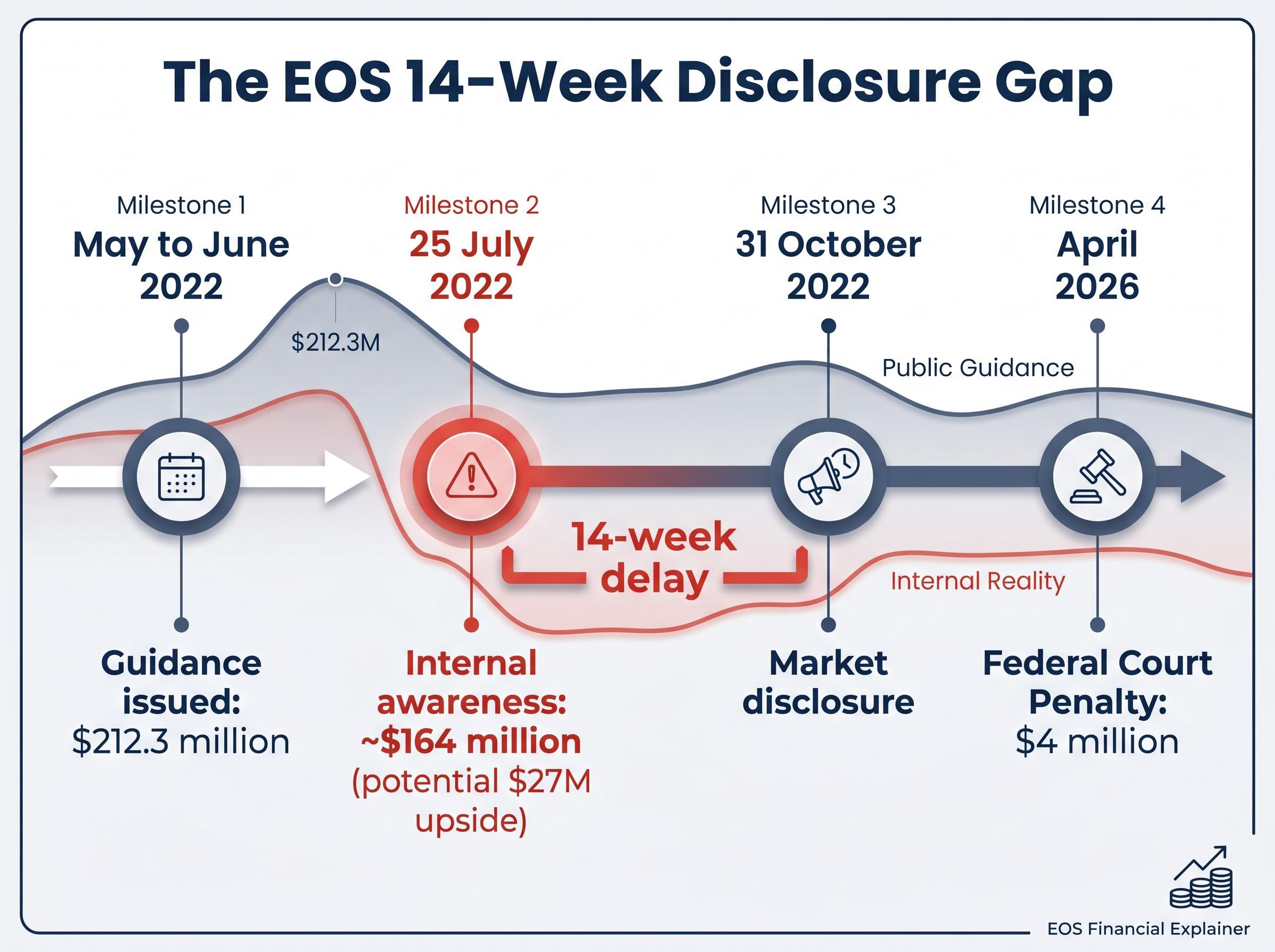

A 14-week silence. That is how long Electro Optic Systems (EOS) waited before telling the market its 2022 revenue would fall roughly $48 million short of its own guidance. In April 2026, the Federal Court responded with a $4 million penalty.

The EOS case is the clearest recent illustration of what happens when an ASX-listed company fails its continuous disclosure obligations. But the legal proceedings against former CEO Dr Ben Greene personally, separate from the corporate penalty, signal something broader: ASIC is no longer treating disclosure failures as a corporate governance abstraction. It is pursuing individuals.

What follows explains exactly how continuous disclosure obligations work under Australian law, what triggers them, where the legal exceptions sit, why individual executives are now personally exposed, and what retail investors can do when a company gets it wrong.

The rule every ASX investor should understand

Listed companies on the ASX operate under a disclosure system designed around a single principle: investors deserve timely access to information that could change their decisions. The legal machinery behind that principle flows from two instruments working together.

- ASX Listing Rule 3.1: Requires immediate disclosure of any information that a reasonable person would expect to have a material effect on the price or value of an entity’s securities.

- Corporations Act s 674(2): Provides ASIC with the statutory enforcement mechanism, applying to information that meets a specific materiality standard.

“Information that a reasonable person would expect reasonable investors to attach material trading significance.”

Listing Rule 3.1 sets the trigger. Section 674 gives ASIC the power to enforce it through civil penalty proceedings. Both must be understood as a linked system rather than alternatives.

ASIC’s Regulatory Guide 62 sets out the regulator’s interpretation of continuous disclosure obligations under the Corporations Act and ASX Listing Rules, covering how materiality is assessed, when the obligation to disclose attaches, and the standards companies are expected to meet in practice.

The penalties reflect how seriously Australian law treats failures in this system. As of 2026, civil penalties reach up to $1.11 million per contravention for individuals and up to $11.1 million for corporate bodies, indexed annually. Every ASX-listed company an investor holds shares in is bound by this framework, and understanding what it actually requires helps investors recognise when a company’s announcement pattern may indicate a disclosure problem, not just operational turbulence.

When big ASX news breaks, our subscribers know first

What actually triggers the obligation to disclose

The disclosure clock does not start when a board meets, when a CEO decides to act, or when a company prepares a formal ASX announcement. It starts when the company internally knows, or should know, of information that meets the materiality test.

The EOS case provides a concrete illustration of how this plays out in practice.

| Date | Event | Significance |

|---|---|---|

| May to June 2022 | EOS issued guidance that revenue would meet or surpass $212.3 million | Market expectation set publicly |

| 25 July 2022 | EOS internally aware revenue would likely reach approximately $164 million (with potential upside of $27 million) | Materiality threshold crossed; disclosure obligation triggered |

| 31 October 2022 | EOS disclosed the revenue downgrade to the market | 14-week delay from internal awareness to public disclosure |

The Federal Court declared EOS in contravention of s 674A(2) from 25 July 2022 through to 31 October 2022. The obligation attached at the point of internal awareness, not at the point of formal board sign-off.

What “immediately” actually means in practice

Regulators and courts treat the immediacy requirement as a matter of hours to days, not weeks, once information is sufficiently definite to be material. The EOS 14-week delay set a stark benchmark for what clearly constitutes a breach.

Companies facing the tension between immediacy and the operational time needed to prepare a proper announcement have a compliant mechanism available: requesting a trading halt from ASX. A trading halt pauses trading while the company prepares and releases its disclosure, satisfying the obligation without forcing a poorly drafted announcement.

Knowing that the obligation attaches at the point of internal awareness helps investors interpret guidance updates more critically, particularly when company language suggests the issue was known well before the announcement date.

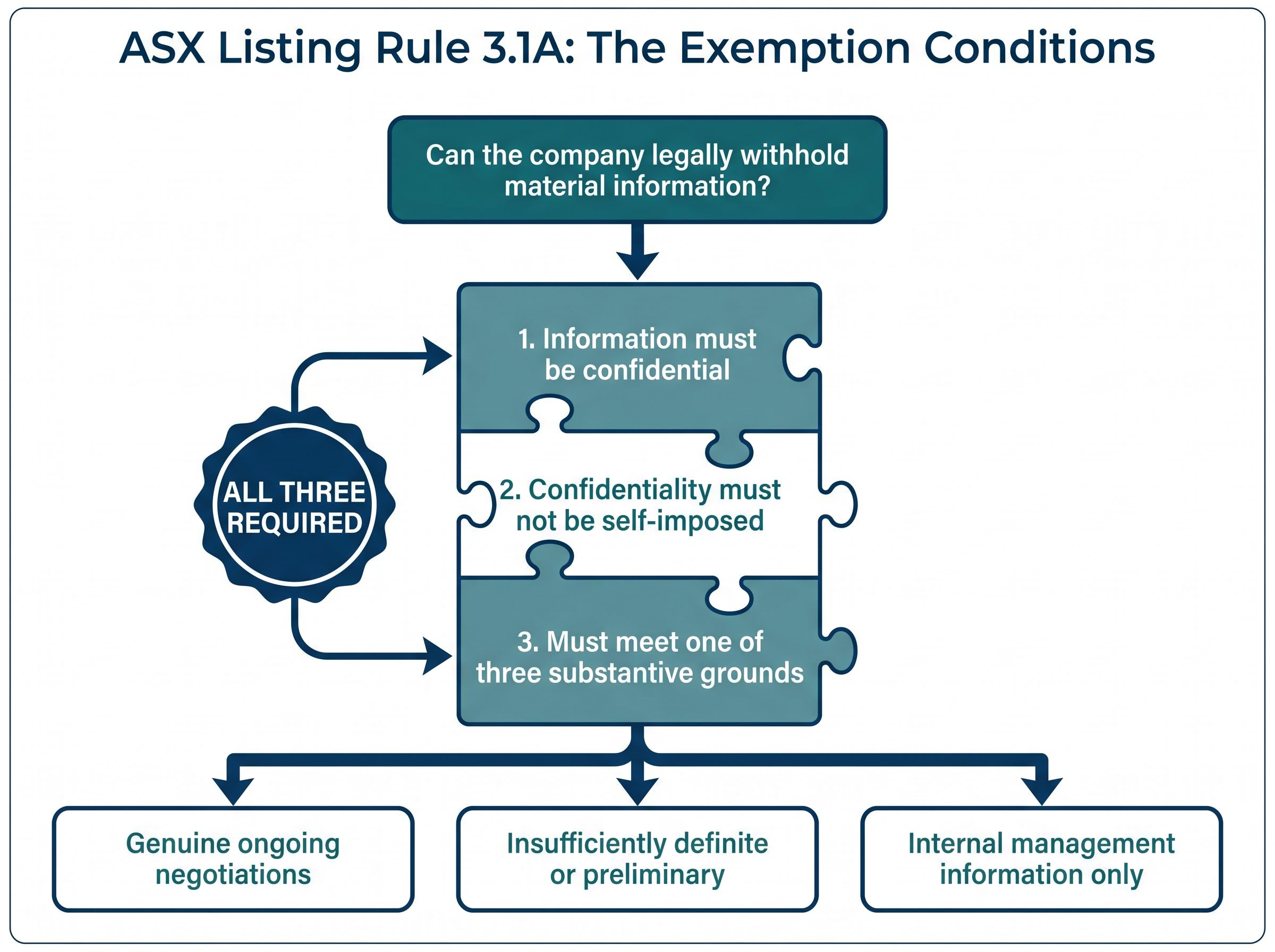

When companies are legally permitted to stay silent

The disclosure obligation is not absolute. ASX Listing Rule 3.1A provides a narrow release valve, but the conditions are strict and cumulative. All three must be satisfied simultaneously for an exemption to apply:

- The information must be confidential.

- The confidentiality must not be self-imposed by the company.

- One of three substantive grounds must be met.

The three substantive grounds within the third condition are:

- Genuine ongoing negotiations, where premature disclosure would prejudice the outcome.

- Insufficiently definite or preliminary information, where the data has not reached the point of materiality.

- Internal management information only, which is not market-sensitive.

Courts interpret these carve-outs narrowly. The exemption does not extend to information that has become sufficiently definite to be material, regardless of whether a formal board process has been completed. Practitioner consensus holds that the carve-outs cannot be used as a default strategy for managing uncomfortable disclosures.

Understanding the narrow scope of these exemptions helps investors evaluate whether a company that delayed an announcement had a legitimate reason or was exploiting ambiguity. That distinction is directly relevant to assessing governance quality.

Why ASIC is now going after individual executives, not just companies

The $4 million corporate penalty against EOS was the headline. The proceedings against its former CEO personally represent the structural shift.

ASIC pursues individuals through two primary mechanisms:

- Section 79 (accessorial liability): Applies to any person knowingly concerned in a company’s contravention of s 674, including by aiding, abetting, or being involved in the breach.

- Section 180 (care and diligence): Requires directors and officers to exercise reasonable care and diligence, which includes maintaining oversight of disclosure governance, not simply delegating to compliance teams.

The proceedings against Dr Ben Greene, filed in October 2025 with a hearing scheduled for Q3 2026 (ASIC MR 25-110MR), allege breaches of both s 180 and s 674. ASIC’s case centres on the allegation that Dr Greene had access to material 2022 revenue data and failed to ensure it was escalated through appropriate internal channels to the board and then to the market.

ASIC Chair Joe Longo characterised timely and accurate market updates as a “fundamental duty” following the EOS corporate penalty outcome.

The personal penalty exposure for individuals, up to $1.11 million per contravention, combined with the public profile of enforcement proceedings, creates significant personal stakes for executives beyond corporate sanctions.

The EOS proceedings are not an isolated development; the Federal Court’s ruling in ASIC v Bekier established that executive liability under section 180 extends to any failure to escalate material compliance risks to the board, not just failures in financial reporting or formal disclosure processes.

When executives face personal liability, the incentive structure around disclosure decisions changes materially. This enforcement direction signals that retail investors can expect boards to treat disclosure governance as a board-level responsibility, not a compliance department function.

What retail investors can do when a company fails its disclosure obligations

Understanding the framework matters. Knowing what to do when it fails matters more.

Retail investors have two main pathways. The first is reporting to ASIC via ASIC Connect, which is free to use. ASIC does not provide direct compensation to complainants, but treats credible reports as potential investigation triggers, particularly where the complaint suggests systemic non-disclosure or significant market impact.

The second is participating in class action proceedings, which seek compensation for financial losses caused by disclosure failures. The relevant legal bases include s 1041H (misleading conduct in financial markets, where delayed or incomplete disclosure caused investors to trade at artificial prices) and s 1317H (compensation orders of up to 125% of proven loss in appropriate cases).

For investors who suspect a company has breached its disclosure obligations, the practical steps are:

- Report the suspected breach to ASIC via ASIC Connect.

- Contact a plaintiff law firm promptly, as class action registration deadlines can be time-sensitive.

- Preserve records of purchase price and announcement dates for any affected holdings.

How class actions work for retail investors

Class actions are typically run by plaintiff firms such as Maurice Blackburn and Slater and Gordon on a no-win, no-fee basis, making them accessible to individual retail investors without upfront legal cost.

Compensation claims carry practical challenges. Investors must establish causation, demonstrating that the disclosure failure, not general market movements, caused the specific loss. In affirmative misstatement cases, proving reliance on a specific statement adds complexity. All claims are subject to a six-year limitation period.

Class action settlements typically require opt-in or opt-out decisions, and default positions vary by case structure. Investors should monitor communications from plaintiff firms actively rather than assuming automatic inclusion.

The a2 Milk Company’s $62 million disclosure-related class action settlement, arising from guidance issued during the FY21 period and fully covered by insurance, illustrates both the potential scale of compensation outcomes and the practical reality that many settlements carry no admission of liability.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

How to read ASX announcements as a more informed investor

The legal framework above translates into a practical reading habit that any ASX investor can apply.

When companies release negative guidance updates, specific language often reveals the internal timeline. Phrases such as “the board became aware of” or “following a review completed on” can indicate whether the gap between internal awareness and public disclosure was appropriate. These are worth reading closely.

Three announcement signals worth tracking:

- Internal timeline language: Phrases disclosing when the board or management first became aware of the issue. A long gap between that date and the announcement date warrants scrutiny.

- Sector-specific scrutiny: Companies in volatile sectors, including defence, technology, resources, and biotech, face particular ASIC attention because forecasting uncertainty does not excuse delay once information is sufficiently definite.

- ASIC’s enforcement page (asic.gov.au): Periodic checks for portfolio companies operating in these sectors provide an early signal of regulatory attention.

The EOS benchmark is instructive: a $48 million revenue gap between guidance and actuals, combined with a 14-week internal awareness window before disclosure, is what a clear breach looks like. A significant share price drop coinciding with a guidance downgrade is not, by itself, evidence of a breach, but the combination of a large price movement and language suggesting extended internal awareness is a governance signal worth investigating.

Investors who read announcements critically and monitor ASIC’s enforcement record are better positioned to make informed hold, sell, or escalate decisions rather than relying solely on company communications.

A tougher disclosure era for ASX executives is already underway

The EOS corporate penalty of $4 million in April 2026 and the ongoing individual proceedings against Dr Ben Greene represent a verified enforcement signal, not a theoretical shift in ASIC’s posture.

Three things matter for retail ASX investors. First, the disclosure obligation triggers at the point of internal awareness, not at the point of public announcement. The EOS timeline, where the company knew of a material revenue shortfall 14 weeks before disclosing it, established that threshold clearly. Second, the exemptions that permit silence are narrow and cumulative; they protect legitimate business interests in specific circumstances, not corporate convenience. Third, when the obligation is breached, recourse exists through ASIC reporting and class action pathways, with compensation mechanisms that can reach up to 125% of proven loss.

ASIC’s pursuit of individual executives is the clearest signal that continuous disclosure obligations are a personal responsibility for every director and officer of an ASX-listed company. The consequences now extend beyond the corporate entity to the individual.

ASIC’s regulatory posture toward ASX-listed entities has intensified on multiple fronts simultaneously: the same month the EOS corporate penalty was issued, ASIC released its Final Report on ASX Limited’s governance and risk management, requiring a $150 million capital charge and a hard deadline for program reset, signalling that enforcement attention extends across the full breadth of market infrastructure.