The April 2026 Strait of Hormuz disruption has severed one of the world’s primary energy arteries, trapping approximately 20 million barrels per day of seaborne oil. This geopolitical escalation is fracturing global markets entirely differently than standard demand-driven recessions. Supply constraints are driving inflation upwards simultaneously with falling economic output. This dynamic renders conventional portfolio protection ineffective. Australian capital faces a specific dilemma, caught between a commodity-backed domestic currency and mounting local interest rate pressures.

This analysis provides a framework for evaluating safe haven investments during a supply-driven inflation shock. It examines the breakdown of traditional correlations across currencies, bonds, and precious metals. The sheer scale of the maritime blockade has bypassed financial system vulnerabilities to strike directly at physical logistics. Portfolio managers can no longer rely on central banks to engineer economic stability through rate cuts when energy prices dictate the inflation curve. Investors require specific methodologies to identify which protective assets actually preserve capital when physical bottlenecks dictate macroeconomic policy.

Quantifying the Strait of Hormuz Energy Bottleneck

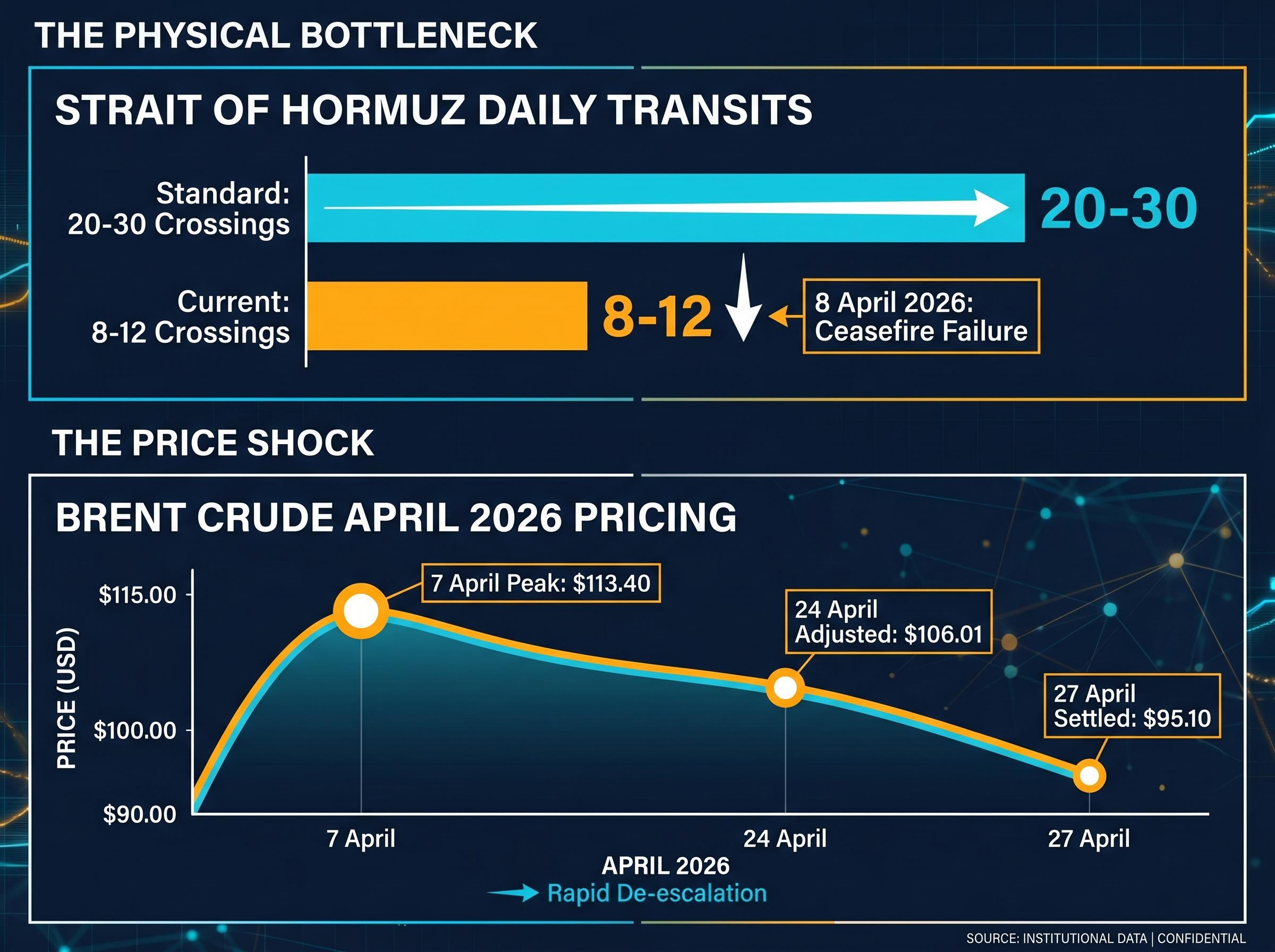

The current market panic stems entirely from a physical supply constraint rather than a structural flaw in the financial system. The failure of the 8 April 2026 ceasefire, mediated by Pakistan, highlighted the operational reality of the ongoing blockade. Maritime intelligence confirms that transit volumes are operating at just 40% to 60% of normal capacity. The seven-day moving average fell from the standard 20 to 30 daily transits down to approximately 8 to 12 crossings.

Maritime Industry Warning Sustained disruptions in the Strait of Hormuz carry profound risks for global supply chains, including prolonged high energy prices, structural inflation spikes, and heightened uncertainty surrounding future diplomatic resolutions or naval responses.

The physical bottleneck trapped roughly 20% of global seaborne oil, creating immediate commodity shockwaves:

Brent crude peaked at $113.40 per barrel on 7 April. Following limited reopenings, Brent adjusted to $106.01 on 24 April. Prices settled near $95.10 per barrel by 27 April. West Texas Intermediate (WTI) crude for April delivery traded at roughly $98.32 per barrel.

Investors cannot accurately position their portfolios without grasping this physical reality. The volatility stems directly from maritime vessel limitations, meaning financial hedges only work if they account for persistent energy scarcity.

When big ASX news breaks, our subscribers know first

Rethinking Defensive Assets in an Era of Supply-Driven Inflation

Historical crisis playbooks often lead investors toward catastrophic allocation errors during energy-induced shocks. Previous crises typically featured collapsing economic growth followed immediately by central bank rate cuts, which boosted sovereign debt valuations. The current scenario presents a fundamentally different mathematical problem. Global markets are facing stagflation risks, characterised by simultaneous high consumer prices and stagnant economic output.

The Central Bank Dilemma

Central banks are completely paralysed by the dual threat of slowing growth and rising energy input costs. They cannot cut benchmark lending rates to stimulate the economy because monetary easing would exacerbate the skyrocketing inflation caused by the oil shortage. This paralysis breaks the conventional 60/40 portfolio model.

In a standard recession, bonds act as a counterweight to falling equities. Today, both asset classes face simultaneous downward pressure. Rising inflation expectations push bond yields higher, destroying the capital value of existing fixed-income holdings.

An NBER analysis of bond-stock comovements confirms that periods of stagflation consistently force nominal government bonds and equities to move in tandem, effectively destroying the diversification benefits that passive investors typically rely upon.

Meanwhile, corporate profit margins compress under the weight of surging energy costs, driving equities lower. A supply-driven inflation shock requires a complete adjustment of capital preservation strategies. Protective assets must either benefit directly from commodity scarcity or offer yields high enough to offset purchasing power erosion. The traditional understanding of a recession assumes demand falls, taking prices down with it. A supply shock reverses this logic entirely, punishing defensive allocations that rely on deflation.

Global Currency Performance in the Energy Crisis

Foreign exchange markets often front-run equity markets during geopolitical shocks. The current crisis has exposed a deep paradox in traditional protective currencies, particularly regarding the Japanese yen. The yen carries a historical reputation as a defensive asset, and early April data showed investors migrating towards it alongside the Swiss franc to hedge against war-tied volatility.

However, Japan relies almost entirely on imported crude oil, creating massive fundamental tension. The currency’s historical premium is actively fighting against the nation’s severe energy vulnerability. The US dollar demonstrates clear structural advantages in this specific environment.

The breakdown of traditional safe haven asset correlations is evident when analyzing historically defensive currencies that now face immense fundamental headwinds. Investors must recognise that historical reputation cannot offset physical energy dependency in the current macroeconomic climate.

The dollar benefits from a flight to safety while simultaneously drawing strength from American domestic fuel production capabilities. Foreign exchange valuations are currently dictated almost entirely by a nation’s proportional reliance on imported petroleum. The US dollar continues to attract capital because it operates as a net producer.

| Major Currency | Energy Status | Historical Crisis Role | April 2026 Performance |

|---|---|---|---|

| US Dollar (USD) | Net Producer | Primary Reserve | Dominant strength |

| Japanese Yen (JPY) | Net Importer | Defensive Asset | Stressed near 159.84 |

| Swiss Franc (CHF) | Net Importer | Defensive Asset | Moderate inflows |

| Australian Dollar (AUD) | Net Exporter | Risk Proxy | Commodity supported |

The USD/JPY exchange rate is currently trading near 159.84, reflecting this specific stress point. Capital flows demonstrate that the yen is acting as a traditional safe haven and its pricing reflects sustained strength despite its energy import status. Understanding this dynamic helps investors evaluate international equities and unhedged global ETFs accurately.

The Australian Dollar and Domestic Yield Pressures

Australian capital allocators face a highly specific local reality. The Australian dollar is demonstrating notable resilience relative to net energy importers, driven entirely by the nation’s status as a major commodity exporter. The AUD/USD exchange rate sits at approximately 0.7077, avoiding the severe depreciation seen in import-heavy European and Asian nations.

Forex analysts note the currency is experiencing volatility directly tied to its commodity exposure rather than acting as a traditional defensive harbour. Analysts do not view the AUD as a commodity-backed safe haven, but this commodity reliance simultaneously acts as an inflation trap for the domestic economy. Local investors are currently navigating this complex environment without specific published guidance from major domestic institutions. The Reserve Bank of Australia has maintained a quiet posture regarding specific portfolio allocations, forcing investors to rely on global macro-hedging strategies.

Sovereign Debt Realities

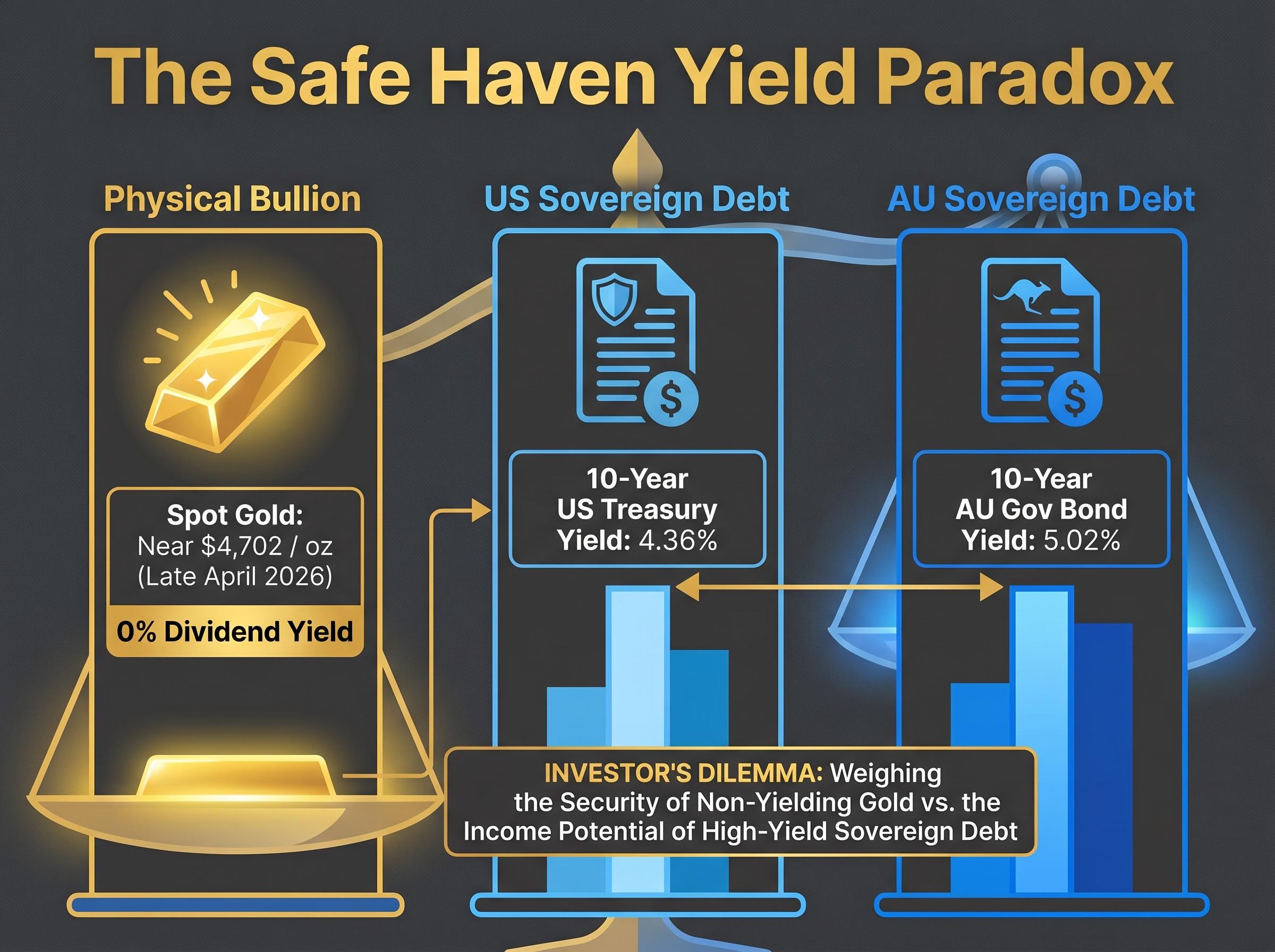

The true cost of the domestic inflation trap appears in the Australian sovereign debt market. The 10-year Australian Government Bond yield sits at a punishing 5.02%, significantly higher than the 10-year US Treasury yield at 4.36%.

This steep yield curve signals that bond markets expect the Reserve Bank of Australia to maintain restrictive monetary policy far longer than its global peers. Australian investors must balance the protective nature of their local currency against the harsh reality of domestic inflation eroding their purchasing power.

Investors exploring tactical restructuring options during this period will benefit from our comprehensive walkthrough of ASX portfolio defense, which examines companies with high return on equity and low debt burdens. Identifying these resilient local assets is essential when broad domestic indexes face severe macroeconomic headwinds.

The Precious Metals and Fixed Income Paradox

Geopolitical fallout has driven massive capital flows into physical bullion, establishing gold as the ultimate non-fiat protection mechanism. Spot prices reached record highs near $4,702 per ounce by late April 2026. Yet this surge in capital value contrasts sharply with the fundamental headwind facing gold. Precious metals offer no regular dividend distributions. Investors must weigh the massive opportunity cost of holding non-yielding bullion while sovereign yields remain exceptionally high.

A recent BlackRock analysis of gold performance demonstrates that bullion prices often accelerate alongside growing public debt burdens, providing institutional justification for holding zero-yield physical assets even when competing bond coupons remain elevated.

The Yield Paradox Investors seeking portfolio protection must choose between the capital preservation of zero-yield physical gold and the guaranteed, elevated income streams available in fixed-income securities, which currently offer multi-year high coupon rates.

This dynamic creates a complex environment for fixed-income allocations. Short-duration bonds are dropping in capital value as inflation expectations adjust upward. However, their periodic coupon payments provide a stabilising anchor for total returns.

The high distributions offered by risk-free sovereign debt actively compete with gold for defensive capital flows. Readers evaluating their holdings need to calculate whether the capital appreciation potential in precious metals outweighs the mathematical certainty of a 5.02% domestic bond yield. Financial models that automatically pair gold and bonds as identical defensive assets fail to capture this tension. Capital is currently rotating rapidly between the safety of physical bullion and the income generation of government paper.

Strategic Capital Allocation Matrix for the Current Crisis

Translating macroeconomic anxiety into a structured decision matrix is necessary for confident portfolio positioning. Broad global financial commentary recommends traditional defensive assets to weather supply-driven inflation, specifically pointing to US Treasuries, Japanese yen, Swiss francs, and defence sector equities. History demonstrates that markets typically recover once a clear trajectory toward conflict resolution emerges, often well before absolute peace agreements are finalised. To navigate the current energy shock, investors can evaluate their capital allocation through three sequential steps:

Implementing systematic equity investment strategies through dollar-cost averaging helps allocators capture discounted international opportunities while managing volatility. This methodical approach ensures capital is deployed efficiently even when market sentiment fluctuates wildly.

- Liquidity assessment: Maintain sufficient liquid capital to capture discounted equity positions when geopolitical tensions show verifiable signs of de-escalation.

- Yield capture: Balance liquid holdings with short-duration fixed-income securities to capture appealing interest distributions while waiting for market stabilisation.

- Commodity hedging: Evaluate exposure to defence sector equities and precious metals to protect against prolonged structural inflation.

This framework empowers readers to audit their current holdings logically. Holding strictly to outdated allocation principles guarantees underperformance when input costs dictate market direction. Deploying new capital strategically requires acknowledging that inflation hedges and cash equivalents currently serve distinct, complementary roles in a modern defensive portfolio. Investors must actively categorise their holdings based on whether they provide yield, capital protection, or growth potential during an energy shock. Passive management approaches leave portfolios exposed to severe drawdowns when central bank interventions are neutralised by external commodity prices.

Formulating a Resilient Path Forward

Supply-driven crises require entirely different protective strategies than standard economic downturns. The April 2026 energy shock demonstrates that traditional negative correlations between equities and bonds fail when maritime bottlenecks force inflation upward. Australian investors hold a highly unique position in this global environment.

Many institutional managers are successfully adopting barbell investment approaches that pair defensive commodity exposure with structural growth sectors like artificial intelligence. This strategic balance ensures portfolios are hedged against immediate energy shocks while remaining positioned for long-term technological disinflation.

They possess a commodity-backed currency that resists devaluation, but they simultaneously face elevated domestic bond yields that punish growth-oriented equities. Investors should urgently review their fixed-income duration and international currency exposures before the next geopolitical escalation occurs. Adjusting portfolios to account for persistent energy scarcity offers the clearest mechanism for capital preservation.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.