What’s Really Driving Oil Price Swings Near Hormuz

2 hrs ago

Akamai Technologies surged nearly 30% in premarket trading on 8 May 2026, marking the largest single-day gain for the stock in more than 22 years. On the same morning, HubSpot, Trade Desk, and Cloudflare each fell by double digits. All four companies reported software earnings on 7 May, yet the gap between winners and losers had little to do with revenue growth. Cloudflare grew 34% year over year and still dropped 12%. What separated these stocks was not the headline number but the source of that growth and where each company sits in the AI spending hierarchy. This article breaks down what drove the divergence, what the losing companies’ results actually showed, and how retail investors can apply a consistent framework when evaluating software earnings in 2026.

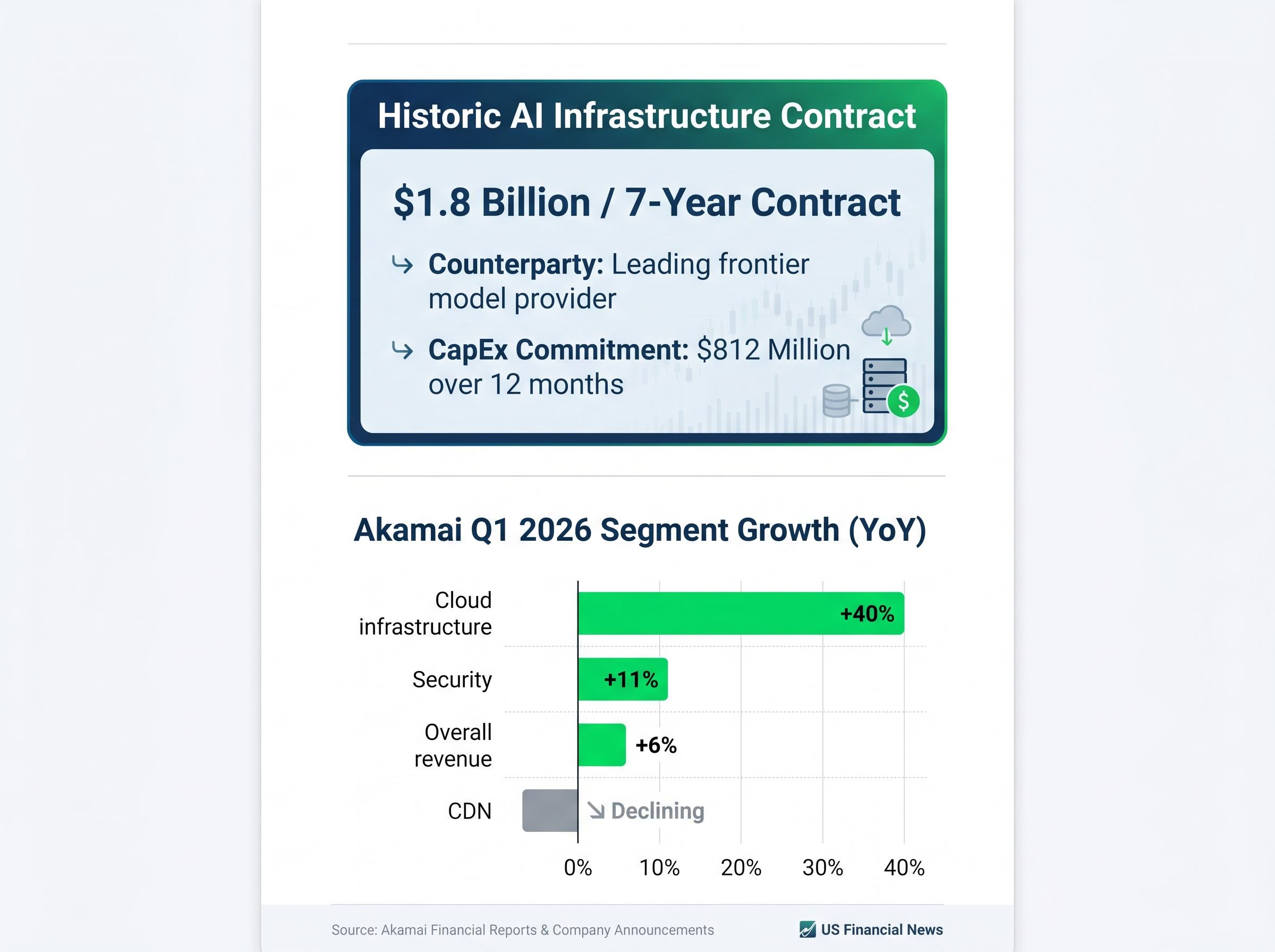

The numbers tell the story before the analysis does. Akamai announced a $1.8 billion, seven-year contract with an unnamed leading frontier model provider, the largest customer deal in the company’s history.

The contract did not arrive in isolation. Akamai’s cloud infrastructure segment grew 40% year over year in Q1 2026, while its legacy content delivery network (CDN) business declined. Security revenue rose 11%, and overall revenue grew 6%. The internal results mirror the contract’s signal: the company is pivoting from content delivery to AI infrastructure at pace.

KeyBanc raised its price target on Akamai from $120 to $195, maintaining an Overweight rating. The firm cited inference revenue growth as a structurally new and larger opportunity than CDN delivery.

The CapEx burden, however, is the detail the headline obscures. An $812 million commitment over 12 months represents a material near-term drag on free cash flow, framing the win as high-reward but not risk-free.

AI infrastructure investment at the scale Akamai is now committing to, with $812 million in CapEx over 12 months, connects directly to the broader capital redirection occurring across the industry: Wall Street anticipates $530-$700 billion in global data centre spending in 2026 alone, with power supply emerging as the primary physical constraint on how fast the buildout can proceed.

| Segment | Q1 2026 YoY Growth |

|---|---|

| Cloud infrastructure | +40% |

| Security | +11% |

| Overall revenue | +6% |

| CDN | Declining |

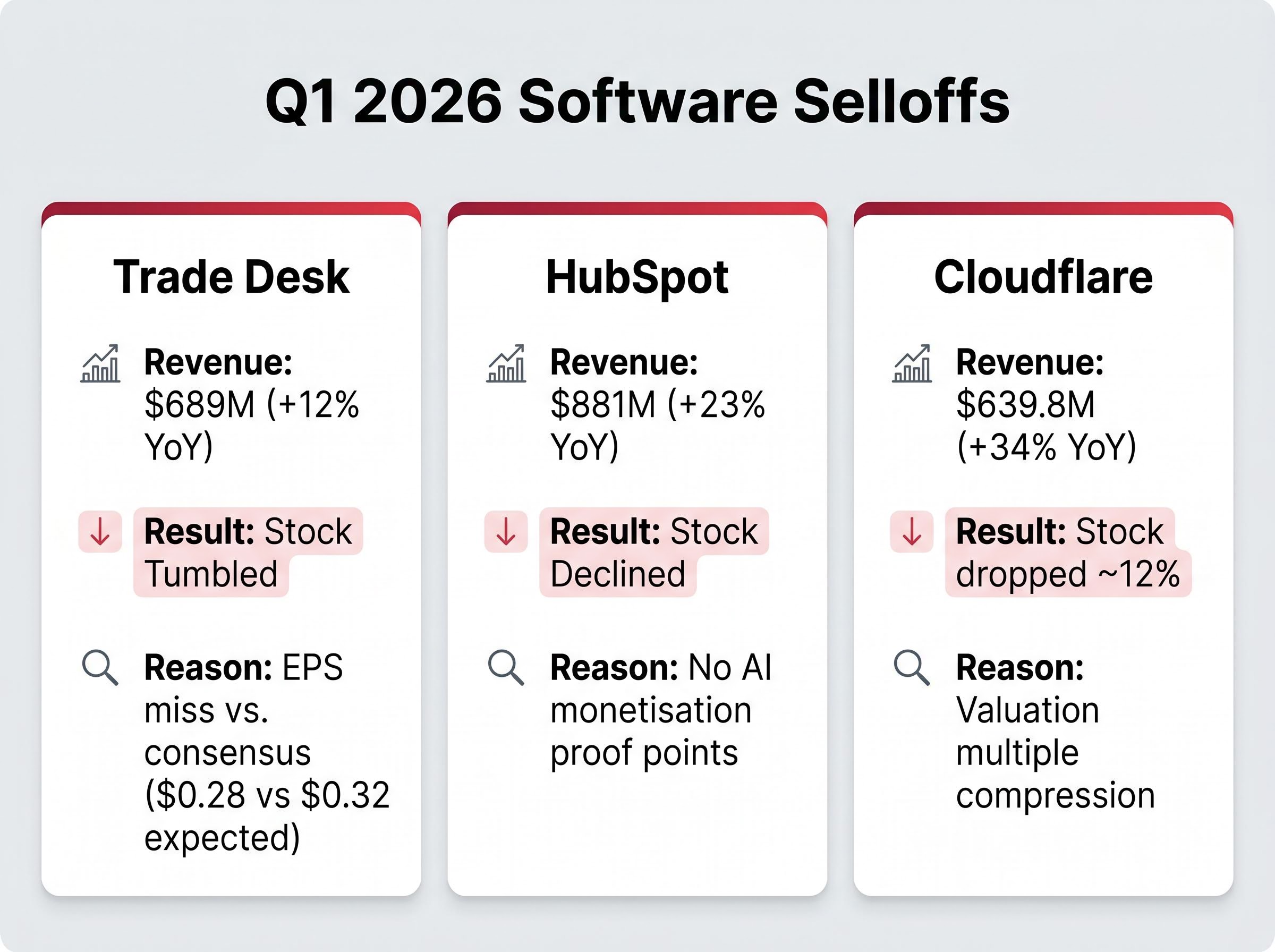

It would be a mistake to treat these three declines as a single story. Each stock fell for a distinct reason, and understanding those reasons matters for how to interpret each name going forward.

| Company | Q1 2026 Revenue | YoY Growth | Stock Reaction | Key Failure Mode |

|---|---|---|---|---|

| Trade Desk | $689M | +12% | Tumbled | EPS miss vs. consensus |

| HubSpot | $881M | +23% | Declined | No AI monetisation proof points |

| Cloudflare | $639.8M | +34% | ~**-12%** | Valuation multiple compression |

Trade Desk reported earnings per share of $0.28 against a consensus expectation of $0.32. Revenue grew 12% year over year to $689 million, and Q2 2026 guidance came in at a minimum of $750 million. None of that mattered. In earnings season, the benchmark is the consensus estimate, not the year-ago figure, and Trade Desk missed it.

HubSpot delivered $881 million in revenue, 23% year-over-year growth, $33 million in GAAP net income, and $154 million in operating cash flow. The problem was not the quarter. The problem was what the quarter did not contain: any visible evidence that the company is monetising AI in a way that justifies its forward multiple.

Cloudflare posed the sharpest paradox. Revenue grew 34% to $639.8 million, operating income reached $73.1 million, and free cash flow hit $84.1 million. The stock still dropped approximately 12%. Valuation multiple compression is now operating independently of fundamental performance for high-growth SaaS names.

The market is not rewarding software growth uniformly in 2026. It is rewarding growth in a specific category, and the distinction comes down to where a company sits in the AI spending stack.

AI infrastructure companies provide the compute, networking, edge delivery, and hosting capacity that model training and inference require. Application-layer SaaS companies provide the end-user tools (CRM platforms, marketing automation, ad tech) that enterprises deploy on top of that infrastructure. In 2026, value capture is concentrating in the infrastructure layer.

SaaS stocks have collectively lost over $1 trillion in market value in 2026 as AI disrupts legacy software models, a dynamic some analysts have characterised as a “SaaSpocalypse.”

The mechanics are straightforward. As enterprises deploy agentic AI, which refers to AI systems capable of performing multi-step software tasks autonomously, the need for traditional per-seat SaaS subscriptions weakens. The “land and expand” model built on net revenue retention (NRR), a measure of how much existing customers spend over time, is slowing across the SaaS cohort as enterprises consolidate vendors and redirect budgets toward AI infrastructure and model providers.

Akamai’s own results illustrate the split in miniature: CDN revenue declining while cloud AI infrastructure grew 40%.

The price target revisions that followed the session were not minor adjustments. They reflected a fundamental reassessment of Akamai’s long-term earnings potential.

| Analyst Firm | Previous Target | New Target | Key Rationale |

|---|---|---|---|

| KeyBanc | $120 | $195 | Inference revenue growth opportunity |

| Evercore ISI | $130 | $165 | $1.8B AI deal as demand signal |

KeyBanc’s 62% price target increase signals that the firm views inference revenue as a structurally different and larger opportunity than CDN delivery, not merely an incremental revenue line. Evercore ISI’s raise anchored specifically to the $1.8 billion AI deal as evidence of enterprise AI infrastructure demand at scale. Following the premarket surge, Akamai was on track for its highest share price levels since the dot-com peak.

The broader analyst community has characterised 2026 as a year of structural repricing in software, with AI infrastructure beneficiaries being separated from legacy SaaS incumbents in terms of long-term earnings potential.

The legacy software repricing playing out across 2026 is not limited to single-quarter earnings reactions; capital is actively rotating out of headcount-dependent platforms and into consumption-based infrastructure models, a structural reallocation that has been accompanied by $1.2 trillion in M&A as incumbents attempt to acquire the AI capabilities they cannot build fast enough organically.

The repricing carries tension, however. Even Akamai, the session’s clear winner, faces real execution risks:

The session on 7 May offers a repeatable framework for the next software earnings release. Three questions, applied consistently, can help anticipate post-earnings reactions rather than being surprised by them.

NRR trends and forward guidance deserve particular attention for SaaS companies navigating the AI transition. Headline revenue growth alone is no longer a reliable predictor of post-earnings stock performance.

For investors who want to move beyond consensus estimates and build their own view on stocks like Akamai or Cloudflare after a volatile earnings session, our comprehensive walkthrough of scenario-based stock valuation walks through a five-step framework covering revenue growth assumptions, margin inputs, exit multiple selection, and probability-weighted return calculations across bear, base, and bull cases.

The AI infrastructure versus legacy SaaS divergence is expected to persist through the Q2 2026 reporting season. Bill Holdings, which also reported on 7 May, gained approximately 12% in premarket trading on the back of above-consensus results in transaction and subscriber fee revenue, providing a secondary example of how beating expectations in the right category continues to drive positive reactions.

The results from 7 May were not a coincidence of single-quarter beats and misses. They were evidence of a durable reordering in enterprise software spending.

The Akamai versus Cloudflare contrast is the sharpest illustration. One company gained 30% on a $1.8 billion AI infrastructure contract. The other lost 12% despite 34% revenue growth. The difference was not execution quality. It was category positioning.

Even strong SaaS growth is being discounted by the market unless it connects directly to AI infrastructure demand. The $1 trillion in SaaS market value lost in 2026 reflects a structural repricing, not a temporary rotation.

Investors evaluating software stocks in 2026 and beyond may benefit from assessing AI infrastructure exposure and NRR trajectory as primary valuation inputs, rather than relying on headline revenue growth alone. The session’s lesson is that the market has already made that shift.

The SaaSpocalypse valuation crisis that emerged in early 2026 drew warnings from institutional heavyweights including Morgan Stanley, who flagged that capital rotation away from legacy software names toward AI infrastructure was not a temporary sector rotation but a fundamental repricing of growth multiples across the SaaS cohort.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AI infrastructure refers to the compute, networking, edge delivery, and hosting capacity that powers model training and inference. In 2026, the market is rewarding companies in this layer over traditional application-layer SaaS providers.

Cloudflare fell approximately 12% after reporting 34% revenue growth due to valuation multiple compression, meaning the market is discounting high-growth SaaS multiples unless the growth connects directly to AI infrastructure demand.

Akamai announced a $1.8 billion, seven-year contract with an unnamed leading frontier model provider, the largest deal in its history, alongside 40% year-over-year growth in its cloud infrastructure segment.

Investors should ask three questions: where the growth is coming from (infrastructure vs. application layer), how the result compares to consensus estimates rather than year-ago figures, and what forward guidance signals about execution risk and spending commitments.

Net revenue retention (NRR) measures how much existing customers spend over time and has been the core growth driver for SaaS companies. In 2026, NRR is slowing across the SaaS cohort as enterprises consolidate vendors and redirect budgets toward AI infrastructure, making it a key metric to monitor.