Lululemon Fundamental Analysis: the Price of Brand Dilution

1 hr ago

Global energy markets are fracturing under geopolitical pressure, placing immediate strain on domestic portfolios. In late April 2026, Brent crude breached $114 USD per barrel following sustained disruptions in the Strait of Hormuz.

For those managing capital, this environment presents a direct threat to purchasing power. Australian allocations currently sit in a crossfire between external energy shocks, a hawkish Reserve Bank of Australia pushing the cash rate to 4.10%, and slowing private sector output.

Developing a calculated inflation investing strategy is a strict requirement for preserving wealth in these conditions. An effective approach requires moving beyond basic savings accounts and deliberately structuring assets to absorb macroeconomic shocks.

This guide provides a systematic blueprint for protecting capital against currency debasement. By evaluating the structural advantages of fixed income, global equities, and cash equivalents, investors can position their portfolios to endure the current period of economic stress.

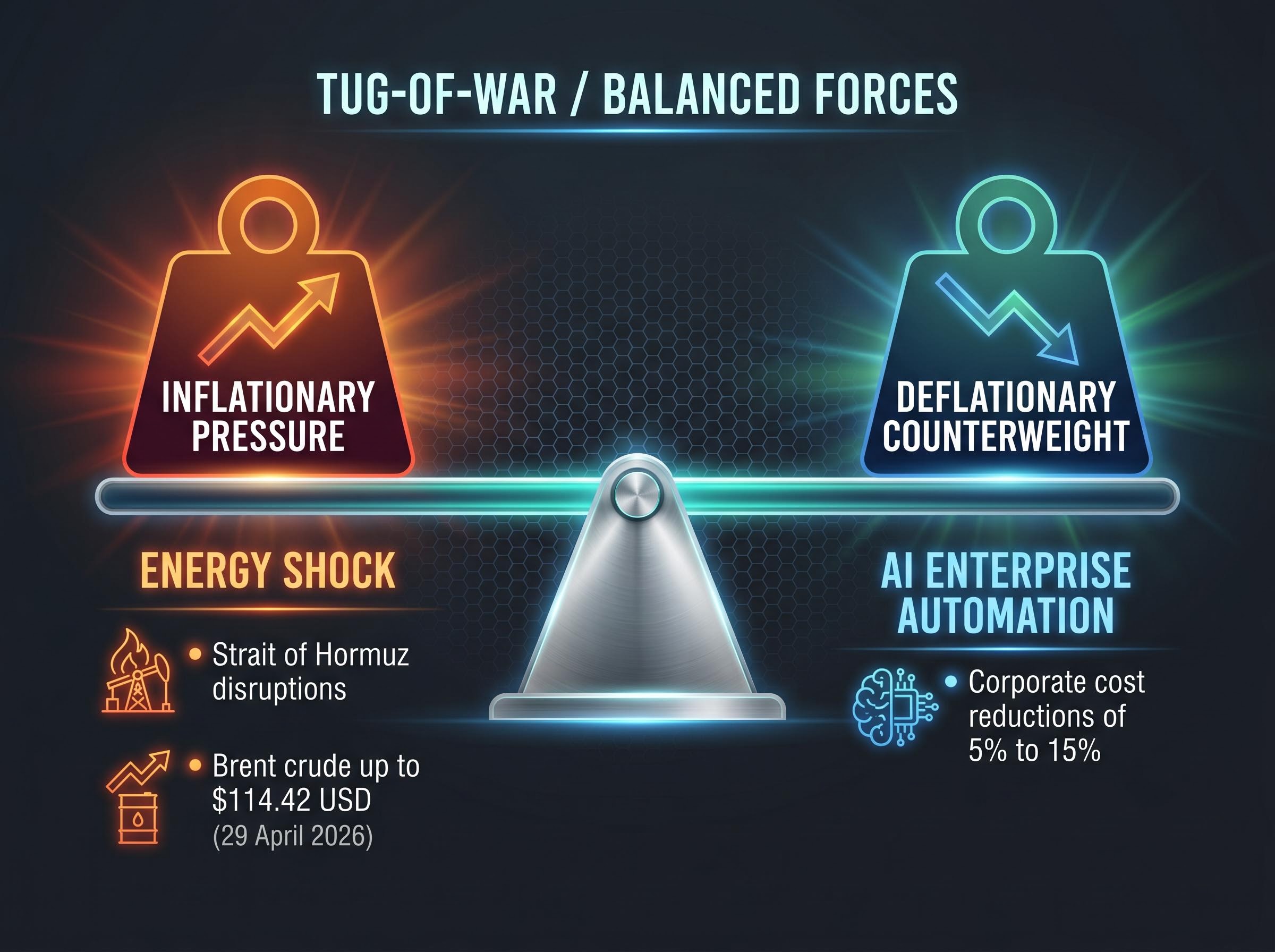

The geopolitical escalation involving Iran triggered a severe supply shock that has defined the financial environment of early 2026. Restricted access through the Strait of Hormuz immediately constrained global petroleum distribution. By 29 April 2026, Brent crude closed sharply elevated between $104.18 and $114.42 USD per barrel.

While energy prices apply direct upward pressure on consumer goods, artificial intelligence introduces a powerful deflationary counterweight. Efficiency gains from enterprise automation are projected to deliver corporate cost reductions of 5% to 15% across high-barrier industries. These technological efficiencies could help ease merchandise pricing, provided the massive energy requirements of data centres do not override the operational savings.

Goldman Sachs macroeconomic projections suggest that the widespread adoption of generative artificial intelligence could increase global output by 7 percent, delivering significant productivity enhancements that partially offset supply-side constraints.

Oil Market Backwardation A backwardation in oil futures indicates that traders are willing to pay a premium for immediate delivery. This pricing structure suggests expectations that current resource scarcity will resolve naturally over time.

These forward-looking projections regarding technological efficiency are subject to market conditions and broad adoption rates. However, understanding this tug-of-war between energy costs and technological disinflation helps contextualise current market volatility. Investors who recognise these conflicting forces are better equipped to avoid reactionary selling.

The Reserve Bank of Australia uses interest rate adjustments to intentionally restrict consumer spending when supply shocks elevate prices. On 17 March 2026, the central bank raised the cash rate to 4.10% in a direct attempt to cool demand.

This aggressive tightening is already restricting domestic output. The S&P Global Flash PMI Composite Output Index dropped to 46.6 in March 2026, confirming a contraction in the private sector. Historical patterns indicate that petroleum-driven price spikes temporarily elevate lending costs before economic slowdowns force authorities to shift their focus back toward stimulating growth.

Despite the slowing economy, the market expects further tightening. ASX futures currently price a 74% probability of a May rate increase, with forecasts suggesting the cash rate could peak at 4.85%. These financial projections remain speculative and subject to change based on incoming economic data.

Widespread price escalation manifests when systemic supply shortages collide with resilient consumer demand. This imbalance forces buyers to compete for limited goods, driving up nominal costs across the economy.

Sustained inflation acts as a silent tax on uninvested capital. When the cost of living outpaces the interest earned on traditional savings, the actual purchasing power of fiat currency continuously degrades.

Research demonstrates the severity of exceeding baseline targets for price expansion in advanced nations, showing a reduction in real GDP growth.

Supply chain bottlenecks that restrict the flow of international goods Elevated energy costs that increase manufacturing and transport overheads * Domestic currency depreciation that raises the cost of imported materials

The Taylor Rule is a mathematical formula suggesting monetary authorities must raise interest rates aggressively when baseline targets are breached. According to historical records, this aggressive response was demonstrated during the 1970s petroleum crisis and the 1980-1982 period, where United States rate hikes successfully reduced price escalation from 14% to 3%. Recognising this historical precedent shows that protecting capital through deliberate investment is a defensive necessity.

Federal Reserve historical analysis confirms that the aggressive tightening undertaken during the Volcker disinflation era successfully restored institutional credibility while demonstrating the practical application of mathematical policy rules.

Maintaining exposure to the stock market remains critical for long-term growth despite the volatility of 2026. Investors who liquidate their equity holdings during an energy shock immediately lock in losses and remove their primary engine for outpacing living costs.

The most effective defensive posture within the stock market involves the quality factor. This investment strategy targets companies exhibiting high return on equity, consistent profit margins, and minimal reliance on debt. The VanEck MSCI World ex Australia Quality ETF (QUAL) specifically screens for these characteristics, providing an upgraded portfolio foundation that resists macroeconomic stress.

Screening for quality metrics becomes especially vital when navigating extreme market concentration risks, as traditional cap-weighted benchmarks are currently heavily skewed by a handful of mega-cap technology firms.

Past performance does not guarantee future results, but quality-screened enterprises historically demonstrate the pricing power needed to pass rising costs onto consumers. Broader international exposure is also highly effective. According to fund data, the Vanguard MSCI Index International Shares ETF (VGS) distributes capital across more than 1,000 major global enterprises, diluting the risk associated with any single geographic region.

Demonstrated pricing power that allows the passing of input costs to end consumers Low corporate debt levels that insulate the balance sheet from rising interest rates * Consistent profit margins that indicate operational efficiency across business cycles

Holding unhedged international shares offers Australian investors a distinct structural advantage during global crises. When geopolitical tensions trigger a flight to safety, the United States dollar typically strengthens while risk-sensitive currencies like the Australian dollar depreciate.

This currency divergence acts as a natural shock absorber for domestic investors. As the Australian dollar weakens against the greenback, the local value of United States-denominated assets inherently increases, partially offsetting underlying share market declines.

The high-rate environment orchestrated by the Reserve Bank of Australia heavily penalises borrowers, but it simultaneously creates a powerful income engine for capital allocators. Elevated interest rates transform previously stagnant defensive instruments into reliable sources of yield.

Retail investors can capture institutional-grade returns through specific Australian exchange-traded funds without locking their capital into fixed-term deposits. These vehicles provide high liquidity, allowing investors to generate income while retaining the flexibility to deploy cash if equity markets correct further.

A deliberate defensive strategy distinguishes between the slight capital risk of corporate bonds and the absolute preservation of high-interest cash. Corporate fixed-income funds generate higher yields by holding company debt, while enhanced cash products strictly prioritise capital stability over aggressive returns.

| ETF Ticker | Asset Class | Current Price (AUD) | Approximate Yield |

|---|---|---|---|

| VBND | Corporate Fixed Interest | $40.70-$40.90 | 5.93% |

| CRED | Investment Grade Bonds | $22.68-$22.77 | 5.16% |

| ISEC | Enhanced Cash | $100.39-$100.42 | 4.19% |

| AAA | High Interest Cash | $50.13-$50.16 | 3.90% |

These yield figures represent the mid-April 2026 market environment. Investors should verify current distributions, as fixed income and cash yields fluctuate dynamically with central bank policy adjustments.

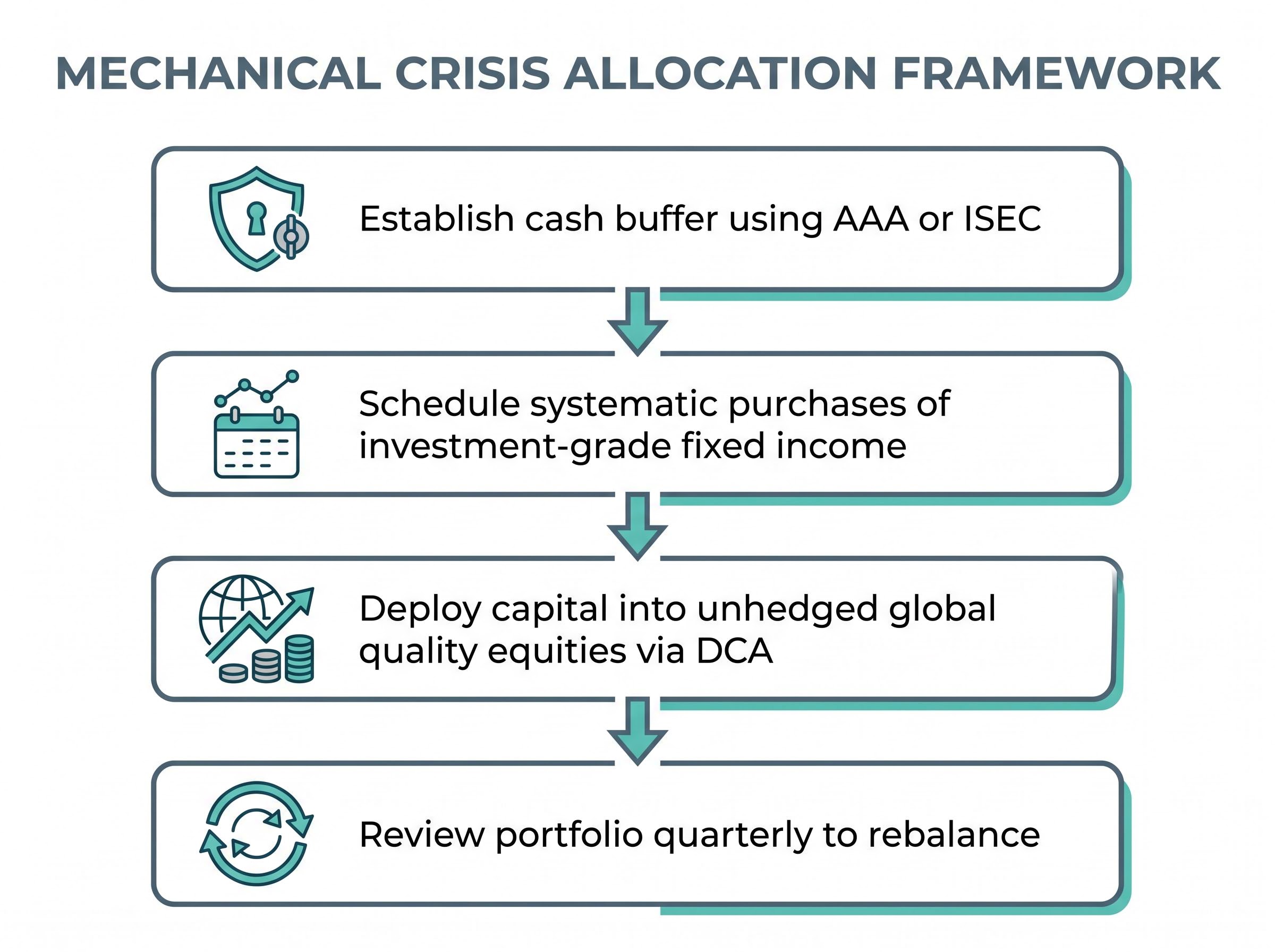

Geopolitical turbulence frequently paralyses market participants, causing them to abandon their financial strategies just when discipline is required most. A mechanical, emotionless allocation framework is the clearest solution for navigating unpredictable headlines from the Middle East.

Dollar-cost averaging provides a mathematical advantage during market contractions. By committing a fixed amount of capital at regular intervals, investors automatically purchase more units when asset prices fall, systematically lowering their average entry cost over time.

Modern defensive portfolios also require diversification beyond standard equities and cash. Traditional safe havens like precious metals are showing diminished effectiveness in the current cycle, prompting allocators to integrate commodities or Treasury Inflation-Protected Securities equivalents.

Scheduled capital allocation methodologies improve long-term accumulation outcomes, particularly when maintained during major drawdowns. This framework removes the pressure of attempting to perfectly time the market bottom.

Investors exploring advanced defensive positioning will find our detailed coverage of supply-driven inflation shocks highly relevant, as it examines why traditional non-yielding assets have underperformed and highlights the shifting dynamics of sovereign bonds.

A resilient portfolio in 2026 must actively balance the immediate income generation of defensive yields with the structural growth of quality global equities. The compounding pressure of the Strait of Hormuz conflict and the Reserve Bank of Australia tightening cycle guarantees near-term volatility, but reacting emotionally to these events damages long-term accumulation.

Market mechanics ultimately reward those who separate structural economic shifts from daily news cycles. The strategic use of unhedged international exposures, combined with systematic allocation into elevated bond yields, provides a mathematical defence against currency debasement.

Recognising these structural advantages, retail investors are aggressively rotating capital into international funds to bypass the concentrated volatility of the domestic resource and financial sectors.

Investors are encouraged to audit their current asset mix immediately. By implementing the mechanical accumulation strategies outlined in this framework, you position your capital to survive external shocks and capture growth as global supply chains eventually stabilise.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

An inflation investing strategy deliberately structures assets to absorb macroeconomic shocks and preserve purchasing power when the cost of living outpaces traditional savings returns.

Investors can protect capital by maintaining exposure to quality global equities with unhedged international exposure and by capitalizing on elevated yields from fixed income and enhanced cash equivalents.

Geopolitical energy shocks, like those in the Strait of Hormuz, create upward pressure on consumer prices, while artificial intelligence introduces a powerful disinflationary counterweight through efficiency gains across industries.

Unhedged international shares offer Australian investors a structural advantage, as a weakening Australian dollar against the US dollar can inherently increase the local value of US-denominated assets, offsetting market declines.

The article discusses Australian exchange-traded funds (ETFs) for corporate fixed interest like VBND and CRED, and enhanced cash products like ISEC and AAA, which offer yield while prioritizing capital stability.