BlackRock Raises AI and Tech Decoupling to Top Risk Tier

19 hrs ago

Westpac has reported a 3% lift in statutory net profit to $3.4 billion for the first half of 2026, alongside a fully franked interim dividend of 77 cents per share, as the bank’s balance sheet expands at its fastest clip in several years.

Released on 5 May 2026, the 1H26 result lands at a moment when Australian bank stocks have already repriced significantly. WBC shares are up approximately 19% over the past 12 months against a 7% gain for the ASX 200. The result therefore arrives under scrutiny: investors want to know whether the fundamentals have kept pace with the share price.

What follows decodes the headline numbers, examines capital strength and credit quality, unpacks segment-level lending growth, and assesses whether the Westpac half-year results give investors reason to hold, add, or reassess their position.

The headline reads well. Statutory net profit of $3.4 billion, up 3% on 1H25, with a fully franked interim dividend of 77 cents per share.

Headline result: Westpac reported statutory net profit of $3.4 billion and declared a fully franked interim dividend of 77 cents per share for 1H26.

The year-on-year comparison flatters the trajectory. Measured against the prior half (2H25), profit fell 5%, a detail that matters for investors tracking the direction of momentum rather than the distance from the same period last year.

Cash profit excluding notable items came in at $3.5 billion, up 1% on 1H25, the cleaner operational measure stripped of one-off items. Return on equity printed at 9.6%.

| Metric | 1H25 | 2H25 | 1H26 |

|---|---|---|---|

| Statutory net profit | $3.3B | $3.6B | $3.4B |

| Cash profit (ex notable items) | $3.5B | — | $3.5B |

The dual comparison is the most useful framing. Year-on-year, the result represents progress. Half-on-half, it reads closer to a plateau. Both readings carry weight depending on the investor’s time horizon.

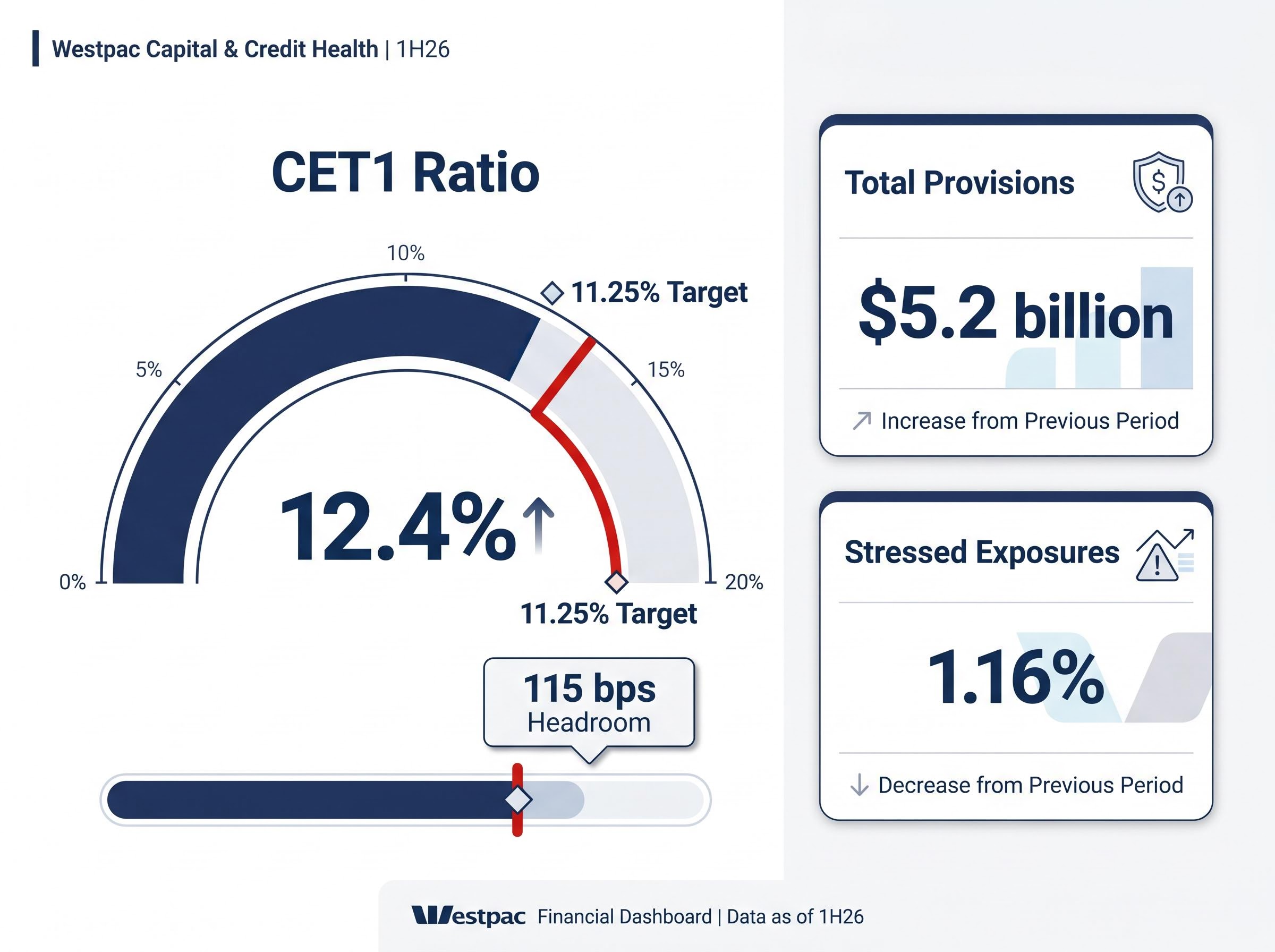

Westpac’s Common Equity Tier 1 (CET1) ratio sits at 12.4%, comfortably above the bank’s own internal target of 11.25%. That 115 basis points of headroom is the mechanical foundation behind the fully franked dividend.

The CET1 ratio measures a bank’s core equity capital as a percentage of its risk-weighted assets. It is the primary gauge regulators and investors use to assess whether a bank holds enough capital to absorb losses while continuing to pay dividends. The Australian Prudential Regulation Authority (APRA) sets a regulatory minimum, and banks set their own internal targets above that floor. A CET1 ratio well above both thresholds signals that a dividend is being paid from a position of strength, not stretched balance sheet capacity.

APRA’s capital adequacy standards set a minimum CET1 ratio of 4.5% for authorised deposit-taking institutions, with additional capital conservation buffers layered above that floor, which means Westpac’s 12.4% reading sits well clear of both the regulatory minimum and its own internal target of 11.25%.

At 12.4%, Westpac sits above both the APRA minimum and its own 11.25% target. The three capital and credit metrics worth tracking:

The provisioning increase reflects proactive risk management rather than deterioration. Stressed exposures moving lower reinforces that credit quality remains sound, even as the bank builds reserves against potential energy-related disruption.

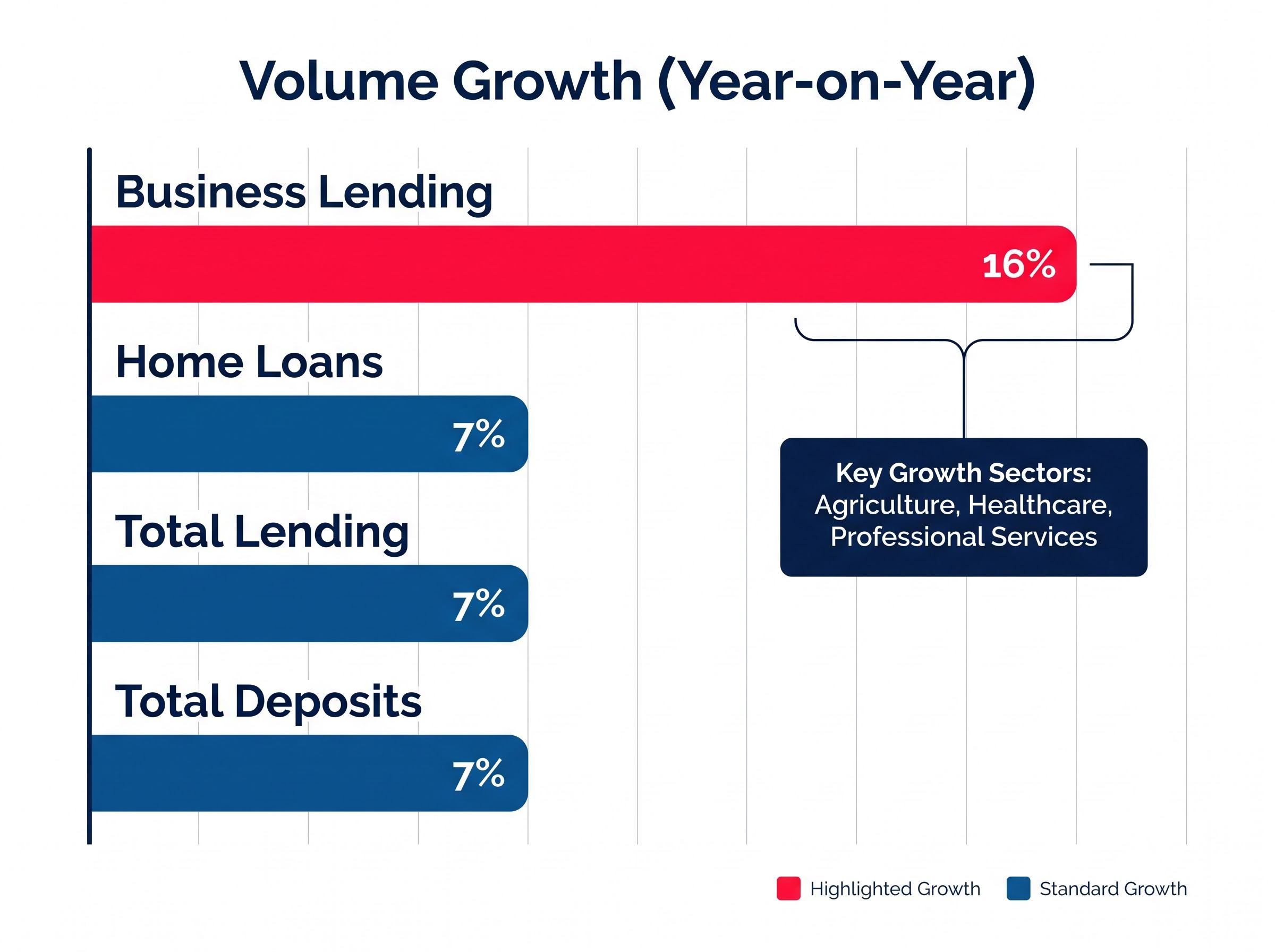

The standout figure in the result sits in business banking.

Westpac’s business lending grew 16% year-on-year in 1H26, the strongest growth rate across the bank’s major lending segments.

That 16% figure reflects targeted expansion across three sectors that management identified as strategic priorities:

Australian home loan volumes grew 7% year-on-year, excluding the RAMS portfolio (a lower-cost distribution channel the bank has been winding down). Total lending and deposit volumes each rose 7% year-on-year, confirming the expansion is broad-based rather than concentrated in a single product line.

The RAMS portfolio sale, which will deliver an additional 22 basis points of CET1 capital on completion in 2H26, also required Westpac to absorb a $75 million post-tax transaction cost in the current half, which is why mortgage growth figures in this result are quoted excluding that channel.

Volume growth at this pace signals that Westpac is gaining market share in the current environment. For the revenue outlook, this matters: even if net interest margins remain under pressure from competitive pricing, higher volumes can offset margin compression and sustain income growth.

Operating expenses declined versus 2H25, a result management attributed to productivity initiatives rather than revenue compression. The near-term cost line is moving in the right direction.

The market’s attention, however, sits further forward.

UNITE is Westpac’s operational simplification programme, now in active implementation. Its stated objectives include:

Chief Executive Officer Anthony Miller framed cost management as a priority that must be balanced with continued customer support through a period of economic uncertainty. The message signals that expense discipline is not coming at the cost of service delivery or investment in growth capabilities.

For investors assessing the medium-term earnings trajectory, the pace and credibility of UNITE execution carries more weight than any single half’s expense figure. It is the clearest forward signal on whether the bank’s efficiency ratio improves structurally over the next two to three years.

The share price tells one story. The return on equity tells another.

| Measure | 12 months ago | Current | Gain |

|---|---|---|---|

| WBC share price | $32.45 | $38.50 | ~19% |

| ASX 200 | 8,158 | 8,730 | ~7% |

| Outperformance | ~12 ppts |

Approximately 12 percentage points of outperformance over a year is a strong outcome for a Big Four bank. The question is whether earnings quality has kept pace.

The current share price of $38.50 represents a pullback from its all-time high of $43.32 reached in February 2026, a decline that predates the 1H26 result and reflects a combination of sector-wide valuation concerns, one-off RAMS transaction costs, and analyst downgrades that built a cautious consensus heading into today’s announcement.

Return on equity at 9.6% sits below the level typically associated with cost-of-equity coverage for major Australian banks, where the threshold is commonly estimated in the 10-11% range. That gap suggests the market is pricing in future improvement, whether from UNITE-driven efficiency gains, volume-led revenue growth, or a more favourable rate environment, rather than rewarding current profitability alone.

Management flagged geopolitical tensions and energy cost pressures as the macro variables that represent the most material risks to the forward case. The RBA’s rate trajectory adds a further layer of uncertainty: rate cuts would support mortgage volumes and household credit quality, but could compress net interest margins further.

Westpac’s 1H26 result delivers genuine positives. Profit growth, a strong capital buffer, and broad-based lending momentum justify near-term confidence.

The three forward variables that will determine whether the re-rating holds are clear: RBA rate decisions and their impact on net interest margin; UNITE programme execution and its effect on the cost base; and any deterioration in household credit quality as cost-of-living pressures persist.

Sector-wide provisioning forecasts from Morgans project total Big Four provisions rising from approximately $2.4 billion in FY25 to $5.5 billion by FY27, a trajectory that frames Westpac’s $5.2 billion provision balance not as an isolated management decision but as part of a structural credit cycle shift playing out across the entire Australian banking sector.

Westpac’s performance will be benchmarked against Commonwealth Bank, ANZ, and NAB as the Big Four reporting season progresses. Institutional investors will use relative metrics across profitability, capital, and efficiency to assess whether Westpac’s premium is warranted.

The RBA’s February 2026 Statement on Monetary Policy outlined the conditions under which further rate adjustments would be considered, providing the baseline scenario that frames expectations for net interest margin trajectory across the major banks through the remainder of 2026.

The full investor presentation and financial schedules are available on the Westpac Investor Centre and the ASX announcements page for those seeking the complete detail behind the headline numbers.

For investors wanting the complete financial breakdown behind these headline figures, our full explainer on Westpac’s 1H26 financial results covers the pre-provision profit build, the cost-to-income ratio improvement to 51.7%, the institutional lending surge of 23%, and the revised GDP and cash rate forecasts that informed management’s provisioning decisions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Westpac reported statutory net profit of $3.4 billion for the first half of 2026, up 3% on the same period last year, and declared a fully franked interim dividend of 77 cents per share. Cash profit excluding notable items came in at $3.5 billion, up 1% on 1H25.

Westpac's Common Equity Tier 1 (CET1) ratio stands at 12.4%, which is 115 basis points above the bank's own internal target of 11.25% and well above the APRA regulatory minimum. This capital buffer provides a strong foundation for the fully franked dividend.

Westpac's business lending grew 16% year-on-year in 1H26, the strongest growth rate across the bank's major lending segments, with targeted expansion in agriculture, healthcare, and professional services. Australian home loan volumes also grew 7% year-on-year, excluding the RAMS portfolio.

UNITE is Westpac's operational simplification programme aimed at reducing legacy systems, deploying artificial intelligence, and achieving a structurally lower cost base over the medium term. For investors, the pace of UNITE execution is the clearest forward signal on whether the bank's efficiency ratio improves over the next two to three years.

Westpac shares have risen approximately 19% over the past 12 months against a 7% gain for the ASX 200, but return on equity sits at 9.6%, which is below the 10-11% range typically associated with cost-of-equity coverage for major Australian banks. The market appears to be pricing in future improvement from UNITE delivery, volume growth, and a more favourable rate environment rather than current profitability alone.