RBC Raises S&P 500 Target to 8,150, Warns of 10% Pullback Risk

1 hr ago

Two ASX-listed data centre stocks delivered sharply divergent moves on 6 May 2026, each anchored by announcements that underline the scale of capital now flowing into Australian digital infrastructure. DigiCo Infrastructure REIT (ASX: DGT) surged after confirming a US$750 million divestment of its Chicago facility, while Infratil (ASX: IFT) reached all-time highs after its subsidiary CDC Data Centres signed what is being described as the largest data centre contract in Australian history: 555MW of contracted capacity with a US investment-grade hyperscaler. The simultaneous events are less coincidence than confirmation. Institutional capital is accelerating into Australian data centre investment at a pace that, even 18 months ago, few ASX portfolios were structured to capture. What follows is an unpacking of both deals, the capital strategies behind them, the earnings trajectories they imply, and the risks that sit between contracted capacity and delivered returns.

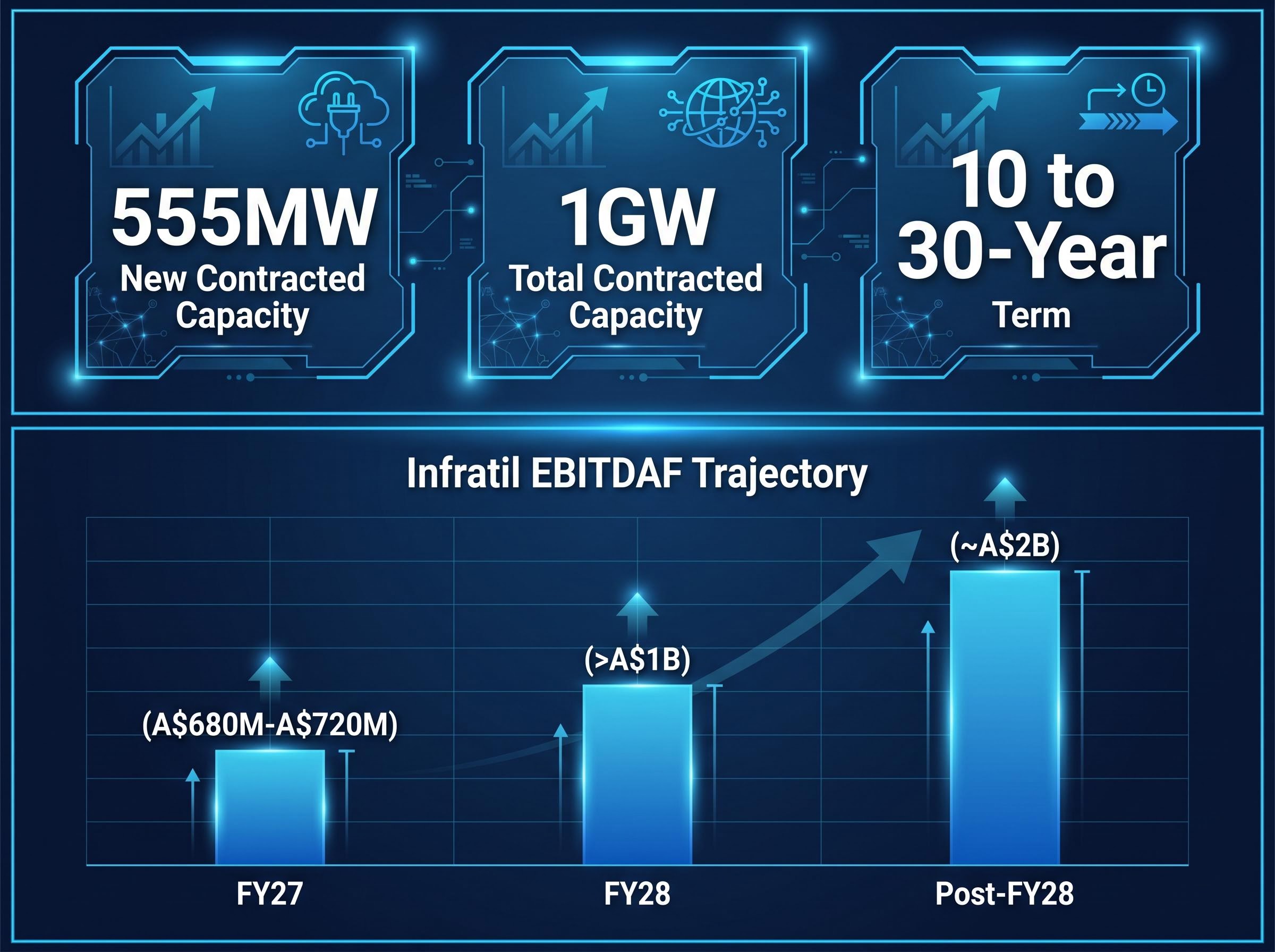

The number lands first: 555MW of contracted data centre capacity, secured under a minimum 10-year term with renewal options extending the total commitment to as long as 30 years. The counterparty is an undisclosed US investment-grade hyperscaler. The deal, announced via ASX on 6 May 2026, pushes CDC’s total contracted capacity past 1GW, a milestone that justifies the “largest data centre contract in Australian history” descriptor attached to it by multiple outlets.

555MW contracted capacity signed with a US investment-grade hyperscaler, making it the largest data centre contract in Australian history by committed power.

Rollout is staggered across three campuses, reflecting national infrastructure breadth rather than a single-site concentration:

The earnings trajectory implied by the contract is substantial. Infratil, which holds a 49.7% stake in CDC, left its FY27 EBITDAF guidance unchanged at A$680 million to A$720 million but projected FY28 EBITDAF to exceed A$1 billion. Once the 555MW contract is fully deployed post-FY28, annualised contracted EBITDAF is estimated at approximately A$2 billion. FY27 capital expenditure (excluding land) is expected to rise to A$3.8 billion to A$4.2 billion, signalling a generational infrastructure build rather than an incremental expansion.

CDC’s FY27 earnings upgrade in March 2026, which lifted EBITDAF guidance to A$680-720 million on the back of 200MW of new operating capacity added in a single quarter, established the baseline that the 555MW contract now extends materially beyond FY28, providing investors with a sequential progression of guidance upgrades rather than a single step-change.

| Period | EBITDAF Guidance |

|---|---|

| FY27 | A$680M-A$720M |

| FY28 | Exceeds A$1B |

| Post-FY28 (annualised, fully deployed) | ~A$2B (contracted) |

For investors holding IFT, the deal provides a concrete, long-duration earnings trajectory extending well beyond FY28, anchored by contracted revenue from a single institutional-grade customer.

Where CDC is building, DGT is recycling. The REIT confirmed the sale of its Chicago CHI1 facility for US$750 million, representing an approximately 5% premium to the November 2024 acquisition price. The move is not a retreat from data centres; it is a capital discipline sequence designed to be read in three steps:

| Metric | Detail |

|---|---|

| Sale price | US$750M |

| Net cash proceeds | ~A$360M |

| Gearing (pre-sale) | 36% |

| Gearing (post-sale) | ~17% |

| DGT share move (6 May 2026) | +22.4% |

DGT shares surged 22.4% on the day, recovering to a year-to-date gain of 4.7%. The gearing reduction to 17% materially improves financial flexibility heading into the SYD1 build, and the flagged distribution review adds a near-term income catalyst for REIT investors evaluating DGT on yield alongside growth.

Both announcements triggered sharp share price moves, but interpreting their durability requires familiarity with how infrastructure REITs report financial health. Three metrics matter most:

REIT valuation mechanics connect interest rate movements to unit prices through four distinct channels: the discount rate applied to future cash flows, the cost of debt capital, yield competition with government bonds, and the broader economic outlook signal; for DGT specifically, the gearing reduction to 17% materially reduces exposure to the cost-of-capital channel that has weighed on infrastructure REITs through the 2022-2025 rate cycle.

EBITDAF strips out depreciation and amortisation alongside finance costs and tax, producing a cleaner measure of operating performance for capital-intensive infrastructure businesses where asset bases are large and long-lived. For Infratil, it is the primary earnings lens.

Contracted capacity (now exceeding 1GW for CDC) adds a layer of earnings visibility that quarterly guidance ranges cannot fully capture. When a hyperscaler commits to 555MW over a minimum 10-year term, the revenue line that flows into EBITDAF is locked in at contracted rates across a multi-year horizon. That is why Infratil’s FY28 EBITDAF projection (exceeding A$1 billion) carries more forward certainty than a typical corporate earnings forecast.

The share price reactions to both announcements were sharp, but the underlying demand signal is what makes them more than one-day events. AI-driven hyperscaler leasing is the structural force creating simultaneous opportunities for CDC (building new contracted capacity) and DGT (recycling offshore capital to fund domestic expansion into the same demand pool).

The counterparty behind CDC’s 555MW deal is described across all available coverage as a “US investment-grade hyperscaler,” a designation that points toward the small group of cloud and AI infrastructure operators whose capital deployment cycles now drive data centre construction globally.

CDC’s undisclosed counterparty is consistently described as a “US investment-grade hyperscaler”, reinforcing the quality of the contracted revenue stream underpinning the 1GW milestone.

Sector-wide capital deployment reinforces the theme:

NEXTDC’s debt syndication of $1.8 billion, committed by a consortium of eight major banks including all four Australian majors and closed within days of the CDC announcement, illustrates how broadly institutional lenders are now extending credit to the Australian data centre sector, with proceeds earmarked for growth capex rather than refinancing of existing obligations.

Supply constraints sharpen the picture. Tight vacancy rates and power grid access challenges across Australian metros mean new capacity commands premium contracted terms, which is precisely the position both CDC and DGT are building toward. These are demand-pull capacity builds anchored by institutional customers with decade-long commitments, not speculative supply additions.

The earnings trajectories presented by both companies are credible, but the gap between contracted capacity and delivered capacity contains genuine execution risk across three categories:

AEMO’s 2024 Integrated System Plan maps the transmission and generation investment required to absorb large new loads entering the National Electricity Market, with connection queue pressures for industrial-scale customers a documented constraint that directly shapes the staging decisions data centre operators must make when committing to multi-campus rollouts.

Infratil confirmed that no additional shareholder equity is required to fund CDC’s new capacity. Financing is expected to come through existing cash, committed debt, and further debt or hybrid instrument issuance. While the absence of equity dilution is positive, the capex range implies significant debt drawdown and hybrid issuance that will affect Infratil’s balance sheet through the FY27-FY28 period. Investors should monitor Infratil’s debt and hybrid instrument disclosures as the multi-campus build-out progresses.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding earnings guidance and capital expenditure are subject to market conditions and various risk factors.

The 6 May 2026 announcements from DGT and IFT mark a threshold. Australian digital infrastructure has moved from emerging sector curiosity to mainstream institutional asset class, with long-duration contracts and billion-dollar capex programmes now the baseline for participation.

The scale of the day’s activity tells the story on its own: 555MW contracted, US$750 million divested, 1GW total CDC capacity reached. Less than a decade ago, AirTrunk had not yet been founded. The pace of change has compressed a generation of infrastructure development into a handful of years.

Infratil reached all-time highs on 6 May 2026, reflecting market confidence in the CDC earnings trajectory and the structural demand thesis underpinning Australian data centre expansion.

The investment question that follows both announcements is whether earnings delivery against the FY28 guidance corridors, DGT’s FFO accretion from FY27 and Infratil’s EBITDAF exceeding A$1 billion in FY28, justifies the valuations implied by the day’s share price moves. The 6 May 2026 announcements are a reference point that investors in both DGT and IFT will return to when assessing whether management delivered on the ambition articulated today.

For investors wanting to model the earnings trajectory against Infratil’s implied CDC valuation, our deep-dive into CDC’s DCF valuation methodology examines how the A$15 billion enterprise value is constructed, why the DCF conservatively excludes pipeline beyond 2040, and what the A$500 million quarterly stake revaluation implies about the market’s view of contracted capacity as a valuation anchor.

CDC Data Centres signed a 555MW contracted capacity deal with a US investment-grade hyperscaler on 6 May 2026, covering a minimum 10-year term with renewal options extending to 30 years, making it the largest data centre contract in Australian history by committed power.

DigiCo (ASX: DGT) sold its Chicago CHI1 facility for US$750 million, reducing its gearing from 36% to approximately 17% post-completion and freeing around A$360 million in net cash proceeds to fund its 88MW SYD1 facility in Sydney.

EBITDAF stands for earnings before interest, tax, depreciation, amortisation, and fair value movements; Infratil uses it as the primary earnings measure for CDC because it strips out non-cash accounting items and produces a cleaner picture of operating performance for capital-intensive, long-lived infrastructure assets.

The main risks include power grid access constraints through AEMO's connection queue process, planning and environmental approvals such as the EPBC Act review facing DGT's SYD1 facility, and capital execution risk given Infratil's A$3.8 billion to A$4.2 billion FY27 capex commitment across multiple campuses simultaneously.

Infratil left FY27 EBITDAF guidance unchanged at A$680 million to A$720 million but projected FY28 EBITDAF to exceed A$1 billion, with annualised contracted EBITDAF estimated at approximately A$2 billion once the 555MW contract is fully deployed post-FY28.