Understanding exactly what inflation is as a macroeconomic concept requires nothing more than a routine trip to the supermarket. A standard basket of groceries that cost $100 five years ago now demands significantly more capital to secure the exact same goods. This silent expansion of retail prices functions as an invisible tax on household wealth and everyday purchasing power.

The Cost of Erosion “When purchasing power erodes, it acts as a silent tax on everyday capital, requiring consumers to spend progressively more to maintain the exact same standard of living.”

Price stability forms the foundation of modern economic health across all global markets. When broad price increases run unchecked, they destroy consumer confidence and severely distort corporate investment decisions. To prevent this destabilisation, advanced economies generally target a steady price growth rate of approximately 2.0%.

The following framework provides a complete understanding of how monetary authorities manipulate the broader economy to protect the value of your money. By examining historical precedents and modern structural drivers, investors can better position their portfolios for long-term resilience.

Decoding the Mechanics of Broad Price Expansion

Before examining how central banks intervene in the economy, it is necessary to understand the fundamental mechanisms that drive broad price increases. At its core, the problem occurs when the supply of money and credit expands faster than the underlying economic output. This dynamic forces buyers to compete for limited resources, driving up the baseline cost of living and doing business.

Economists broadly categorise these price expansion mechanisms into four primary drivers:

Demand-Pull: This occurs when aggregate consumer and corporate demand outpaces the economy’s production capacity, meaning too much money chases too few goods. Cost-Push: This is driven by rising input expenses, such as increased wages or raw material prices, which manufacturers then pass directly to end consumers. Built-in Expectations: This stems from adaptive worker expectations, where employees demand higher wages to match rising living costs, triggering a self-perpetuating wage-price spiral. Monetary Expansion: This happens when central banks increase the money supply at a rate that significantly exceeds gross domestic product growth.

These mechanisms carry severe macroeconomic consequences when left unmanaged. According to International Monetary Fund calculations, when price growth is excessive in developed nations, real gross domestic product contracts.

How Economists Measure the Damage

Financial authorities rely on two primary barometers to measure economic heat and track the erosion of purchasing power. The Consumer Price Index measures retail-level changes by tracking a representative basket of goods and services purchased by typical households. Conversely, the Producer Price Index tracks wholesale-level pricing changes, offering a leading indicator of costs that will eventually reach the consumer.

The BLS Consumer Price Index methodology relies on continuous expenditure surveys to ensure the selected basket of goods accurately reflects current consumer buying patterns rather than outdated consumption models.

The data captured by these indices consistently reveals a disproportionate impact on lower-income demographics. These households allocate a significantly larger percentage of their available capital to basic necessities like food, housing, and energy. Consequently, when the consumer index rises, the most vulnerable demographics suffer the sharpest reduction in their actual standard of living.

When big ASX news breaks, our subscribers know first

Central Bank Arsenals and the Mathematics of Demand Destruction

When broad price expansion threatens economic stability, national monetary authorities deploy cold mathematical logic to restrict the broader economy. The primary mandate of a central bank is to maintain price stability while supporting maximum sustainable employment. To achieve this, their most effective tool is the manipulation of benchmark borrowing costs.

Raising the baseline cost of debt sets off a deliberate chain reaction designed to suppress consumer purchasing and halt corporate expansion. When central banks increase their target rates, retail banks immediately pass these higher costs onto borrowers.

The step-by-step chain reaction of a single interest rate hike typically unfolds in the following sequence:

- The central bank raises the overnight borrowing rate charged to commercial banks.

- Commercial institutions immediately increase their prime lending rates to protect profit margins.

- Consumer mortgage rates, auto loans, and credit card yields adjust upwards.

- Corporate borrowing becomes more expensive, leading companies to delay expansion and hiring.

- Consumers reduce discretionary spending as debt servicing consumes more of their monthly income.

- Aggregate demand falls across the economy, forcing sellers to halt price increases to attract scarce buyers.

Policymakers often rely on mathematical frameworks like the Taylor Rule to determine the exact severity of these interventions. Under a standard Taylor Rule directive, policymakers increase baseline borrowing costs when the inflation rate exceeds the official target. This aggressive formula ensures that interest rates rise fast enough to genuinely cool demand, rather than merely keeping pace with rising prices.

Applying these formulas becomes increasingly difficult when sudden energy supply disruptions squeeze consumer spending, effectively trapping policymakers in a static holding pattern.

The Volcker Shock and Historical Stabilisation Blueprints

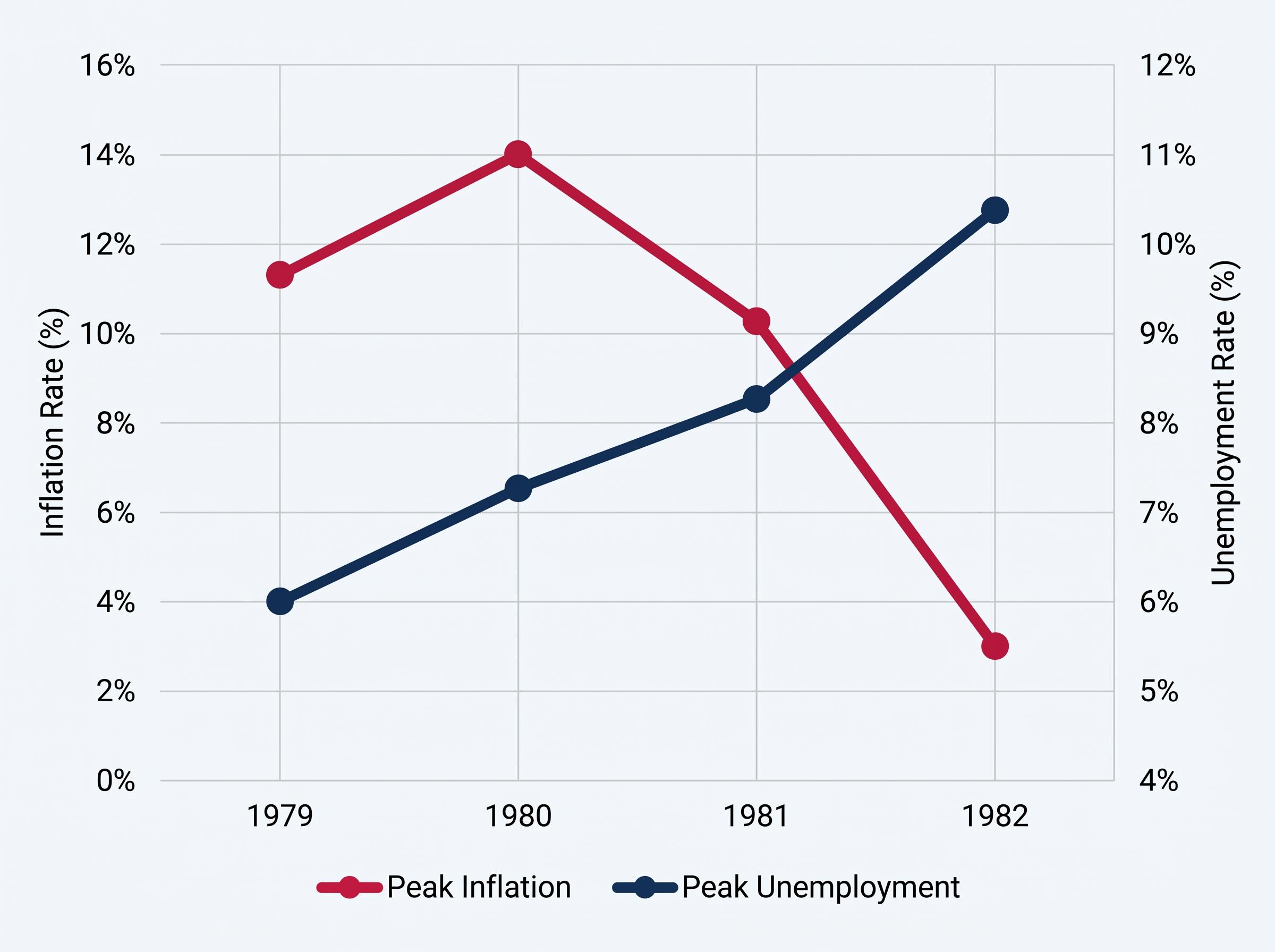

Theoretical policy frameworks trace their origins to the severe economic pain required to break entrenched price expectations during previous historical crises. The late 1970s and early 1980s serve as the ultimate case study in dismantling a deeply rooted wage-price spiral. Under Federal Reserve Chair Paul Volcker, the United States central bank executed a critical paradigm shift in October 1979.

Rather than simply targeting interest rates, the Volcker-led Federal Reserve shifted to aggressive money supply targeting. This approach contrasted sharply with the more gradual stabilisation strategies adopted by global central banks throughout the 1990s. The 1980s intervention demonstrated the delicate trade-off policymakers face between halting price escalations and inducing severe unemployment contractions.

The United States Federal Reserve intervention between 1980 and 1982 successfully crushed price growth from double-digit levels. However, this mathematical victory required pushing up the national unemployment rate, devastating manufacturing sectors and triggering a severe recession.

| Timeline | Peak Inflation Rate | Peak Unemployment | Policy Action |

|---|---|---|---|

| 1979 | 11.3% | 6.0% | Shift to money supply targeting |

| 1980 | 14.0% | 7.5% | Aggressive monetary contraction begins |

| 1981 | 10.3% | 8.5% | Interest rates pushed to record highs |

| 1982 | 3.0% | 10.8% | Price stability achieved amid severe recession |

By studying these historical precedents, modern analysts gain the perspective needed to separate normal monetary tightening cycles from unprecedented economic shocks. The 1980s blueprint proved that central bank credibility remains the most vital asset in resetting consumer expectations.

New Structural Drivers Shaping the 2026 Global Economy

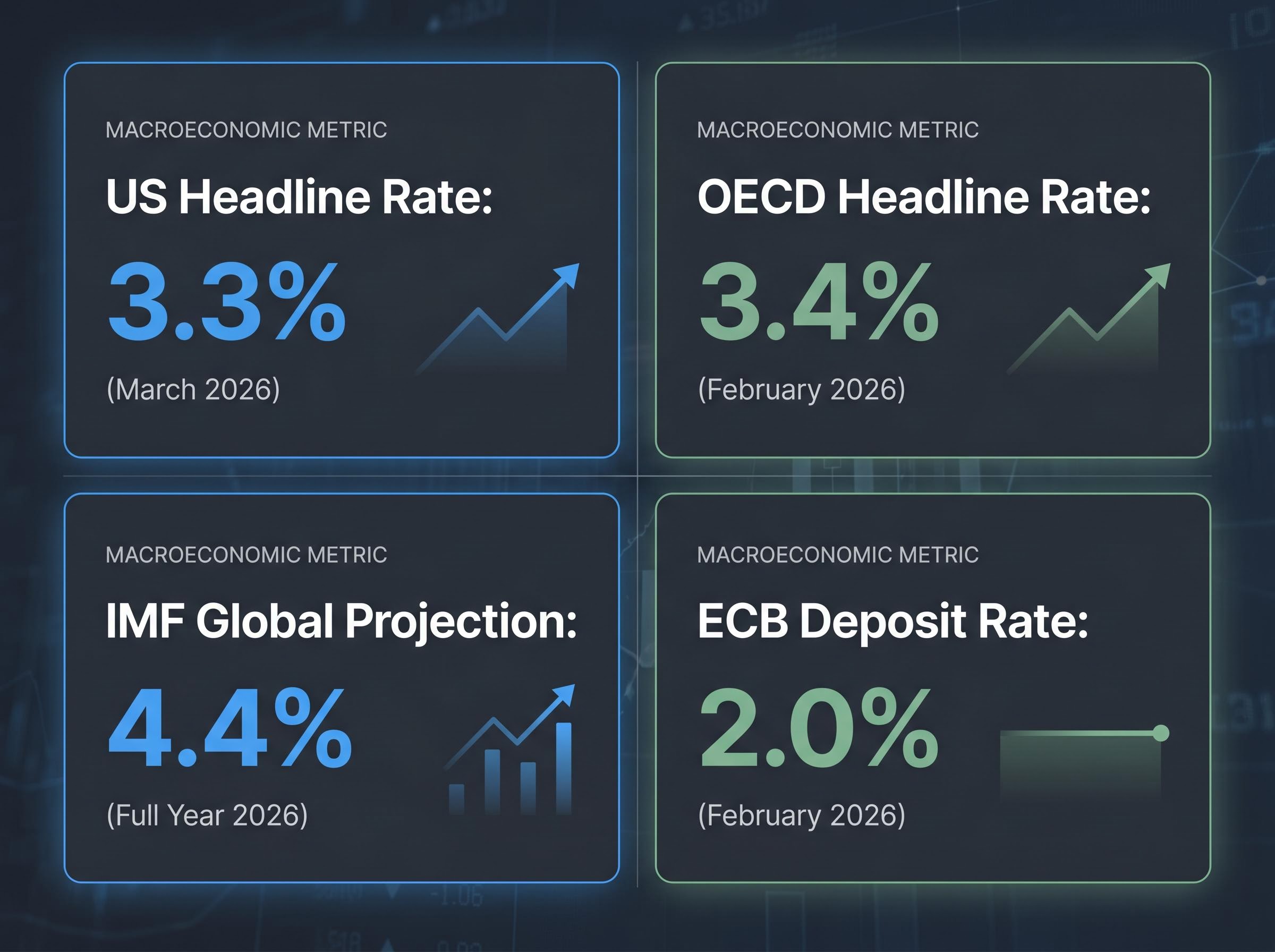

The clear lessons of the 1980s now face the complex realities of the April 2026 global market environment. Modern central banks find themselves delicately balancing growth requirements against remarkably sticky price pressures. Global metrics reflect this persistent tension, with the United States headline rate sitting at 3.3% in March 2026.

Similarly, the OECD nations registered a headline rate of 3.4% in February 2026. Looking ahead, the International Monetary Fund projects global headline price growth to reach 4.4% for the full year of 2026. These elevated baselines are driven by new structural forces that complicate traditional central banking models and disrupt old economic assumptions.

The April 2026 World Economic Outlook projections confirm that persistent geopolitical friction and shifting global supply chains will likely keep baseline manufacturing costs elevated throughout the forecast period.

Geopolitical trade barriers and massive supply chain realignments away from China are permanently elevating baseline manufacturing costs globally. Simultaneously, the rapid integration of artificial intelligence is altering global energy consumption patterns, creating a highly complex macroeconomic variable.

The AI Paradox “Artificial intelligence presents a dual-sided dynamic for the modern economy. It functions as a powerful disinflationary productivity tool for corporate margins, while simultaneously acting as an inflationary force due to the massive energy demands of its required data infrastructure.”

Central Bank Balancing Acts in 2026

Faced with these structural shifts, major monetary authorities are executing highly coordinated hold positions. The European Central Bank maintained its deposit rate at 2.0% in February 2026, matching the cautious holding patterns of both the Federal Reserve and the Bank of England.

These institutions are actively monitoring commodity markets for forward-looking signals. For instance, recent petroleum market backwardation suggests that institutional traders expect current supply disruptions to resolve quickly. This pricing structure gives central banks the temporary breathing room needed to maintain their current interest rate plateaus without triggering immediate recessions.

Capital Allocation Frameworks for Volatile Pricing Environments

Understanding macroeconomic theory holds little value unless it translates into highly actionable financial defence. Modern portfolio resilience requires significant adaptation, given that traditional safe havens like standard fixed-income securities have lost their historical effectiveness. Investors must develop concrete defensive strategies to maintain control over their financial trajectory in a high-cost environment.

Financial professionals increasingly advise a shift toward alternative assets and broad international equity exposure to counter domestic currency dilution. Equities remain a primary defensive tool, provided investors select companies possessing strong pricing leverage that can pass rising input costs directly to consumers. Additionally, maintaining systematic periodic investing is vital to avoid the psychological pitfalls of emotional market timing.

To navigate the 2026 macroeconomic climate, analysts suggest focusing on the following asset classes and investment vehicles:

Sovereign Debt: Securing predictable yield through short-duration government bonds to minimise interest rate risk. High-Yielding Deposits: Maintaining liquid capital in high-yielding deposit accounts to capture elevated central bank base rates. Alternative Assets: Allocating capital to infrastructure and real estate investment trusts that feature inflation-linked revenue contracts. Commodity Equities: Taking positions in the energy and materials sectors that directly benefit from supply constraints. * Quality Factor Equities: Focusing on large-capitalisation companies with minimal debt and high free cash flow generation.

This framework transforms theoretical economic knowledge into practical capital protection. By diversifying away from conventional, highly correlated assets, investors can build a protective barrier against the persistent erosion of purchasing power.

For readers wanting to adapt their portfolios to complex supply constraints, our comprehensive walkthrough of macro investing rules examines how energy shocks reshape currency markets and dictate defensive rotation strategies.

The Ongoing Pursuit of Global Economic Equilibrium

National monetary authorities must constantly synthesise the delicate balance between fostering economic growth and preventing severe currency debasement. While the underlying drivers evolve from the oil shocks of the 1970s to the artificial intelligence energy demands of 2026, the fundamental mechanics remain entirely constant. The continuous interplay of supply, demand, and overall money supply dictates the trajectory of global wealth.

Historical data confirms the inevitability of the macroeconomic cycle, demonstrating that aggressive monetary tightening eventually gives way to growth stimulation once target rates are achieved. Central banks will pivot toward rate reductions when aggregate demand sufficiently cools, requiring constant portfolio evaluation.

Navigating these cycles requires investors to remain highly adaptable in their personal financial planning. This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions, as past performance does not guarantee future results.