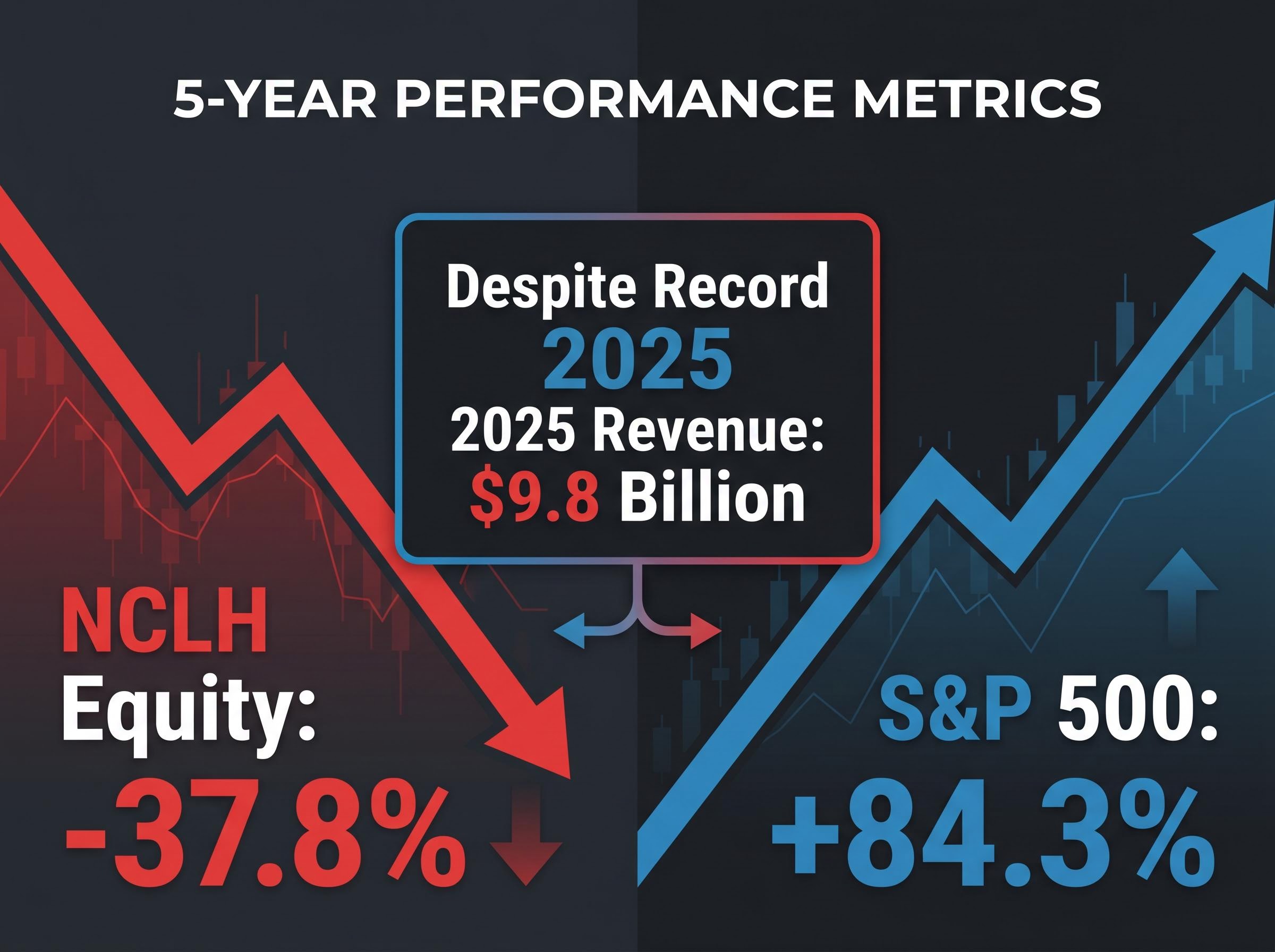

Any thorough NCLH stock analysis must reconcile a fundamental contradiction in the modern maritime travel sector. Norwegian Cruise Line Holdings generated an unprecedented $9.8 billion in total revenue for 2025, yet, according to market data, its equity has suffered a 37.8% decline over the past five years. According to financial reports, this capital destruction occurred while the broader S&P 500 index delivered an 84.3% gain for passive investors.

As of April 2026, the company is undergoing a massive corporate governance shift driven by activist investor Elliott Investment Management. This aggressive intervention creates a critical junction for potential equity purchasers evaluating the turnaround potential against historical underperformance.

What follows is a comprehensive breakdown of the company’s premium valuation, recent operating metrics, and direct peer comparisons. Examining these elements explains why many financial observers currently advise investors to delay initiating new positions until the restructured governing committee proves its strategic viability.

The Disconnect Between Historical Returns and Premium Pricing

The central tension surrounding Norwegian Cruise Line Holdings lies in the gap between its historical wealth creation and its current market pricing. Investors who held the equity over the past five years absorbed a 37.8% capital contraction. During this exact timeframe, benchmark passive investments tracking the S&P 500 returned 84.3%.

Even as passive benchmarks celebrate recent gains, the S&P 500’s all-time high masks underlying economic fragility and elevated energy costs that could disproportionately impact fuel-dependent travel equities.

Despite this stark value destruction, the equity continues to trade at a premium valuation multiple compared to its direct maritime competitors. According to market analysts, the earnings valuation multiple has contracted to 21 from an earlier peak of 24, but it still reflects expectations of aggressive future growth rather than historical reality.

This fundamental disconnect is the primary reason institutional observers are urging caution. Investors are essentially being asked to pay peak industry multiples for a historically underperforming asset based entirely on the promise of future operational restructuring.

Market Observer Consensus “Financial observers recommend delaying equity purchases until the revised governing committee outlines concrete strategic initiatives and demonstrates an ability to reverse the long-term margin compression.”

The gap between what the company has achieved and what the market is pricing requires careful scrutiny of the underlying operating metrics.

When big ASX news breaks, our subscribers know first

Decoding Cruise Valuations and Passenger Metrics

Before dissecting the specific 2025 financial results, market participants need a clear understanding of the levers that drive cruise line profitability. Top-line revenue expansion can often present a misleading picture of corporate health if unit profitability or cabin utilisation simultaneously drops.

A similar analytical approach is required across the broader consumer sector; for instance, a recent Dutch Bros stock analysis demonstrates how aggressive headline expansion frequently masks underlying margin compression if unit-level economics begin to deteriorate.

The hospitality industry relies on specific operational metrics to measure genuine financial success rather than just aggregate sales volume. Understanding these metrics helps investors independently evaluate whether the current pricing is justified.

Passenger Density: This metric calculates fleet occupancy based on the hospitality standard that assumes two guests occupy each available cabin. Profitability Per Available Traveller Day: This measures the actual yield or onboard spending extracted from each guest, stripping out structural operating costs. Trailing P/E Ratio: This compares the current stock price to actual earnings over the past 12 months, which currently sits at 19.34 for Norwegian Cruise Line Holdings. Forward P/E Ratio: This projects valuation against estimated future earnings, currently estimated at 7.35 but heavily dependent on aggressive analyst assumptions.

Calculations regarding top-line expansion also frequently omit international currency exchange fluctuations. Evaluating these specific data points prevents retail investors from making allocation decisions based solely on heavily marketed headline revenue figures. True financial health in this sector requires expanding margins, not just adding more ships to the water.

Parsing the 2025 Financial Results and Stagnating Utilization

The full-year 2025 financial results illustrate the exact revenue illusion that warrants investor caution. Total incoming capital expanded by 3.7% to reach an impressive $9.8 billion for the year. This aggregate growth included $2.24 billion in the final quarter, up from the $2.1 billion recorded in the first quarter of 2025.

| Reporting Period | Top-Line Revenue | Cabin Utilisation Rate |

|---|---|---|

| Q1 2025 | $2.10 Billion | 104.9% |

| Q4 2025 | $2.24 Billion | 103.5% |

| Full Year 2025 | $9.80 Billion | 103.5% |

While the total capital influx appears strong, the underlying operational metrics reveal structural weaknesses. According to company data, profitability per available traveller day did climb 2.4% to reach $301.52. However, corporate executives issued warnings regarding stagnating unit profitability for the current annual period.

The official SEC Form 10-K filings confirm that this slight yield increase was largely offset by rising baseline operating costs, which prevented the top-line expansion from flowing through to the bottom line.

The Impact of Dropping Passenger Density

The most troubling operational signal is the contraction in cabin utilisation. According to reported figures, the density metric dropped to 103.5%, falling directly from the prior benchmark of 104.9%.

This contraction directly impacts onboard spending and limits overall margin expansion. When ships sail with fewer third and fourth passengers in cabins, the highly profitable discretionary spending at bars, casinos, and specialty restaurants declines proportionately.

Furthermore, this dropping metric limits the company’s pricing power in a highly competitive global travel market. Shrinking organic demand forces management to choose between cutting baseline ticket prices to fill ships or accepting lower total passenger counts that drag down aggregate profitability.

The Elliott Management Catalyst and Overhauled Governance

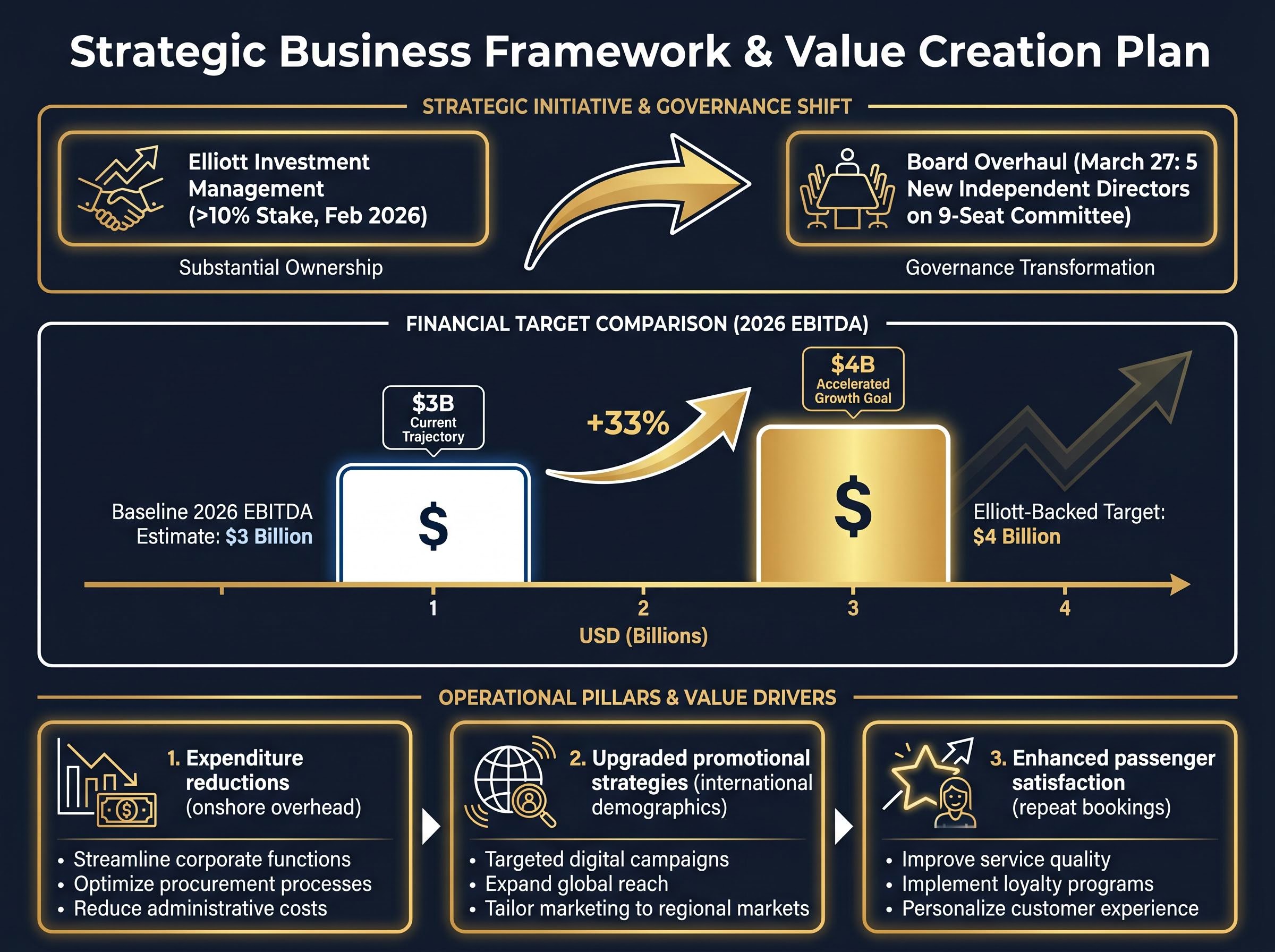

Historical pessimism is currently battling against the forward-looking disruption initiated by activist intervention. In February 2026, Elliott Investment Management accumulated a stake exceeding 10% in the company. This aggressive move immediately forced a conversation about leadership competence and structural capital allocation.

The pressure culminated in a March 27 cooperation agreement that overhauled the governance structure. This resulted in the appointment of five new independent directors to the nine-seat oversight committee. The new leadership roster features seasoned executives.

This restructured board has already implemented highly ambitious turnaround targets. Current baseline estimates project approximately $3 billion in 2026 EBITDA. In stark contrast, the newly instituted Elliott-backed operational target aims to generate over $4 billion in EBITDA by year-end.

The proposed initial turnaround initiatives focus on three distinct operational pillars:

- Aggressive expenditure reductions targeting redundant onshore corporate overhead.

- Upgraded promotional strategies designed to capture higher-yielding international demographics.

- Enhanced passenger satisfaction protocols aimed at increasing repeat booking rates.

This activist momentum represents the primary bullish catalyst for the equity. The introduction of leadership with proven experience at premium consumer brands suggests a shift toward prioritising guest yield over sheer volume. Investors must now evaluate whether these aggressive targets are realistic enough to warrant a speculative allocation before the turnaround fully materialises.

For readers wanting to understand the mechanics of this specific corporate governance shift, our full explainer on activist boardroom interventions details exactly how Elliott Investment Management secured its board seats and outmanoeuvred legacy leadership.

Industry Peer Comparisons and Wall Street Sentiment

Weighing this speculative turnaround requires grounding the analysis in cold market realities. Investors must compare these forward-looking promises against the proven valuation multiples of direct industry rivals. As of late April 2026, the comparative landscape presents a challenging argument for Norwegian Cruise Line Holdings.

The stock currently trades at $17.39, showing strong year-to-date momentum of +22.11%. However, its trailing multiple of 19.34 remains expensive compared to Carnival Corporation, which trades at $25.45 with a trailing multiple of just 11.22.

| Company | Stock Price | Trailing P/E | Forward P/E | YTD Performance |

|---|---|---|---|---|

| Norwegian (NCLH) | $17.39 | 19.34 | 7.35 | +22.11% |

| Royal Caribbean (RCL) | $252.65 | 16.19 | 14.10 | +8.94% |

| Carnival (CCL) | $25.45 | 11.22 | 11.26 | +16.25% |

Wall Street sentiment remains distinctly mixed amid fuel cost concerns and operational uncertainty. On April 27, JPMorgan maintained a neutral rating while lowering its price target to $18.00. Earlier in the month, UBS cut its target to $22.00.

These recent Wall Street analyst forecasts highlight a growing institutional scepticism regarding the timeline of the proposed recovery, with major firms lowering their expectations to align with prolonged operational challenges.

Broader consensus outlooks still range from $24.00 to $25.00, indicating some institutional belief in the turnaround. Yet, investors are essentially paying a premium multiple relative to safer alternatives like Carnival or the higher-quality operations of Royal Caribbean. Allocating capital here requires strong conviction that the new board can execute its mandate without succumbing to the broader macroeconomic pressures facing the travel sector.

Navigating the Buy or Wait Decision for NCLH Shares

The decision facing potential shareholders requires synthesising two fiercely competing forces. The undeniable activist momentum and strong top-line aggregate revenue are battling against declining passenger utilisation and stubbornly premium valuations.

The core recommendation from financial observers is to delay equity purchases until the new governing committee proves its strategy. The gap between the baseline $3 billion EBITDA estimate and the aggressive $4 billion activist target leaves entirely too much room for operational disappointment.

Investors should monitor upcoming quarterly earnings for specific turnaround signals. A true operational recovery will be marked by a reversal in the cabin utilisation decline and concrete evidence of onshore cost reductions taking effect. Until those specific metrics stabilise, the equity remains priced for a flawless execution that historical performance does not currently support.

Much like the current Starbucks turnaround initiatives aimed at restoring profitability through core operational efficiencies, Norwegian Cruise Line Holdings must prove it can execute fundamental business improvements rather than simply relying on industry-wide price inflation.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.