Goldman Sachs Cuts 2026 Smartphone Shipment Forecast 10% on AI Crunch

18 mins ago

Apple’s fiscal Q3 revenue growth guidance of 14-17% arrived Thursday night and immediately rendered Wall Street’s 9.5% consensus estimate almost embarrassingly conservative. The gap between the two figures, announced alongside the company’s fiscal second-quarter results on 30 April 2026, is the kind of revision event that forces institutional models to reprice the most closely watched equity in U.S. markets.

The quarter itself delivered a broad beat. Total revenue hit $111.18 billion, diluted earnings per share came in at $2.01, and operating cash flow reached a record $28.7 billion. But the result landed during a U.S. earnings season in which American companies are already outpacing European peers on beats, according to Barclays strategists, and Apple’s forward outlook added the heaviest single-name confirmation of that momentum.

What follows breaks down every segment result against consensus, explains what is driving the bullish Q3 outlook, details the $100 billion buyback authorisation, and identifies the supply-side risks that investors should track in the months ahead.

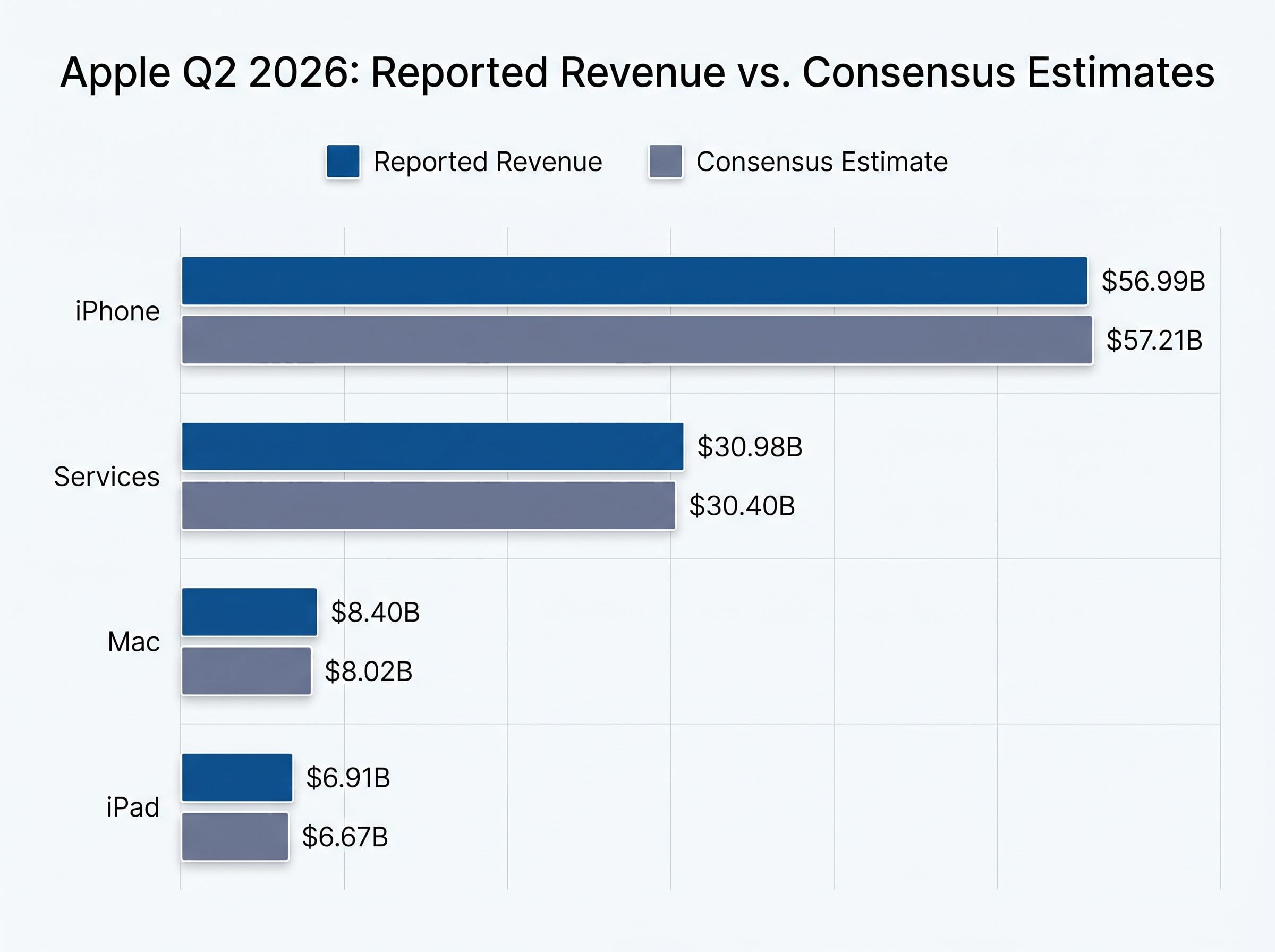

Apple reported total revenue of $111.18 billion for its fiscal second quarter (January through March 2026), beating the $109.66 billion consensus estimate and marking a 17% increase year over year. Diluted EPS of $2.01 topped the $1.95 estimate, reflecting 22% year-over-year growth. Record operating cash flow of $28.7 billion underpinned the quarter’s financial strength.

The quarterly figures represented Apple’s best-ever March quarter across multiple categories. Yet the number that reshaped the conversation arrived in the outlook.

The analytical frame of guidance over results has defined this earnings cycle from the start, with companies representing roughly 44% of S&P 500 market cap reporting in a single week and the index at record levels, creating conditions where forward-looking signals carry more repricing power than any single quarterly beat.

Apple guided Q3 revenue growth of 14-17%, nearly double the Wall Street consensus estimate of approximately 9.5%.

That gap between company guidance and analyst consensus is not a rounding difference. It is a structural repricing signal, and it dominated the post-release discussion.

The Q3 guidance range requires a demand story strong enough to justify it. The product-level data from Q2 provides that evidence across three distinct revenue streams.

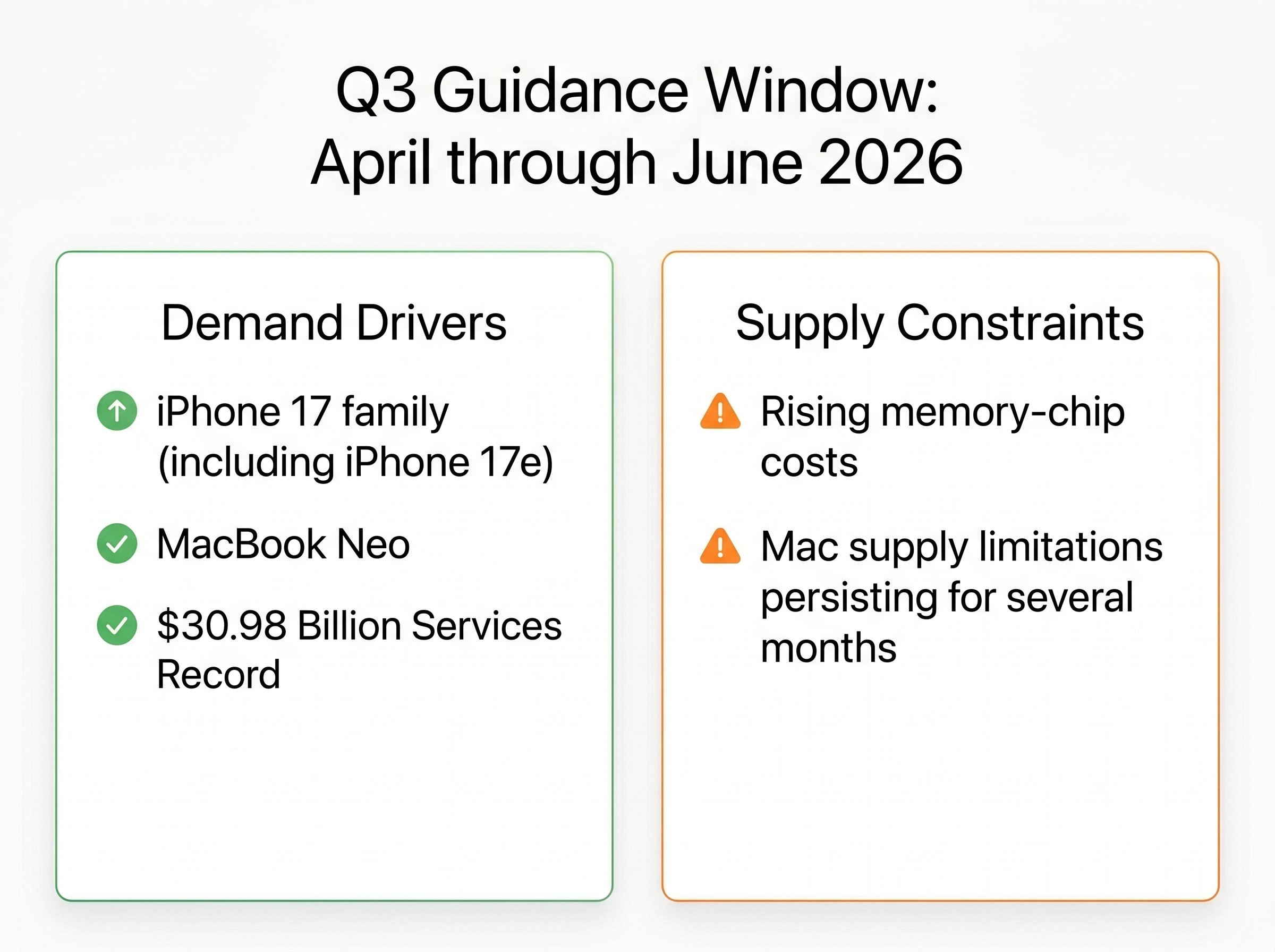

iPhone revenue reached $56.99 billion, up approximately 22% year over year from $46.71 billion in Q2 FY2025. Tim Cook, Chief Executive Officer, described the iPhone 17 lineup as the “most popular lineup in our history,” citing “extraordinary demand” across geographic markets. The iPhone 17 family, including the iPhone 17e, was introduced during the quarter and drove the bulk of the revenue acceleration.

Mac revenue grew to $8.4 billion, up 6% year over year and beating the $8.02 billion consensus estimate. Cook noted that the recently launched MacBook Neo is “captivating customers worldwide,” adding a second hardware growth vector to the demand picture. The Q3 guidance, in other words, is not a single-product bet.

| Segment | Reported Revenue | Consensus Estimate | YoY Change | Result |

|---|---|---|---|---|

| iPhone | $56.99B | $57.21B | +22% | Slight miss |

| Services | $30.98B | $30.40B | +16.3% | Beat |

| Mac | $8.40B | $8.02B | +6% | Beat |

| iPad | $6.91B | $6.67B | +8% | Beat |

Services revenue reached $30.98 billion, up 16.3% year over year and beating the $30.40 billion consensus estimate. The figure set a new all-time record for the segment.

The significance extends beyond the quarterly number. Services carries a recurring-revenue profile that supports the forward guidance’s credibility even if hardware shipments face short-term friction from supply constraints. For the Q3 outlook to hold at the upper end, Services’ momentum reduces the amount of incremental hardware volume required to clear the bar.

Alongside the quarterly results, Apple’s board authorised an additional $100 billion share repurchase programme and increased the dividend to $0.27 per share, payable 14 May 2026.

Apple authorised a $100 billion share repurchase programme, backed by record operating cash flow of $28.7 billion for the quarter. The quarterly dividend increases to $0.27 per share, payable 14 May 2026.

A share repurchase programme works through a straightforward mechanism that directly benefits existing shareholders:

For retail investors in particular, the combined effect of buybacks, dividends, and earnings growth clarifies why Apple remains a core holding across institutional and individual portfolios. The $100 billion authorisation signals management’s confidence that the current share price represents a productive use of capital.

The Q2 results were not without friction. Cook acknowledged supply issues that affected both Mac and iPhone during the quarter, pointing to rising memory-chip costs and Mac supply limitations expected to persist for several months.

The evidence showed up in the numbers. iPhone revenue of $56.99 billion came in marginally below the $57.21 billion consensus estimate, the only major segment to miss. Supply-side friction was a contributing factor. Mac revenue still grew to $8.4 billion despite constraints, suggesting underlying demand absorbed the headwind, but the miss on iPhone consensus underscored that supply limitations are capping what would otherwise be even stronger results.

The two distinct supply risks investors should monitor:

Memory chip availability sits at the intersection of Apple’s supply constraint problem and a broader semiconductor market dynamic: hyperscalers committed $635-700 billion in FY2026 infrastructure capital expenditure are competing for the same advanced memory capacity that Apple needs to fulfil iPhone and Mac demand, tightening the market from multiple directions.

The “several months” timeline Cook referenced maps directly onto the Q3 guidance period, which covers April through June 2026. If constraints ease within that window, the 14-17% revenue growth guidance becomes achievable at the upper end. If they persist or worsen, the lower end becomes more likely.

This overlap makes supply chain resolution the single most important monitoring variable for investors between now and the next earnings call. The demand picture, as evidenced by the Q2 results, is not in question. Execution on the supply side is.

TrendForce DRAM pricing forecasts for 2026 indicate that the cost pressures Cook cited are part of a broader industry-wide supply dynamic, one that has historically taken multiple quarters to resolve once a supercycle inflection point is reached.

Apple’s quarter did not arrive in isolation. Barclays strategists noted that blended Q1 2026 EPS growth is trending upward across U.S. equities and that American earnings beats are considerably stronger than those of European peers during this reporting cycle.

The timing amplified the attention. Apple released results while most European markets were closed for Labour Day on 1 May 2026, concentrating investor focus on U.S. earnings flow. U.S. equity futures moved upward following record-setting Wall Street closes prior to the release.

A strong earnings season amplifies the signal from any individual beat. Apple’s result, as the most closely watched name in U.S. equities, adds the heaviest confirmation yet that corporate America is outperforming expectations this quarter.

Three elements define the Apple story coming out of this quarter. The Q2 result was a broad beat, with $111.18 billion in revenue, 22% EPS growth, and records across Services and operating cash flow. The Q3 guidance of 14-17% revenue growth nearly doubled the 9.5% analyst consensus, backed by iPhone 17 demand that Cook called extraordinary and a Services segment generating $30.98 billion in recurring revenue.

The unresolved variable is supply. Memory-chip constraints and Mac supply limitations are expected to persist for several months, a timeline that sits directly inside the Q3 window. Demand is not the question. Whether Apple can deliver the hardware to meet it is.

Record results, record guidance, and an unresolved supply constraint timeline that will determine whether the upper end of the Q3 outlook is achievable.

Investors tracking Apple through the next 60-90 days have a clear framework: monitor supply chain signals, track whether memory-chip cost pressures ease, and watch for any management commentary on constraint resolution ahead of the Q3 report.

For readers wanting to stress-test the demand narrative, our deep-dive into whether Apple’s Q2 tailwinds are durable examines the role of temporary factors including inventory frontloading ahead of tariff uncertainty, Samsung’s Galaxy S26 delay, and the memory shortage projected to persist through late 2027, each of which complicates a straight-line extrapolation from Q2’s record results to sustained outperformance.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including Apple’s Q3 guidance range, are subject to change based on market developments, supply chain conditions, and company performance.

Apple reported fiscal Q2 2026 revenue of $111.18 billion, beating the $109.66 billion consensus estimate, with diluted EPS of $2.01 versus the $1.95 estimate and record operating cash flow of $28.7 billion.

Apple guided Q3 2026 revenue growth of 14-17%, nearly double the Wall Street consensus estimate of approximately 9.5%, making it one of the most significant guidance beats among large-cap U.S. equities this earnings season.

The $100 billion share repurchase programme reduces the total shares outstanding, which amplifies earnings per share growth over time; Apple also raised its quarterly dividend to $0.27 per share, payable 14 May 2026, combining two direct return mechanisms for shareholders.

Apple CEO Tim Cook cited rising memory-chip costs and Mac supply limitations expected to persist for several months, risks that sit directly inside the April-to-June Q3 window and could limit results to the lower end of the 14-17% guidance range if they are not resolved.

Apple's Services segment set a new all-time record at $30.98 billion in revenue, up 16.3% year over year and beating the $30.40 billion consensus estimate, adding a durable recurring-revenue layer that supports the credibility of the Q3 guidance.