Your US Index Fund Is a Five-Stock Bet in Disguise

1 min ago

Investors in two Blue Owl Capital private credit funds requested the return of $5.4 billion in the first quarter of 2026, with one fund seeing withdrawal requests equal to 40.7% of its outstanding shares. The funds can only honour 5% per quarter. The mismatch between what investors want back and what the structure permits has become the most visible stress test private credit has faced since the asset class began attracting retail capital at scale. OWL shares have fallen roughly 43% year-to-date as of early April 2026, collapsing from a 52-week high of $21.08 to approximately $8.57. AI disruption fears have rattled software-sector valuations, and Blue Owl’s technology-heavy private credit portfolios sit directly in the crosshairs. What follows is an analysis of what is actually happening inside these funds, how Business Development Company (BDC) structural rules are shaping investor outcomes, what the credit data says versus what the markets fear, and what different classes of investors should understand about their position.

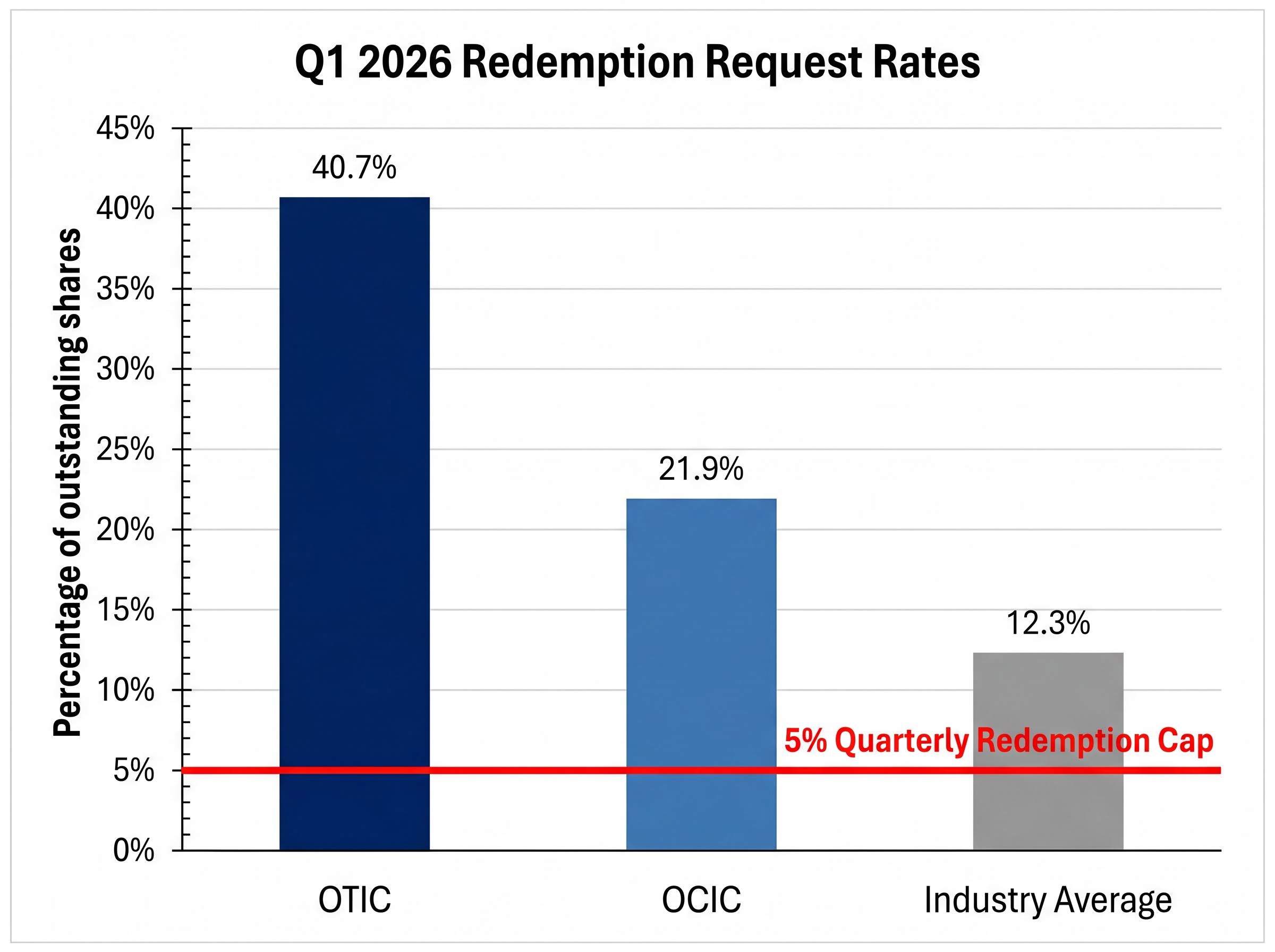

The numbers speak before any explanation is needed. Blue Owl Credit Income Fund (OCIC), the firm’s flagship with approximately $36 billion in assets under management, received redemption requests representing 21.9% of outstanding shares in Q1 2026. Blue Owl Technology Income Fund (OTIC), a smaller fund with approximately $6.2 billion in AUM concentrated in software-sector lending, received requests for 40.7% of outstanding shares.

Both funds are capped at 5% redemptions per quarter. The gap between demand and structural capacity created immediate backlogs running into the billions.

The deterioration was sudden. In Q4 2025, OTIC’s redemption request rate sat at approximately 15.4%-17%, and the fund met every request in full. One quarter later, that rate more than doubled. The industry average perpetual BDC redemption request in Q1 2026 was 12.3% of outstanding shares, placing OCIC at nearly double and OTIC at more than triple the norm.

Blue Owl attributed the surge to “heightened market concerns around AI-related disruption to software companies.”

The AI disruption in tech that Blue Owl attributes to the surge in OTIC redemption requests is not a vague headline risk; the US software market absorbed an estimated $2 trillion in wealth destruction in early 2026 as capital migrated away from headcount-dependent licensing models toward consumption-based and synthetic infrastructure platforms.

| Metric | OCIC | OTIC |

|---|---|---|

| AUM (Q1 2026) | ~$36 billion | ~$6.2 billion |

| Q4 2025 redemption request rate | Below cap (fully met) | ~15.4%-17% (fully met) |

| Q1 2026 redemption request rate | 21.9% | 40.7% |

| Quarterly redemption cap | 5% | 5% |

| Approximate backlog implied | ~16.9% of shares unmet | ~35.7% of shares unmet |

The scale of the overshoot, particularly at OTIC, indicates that a concentrated subset of the shareholder base moved simultaneously rather than drifting toward exits over multiple quarters.

The 5% cap is not an emergency measure. It is the way non-traded BDCs are designed to operate. A Business Development Company is a closed-end investment vehicle that lends to mid-market companies, typically private firms that cannot easily access public bond markets. Unlike an open-ended mutual fund or an exchange-traded fund, a non-traded BDC does not offer daily liquidity. Investors commit capital with the understanding that redemptions are periodic and structurally limited.

The 5% quarterly cap exists to prevent forced asset sales. If a fund holding illiquid private loans were required to honour all redemption requests immediately, it would need to sell those loans at distressed prices, destroying value for remaining shareholders. The cap ensures orderly portfolio management at the cost of immediate liquidity.

Blue Owl applied the cap as designed. The Securities and Exchange Commission (SEC) has not proposed changes to the 5% cap rule as of the time of writing, and OCIC’s leverage ratio of approximately 0.7x sits well below the BDC-mandated ceiling of 2x, signalling structural headroom rather than distress.

The SEC staff guidance on BDC redemption requirements under Section 61(a) of the Investment Company Act of 1940 establishes the regulatory framework that allows non-traded BDCs to limit shareholder redemptions to periodic windows, making the 5% quarterly cap a feature of the structure rather than an emergency override.

The mechanics of the queue are where frustration compounds:

Sustained redemption backlogs can constrain portfolio management decisions. Fund managers may begin shifting toward more liquid assets to meet future obligations, potentially altering the yield and risk profile that attracted investors in the first place.

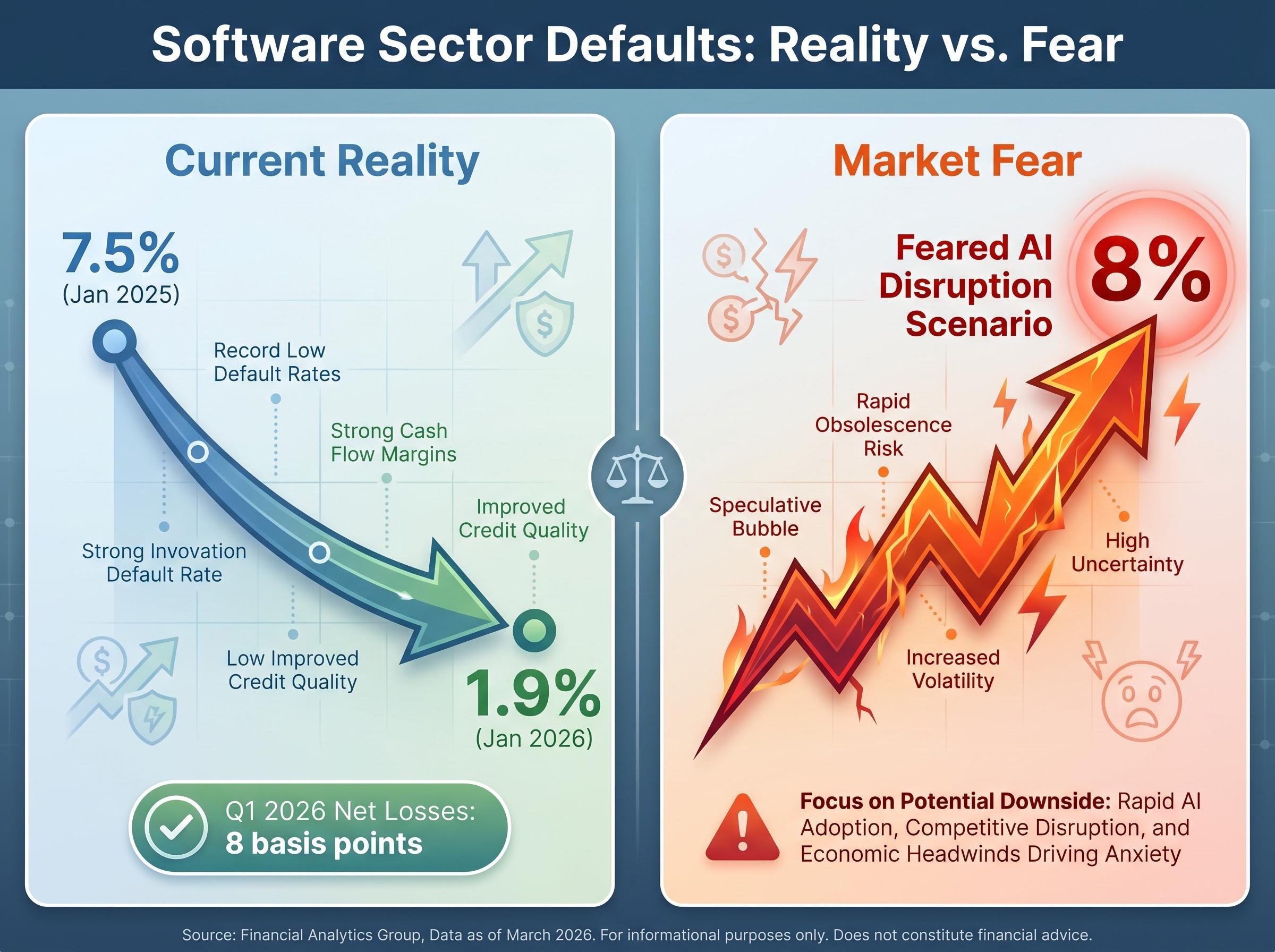

The actual credit performance of these portfolios does not match the intensity of the exit pressure. Net losses across both funds stood at just 8 basis points as of Q1 2026.

Net portfolio losses: 8 basis points. This is the figure that sits most uncomfortably alongside $5.4 billion in redemption requests.

The software and cloud services private credit default rate was approximately 1.9% in January 2026, down from 7.5% in January 2025. The near-term trajectory is improving, not deteriorating.

What investors appear to be pricing in is a different story entirely. Forward-looking warnings from analysts flag the potential for software-sector defaults to surge to approximately 8% if AI disruption accelerates the displacement of incumbent software companies. The broader private credit market saw default estimates of 1.6%-4.7% for 2025.

The distance between 1.9% and 8% is where the entire crisis lives. Q2 2026 data will begin to indicate which direction the gap closes.

Private credit default rates across the broader market are themselves under debate: Proskauer’s Private Credit Default Index registered 2.73% for Q1 2026, while Fitch projects leveraged loan defaults reaching 4.5%-5.0% for the full year, a range that sits between the current 1.9% software-sector figure and the feared 8% AI disruption scenario that is driving exit pressure at OTIC.

Blue Owl is not the only manager that invoked the 5% cap in Q1 2026. Apollo, Ares, and BlackRock’s HPS all applied redemption caps during the same period, confirming that elevated withdrawal pressure affected the broader non-traded BDC industry.

Industry-wide private credit redemption data from Robert A Stanger cited in contemporaneous reporting confirmed that only approximately two-thirds of requested redemptions across the sector were fulfilled in the period, with Apollo, Ares, BlackRock’s HPS, and Morgan Stanley all invoking quarterly caps alongside Blue Owl.

The difference is degree. The industry average redemption request rate was 12.3% of outstanding shares. OCIC’s 21.9% nearly doubled that benchmark, and OTIC’s 40.7% exceeded it by more than three times.

| Fund / Manager | Q1 2026 redemption request rate | 5% cap invoked |

|---|---|---|

| Industry average (perpetual BDCs) | 12.3% | Varies |

| Blue Owl OCIC | 21.9% | Yes |

| Blue Owl OTIC | 40.7% | Yes |

| Apollo, Ares, BlackRock HPS | Below Blue Owl levels | Yes |

The fund-specific drivers behind Blue Owl’s outlier position are identifiable. OTIC’s portfolio carries concentrated software-sector lending exposure, and its shareholder base is weighted toward wealth channels and international investors, a composition that appears more sensitive to AI disruption headlines. By shareholder count, 90% of OCIC investors chose not to request redemption, reinforcing the interpretation that the pressure is concentrated rather than broad-based.

The peer comparison points toward a Blue Owl-specific story rather than the leading edge of a systemic private credit crisis, though the industry-wide cap invocations confirm that the underlying sentiment is not confined to a single manager.

Different investors in the same fund are living through structurally different versions of this crisis.

Bond investors in OCIC hold instruments that sit above equity in the capital structure. Their position is effectively collateralised against the fund’s underlying loan assets, with a substantial equity buffer absorbing losses before any bondholder impairment. OCIC’s leverage of approximately 0.7x versus the 2x BDC ceiling provides meaningful headroom.

Equity shareholders face a different reality:

BDC dividend sustainability failures elsewhere in the sector illustrate what structural stress looks like when it reaches the income statement: Oxford Square Capital’s Q1 2026 payout ratio reached approximately 210% of net investment income, with NAV collapsing 21.9% in a single quarter while the fund continued distributing capital it had not earned, a trajectory that contrasts sharply with Blue Owl’s current position of minimal net losses and leverage well within statutory limits.

The rating agencies are themselves split on where the risk sits. Moody’s shifted its outlook on OCIC to “negative” on 8 April 2026, citing the surge in redemption requests. One day later, on 9 April 2026, Fitch affirmed OCIC at ‘BBB-‘ with a stable outlook, reflecting confidence in the underlying portfolio’s credit quality.

The Moody’s-Fitch split is not background noise. It reflects a genuine, unresolved analytical disagreement about how much structural protections matter when sentiment-driven redemption pressure reaches this intensity.

For investors holding bonds and those holding equity in the same fund, the practical exposure is materially different, even as the headlines treat the crisis as a single event.

The static picture of Q1 2026 is now established. What happens next depends on a specific set of observable variables, and Q2 2026 represents the first meaningful data point for determining whether pressure moderates or compounds.

The most consequential analytical question facing investors in these funds is straightforward: is this a sentiment-driven event that corrects as AI disruption fears moderate, or the early stage of a fundamentals-driven event triggered by actual default acceleration? Q2 2026 data will begin to answer it.

Corporate refinancing pressures add a structural dimension to the timeline: a $15 trillion refinancing wall expected between 2026 and 2028 is already pushing institutional capital away from legacy leveraged loans and into hybrid AI debt structures, a reallocation dynamic that could accelerate software-sector default rates well before any direct AI-driven revenue disruption materialises at the company level.

The current data is not alarming. Eight basis points of net losses, a declining software default rate, 90% of OCIC shareholders choosing to stay, and leverage well within structural limits all point toward portfolios that remain sound by measurable standards.

The structural and sectoral risks are not trivially dismissible either. A $5.4 billion backlog of unmet redemption requests, a 40.7% request rate at OTIC, a rating agency split between Moody’s and Fitch, and a forward default scenario that could reach 8% if AI disruption proves as damaging as feared all represent genuine uncertainties rather than phantom concerns.

OCIC’s $36 billion in AUM provides Blue Owl with a scale advantage that smaller peers cannot replicate when absorbing sustained redemption pressure. Whether that advantage proves sufficient depends on what happens in the quarters ahead.

Investors need to hold two realities simultaneously: the underlying credit quality has not deteriorated, but the structural queue, concentrated shareholder pressure, and forward-looking AI disruption scenario are real enough that Q2 2026 will meaningfully shift the analytical picture in one direction or the other.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Forward-looking statements regarding default rates and redemption trajectories are speculative and subject to change based on market developments and portfolio performance.

The Blue Owl redemption crisis refers to $5.4 billion in investor withdrawal requests hitting two Blue Owl private credit funds in Q1 2026, far exceeding the 5% quarterly redemption cap built into non-traded BDC structures. It matters because it represents the largest visible stress test private credit has faced since the asset class began attracting retail capital at scale.

Blue Owl's funds are non-traded Business Development Companies (BDCs), which are structured to limit redemptions to 5% of outstanding shares per quarter to prevent forced sales of illiquid private loans at distressed prices. This means investors with unfilled requests must wait in a queue that carries forward into subsequent quarters.

Despite the scale of redemption requests, net losses across both funds stood at just 8 basis points as of Q1 2026, and the software-sector private credit default rate fell from 7.5% in January 2025 to approximately 1.9% in January 2026. The exit pressure appears driven by fear of future AI-related defaults rather than deterioration in current portfolio performance.

The industry average redemption request rate for perpetual BDCs in Q1 2026 was 12.3%, while Blue Owl's OCIC reached 21.9% and its technology-focused OTIC fund hit 40.7%, more than three times the sector norm. Apollo, Ares, and BlackRock's HPS also invoked quarterly caps during the same period, confirming industry-wide pressure, but at lower levels than Blue Owl.

The most critical signals to monitor include Q2 2026 redemption request rates for OCIC and OTIC, the trajectory of software-sector default rates relative to the feared 8% AI disruption scenario, and whether peer BDC filings from Apollo, Ares, and BlackRock's HPS show rising request rates suggesting broader systemic stress rather than a Blue Owl-specific problem.