brown Abbott observed, however, that the headline masked significant divergence between financials and technology performers and lagging sectors, a “haves vs. have-nots” dynamic within the index itself. Even the good year carried concentration risk beneath the surface.

The performance gap of the past decade is not random. It traces directly to what the ASX actually contains.

Financials account for approximately 30% of ASX index weight. Combined with materials and resources, those two sector groups represent approximately 50-60% of the total index. The S&P 500 is a structurally different market, with technology representing approximately 30% or more of index weight.

The ASX technology sector delivered approximately 50% returns in 2024, according to Maple-Brown Abbott, but it represents such a small proportion of the index that its contribution to portfolio returns remains limited for broadly weighted domestic holders.

The sector breakdown explains the return gap. It also explains why the gap is a structural feature rather than a cyclical accident that will naturally reverse.

According to Dimensional Fund Advisors data, a portfolio with 60% allocated to the ASX 300 creates a larger individual position in Commonwealth Bank of Australia than in all emerging market equities combined, despite those markets representing approximately 40% of global GDP.

The mechanism is straightforward. The ASX is a concentrated index. CBA is its largest constituent. When an investor overweights a concentrated index at 60%, the position in the dominant stock compounds accordingly.

The implication extends beyond sector concentration to individual name concentration. A portfolio that ostensibly holds “Australian equities” is, in practice, making a very large bet on a small number of financial institutions within a single economy. That is a diversification gap that no amount of franking credits can address on its own.

Franking credits are the most common justification Australian investors give for domestic overweighting, and they deserve serious treatment rather than dismissal.

Australian companies pay corporate tax at a rate of 30%. Under the dividend imputation system, when these companies distribute dividends, they can attach franking credits representing tax already paid at the corporate level. Shareholders then use those credits to offset their own income tax liability. If the credit exceeds the shareholder’s tax obligation, they receive the difference as a cash refund.

The effect is real. Australian gross dividend yields have historically sat at 4-5%, compared with approximately 2% for global equities. Morningstar Australia estimates franking credits add approximately 2% per annum to ASX returns on a long-term average basis, with the typical range falling between 1.5% and 2.5% annually.

The question is whether that 2% offset changes the conclusion.

Over 10 years to June 2025, even with full franking inclusion, the ASX at 11.1% trailed the MSCI World at 12.5% (a 1.4 percentage point gap) and the S&P 500 at 15.5% (a 4.4 percentage point gap). Over 20 years, franking-adjusted ASX returns at approximately 11.3% edged ahead of international ex-US markets, the one timeframe where the franking offset holds up against non-US global exposure.

The arithmetic is specific: a 2% franking credit yield closes roughly half the 1.4 percentage point gap against the MSCI World over 10 years, and less than half of the 4.4 percentage point gap against the S&P 500.

The imputation system does not deliver equal value to all investors. The benefit depends entirely on the recipient’s tax position:

For SMSF trustees in pension phase and retirees wanting to model how the imputation system translates into actual cash refunds, our dedicated guide to franking credit calculations walks through the 30/70 formula with worked examples, covering the 45-day holding rule, the automatic ATO refund process introduced in 2025, and how grossed-up yields compare across fully and partially franked stocks.

For income-focused retirees and complying super funds, the franking case has genuine weight. For growth-oriented investors in accumulation phase with decades of compounding ahead, the data suggests the franking offset does not justify the concentration cost.

The question is not whether to own Australian equities. It is what weight they should carry, and whether that weight reflects a deliberate decision or an inherited default.

The traditional super fund split of approximately 45% domestic and 55% international equities has been embedded in many default options for years. Critics argue this does not reflect a considered view on expected returns but rather institutional inertia, a legacy allocation that has not been re-evaluated against the ASX’s declining share of global market capitalisation.

Fisher Investments Australia, in analysis published August 2025, labelled home bias “suboptimal” and cited the fact that global markets do not move in lockstep with the ASX as the core diversification argument for reducing domestic concentration.

Dimensional’s Baru Singh has noted that some home bias is reasonable given franking credits and the behavioural benefit of familiarity, but that concentration above a considered threshold represents a risk not compensated by the evidence.

The appropriate domestic allocation varies by investor profile:

No single number applies to all three. The floor is the ASX’s 2% global weight; the ceiling is wherever the investor’s own tax position, income needs, and risk tolerance place it. The point is that the number should be chosen, not inherited.

Over the past decade, the annualised gap between the ASX (at 11.1% including franking) and the S&P 500 (at 15.5%) amounts to 4.4 percentage points per year. For a growth-oriented investor who held full domestic concentration rather than US exposure, that gap compounded year after year across the most recent decade of data.

A 4.4 percentage point annualised drag over 10 years is not a rounding error. On a $500,000 portfolio, the difference between 11.1% and 15.5% compounding annually represents hundreds of thousands of dollars in foregone returns.

The behavioural drivers that produced this outcome remain active. The 2023 ETF flow data showed domestic bias strengthening (Australian ETF inflows of $5.3 billion versus global inflows of $2.2 billion) at precisely the moment global equities were rebounding. Coalition Greenwich’s 2025 survey of institutional investors, conducted September-October 2025, noted the persistence of domestic equity tilts among major Australian funds.

International ETF inflows told a different story in early 2026: for the first time on record, international ETFs overtook domestic funds as the most purchased category on Selfwealth by Syfe in Q1 2026, with $6.9 billion flowing into international equity ETFs across the broader Australian market, suggesting that the behavioural shift the data has long argued for may finally be underway.

Fisher Investments Australia’s August 2025 assessment remains pointed: home bias is “suboptimal” for growth investors. The familiarity that makes domestic stocks feel safer is the same familiarity that has, over the most recent measurable period, delivered lower returns at higher concentration.

The evidence does not demand that Australian investors abandon domestic equities. Franking credits remain valuable for specific investor profiles. The ASX provides income characteristics that global indices do not replicate. Some home bias is structurally defensible.

What the evidence does demand is a deliberate answer to a specific question: when was the last time the domestic equity weighting in a given portfolio was actively chosen based on current data rather than inherited from a default setting designed years ago? If the answer is unclear, the cost of that ambiguity has been compounding since at least 2015.

Investors ready to act on that question will find our comprehensive walkthrough of portfolio rebalancing strategy covers the specific execution sequence for Australian investors: starting with new contributions and dividend redirection inside super, moving to SMSF and tax-advantaged account sales, and only using taxable account sales as a last resort, with worked examples of drift thresholds and alternative capital destinations including private credit and fixed income.

The data across the most recent decade consistently shows that excessive domestic concentration has cost Australian growth investors materially. The ASX’s structural composition, heavily weighted to financials and materials and underweight in global technology, makes this a predictable outcome rather than an accident of timing.

For income-focused retirees and pension-phase super members, the franking credit advantage provides genuine and measurable compensation. That nuance is real and should not be dismissed. For growth-oriented investors with long compounding horizons, the offset falls well short of the gap.

This article has laid out the scale of the mismatch, the return evidence across multiple timeframes, the structural mechanics of ASX concentration, and the specific investor profiles for whom different allocations are supported by data. The next step sits with the individual portfolio. The framework is here. The question is whether the current allocation reflects a decision or a default.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

Australian home bias refers to the tendency of Australian investors to allocate a disproportionately large share of their portfolio to ASX-listed stocks. Despite the ASX representing only about 2% of global equity market capitalisation, superannuation funds have historically placed 45-55% of their equities exposure in domestic stocks.

Morningstar found that even with full franking credit inclusion, the ASX returned 11.1% annually over the 10 years to June 2025, still trailing the MSCI World at 12.5% and the S&P 500 at 15.5%. Franking credits add roughly 2% per annum on average, which closes part of the gap against the MSCI World but less than half of the gap against the S&P 500.

Financials account for approximately 30% of ASX index weight, and combined with materials and resources the two sector groups represent around 50-60% of the total index. By contrast, technology represents roughly 30% or more of the S&P 500, giving it significantly broader sector distribution and exposure to the technology-led growth that dominated the past decade.

Pension-phase superannuation members (taxed at 0%) and accumulation-phase super members (taxed at 15%) receive the highest benefit from franking credits because excess credits are refunded as cash. Growth-oriented investors with higher marginal tax rates and long compounding horizons receive limited benefit relative to the global capital growth opportunity cost.

Investors can reduce home bias by redirecting new contributions and dividends toward global equity funds inside superannuation before touching existing holdings, and by prioritising sales inside tax-advantaged accounts such as SMSFs before using taxable accounts. The key step is actively choosing a domestic allocation based on current return data and personal tax position rather than inheriting a default fund weighting.