Why Australian Investment Grade Bonds Now Yield 6-7%

24 mins ago

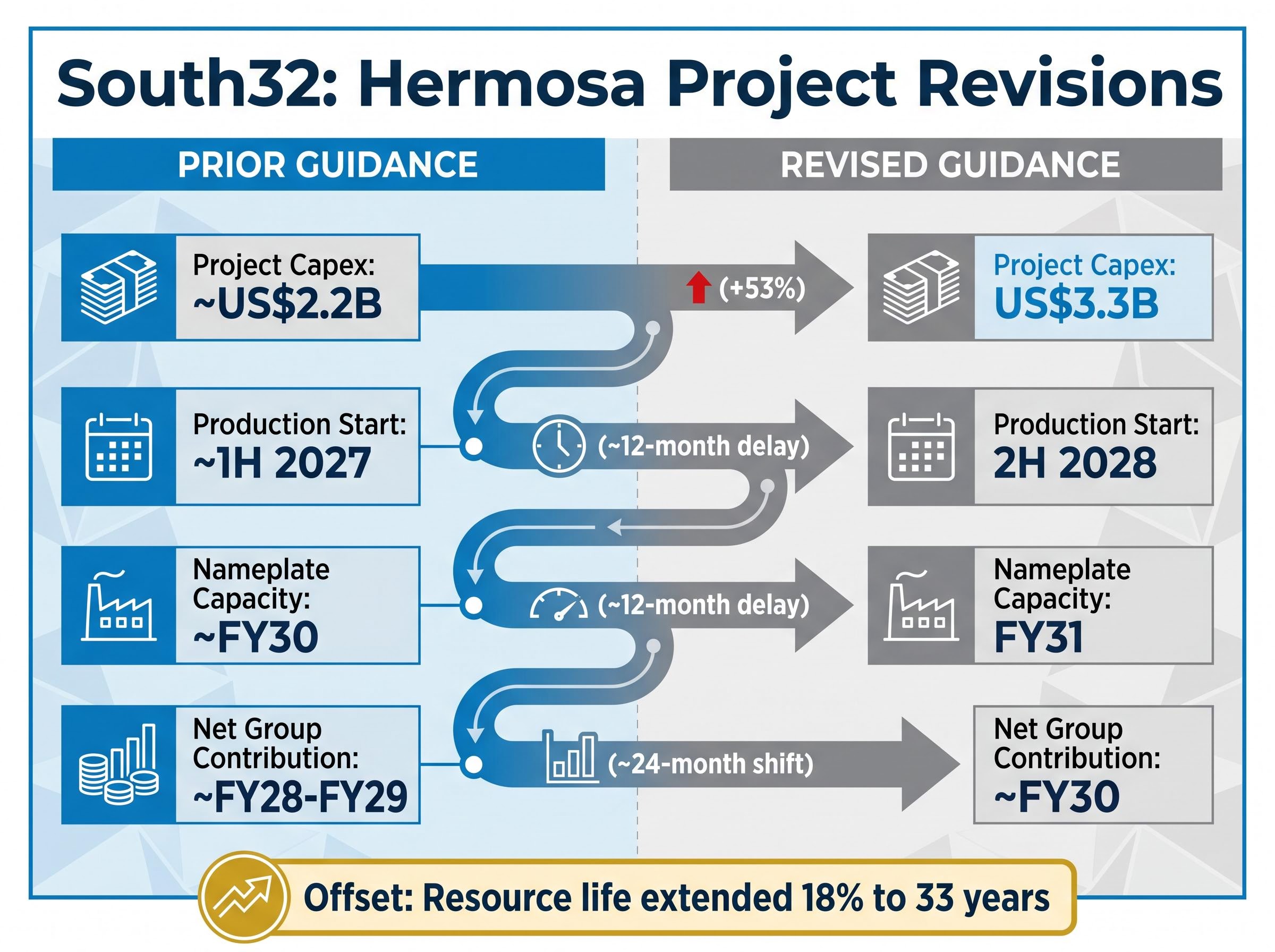

South32’s Hermosa project just became 53% more expensive and 12 months longer. The disclosure, made on 30 April 2026, revised the project’s capital expenditure to US$3.3 billion (approximately A$5.1 billion), pushed initial production to the second half of 2028, and wiped 5.4% from the company’s share price in a single session. Four major brokers cut their target prices by between 6% and 22%, though three of the four retained buy or overweight ratings.

Capex blowouts at large-scale mining projects are not aberrations. They are a structurally embedded feature of the industry, particularly for greenfield developments above US$1 billion in scale. The Hermosa revision lands in a period when ASX-listed resource investors have already absorbed similar revelations from BHP’s Jansen project and Fortescue’s Iron Bridge development. The pattern is consistent enough to demand a framework, not just a reaction.

What follows uses Hermosa as a live case study to explain why mining capex overruns happen, how analysts reprice risk when they do, and what a measured investor response looks like when a project blows its budget.

The arithmetic speaks first. South32 sanctioned the Hermosa project under a cost base that has now been revised upward by 53%, taking the total capex estimate to US$3.3 billion, or approximately A$5.1 billion at current exchange rates. The production start date has shifted approximately 12 months to the second half of 2028, and nameplate capacity is now expected in FY31, also roughly a year later than prior guidance.

Macquarie now models the project’s net group contribution around FY30, approximately five years after the investment phase began. That delay in cash flow generation is where the NPV damage concentrates: the total volume of cash the project may produce has not changed dramatically, but the present value of that cash has fallen because it arrives later.

| Metric | Prior Guidance | Revised Guidance | Change |

|---|---|---|---|

| Project capex | ~US$2.2B | US$3.3B (~A$5.1B) | +53% |

| Production start | ~1H 2027 | 2H 2028 | ~12-month delay |

| Nameplate capacity | ~FY30 | FY31 | ~12-month delay |

| Net group contribution | ~FY28-FY29 | ~FY30 | ~24-month shift |

Management announced a partial offset: an 18% resource life extension to 33 years, framed as long-term value preservation. That extension matters on a discounted cash flow basis, but it does not erase the five-year wait for meaningful cash contribution.

Market impact: South32 shares fell 5.4% on 30 April 2026, the day of the announcement, reflecting the immediate repricing of timeline risk across the investor base.

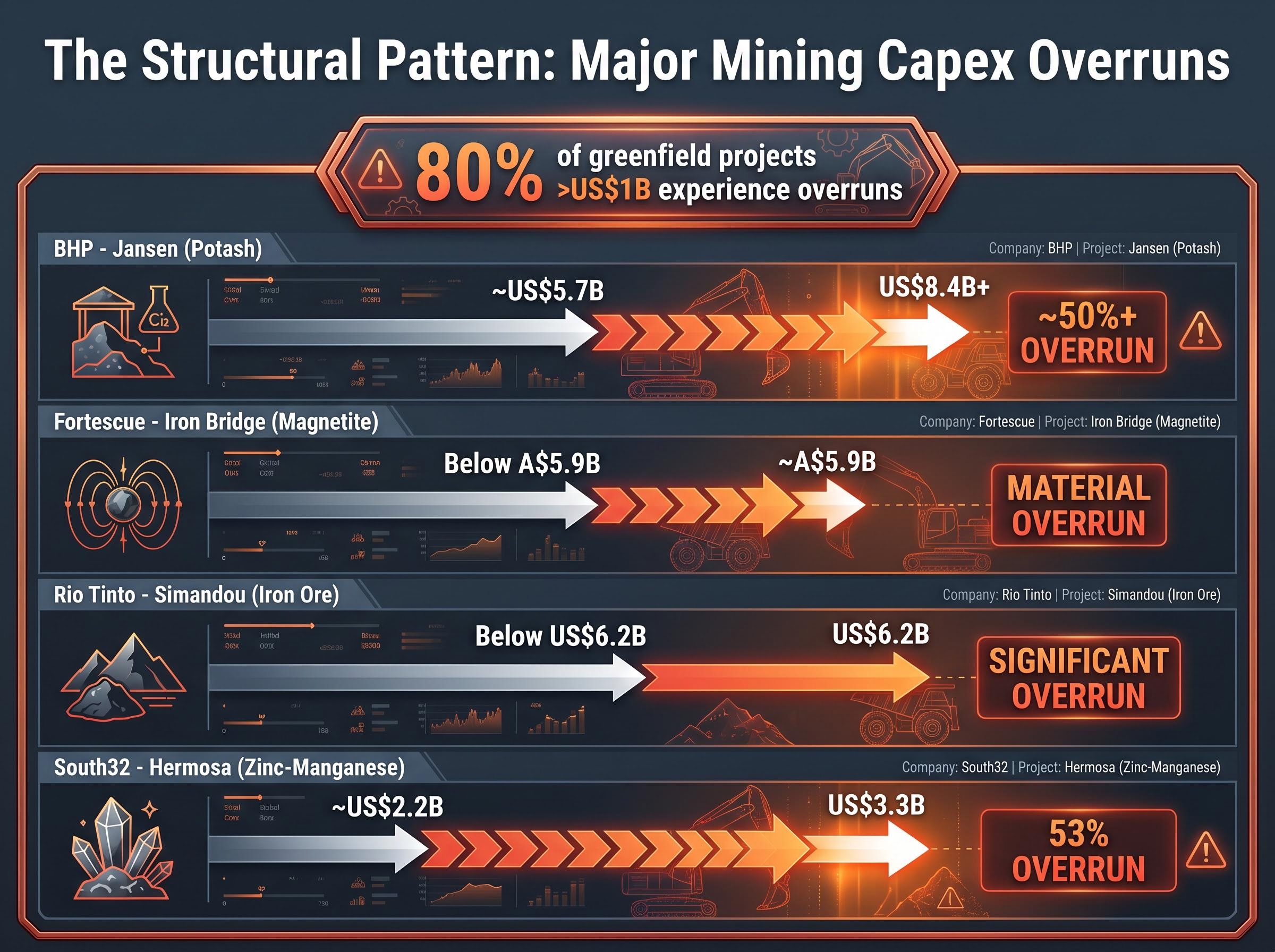

The instinct after a capex blowout is to blame management. The data suggests something more systemic. Industry consensus estimates place the likelihood of cost overruns at approximately 80% for greenfield projects exceeding US$1 billion in scale. Hermosa is not an outlier; it is a data point within a well-documented distribution.

Four structural drivers account for the bulk of that pattern:

Approximately 80% of greenfield mining projects exceeding US$1 billion in scale experience cost overruns, according to industry consensus estimates. The question for investors is not whether a project will overrun, but by how much.

Front-End Engineering and Design (FEED) is the phase at which project costs are formally sanctioned by boards, the point where a project moves from concept to committed capital. Contingency buffers set at this stage have historically been insufficient for large greenfield developments.

McKinsey research on mining project delivery highlights that capex forecasting at sanction is structurally prone to underweighting volatile input prices and contractor availability. The industry response has been a trend toward higher recommended contingency buffers: Macquarie and other brokers now recommend 20-30% buffers as standard at project sanction, a figure that reflects accumulated failures rather than theoretical modelling.

Greenfield project execution at the scale Hermosa represents involves contractor selection, phased procurement, and site-specific engineering challenges that are only partially visible at the FEED stage — the engineering and labour hire contract structures used in contemporary large-scale mining developments illustrate why scope changes discovered during construction routinely exceed the contingency buffers set at sanction.

McKinsey research on mining project delivery finds that megaprojects valued at US$1 billion or more experience cost overruns averaging at least 79% above initial budget estimates and schedule delays averaging 52% above initial time frames — figures that position Hermosa’s 53% overrun well within the documented distribution rather than outside it.

Hermosa was sanctioned under cost assumptions that did not fully account for post-2022 input cost volatility. The 53% overrun exceeds even the upper end of recommended contingency ranges, suggesting the initial cost base carried insufficient margin for the conditions that followed.

Placing Hermosa alongside its peers reveals a sector-wide condition rather than a company-specific failure. Three verified examples illustrate the scale of the pattern.

BHP’s Jansen potash project in Canada moved from an original estimate of approximately US$5.7 billion to US$8.4 billion, with a further US$1 billion increase confirmed in January 2026. BHP shares recovered substantially after the updated guidance was absorbed by the market.

Fortescue’s Iron Bridge magnetite project in Australia reached total capex of approximately A$5.9 billion, materially above earlier estimates, driven by tariffs, contractor underperformance, and broader inflation.

Rio Tinto’s Simandou iron ore project in Guinea carried a US$6.2 billion capex announced in late 2023 and early 2024, with first production targeted for 2025, reflecting labour and input cost pressures at the time of sanction.

| Project | Company | Original Capex | Revised Capex | Overrun Scale |

|---|---|---|---|---|

| Jansen (Potash) | BHP | ~US$5.7B | US$8.4B+ | ~50%+ |

| Iron Bridge (Magnetite) | Fortescue | Below A$5.9B | ~A$5.9B | Material |

| Simandou (Iron Ore) | Rio Tinto | Below US$6.2B | US$6.2B | Significant |

| Hermosa (Zinc-Manganese) | South32 | ~US$2.2B | US$3.3B | 53% |

The pattern is consistent. Investors who treat every capex overrun as a company-specific red flag will consistently mis-price risk. The real question is not whether a project overran but by how much, and whether management’s revised estimates carry credibility.

Four major brokers responded to the Hermosa disclosure within 24 hours. All four cut their target prices. Three of the four retained buy or overweight ratings. That combination, lower target but maintained conviction, tells a specific story about the repricing mechanics.

| Broker | Prior Target | New Target | Change | Rating |

|---|---|---|---|---|

| Macquarie | A$5.80 | A$4.50 | -22% | Outperform (retained) |

| JPMorgan | A$5.10 | A$4.80 | -6% | Overweight (retained) |

| UBS | A$5.20 | A$4.50 | -13% | Buy (retained) |

| Jefferies | A$5.25 | A$5.25 | No change | Buy (retained) |

The NPV repricing works as follows: a later production start reduces the present value of future cash flows even if the total cash flow remains unchanged. Money received further in the future is worth less today. Macquarie applied earnings estimate reductions of 18% for FY28, 18% for FY29, and 9% for FY30, illustrating how a 12-month delay cascades unevenly across the earnings profile rather than reducing all years equally.

Macquarie now models the net group contribution inflection point at approximately FY30, a shift of roughly 24 months from prior estimates. That extended timeline is where the bulk of the target price reduction originates.

The spread between Macquarie’s A$4.50 and Jefferies’ A$5.25 encapsulates where the genuine uncertainty sits: in the terminal value assumptions for a project now five years from meaningful cash flow contribution. Retained buy ratings across the board signal that all four brokers consider the revised economics value-accretive at current prices, just less so than previously modelled.

Major mining sector valuations remain materially compressed relative to prior commodity booms, with large-cap miners trading at roughly 7-8x EV/EBITDA compared to approximately 14x during the 2008-2010 cycle — which means capex overruns at individual projects are repriced against a backdrop where the sector as a whole already carries a significant discount to historical multiples.

The broker response is methodical. The market response is less so. South32 shares fell 5.4% on 30 April 2026, consistent with observed patterns for ASX-listed miners receiving negative capex news.

Two distinct investor responses tend to emerge:

The recovery framework from comparable situations is instructive. BHP shares recovered substantially following the Jansen update, with recovery occurring over a 12-24 month period as management delivered on revised production milestones. Projects with repeat overruns or missed production targets tend to carry persistent valuation discounts.

The primary post-overrun signal is milestone adherence on the revised schedule, not the share price trajectory in the weeks following the announcement. Macquarie’s modelling now places meaningful cash flow contribution at approximately FY30: investors holding South32 for Hermosa’s contribution should re-evaluate their time horizon against that benchmark.

Debt refinancing activity, noted in the period following the announcement, offers a secondary signal. It indicates management is actively managing the balance sheet consequences of the revised capex, which is relevant to whether dividends or buybacks are affected during the extended construction phase.

The 18% resource life extension to 33 years means Hermosa’s fundamental economic case is longer-dated than before the announcement, not weaker. On a 10-year view, the project’s value proposition remains intact. On a five-year view, it has deteriorated materially.

Australia’s Critical Minerals Strategy, administered by the Department of Industry Science and Resources, sets out the regulatory approval frameworks and investment conditions that govern large-scale developments in battery metals and manganese — the commodity categories that define Hermosa’s long-term strategic rationale for South32.

The revised US$3.3 billion capex and 2H 2028 production start are management estimates, not guarantees. The structural drivers of overruns, labour shortages, permitting complexity, input cost volatility, have not disappeared from the industry. They remain active pressures on every large greenfield project under construction.

Broker target range post-revision: A$4.50 (Macquarie, UBS) to A$5.25 (Jefferies). At these levels, South32 is priced for a project that performs to its second set of expectations. A third revision would likely eliminate the remaining upside buffer.

Broker consensus held its buy and overweight ratings, indicating the revised economics are still regarded as value-accretive at current prices. The margin for further error, however, is materially narrower than it was 48 hours ago.

Hermosa offers a framework that applies well beyond South32. When the next large mining capex revision is disclosed, four questions structure the response:

The structural context also matters. An overrun announced during sector-wide cost inflation, when 80% of greenfield projects are experiencing similar pressures, is a different signal from one announced when peer projects are coming in on budget. Macquarie’s recommendation of 20-30% contingency buffers at project sanction serves as a useful benchmark for how much cost headroom a project needs to be considered well-structured.

Hermosa is a case study in a structural industry pattern, not a South32-specific failure. The investor framework it illustrates, separating the mechanical NPV repricing from the reflexive sell impulse, applies to any large greenfield mining development on the ASX.

What remains genuinely uncertain is whether the revised estimates hold, whether South32 management’s credibility on Hermosa can be rebuilt through milestone delivery, and whether sector-wide input cost pressures continue to ease or intensify.

The primary thing to watch is not the share price in May 2026. It is whether the 2H 2028 production start is confirmed over the next 12 months. That will be the first meaningful data point on whether the revised case is credible.

Investors interested in tracking Hermosa’s progress should monitor South32’s next quarterly update for any revision to the 2H 2028 production start guidance. Those looking to build a broader framework for evaluating mining project risk may find the McKinsey analysis on capex forecasting in mining project delivery a useful starting point.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Mining capital cost overruns occur when a project's actual construction costs exceed the budget approved at sanction, driven by labour shortages, engineering scope changes, permitting delays, and systematic underestimation at the FEED stage. Industry data shows approximately 80% of greenfield mining projects exceeding US$1 billion in scale experience cost overruns, making them a structural feature of the industry rather than isolated management failures.

South32 revised Hermosa's capex upward by 53% to US$3.3 billion (approximately A$5.1 billion) on 30 April 2026, pushing the initial production start to the second half of 2028 and nameplate capacity to FY31, each roughly 12 months later than prior guidance.

The most important post-overrun signal is milestone adherence on the revised construction schedule, not the share price movement in the weeks following the announcement. Investors should also monitor debt refinancing activity and whether independent brokers retain buy or overweight ratings after cutting their target prices.

Brokers reduce their net present value models to reflect the lower present value of cash flows that now arrive later, cascading earnings estimate cuts unevenly across future financial years. In Hermosa's case, four major brokers cut target prices by between 6% and 22%, but three of the four retained buy or overweight ratings, signalling the revised economics are still considered value-accretive at current prices.

Hermosa's 53% overrun is significant but sits within the documented range for large greenfield developments, with BHP's Jansen potash project exceeding 50% above its original estimate and McKinsey research finding megaprojects average cost overruns of at least 79% above initial budgets. Hermosa is a data point within a well-established industry distribution rather than an outlier.