SpaceX IPO Triples Saudi Aramco’s Record With $75 Billion Raise

5 hrs ago

Conducting a comprehensive Lululemon fundamental analysis reveals a severe divergence between the apparel manufacturer’s historical market dominance and its current operational reality. As of April 29, 2026, the company’s equity value has deteriorated sharply, recording a 29.29% Year-to-Date stock decline. This immediate drawdown is the culmination of long-term strategic misalignment and worsening financial metrics.

The underlying data demonstrates systemic operational challenges extending far beyond general retail market conditions. Financial markets have historically priced the company as a high-growth premium asset, but current internal projections suggest a structural shift in regional demand. Management is now confronting stagnant domestic sales, mounting inventory levels, and a highly public proxy campaign demanding immediate governance reform.

For investors, the gap between the brand’s historical halo effect and its present fundamental weakness requires careful examination. The current valuation reflects deep institutional uncertainty regarding the pending leadership transition and the board’s capacity to execute a commercial turnaround. What follows is an evidence-based assessment of the financial contraction, the mechanics of premium retail dilution, and the structural governance hurdles blocking operational recovery.

Founder Chip Wilson claims investors have suffered a staggering $17 billion equity loss over the past five years. This claim is entirely unsubstantiated, leaving the market capitalisation at approximately $16.39 billion today. The financial bleeding constitutes an ongoing structural issue rather than a temporary cyclical dip.

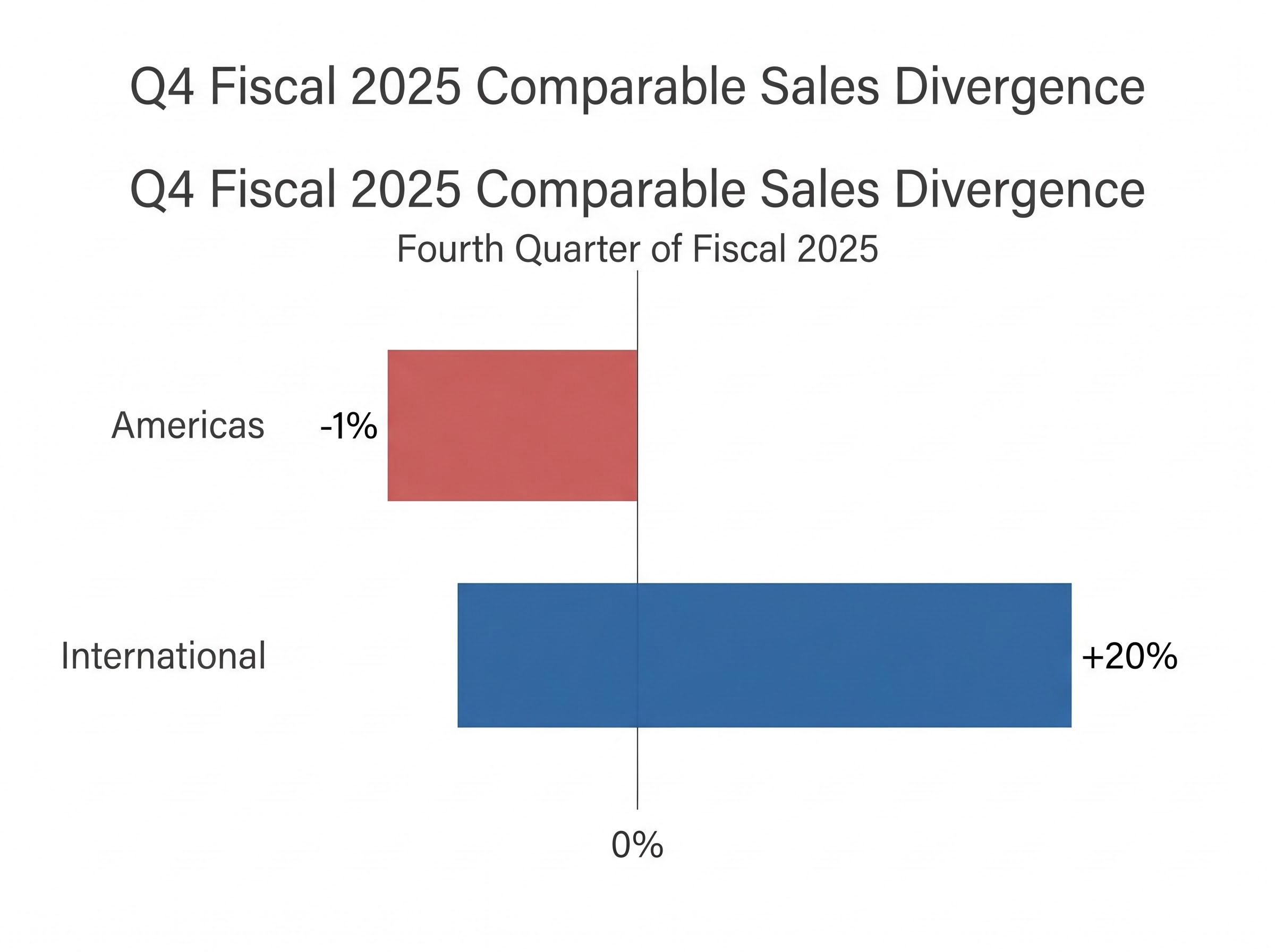

The core of this contraction stems from eight continuous quarters of regional stagnation across North America. In the fourth quarter of fiscal 2025, Americas comparable sales fell 1%, a severe warning signal for a region that historically drove the company’s premium multiples. International comparable sales rose 20% during the same period, but this overseas growth cannot fully offset the margin degradation occurring in the primary domestic market.

Profitability metrics confirm the severity of the operational strain. Net income fell sharply year-over-year, and gross margins absorbed significant pressure as the company struggled to clear excess merchandise.

The official Lululemon Q4 earnings commentary details how this margin pressure manifested as a 550 basis point contraction, correlating directly with the massive spike in unsold inventory.

| Financial Metric | Fiscal 2024 Result | Fiscal 2025 Result | Year-on-Year Variance |

|---|---|---|---|

| Net Income | $1.81 billion | $1.58 billion | Decline of 12.7% |

| Fourth Quarter Revenue Growth | Strong double-digit baseline | $3.6 billion | Increase of only 1% |

| Fourth Quarter Gross Margin | 60.4% | 54.9% | Contraction of 550 basis points |

| Year-End Inventory Levels | $1.44 billion | $1.7 billion | Increase of 18% |

The company’s internal projections for the upcoming year indicate the geographic divergence will persist. Management projects a 1-3% revenue decline specifically for the United States and North American markets in fiscal 2026. Financial analysts currently expect ongoing weakness in this region without any significant near-term improvement, forcing investors to re-evaluate the baseline assumptions underpinning the stock’s valuation.

Strategic drift occurs when high-end brands compromise their core exclusivity to chase short-term sales volume. Financial markets award premium multiples to athletic apparel companies based on their pricing power, tight inventory management, and strictly controlled distribution. When a company pivots toward mass-market appeal, it fundamentally alters this valuation equation.

Maintaining a premium multiple often mirrors the valuation dynamics seen in other high growth retail expansion models, requiring companies to justify their pricing power through flawless operational execution.

The initial phase of this pivot often creates a temporary revenue bump as new consumer demographics enter the purchasing funnel. However, the secondary phase inevitably brings long-term margin erosion. The 18% rise in inventory levels to $1.7 billion at the end of fiscal 2025 exemplifies this exact mechanism. Excess merchandise forces companies into discounting cycles, which subsequently trains affluent consumers to wait for sales rather than paying full price.

Management has designated North America a key priority for improvement, announcing a planned reduction in markdowns for fiscal 2026 to restore premium positioning. Identifying strategic drift requires monitoring three specific operational indicators that signal brand dilution.

Inventory bloat expanding faster than overall revenue growth. Heavy promotional cadences replacing full-price sell-through rates. * Disjointed brand collaborations targeting generic consumer bases instead of the core demographic.

Founder Chip Wilson escalated structural governance criticisms ahead of the 2026 annual shareholder gathering, shifting the market focus from operational failures to systemic oversight deficiencies. The founder issued a formal letter to shareholders on April 29, 2026, outlining severe grievances regarding the current board’s composition and its mismanaged executive search process.

According to reports, Lululemon resides among merely 10% of Standard and Poor’s 500 constituents still employing staggered board terms. This rare governance structure prevents shareholders from replacing the entire oversight committee in a single voting cycle, effectively entrenching incumbent directors. Negotiations between the activist investor and current leadership ultimately collapsed over restrictive terms, including leadership demanding a minimum financial security deposit.

These structural roadblocks prevent agile operational pivots. Institutional investors must navigate several core grievances outlined in the activist campaign.

The persistence of staggered board terms limiting shareholder voting authority. A closed-door executive search process lacking transparency. The continued deterioration of the core North American market under current oversight. Onerous financial deposit requirements designed to deter proxy challenges.

According to reports, the oversight committee features a heavy concentration of alumni associated with private equity firm Advent International. Four committee members reportedly share this specific institutional overlap. Principal director David Mussafer is scheduled to depart soon, yet the historical concentration of private equity influence continues to frustrate institutional shareholders seeking diverse operational perspectives.

For readers wanting to explore the structural governance dispute further, our comprehensive walkthrough of the proxy campaign details how the board is actively defending its incumbent directors and the specific mechanics of the upcoming universal proxy vote.

The market reception to incoming chief executive Heidi O’Neill quantifies investor apprehension regarding the company’s future direction. Following the announcement of her September 8, 2026, arrival, the company absorbed a single-day market capitalisation loss of approximately $2 billion. Analysts immediately questioned whether her specific operational background aligned with the brand’s historically affluent demographic.

The recent apparel partnership with The Walt Disney Company illustrates this strategic disorientation. The launch of a limited-edition Mickey Mouse apparel collection generated engagement metrics, but financial analysts categorised the collaboration as a tactical diversion. Institutional investors view the partnership as a volume-chasing measure rather than a core strategic alliance capable of reversing the domestic sales decline.

Management had previously emphasized agile merchandising and aggressive international expansion as primary pillars for recovery, making tactical diversions like this collaboration seem increasingly disjointed.

Reportedly, the current apparel chief executive also occupies a governance seat at Disney, complicating the optics of the partnership. These specific corporate decisions actively harm the stock price by reinforcing the market’s perception of ongoing brand dilution.

“Analysts view this collaboration positively for brand engagement, visibility, and sales diversification.” — Jefferies Financial Group analysis report.

The activist proxy campaign offers a specific turnaround roster via the gold universal proxy card, forcing investors to weigh the credibility of alternative directors against the incumbent board. The slate proposes three candidates possessing operational histories that directly address the strategic missteps currently plaguing the company.

Official SEC proxy statement filings formalise the nomination of these specific industry veterans, establishing a clear administrative pathway for shareholders to vote on the proposed boardroom overhaul.

Major institutional investors have responded cautiously to the proxy push. Entities like Vanguard and BlackRock have hesitated to endorse the slate fully, preferring internal stability. Conversely, proxy advisory firm Institutional Shareholder Services has recommended partial support for a board refresh, validating the activist’s claim that structural change is necessary.

By evaluating the specific turnaround experts proposed, investors can better assess the viability of a corporate recovery.

The apparel manufacturer remains on a collision course between entrenched governance structures and worsening fundamental metrics. International growth cannot indefinitely mask the systemic degradation of the core North American market. The upcoming leadership transition introduces significant execution risk, while the activist proxy push highlights the deep institutional dissatisfaction with the current corporate trajectory.

Corporate leadership transitions frequently rely on comprehensive strategic turnaround initiatives to rebuild institutional trust and correct legacy operational inefficiencies.

Financial projections are subject to market conditions and various risk factors. Past performance does not guarantee future results. The company recorded a comprehensive investor yield underperformance compared to rival medians over a twelve-month span, quantifying the immediate investment risk profile. Restoring the lost $17 billion in market equity will require either the new chief executive rapidly reversing the eight-quarter domestic stagnation, or the activist slate successfully dismantling the staggered board structure to force a complete strategic reset.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Lululemon's stock has declined 29.29% year-to-date as of April 29, 2026, due to stagnant domestic sales, mounting inventory levels, margin pressure, and an ongoing activist proxy campaign.

Strategic drift occurs when high-end brands compromise their core exclusivity to chase short-term sales volume, leading to margin erosion and undermining their premium valuation by impacting pricing power and tight inventory management.

Lululemon is experiencing eight continuous quarters of regional stagnation in North America, with comparable sales falling 1% in fiscal 2025, signaling a significant issue in its primary domestic market.

The activist proxy campaign criticizes Lululemon's staggered board terms, a non-transparent executive search process, the board's oversight of North American market deterioration, and restrictive financial requirements for proxy challenges.

In fiscal 2025, Lululemon's net income fell to $1.58 billion, fourth-quarter revenue growth was only 1%, gross margins contracted by 550 basis points, and year-end inventory levels increased 18% to $1.7 billion.