Why Cochlear’s 40% Collapse Was Bigger Than Its Earnings Cut

7 mins ago

When a company announces a $1 billion capital raise, investors typically sell first and ask questions later. NextDC’s (ASX: NXT) April 2026 hybrid securities offer produced the opposite reaction, and the mechanics of why it did so reveal more about the NextDC share price trajectory than the headline number alone.

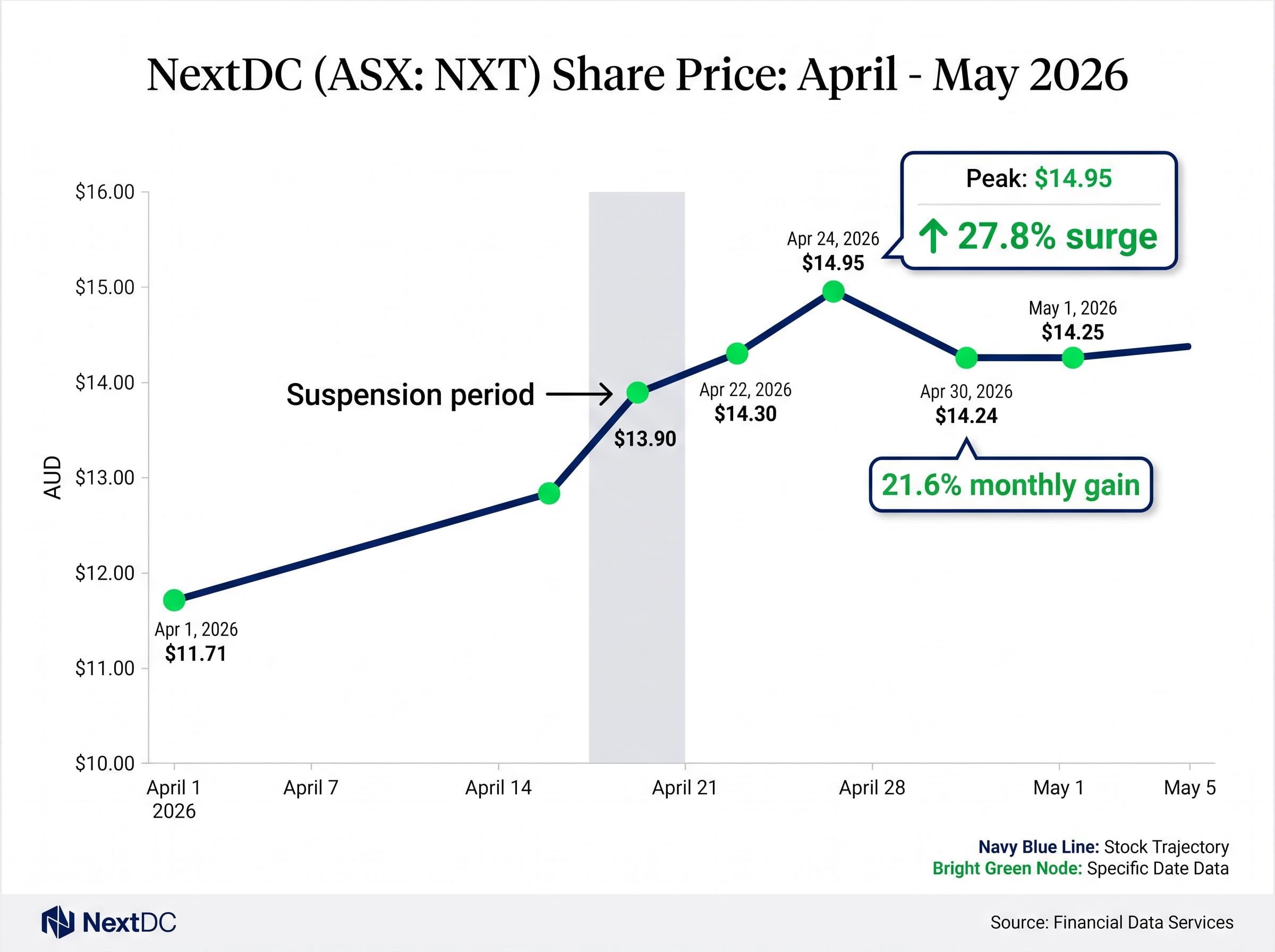

NextDC entered April 2026 trading at $11.71. By 30 April it closed at $14.24, a 21.6% monthly gain driven almost entirely by events surrounding the hybrid securities announcement and the contracted utilisation data released alongside it. The raise itself was subsequently upsized to $1.7 billion through a delayed draw tranche anchored by a single institutional investor. For investors following the stock, the episode raises a question more interesting than whether the price went up: why did it go up, and does the market’s logic hold?

What follows unpacks the mechanics of the raise, the contracted demand figures underpinning investor confidence, and the risks that the share price surge may be obscuring, giving investors the analytical framework to assess NextDC on current fundamentals rather than momentum.

The standard playbook is straightforward. A company announces a large capital raise, existing shareholders face dilution, and the share price drops as sellers front-run the discount. NextDC’s April raise broke that pattern.

Shares held at $13.90 during the suspension period (20-21 April), then rose to $14.30 on 22 April and peaked at $14.95 on 24 April. Market coverage cited a 27.8% surge figure as the headline reaction. The initial offer of $1.0 billion was upsized to $1.7 billion in total hybrid securities capacity, and the price kept climbing.

Three structural features explain why the typical dilution reflex did not fire:

$14.95 on 24 April marked the post-announcement peak, representing the market’s immediate enthusiasm before minor profit-taking brought shares back toward $14.24 at month end.

The announcement also coincided with contracted utilisation data that reset the market’s growth expectations upward. That timing mattered. A raise paired with evidence of accelerating demand reads as expansion capital, not balance sheet repair. The market priced it accordingly.

The instrument itself is worth understanding on its own terms before interpreting investor behaviour around it.

NextDC’s hybrid securities carry a 100-year maturity (effectively perpetual from a practical standpoint) and a fixed coupon that steps up over time, creating an economic incentive for the company to redeem them rather than pay escalating interest indefinitely. The coupon schedule runs as follows:

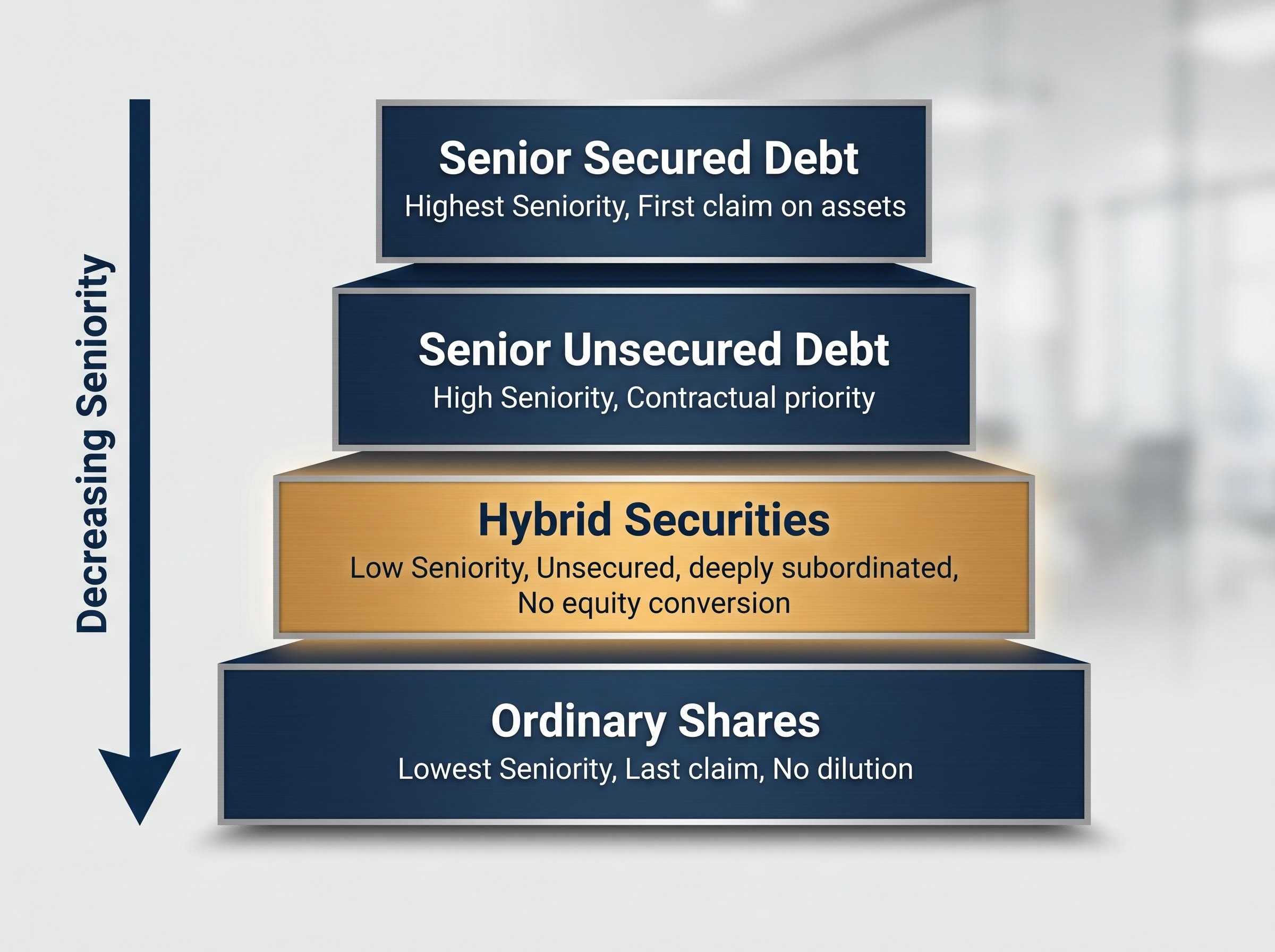

The securities are unsecured and deeply subordinated. In the capital stack, they sit below all forms of debt and above ordinary shares. This positioning is the mechanical reason the raise did not trigger the dilution response that equity placements produce: no new ordinary shares were created.

| Capital Stack Layer | Seniority | Typical Security | Investor Implication |

|---|---|---|---|

| Senior Secured Debt | Highest | Bank facilities, secured bonds | First claim on assets in distress |

| Senior Unsecured Debt | High | Corporate bonds | Contractual priority over subordinated layers |

| Hybrid Securities | Low | NextDC April 2026 offer | Absorbs losses before debt, protected before equity |

| Ordinary Shares | Lowest | NXT ordinary equity | Last claim; no dilution from hybrid issuance |

The absence of equity conversion is the detail that matters most. Instruments with conversion features (such as convertible notes) create an overhang of potential future shares. These hybrids carry no such overhang.

The hybrid securities offer terms, including the five-year non-call period, the coupon step-up schedule, and La Caisse’s binding commitment structure, were set out in the original April announcement before the subsequent upsizing to $1.7 billion confirmed institutional appetite for the instrument.

A capital raise with favourable structural terms still requires an answer to the obvious question: what is the money for? NextDC’s contracted utilisation data, released alongside the offer, provided that answer with unusual precision.

667 MW of contracted utilisation as of 31 March 2026, representing a 60% quarterly increase, served as the headline demand signal underpinning investor confidence in the raise.

The numbers bear closer examination for what they reveal about the nature of the demand:

The forward order book figure is where the analytical weight sits. Those 544 MW represent demand that has been committed by customers but not yet deployed, meaning it has not yet appeared in revenue. For investors assessing whether the capital being raised will earn a return, contracted but unrecognised demand is the most direct evidence available.

The contracted utilisation trajectory that produced the 667MW figure as of March 2026 had already been accelerating through the first half of FY26, when NEXTDC reported 416.6MW of contracted utilisation and a 297MW forward order book that management identified as the primary FY27 earnings catalyst.

Management has indicated expected contracted EBITDA (earnings before interest, tax, depreciation, and amortisation) exceeding $1.0 billion over time. The demand driving these figures comes predominantly from hyperscale cloud providers and AI infrastructure customers, a category where contract sizes tend to be large and contract durations tend to be long.

For Australian investors evaluating NextDC as an AI infrastructure position, the contracted utilisation figures are the most durable piece of evidence available. Share price targets are analyst constructs; signed contracts with hyperscalers are not.

The demand story and the capital intensity story are two sides of the same coin. Delivering 667 MW of contracted capacity, and the 544 MW behind it in the order book, requires capital expenditure at a scale that changes the financial profile of the company over the near term.

FY26 capex guidance has been increased to $2.7-$3.0 billion, up $300 million from prior guidance. The S4 Sydney facility alone is expected to absorb approximately $1.5 billion through the end of FY2027. Looking further out, FY27 capex is forecast at approximately $5.0 billion.

| Period | Capex Estimate | Capital Source |

|---|---|---|

| FY26 | $2.7-$3.0 billion | Hybrid securities ($1.7B), equity offer ($1.5B), operating cash flow |

| FY27 | ~$5.0 billion | Continued deployment of raised capital, potential further funding |

| S4 Sydney (through FY27) | ~$1.5 billion | Allocated from above capital sources |

At this level of capital expenditure, investors are not buying near-term earnings yield. They are buying a long-duration infrastructure asset whose returns will materialise as contracted capacity converts into recognised revenue over multiple years.

Separate from the hybrid securities, NextDC announced a pro-rata accelerated non-renounceable entitlement offer to raise approximately $1.5 billion. Unlike the hybrid, this offer does increase the ordinary share count.

The retail component of the offer closes on 11 May 2026. Existing shareholders face a binary decision: participate and maintain their proportional ownership, or decline and accept dilution. That decision rests on each investor’s assessment of whether the current price (around the $14.25 area) fairly reflects the contracted EBITDA pipeline that the capital will fund.

The distinction matters. The hybrid securities did not dilute ordinary shareholders. The equity entitlement offer does.

NextDC operates at the physical layer of the AI infrastructure stack. The company owns and operates the data centres, specifically the power delivery, cooling systems, and network connectivity, that hyperscale cloud providers and AI workloads require. It sits one layer below the cloud platforms and two layers below the AI software applications that generate headlines.

Understanding where NextDC sits in that stack clarifies the risk profile:

For Australian retail investors, NextDC represents one of a limited number of ASX-listed companies providing direct physical AI infrastructure exposure. The position is AUD-denominated and subject to domestic regulatory oversight, which may suit investors who prefer local market exposure to the AI infrastructure theme rather than navigating offshore alternatives.

Many investors following the share price surge will be encountering hybrid securities mechanics and data centre economics for the first time. The category matters: this is infrastructure investment with technology-sector demand characteristics, not a software growth story with infrastructure costs.

Honest analysis requires acknowledging what the available data can and cannot support. Without broker consensus EBITDA forecasts or enterprise value to EBITDA (EV/EBITDA) peer comparisons from public sources, a rigorous valuation exercise is not possible at the time of writing. What is possible is framing the competing interpretive positions that the available data supports.

Information gap: No broker consensus estimates for revenue, EBITDA, or free cash flow, and no publicly available EV/EBITDA peer comparison data, were accessible at the time of writing. Investors should seek independent research to supplement this analysis.

Data centre valuation methods in the Australian market are being tested by the speed of demand growth: Infratil’s CDC stake rose A$500 million in a single quarter to imply a total enterprise value of A$15.0 billion, a move driven by DCF assumptions that conservatively exclude pipeline development beyond 2040 and therefore may understate long-run value.

Bull case factors:

Bear case factors:

The data points worth monitoring as new information becomes available include: quarterly contracted utilisation updates, capex execution against the $2.7-$3.0 billion FY26 guidance, and any broker research revisions published following the capital raise.

For investors wanting to stress-test the bear case in more depth, our full explainer on AI infrastructure demand constraints examines the multi-year grid interconnection backlogs, software monetisation gaps, and power procurement challenges that could slow the hyperscaler capex cycle underpinning NextDC’s forward order book.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The April share price movement was not a single catalyst but three converging signals. The hybrid structure neutralised the dilution reflex that ordinarily punishes capital raises. The contracted utilisation data, particularly the 60% quarterly increase to 667 MW, reset the market’s growth expectations with hard contractual evidence rather than management guidance alone. And La Caisse’s $1.7 billion anchor commitment provided the institutional imprimatur that gave smaller investors confidence to follow.

That market verdict will be tested over the next 12-18 months. The FY27 capex forecast of approximately $5.0 billion represents a commitment that must translate into deployed, revenue-generating capacity on schedule. If contracted utilisation growth decelerates or capex execution slips, the premium embedded in the current price becomes difficult to sustain.

The investor takeaway: NextDC’s share price in May 2026 reflects a long-duration bet on AI infrastructure demand. The capital raise mechanics explain why the market repriced the stock upward rather than treating the offer as a warning sign. Whether that repricing proves justified depends on execution against a buildout programme of a scale that few ASX-listed companies have attempted.

NextDC's hybrid securities carry no equity conversion mechanism, meaning no new ordinary shares were created and existing shareholders faced no dilution from the hybrid offer itself, removing the usual trigger for post-raise selling.

NextDC's hybrid securities are unsecured, subordinated instruments with a 100-year maturity and a fixed coupon that steps up over time, sitting below all debt but above ordinary shares in the capital stack, with no conversion into ordinary equity.

As of 31 March 2026, NextDC reported 667 MW of contracted utilisation, up 60% quarter-on-quarter, plus a 544 MW forward order book representing committed but undeployed demand that underpins the company's long-term revenue visibility.

NextDC has guided FY26 capex of $2.7-$3.0 billion and forecast FY27 capex of approximately $5.0 billion, meaning near-term earnings growth is constrained and investors are effectively buying a long-duration infrastructure asset whose returns will emerge as contracted capacity converts to recognised revenue over multiple years.

Yes, the separate pro-rata accelerated non-renounceable entitlement offer, which targets approximately $1.5 billion, does increase the ordinary share count, unlike the hybrid securities offer; existing shareholders who decline to participate will experience proportional dilution.