Palantir just posted 85% revenue growth in a single quarter, paired with a Rule of 40 score that management compared not to software peers but to NVIDIA and Micron. That framing alone signals how dramatically the company’s self-positioning has shifted.

The Q1 2026 results, released 4 May 2026, arrived at a moment when investors are actively searching for which AI software companies can translate infrastructure spending into durable revenue acceleration. Palantir delivered revenue of $1.63 billion against a Wall Street consensus of $1.54 billion, and adjusted earnings per share of $0.33 versus the $0.28 expected. What follows is a breakdown of what drove the growth at the segment level, what the raised full-year guidance of $7.65 billion implies for the company’s trajectory, and how investors should interpret the post-earnings stock reaction.

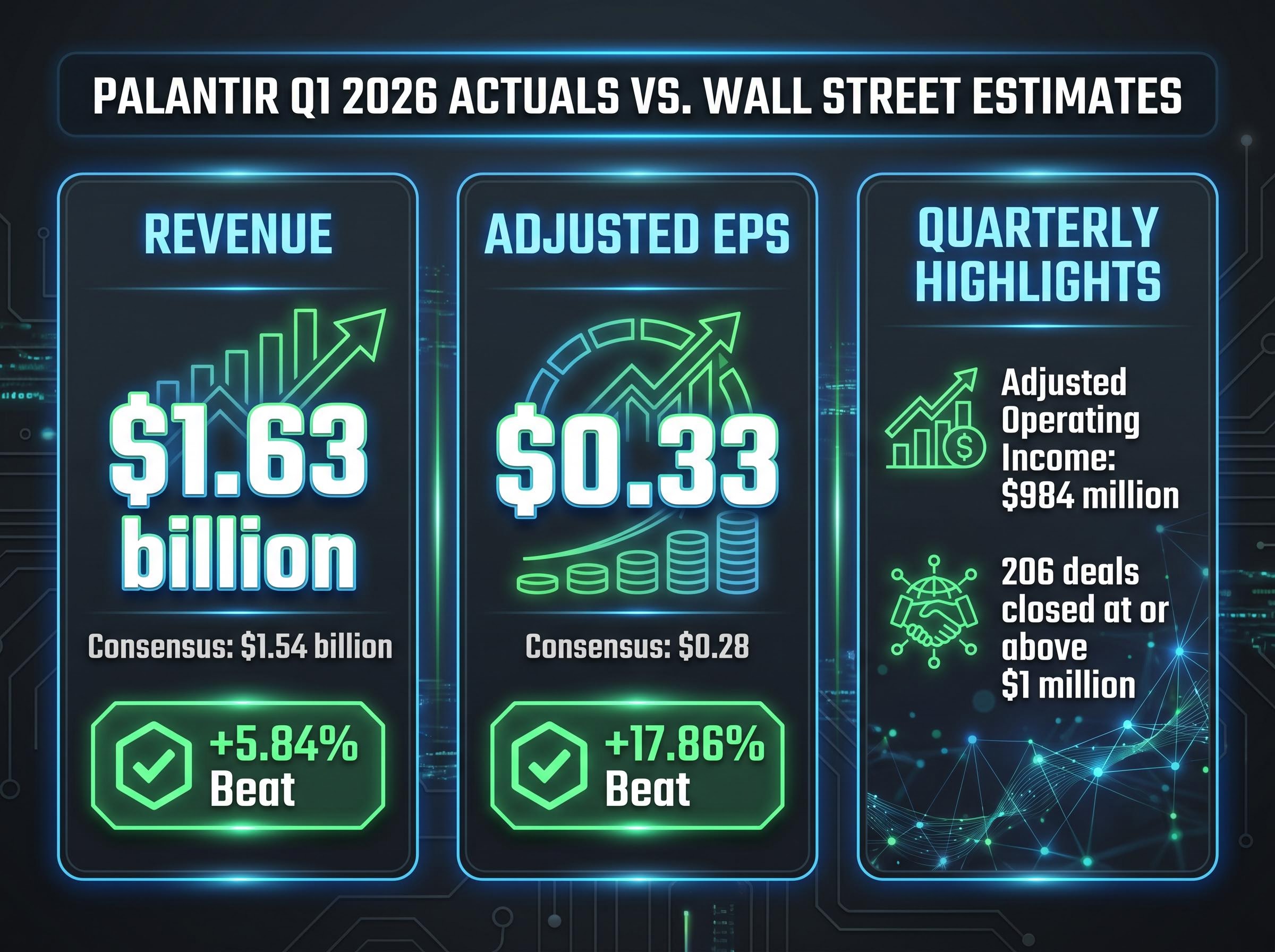

Q1 2026 by the numbers: how far Palantir beat expectations

The consensus miss was not marginal. Revenue exceeded estimates by 5.84%, and adjusted EPS beat by 17.86%, a dual surprise that implies Wall Street was meaningfully undermodelling the company’s current growth rate.

85% year-over-year revenue growth, the strongest expansion rate Palantir has recorded since its 2020 direct listing.

Adjusted operating income reached $984 million, reinforcing that the growth arrived alongside expanding profitability rather than at its expense. The quarter also produced 206 deals closed at or above $1 million, a figure that suggests the acceleration is broadly distributed across the customer base rather than concentrated in one or two outsized contracts.

A beat of this magnitude at this revenue scale is uncommon in enterprise software. For investors evaluating the stock, the gap between expectations and actuals raises a direct question: how far behind the curve are current analyst models?

| Metric | Q1 2026 Actual | Consensus Estimate | Beat |

|---|---|---|---|

| Revenue | $1.63 billion | $1.54 billion | +5.84% |

| Adjusted EPS | $0.33 | $0.28 | +17.86% |

| Adjusted Operating Income | $984 million | N/A | N/A |

When big ASX news breaks, our subscribers know first

What powered the growth: U.S. commercial and government segment breakdown

U.S. total revenue grew 104% year-over-year, making domestic operations the primary engine behind the consolidated 85% figure. The government and commercial segments both contributed, but the story each tells is different.

U.S. government revenue reached $687 million, up 84% year-over-year. A concrete anchor for that figure is the Department of Homeland Security (DHS) contract awarded in February 2026, worth up to $1 billion, to deploy AI and data analytics platforms across multiple agencies. That single award illustrates the scale of federal AI procurement now flowing through Palantir’s pipeline.

Federal AI procurement has accelerated sharply in 2026, driven in part by the Pentagon assembling a seven-vendor defence AI coalition after the collapse of its Anthropic contract in January, creating concentrated contract flow toward vendors with established government cloud infrastructure and cleared deployment capabilities.

DHS contract: up to $1 billion, awarded February 2026, deploying AI and data analytics across multiple federal agencies.

The more structurally significant number, however, sits on the commercial side. U.S. commercial revenue grew 133% year-over-year, the standout metric of the entire quarter.

- U.S. total revenue growth: 104% year-over-year

- U.S. commercial revenue growth: 133% year-over-year

- U.S. government revenue: $687 million, up 84% year-over-year

That 133% figure matters most to the long-term investment thesis because it reflects enterprise adoption of the Artificial Intelligence Platform (AIP), Palantir’s commercial AI product, beyond its traditional government base. If the government segment demonstrates contract durability, the commercial segment demonstrates addressable market expansion.

Understanding the Rule of 40 and why Palantir is reframing its peer group

The Rule of 40 is a benchmark widely used to evaluate software companies. It adds a company’s revenue growth rate to its adjusted operating margin; a combined score above 40 is generally considered strong, indicating that a business is balancing growth and profitability effectively.

The Rule of 40 benchmark adds a company’s revenue growth rate to its free cash flow or operating margin, with scores above 40 commanding materially higher revenue multiples; Bain and Company data from April 2026 shows each 10-point improvement above 40 added 1.1x EV/Revenue multiple, up from 0.8x in Q1 2023, meaning the market is now pricing Rule of 40 outperformance more aggressively than at any point in the prior decade.

Palantir’s score: 145%.

The calculation:

- Revenue growth rate: 85%

- Adjusted operating margin: 60%

- Combined Rule of 40 score: 85% + 60% = 145%

A score above 100 is exceptionally rare in software. CEO Alex Karp used the earnings release to frame that rarity in specific competitive terms.

“Palantir’s Rule of 40 score has soared to 145%. We have shattered the metric, a feat matched only by other fellow AI infrastructure companies: NVIDIA, Micron and SK hynix.”

The peer comparison is deliberate. By benchmarking against AI hardware and infrastructure names rather than enterprise software companies such as Snowflake or Databricks, Karp is signalling that Palantir views itself as an AI infrastructure layer, not a traditional SaaS (software as a service) vendor. For investors, this reframing directly affects which valuation framework applies: AI infrastructure multiples versus enterprise software multiples produce materially different price targets.

Full-year 2026 guidance raised to $7.65 billion, and what the upgrade signals

Management raised full-year 2026 revenue guidance to a range of $7.650 billion to $7.662 billion, against a prior Wall Street consensus of approximately $7.2 billion. That gap is not incremental. The updated range implies full-year growth of approximately 71%, a 10-percentage-point increase relative to the roughly 61% growth rate implied by prior quarter guidance.

The revision was not limited to the topline. Full-year adjusted operating income guidance was set at $4.440 billion to $4.452 billion, and adjusted free cash flow guidance was raised to a range of $4.2 billion to $4.4 billion. Management attributed the upgrade to growing confidence in accelerating U.S. market demand.

AI investment in GDP accounts contributed approximately 1 percentage point of Q1 2026 growth, with high-tech categories including IT equipment, data centres, software, and R&D being the primary driver of the rebound from 0.5% in Q4 2025, providing the macro-level confirmation that enterprise AI platform spending is translating into measurable economic output rather than remaining confined to balance sheet commitments.

| Full-Year 2026 Guidance | Updated Range | Prior Consensus / Guidance |

|---|---|---|

| Revenue | $7.650B – $7.662B | ~$7.2B (consensus) |

| Adjusted Operating Income | $4.440B – $4.452B | N/A |

| Adjusted Free Cash Flow | $4.2B – $4.4B | N/A |

Guidance upgrades that raise revenue, operating income, and free cash flow simultaneously are materially different from topline-only revisions. For investors, the signal is that management sees margin expansion and cash generation as durable alongside the growth acceleration, not as a trade-off against it.

How the market reacted, and what investors should watch next

The initial reaction was caution. After-hours trading on 4 May saw PLTR decline approximately 3% before stabilising. By the close on 5 May, the stock had recovered to $146.03, up 1.36% from the prior close of $144.07, on volume of 63,559,848 shares.

That sequence, a dip followed by a modest recovery rather than a sharp rally, suggests the market digested strong results against a stock that has already priced in significant growth expectations. No verified analyst upgrades, downgrades, or price target changes had been confirmed as of 5 May 2026. Bloomberg, Reuters, and Benzinga remain the sources to monitor as Wall Street analyst notes emerge.

What to watch heading into Q2 2026

Three forward-looking signals will determine whether Q1 represented an inflection point or an already-embedded expectation:

- U.S. commercial revenue growth trajectory: whether the 133% rate sustains above 100% into Q2

- AIP enterprise contract velocity: the pace and scale of new platform deals beyond the existing government base

- Rule of 40 sustainability: whether the 145% score holds above 100 as the revenue base scales and comparisons steepen

No analyst consensus updates for Q2 have been verified; these remain watch items rather than confirmed data points.

Palantir’s AI infrastructure bet is paying off, but the valuation question remains open

Three signals defined Q1 2026: a consensus beat broad enough to question current analyst models, a 133% U.S. commercial growth rate that validates enterprise AI platform adoption, and a guidance revision that raised the full-year growth trajectory by 10 percentage points to 71%.

The unresolved tension is equally clear. Record growth and a 145% Rule of 40 score arrived alongside a stock that opened 5 May only modestly higher, reflecting a valuation that has already embedded substantial growth expectations. Whether that valuation is justified depends on what comes next.

Consumer spending deceleration to 1.6% annualised in Q1 2026, combined with a geopolitical energy shock lifting headline PCE inflation 0.7% month-over-month in March, creates a macro backdrop that complicates the Federal Reserve’s rate path and adds a layer of cyclical risk to the growth assumptions embedded in Palantir’s elevated valuation multiples.

Q2 2026 results will reveal whether this quarter marked the beginning of a sustained acceleration or the point at which the growth rate peaked. Investors tracking Palantir stock will find the answer in the same three metrics: commercial growth, contract velocity, and whether profitability scales with revenue or compresses against it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including management guidance, are subject to change based on market developments and company performance.