Barclays Warns of Prolonged Market Volatility Under New Fed Reality

Jun 27, 2026

Barclays has removed every expected 2026 Federal Reserve rate cut from its forecast, with economist Marc Giannoni publishing a revised outlook on Monday 4 May that places the next reduction at March 2027 at the earliest. The revision is conditional: Giannoni requires clear evidence that inflation is returning toward the Fed’s 2% target before any easing begins. The call lands as Brent crude trades above $112 per barrel, the 29 April Federal Open Market Committee (FOMC) statement signalled no near-term easing, and at least four major Wall Street peers have made near-identical moves in recent days. What follows is a breakdown of the specific drivers behind the Barclays call, how it sits within the broader repricing of rate expectations, and what the shift means for investors holding rate-sensitive assets.

The bridge between the oil call and the rate call is a set of inflation numbers that sit uncomfortably far from the Fed’s target.

| Metric | Prior Forecast | Revised Forecast | Change |

|---|---|---|---|

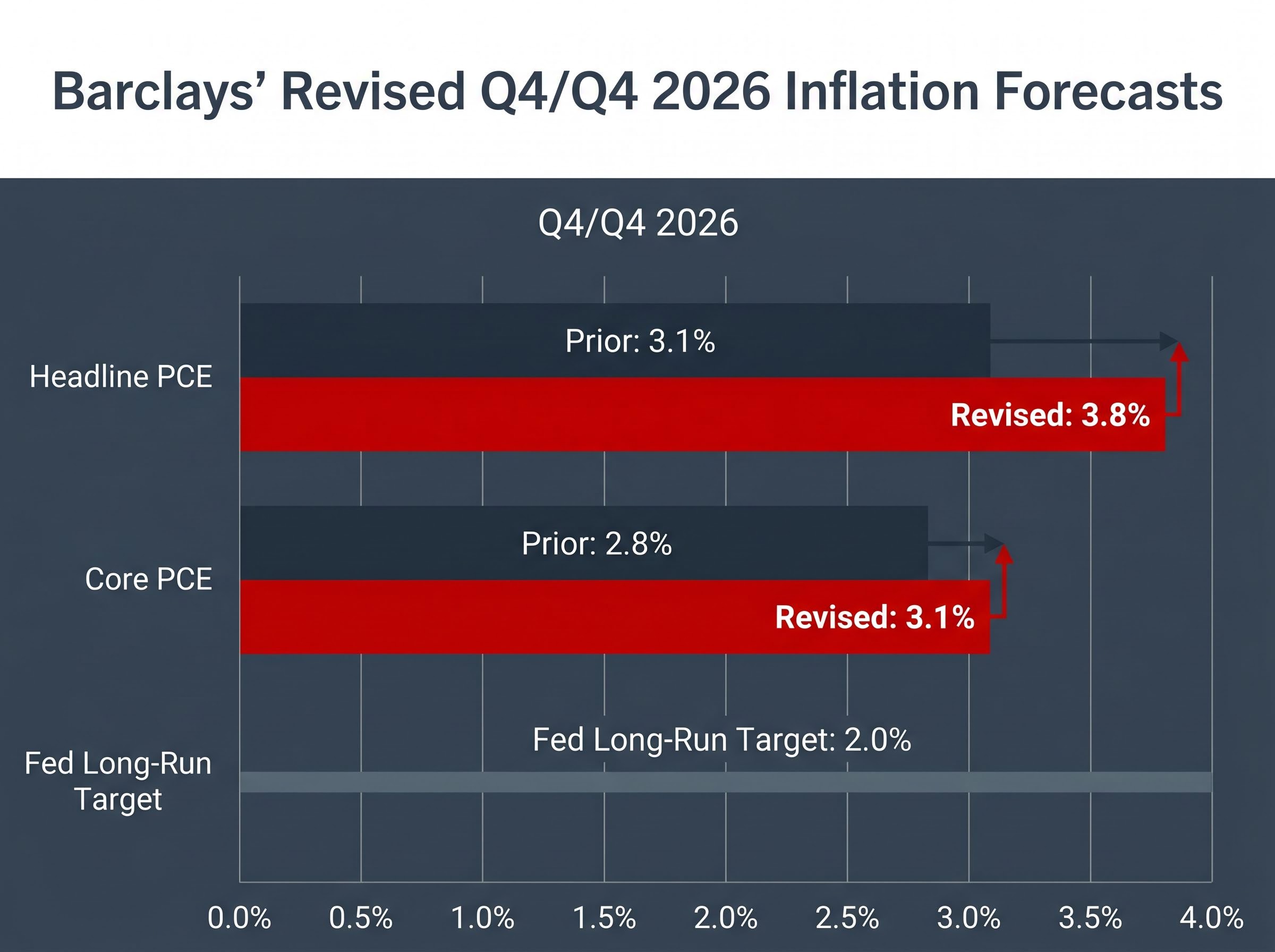

| Headline PCE (Q4/Q4 2026) | 3.1% | 3.8% | +0.7 percentage points |

| Core PCE (Q4/Q4 2026) | 2.8% | 3.1% | +0.3 percentage points |

| Fed Long-Run Target | 2.0% | 2.0% | Unchanged |

Headline PCE at 3.8% would run nearly double the Fed’s 2% target. Core PCE at 3.1% is projected to remain above 3% year-on-year through the end of 2026, with the monthly run-rate above 2.5% annualised according to Giannoni’s note.

Current data supports the direction. The Bureau of Economic Analysis (BEA) released March 2026 core PCE data on 30 April, showing approximately 2.8% year-on-year. The 29 April FOMC statement used explicit language: “policy to remain restrictive amid upside inflation risks from energy.”

San Francisco Fed President Mary Daly indicated in early May 2026 that core PCE remaining above 2.8% sustains a pause in easing into 2027.

With headline PCE forecast nearly double the target, the arithmetic leaves little room for the Fed to justify a cut before Q1 2027.

Giannoni’s revised forecast now projects a single 25 basis point cut in March 2027, replacing a prior baseline that included 2026 reductions. The shift rests on two named drivers:

The conditions attached to even the March 2027 move are explicit. Giannoni requires sustained evidence that core Personal Consumption Expenditures (PCE) inflation, the Fed’s preferred measure, is trending convincingly toward 2% before a cut becomes appropriate.

The April 29 FOMC decision held rates at 3.5%-3.75% against a backdrop of four dissenting votes, the broadest internal committee split in years, with hawks outnumbering the lone dovish dissenter three to one and the statement language itself becoming a point of public disagreement among committee members.

Barclays also flagged the Strait of Hormuz as an unresolved upside risk. If geopolitical escalation disrupts transit volumes through the strait, the resulting supply shock could delay even the 2027 move, pushing the first cut further into the second half of next year.

The specificity of the forecast, a single quarter with a single cut, makes it one of the most precisely hawkish calls published this cycle.

The rate call did not originate with the monetary policy team. It started with oil.

The relationship between oil price and recession risk has a consistent historical pattern: every major U.S. recession since 1973 has been preceded by an oil shock following the same structural transmission now visible in 2026, with reduced consumer disposable income, rising business input costs, and Fed rate pressure operating simultaneously.

Barclays’ energy analysts revised their crude price baseline in early May 2026, and the numbers fed directly into the macro forecast. The table below shows the updated projections across both benchmarks.

| Quarter | Brent Forecast | WTI Forecast | Key Driver |

|---|---|---|---|

| Q2 2026 | $115/barrel | $105/barrel | Strait of Hormuz risk premium, OPEC+ cuts |

| Q3 2026 | $105-$110/barrel | $98-$100/barrel | Gradual supply normalisation |

| Q4 2026 | $100/barrel | $93/barrel | Demand moderation, partial de-escalation |

| Full-Year Average | $100/barrel | $93/barrel | Elevated baseline vs. prior $95 estimate |

As of 4 May, Brent spot sits at $112.28, already above the full-year average. Goldman Sachs has modelled a scenario where Brent peaks near $120 in Q3 2026 if Hormuz transit volumes drop materially, with a potential 5-7 million barrels per day shortfall.

Headline PCE is affected directly by energy prices; when petrol and heating costs rise, the index moves immediately. Core PCE, which strips out food and energy, is affected indirectly, but the channel is real. Transportation costs, packaging, and goods production all carry energy inputs. When Brent sustains above $110, those costs bleed into the prices consumers pay for everything from groceries to medical services.

This pass-through is what pushed Barclays’ core PCE forecast 0.3 percentage points higher than its prior estimate, a revision large enough to change the rate call entirely.

Federal Reserve research on oil price pass-through quantifies both the direct and indirect channels through which crude price increases reach non-energy consumer prices, finding that sustained elevation in oil costs bleeds into goods and services categories well beyond transport and fuel within two to three quarters.

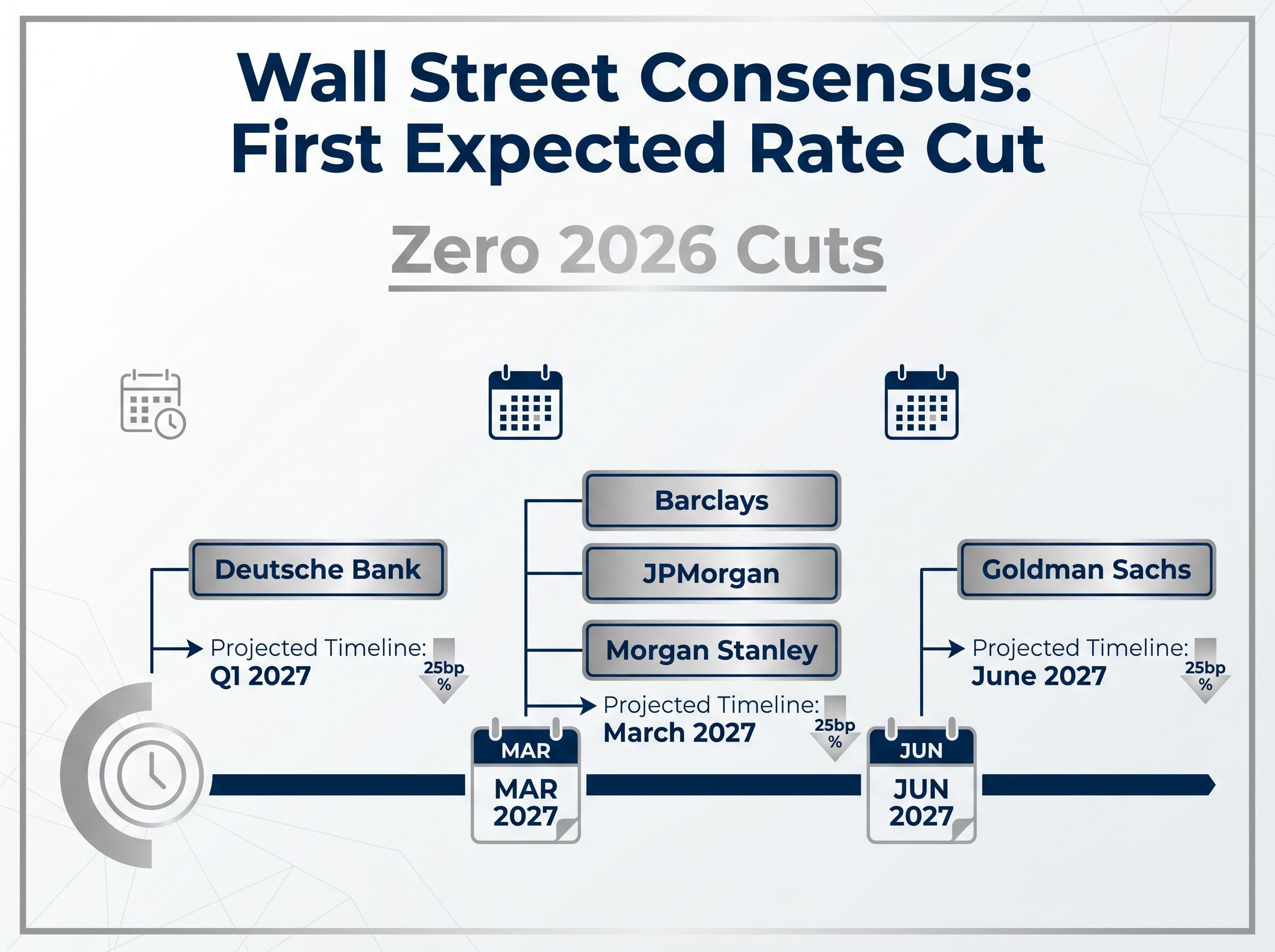

The Barclays revision is not an outlier. Four other major banks have published similar moves in late April and early May.

| Institution | 2026 Cut Expectation | First Expected Cut | Key Driver Cited |

|---|---|---|---|

| Barclays | Zero | March 2027 (25bp) | Oil baseline revision, labour market strength |

| Goldman Sachs | Zero (base case) | June 2027 (25bp) | Sticky core PCE, labour resilience |

| JPMorgan | Zero | March 2027 (25bp) | Headline PCE risks from Brent above $110 |

| Morgan Stanley | Zero | March 2027 (25bp) | Energy pass-through to core; 3.0% core PCE forecast |

| Deutsche Bank | Zero | Q1 2027 (25bp) | Strait of Hormuz risk, delayed pivot |

The alignment is striking. Five institutions, publishing independently within a two-week window, arrived at the same conclusion: no 2026 cuts, first move in Q1 2027.

Two data points add nuance to the consensus:

Barclays also trimmed its 2026 GDP forecast to 2.1%, down 0.3 percentage points from its prior estimate, consistent with the growth cost of a prolonged restrictive rate environment.

The repricing showed up across asset classes on 4 May.

Rate-sensitive sectors absorbed the largest losses:

Energy equities moved in the opposite direction:

Central bank policy divergence is a secondary consequence of the same oil shock driving the U.S. rate repricing: while the Fed holds on inflation grounds, other major central banks are navigating different growth-inflation trade-offs, creating cross-currency dynamics and capital flow shifts that compound the portfolio implications of a prolonged restrictive environment.

The 10-year Treasury yield climbed 11 basis points to 4.62%, while the 2-year yield rose 8 basis points to 4.48%, reinforcing that the bond market is pricing for a sustained period of restrictive rates.

The FOMC dot plot shows a median fed funds rate of 4.75-5.00% through 2026. The divergence between energy equities and rate-sensitive sectors is the practical portfolio expression of the oil-inflation-Fed feedback loop, and any data that moves the CME’s residual 16.2% cut probability higher or lower will generate sharp repricing in both directions.

The “no 2026 cuts” consensus is data-dependent, not permanent. Three specific conditions would need to shift to reopen the easing debate:

The Strait of Hormuz situation cuts both ways. It is currently the primary upside risk to oil and inflation, but a resolution could rapidly reverse the energy dynamics underpinning the entire “higher for longer” thesis.

CME FedWatch’s 16.2% probability of at least one 2026 cut reflects positioning that has not fully converged with bank forecasts. The gap between the 0% probability implied by five major banks and the 16.2% priced by futures markets suggests ongoing uncertainty rather than settled consensus. The slight yield curve steepening on the long end signals that bond markets see rates settling at elevated levels, but not rising further from here.

The CME FedWatch Tool translates federal funds futures positioning into implied probabilities for each scheduled FOMC meeting, making it the standard market reference for tracking the real-time gap between futures pricing and bank forecast consensus.

The convergence of Barclays, Goldman Sachs, JPMorgan, Morgan Stanley, and Deutsche Bank on a “no 2026 cuts” baseline represents the strongest hawkish signal the market has received this cycle. Five independently published revisions, all within two weeks, all pointing to the same quarter for the first move.

The timeline is explicitly data-dependent. Oil prices and PCE readings are the two variables that will determine whether March 2027 holds or shifts. The CME’s residual 16.2% cut probability means any material data surprise, whether a Hormuz resolution that sends crude lower or a PCE print that breaks above 3.5%, will generate rapid repricing across equities, bonds, and rate-sensitive sectors.

Incoming Fed leadership adds a further layer of uncertainty to the timeline: Kevin Warsh’s confirmation advance on 29 April means the committee Powell shaped will operate under a new chair from 15 May, and Warsh’s most significant near-term policy lever may be balance sheet reduction rather than the fed funds rate itself.

The FOMC’s 29 April statement framed the path as “data-dependent,” with no near-term easing signalled. That language now aligns with the entirety of major Wall Street forecasting.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Barclays has removed all expected 2026 Federal Reserve rate cuts from its forecast, with economist Marc Giannoni now projecting a single 25 basis point cut in March 2027 at the earliest, conditional on core PCE inflation trending convincingly toward the Fed's 2% target.

Barclays revised its forecast primarily because its energy team raised the Brent crude price baseline to $115 per barrel for Q2 2026, which lifted the headline PCE forecast to 3.8% and core PCE to 3.1% for Q4/Q4 2026, both far above the Fed's 2% target; continued labour market strength removed the precautionary case for cutting.

Goldman Sachs, JPMorgan, Morgan Stanley, and Deutsche Bank have all published similar revisions in late April and early May 2026, each projecting zero cuts in 2026 and a first 25 basis point move in Q1 2027, representing a rare convergence of five major Wall Street institutions within a two-week window.

Three conditions would need to shift: a sustained drop in Brent crude below $95 to ease headline PCE pressure, core PCE falling below 2.8% on a sustained basis, or significant deterioration in the labour market, any of which Fed Chair Jerome Powell indicated would be required before the committee considers a policy pivot.

On 4 May, REITs fell 1.8%, utilities dropped 1.4%, and the Nasdaq declined 1.3% as higher discount rates compressed valuations, while the 10-year Treasury yield climbed 11 basis points to 4.62%; energy equities bucked the trend, with the S&P 500 energy sector rising 1.2% as elevated crude prices that are keeping the Fed on hold directly benefit producers.