As of 30 April 2026, Morningstar’s price-to-fair-value composite for US equities sat at 0.95, recovering from a trough of 0.88 at the close of March. That seven-point swing in a single month represents one of the sharpest valuation compressions in recent memory, and it did not lift all sectors equally.

April’s rally was heavily concentrated in communications (up more than 18%) and technology (up more than 17%), while energy fell roughly 3% and healthcare posted slight losses. The result is a market where sector-level dispersion now tells a far more actionable story than index-level averages. Investors using April’s headline recovery as a single data point are missing the rotational dynamics underneath.

What follows maps the current valuation landscape across US equity sectors using Morningstar’s price-to-fair-value framework, identifies where genuine post-rally opportunities remain, flags which sectors have moved from attractive to extended, and anchors each assessment to the dominant macro and earnings-season forces shaping the second half of 2026.

How to read the post-April valuation map

Morningstar’s price-to-fair-value ratio compares a stock’s current market price to what Morningstar’s equity analysts estimate the business is actually worth. A reading below 1.00 means the stock (or, aggregated upward, the sector) trades below estimated fair value. A reading of 0.95 at the index level, then, implies a 5% aggregate discount for US equities. That single number, however, conceals wide dispersion across sectors: some trade at discounts exceeding 10%, while others carry premiums approaching 20%.

The sector-level picture connects directly to a broader growth stock discount that sat at 21% as recently as late March 2026, a level Morningstar data shows has occurred less than 5% of the time since 2011, and the partial recovery since then still leaves growth-oriented portfolios with meaningful upside relative to assessed fair value.

The distinction matters. A market-wide discount and a selective opportunity are not the same thing.

“US equities recovered from a 0.88 price-to-fair-value trough in March 2026 to 0.95 by April 30, still below fair value at the index level but masking extreme sector divergence.”

Four macro forces shape the backdrop against which every sector valuation should be read:

- Earnings momentum: FactSet’s blended Q1 2026 EPS growth came in at 27.1% year-over-year, with profit margins near 13.4%, reflecting broad-based corporate strength.

- The AI capex supercycle: Hyperscaler capital expenditure commitments for 2026 are roughly double prior estimates, anchoring demand across technology and industrial supply chains.

- Federal Reserve policy: The fed funds rate remains paused at 3.50%-3.75%, creating a rate environment that supports growth equity valuations while constraining the rate-sensitive recovery in small-caps and real estate.

- The tariff environment: A global 10% import duty imposed in February 2026 continues to inject margin uncertainty across import-exposed sectors.

FactSet Earnings Insight for Q1 2026 places the blended EPS growth rate at 27.1% year-over-year with a net profit margin of approximately 13.4%, figures that frame the earnings backdrop against which every sector valuation discount or premium in this analysis should be assessed.

Goldman Sachs forecasts the S&P 500 to rise approximately 6% in 2026, with AI investment contributing roughly 40% of earnings growth. That estimate provides a useful ceiling: sectors trading well above fair value need to deliver earnings growth beyond the index-level consensus to justify their premiums.

When big ASX news breaks, our subscribers know first

Technology and Communications: Diverging Valuations Beneath the Post-Rally Headlines

A 17% monthly gain in technology and an 18% surge in communications would, in most environments, signal a sector that has run past fair value. The opposite is true here. Technology remains the most undervalued sector in Morningstar’s US coverage universe, trading at an 11% discount to fair value even after April’s advance.

AI’s leading beneficiaries: the valuation story

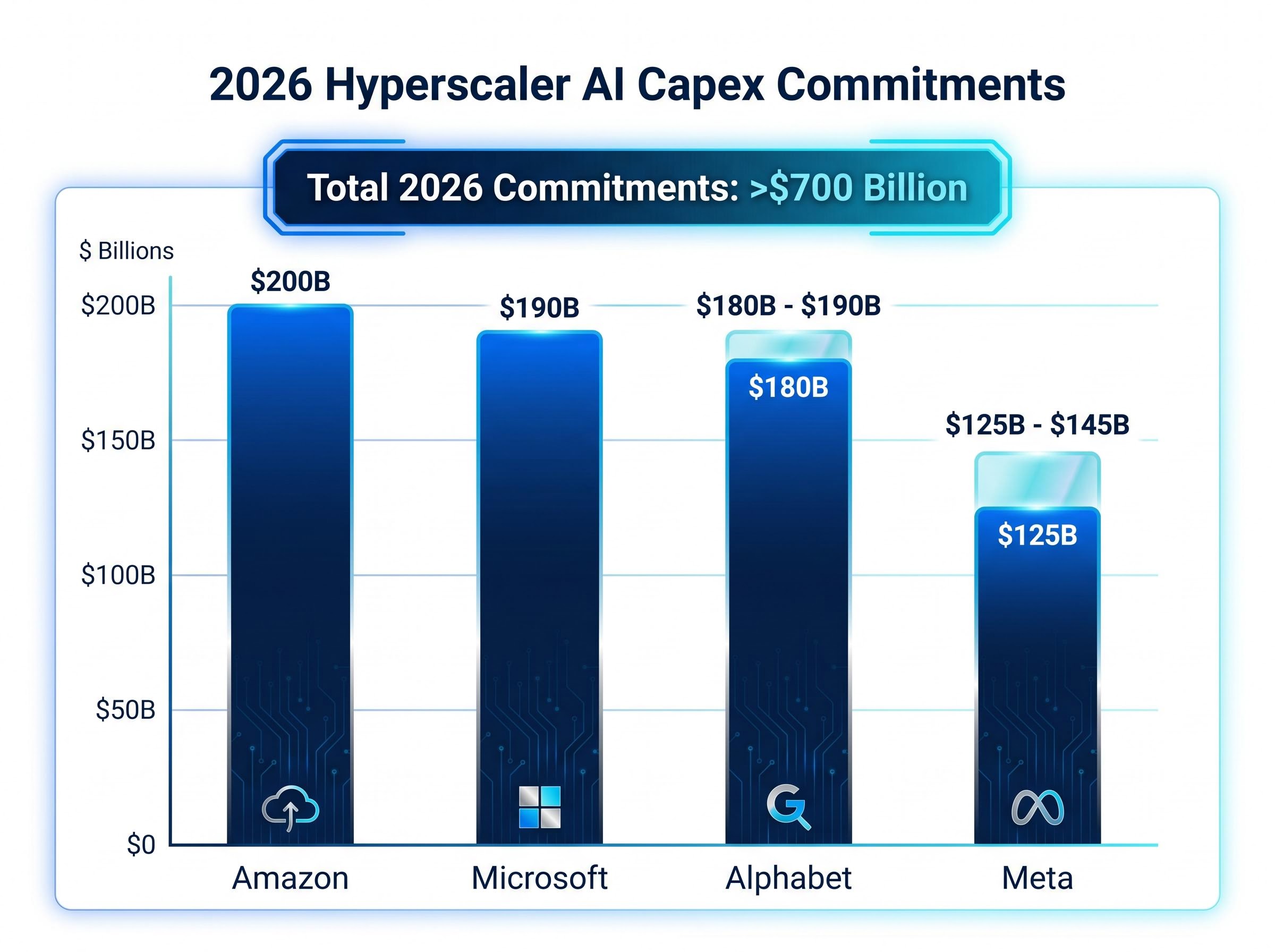

The discount is structurally supported by the scale of hyperscaler capital commitments now flowing into the AI supply chain. Microsoft projects approximately $190 billion in 2026 capex. Amazon has announced $200 billion, the majority AI-related. Alphabet is spending $180-$190 billion, with even higher figures expected in 2027. Meta has committed $125-$145 billion. These figures are roughly double prior estimates and represent the demand anchor for AI infrastructure names.

The hyperscaler capital commitments underpinning technology’s valuation discount are larger than most sell-side models anticipated: Q1 2026 alone saw $130 billion deployed across the four major cloud providers, with Microsoft reporting an annualised AI revenue run rate surpassing $37 billion, up 123% year-over-year, providing commercial revenue justification that distinguishes the current cycle from prior infrastructure build-outs.

Nvidia and Broadcom carry Morningstar 4-star ratings with wide economic moat designations, meaning their competitive advantages are assessed as durable over a 20-year horizon. Alphabet, also rated 4-star with a wide moat, drove almost the entirety of communications’ April advance, making that sector’s headline performance a narrower story than it first appears.

Goldman Sachs estimates 22% EPS growth for the technology sector in Q2 2026, reinforcing the earnings case behind the valuation discount.

Tech’s overextended areas: where value is scarce

Not every technology name participates in the discount. Ciena and Western Digital, both lacking wide moat designations, sit on the overvalued end of Morningstar’s spectrum. The distinction is economic moat: companies exposed to commodity hardware cycles without durable pricing power tend to compress toward fair value as supply catches demand.

| Stock | Sector | Morningstar Rating | Moat | Valuation Status |

|---|---|---|---|---|

| Nvidia (NVDA) | Technology | 4-star | Wide | Undervalued |

| Broadcom (AVGO) | Technology | 4-star | Wide | Undervalued |

| Alphabet (GOOGL) | Communications | 4-star | Wide | Undervalued |

| Ciena (CIEN) | Technology | — | None | Overvalued |

| Western Digital (WDC) | Technology | — | None | Overvalued |

Healthcare and financials: the quiet undervaluation case

While April’s capital flowed into AI-linked sectors, healthcare and financials were largely bypassed. That neglect created two of the more interesting valuation gaps in the current market.

Healthcare sits at a 7% discount to Morningstar fair value, the second-largest discount among major sectors. The most attractive subsegment is not pharma but medical devices, diagnostics, and instruments, where names like Danaher (DHR), Medtronic (MDT), and Abbott (ABT) offer a combination of durable demand profiles and post-April pricing that reflects none of April’s enthusiasm.

- Danaher (DHR): Life sciences instrumentation leader trading below Morningstar’s fair value estimate

- Medtronic (MDT): Medical device exposure with steady recurring revenue from surgical and cardiac portfolios

- Abbott (ABT): Diagnostics and device diversification providing defensive earnings characteristics

Healthcare was one of only two sectors to post negative returns in April, with losses broadly distributed. Johnson & Johnson (JNJ), rated 2-star by Morningstar (indicating overvaluation), was the single largest individual detractor.

“Healthcare was one of only two sectors to decline in April 2026 and now sits at a 7% discount to fair value, with medical devices and diagnostics representing the deepest pockets of opportunity.”

Financials trade at a 5% discount, tied with real estate for the third-most undervalued sector. The sector entered 2026 as the second-most overvalued in Morningstar’s coverage; its status as the second-worst year-to-date performer has since unwound that prior premium. Net interest margin expansion dynamics in the current rate environment support the earnings case, particularly for regional banks.

Goldman Sachs has upgraded healthcare to overweight and expressed a preference for regional banks within financials, providing institutional validation for both discount theses.

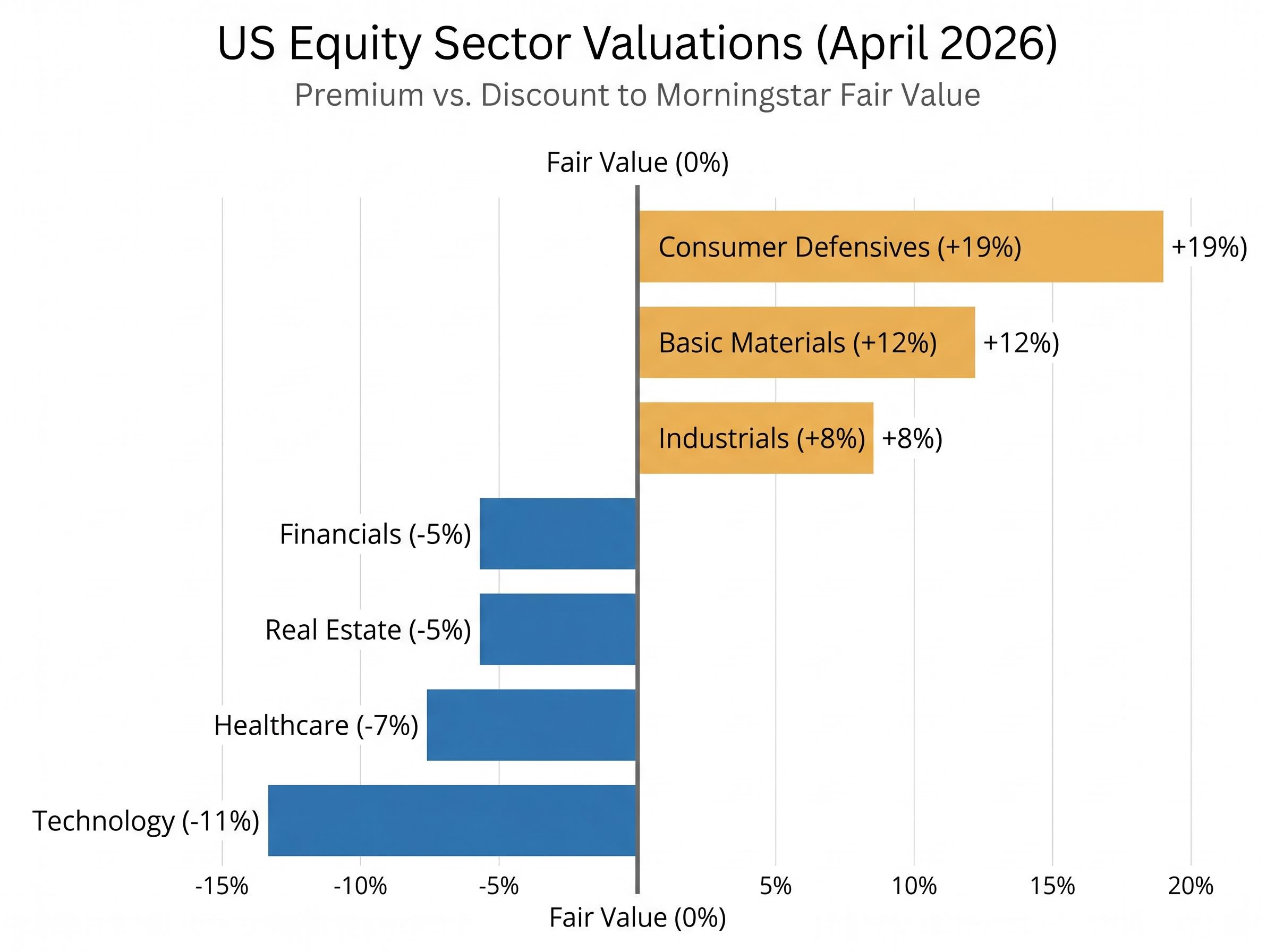

Where April’s rally created overvaluation: energy, consumer defensives, and industrials

April’s momentum did not create opportunity everywhere. Four sectors now trade at meaningful premiums to fair value, and the durability of those premiums varies considerably.

- Consumer defensives (19% premium): The starkest overvaluation case in the market, but the distortion is concentrated. Walmart and Costco, both rated 1-star by Morningstar, account for the bulk of the sector premium. Stripped of those two mega-cap names, the sector is approximately fairly valued.

- Industrials (8% premium): A nearly 17% year-to-date rally, attributed largely to the AI infrastructure supply chain narrative, has priced in a durable demand signal that may fade as hyperscaler capex cycles normalise.

- Basic materials (12% premium): A 14%+ year-to-date advance has compressed valuations beyond what fundamentals support. This is post-rally momentum, not a structural rerating.

- Energy (complex): The sector posted year-to-date gains of approximately 30.7% while declining roughly 3% in April as crude prices eased. WTI crude sits near $103.92 per barrel; Brent near $110.45. The Reuters 2026 oil price survey averages approximately $86.38, suggesting the current elevated pricing, supported by geopolitical factors including Iran-related supply disruptions, may not persist.

The Reuters 2026 oil price survey, published in January, placed the consensus Brent crude forecast well below current spot prices, reinforcing the reversion risk embedded in energy sector valuations that have rallied more than 30% year-to-date.

| Sector | Premium/Discount | YTD 2026 Return | Key Driver | Key Risk |

|---|---|---|---|---|

| Consumer Defensives | +19% premium | Moderate | WMT/COST mega-cap weighting | Premium concentrated in two names |

| Basic Materials | +12% premium | ~14%+ | Post-rally momentum | No fundamental rerating support |

| Industrials | +8% premium | ~17% | AI infrastructure demand | Capex cycle normalisation |

| Energy | Elevated | ~30.7% | Geopolitical crude premium | Oil price reversion to ~$86 avg. |

Small-caps and real estate: the overlooked deep-value cases

April’s rally restored index-level confidence. It did not restore small-cap valuations.

The Russell 2000 trades at an 18% discount to Morningstar fair value, the widest gap among all major equity categories. For context, the discount by capitalisation tier as of 30 April 2026:

- Large-cap: 4% discount

- Mid-cap: 4% discount

- Small-cap: 18% discount

The disparity is stark. The AAII overall bullish sentiment reading stood at 38.13% as of early May 2026, reflecting a market that has recovered confidence at the index level. Small-cap flows and valuations have not reflected equivalent enthusiasm.

The 18% valuation discount in small-caps is not purely a macro story: a structural small-cap quality deficit, measured at -0.64 on Morningstar’s quality factor score as of December 2025, reflects nearly half of Russell 2000 companies being unprofitable, a proportion that has roughly doubled since the Global Financial Crisis as private equity and venture capital have systematically removed the highest-quality names from public indexes.

“At an 18% discount to fair value, small-cap equities represent the deepest valuation gap in Morningstar’s US coverage universe as of April 30, 2026.”

The current Fed pause at 3.50%-3.75% creates a scenario where any future rate cuts would disproportionately benefit small-cap valuations and earnings, given these companies’ heavier reliance on floating-rate debt. Goldman Sachs sees small-cap rotation accelerating on rate cut expectations, adding institutional weight to the discount thesis.

Real estate’s hidden gems: the case for cell tower REITs

Real estate trades at a 5% discount to fair value (tied with financials) despite year-to-date gains exceeding 10%. Within the sector, the highest-conviction opportunity sits in cell tower REITs: American Tower (AMT) and Crown Castle (CCI). Both remain out of favour despite durable infrastructure demand driven by 5G densification and, increasingly, AI-related data transmission requirements. The combination of a sector-level discount and a structural demand tailwind positions cell tower REITs as the most asymmetric opportunity within the real estate coverage.

Positioning for what April left unfinished

The valuation hierarchy that emerged from April’s rally is unusually clear.

- Where opportunity persists: Technology (11% discount) and communications remain the most undervalued large-cap sectors. Healthcare (7% discount) and financials (5% discount) offer quieter but meaningful gaps. Small-caps carry the widest discount at 18%, the deepest value in Morningstar’s US coverage universe.

- Where caution is warranted: Consumer defensives (19% premium, concentrated in Walmart and Costco), basic materials (12% premium), and industrials (8% premium) are the sectors where April’s momentum has most meaningfully outrun fundamental value.

- The structural risk to monitor: AI capex commitments at the hyperscaler level, totalling more than $700 billion across Microsoft, Amazon, Alphabet, and Meta in 2026 alone, are larger than most investors have priced in. The supply-demand dynamics in commodity hardware could compress margins for names without economic moats once the current shortage cycle turns.

Investors assessing post-April positioning may find the most favourable risk-reward in adding to wide-moat AI leaders on any pullback, reducing exposure to consumer defensives at a 19% premium, and examining the small-cap discount before institutional rotation narrows the gap.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—