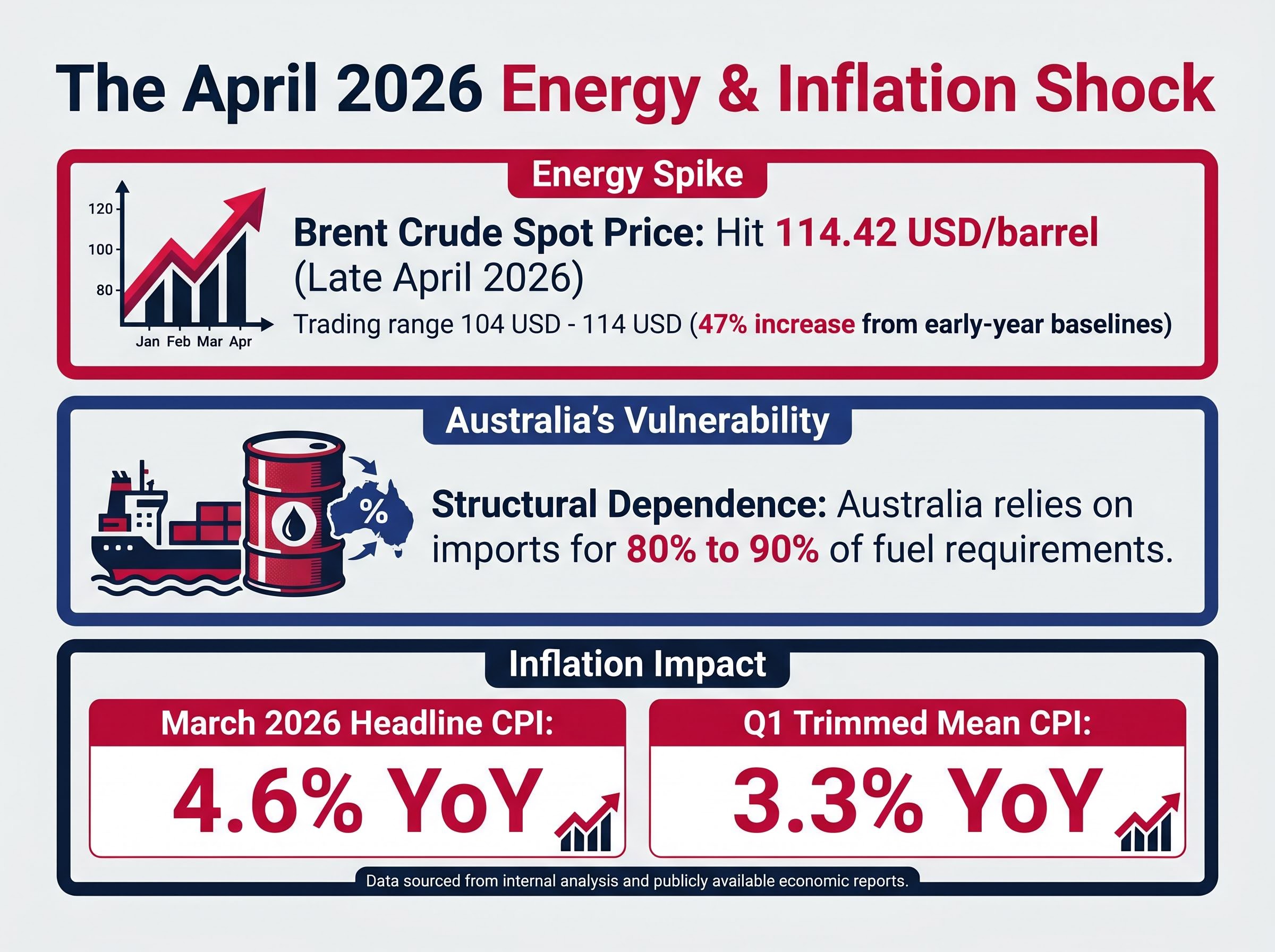

Spot prices for Brent crude hit 114.42 USD per barrel in late April 2026, generating immediate panic across global markets. Yet beneath the surface of this energy shock, financial markets are pricing in a completely different long-term reality. This divergence between immediate commodity spikes and forward-looking market signals defines the current trajectory for inflation and interest rates in Australia.

The closure of the Strait of Hormuz has pushed local price growth well above the target set by the Reserve Bank of Australia. However, forward indicators suggest this specific geopolitical crisis will be transient.

Extreme market backwardation and broader global macroeconomic forces indicate that the upcoming cycle of monetary tightening could ultimately reverse. These signals suggest rate reductions remain a strong possibility within a 6-12 month horizon. This analysis provides a framework for interpreting how immediate supply shocks interact with structural economic trends to dictate future monetary policy.

The Strait of Hormuz Squeeze and Australia’s Headline Resurgence

The Middle East conflict and the subsequent closure of the Strait of Hormuz have triggered severe disruptions across global energy supply chains. Brent crude is currently trading between 104 USD and 114 USD per barrel. This represents an approximate 47% increase from early-year baselines, creating an immediate supply squeeze that translates directly into higher consumer costs.

Australia remains exceptionally vulnerable to this specific geopolitical shock compared to other developed economies. The nation relies on foreign imports for 80% to 90% of its fuel requirements. This heavy structural dependence means international energy spikes pass immediately into the domestic economy, leaving policymakers with limited tools to shield consumers from the impact.

The DCCEEW energy commodity trade statistics confirm that this structural imbalance leaves the nation acutely exposed to foreign market volatility, as domestic refineries cannot fully buffer the pricing impact of international crude shortages.

The sudden acceleration in energy costs has triggered a sharp resurgence in local consumer price data. Investors face a macroeconomic environment where the fundamental drivers of market volatility are external rather than domestic.

Headline consumer price index (CPI) accelerated to 4.6% year-over-year in March 2026. Quarter one trimmed mean CPI reached 3.3% year-over-year. June quarter projections indicate headline inflation will range between 4.2% and 4.6% annually. The Commonwealth Bank of Australia forecasts a 1.0% trimmed mean gain for the June quarter.

The severity of this price acceleration explains the sudden shift in local economic sentiment. Portfolio managers must now account for a renewed inflationary cycle driven entirely by offshore supply constraints.

When big ASX news breaks, our subscribers know first

The Silent Deflationary Counterweights Preparing to Suppress Prices

Powerful macroeconomic forces are currently operating beneath the surface of the energy shock. While the petroleum crisis dominates immediate headlines, massive structural trends make the current cost spike look increasingly isolated. Rapid technological advancements and shifting global trade patterns are exerting severe downward pressure on broad consumer prices.

In particular, rapid AI integration is structurally lowering operational costs across service sectors, providing a crucial long-term buffer against rising physical commodity expenses.

Economists are currently excluding these structural factors from their near-term forecasts due to the immediacy of the geopolitical conflict. The analytical focus remains heavily anchored on the Hormuz disruption and the resulting supply-side inflation. Once oil markets stabilise, these underlying deflationary counterweights will dominate the macroeconomic narrative and force a reassessment of long-term yields.

Artificial intelligence productivity gains are serving as a major deflationary force across multiple service and knowledge sectors. American trade restrictions have resulted in the global diversion of discounted Chinese manufacturing exports, suppressing international goods pricing. * Decreasing American property rental costs, driven by massive new housing inventory, are serving as a leading indicator for global property trends.

These forces explain why long-term bond markets are pricing in a return to lower yields despite current headline panic. The underlying structure of the global economy is shifting toward cost suppression rather than sustained inflation. This reality creates a striking contrast with the temporary energy squeeze dominating current central bank policy decisions. Investors looking past the immediate quarter are factoring these silent counterweights into their long-term allocation strategies.

Decoding Backwardation: Why Futures Markets Reject a Permanent Crisis

A backwardation in commodity futures is Wall Street’s clearest signal that traders expect a crisis to resolve rather than escalate. When near-term contracts price higher than longer-dated ones, buyers are paying a premium for immediate delivery. This inversion of the futures curve indicates that immediate supply expenses vastly exceed long-term pricing expectations.

The petroleum futures market is currently in a state of extreme backwardation. Traders are pricing the Hormuz closure as an acute, temporary shock rather than a permanent structural deficit in global energy markets. By understanding this mechanism, investors gain a sophisticated lens to interpret commodity pricing beyond short-term headlines. The market is mathematically encoding its expectation that international supply chains will eventually normalise.

Institutional CME Group commodities market analysis validates that such severe curve inversions typically signal an imminent normalisation of supply chains, giving commercial participants confidence that current spot premiums will fade.

Historical Precedents for Supply Normalisation

Historical data complicates the immediate panic surrounding the energy spike. G7 economy market pricing indicators show that when supply constraints elevate borrowing costs, those metrics typically decline within six to 12 months.

Historical Market Analysis “Past performance does not guarantee future results. However, historical G7 economic data demonstrates that interest rates elevated by acute supply constraints typically reverse once the initial supply shock normalises.”

This transient shock expectation contrasts sharply with the unanchored inflation periods of the 1970s. The current environment lacks the entrenched wage-price spirals that defined previous decades of severe economic stagnation.

International Monetary Fund research notes that a complete absence of price growth produces adverse economic consequences, highlighting the delicate balance central banks must maintain. The market views the current environment as a temporary supply squeeze rather than a permanent macroeconomic shift.

The Reserve Bank Dilemma Amid a 74 Percent Hike Probability

The Reserve Bank of Australia faces a complex monetary dilemma amid these competing economic forces. The central bank must manage immediate supply-side inflation without triggering a severe economic contraction. Reserve Bank Deputy Governor Andrew Hauser has warned that the current policy stance may not be restrictive enough to achieve the target range.

This reactionary posture highlights the fragility of further tightening in an economy already straining under elevated borrowing costs. The Taylor Rule benchmark frames the massive scale of rate increases theoretically required to crush current price growth. This widely monitored metric suggests a rate elevation is theoretically necessary for surplus inflation.

| Metric | Current April 2026 Level | Market Implication |

|---|---|---|

| RBA Cash Rate | 4.10% | Base borrowing costs remain elevated with upward pressure |

| 3-Month Bank Bill Rate | 4.35% | Short-term yields reflect sustained tight monetary conditions |

| May 2026 Hike Probability | 74% | Financial markets anticipate immediate further tightening |

The actual path the central bank might take will likely be more measured than theoretical models suggest. Australian financial markets are currently pricing a 74% probability for a May 2026 rate hike. This provides clear near-term monetary policy expectations, helping investors prepare for an imminent higher-for-longer yield environment before an eventual pivot. A careful assessment of these metrics allows market participants to calibrate their expectations against actual central bank mandates.

International banks are also closely monitoring critical equity market thresholds, as sustained energy costs near these trigger points often foreshadow broad valuation corrections that could further restrict a central bank’s policy flexibility.

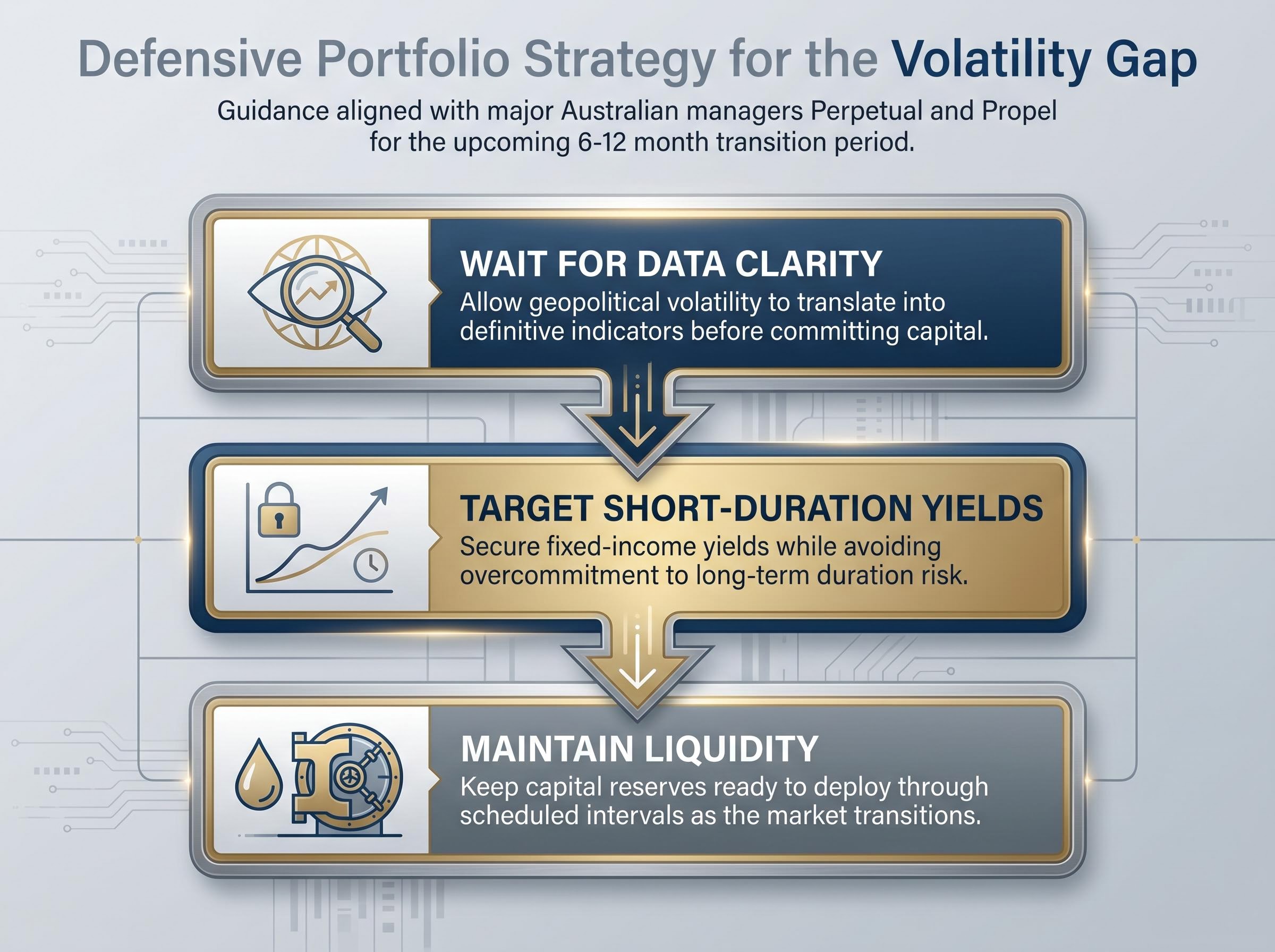

Navigating Australian Portfolios Through the Volatility Gap

Translating this complex macroeconomic conflict into practical defensive posturing is critical for capital protection. Major Australian portfolio managers are currently advocating a cautious, wait-and-see approach as the situation develops. Perpetual and Propel have issued guidance advising against rushing into aggressive assumptions before fully digesting quarter one consumer price figures.

The current cycle has challenged traditional defensive assets, forcing a recalibration of established allocation models. Portfolio managers highlight the necessity of securing elevated fixed-income yields now, while remaining highly cautious regarding duration risk. Heavy reliance on imported fuel introduces significant recession risks tied to a consumer spending slowdown and potential rationing. This creates a volatile gap that requires disciplined capital allocation strategies from domestic investors.

- Wait for concrete data clarity before committing capital, allowing the current geopolitical volatility to translate into definitive economic indicators.

- Secure short-duration fixed-income yields to capitalise on the current restrictive monetary policy without overcommitting to long-term duration risk.

- Maintain liquid capital reserves to deploy funds through disciplined, scheduled intervals as the market transitions.

This framework ensures investors can protect their wealth during the anticipated six to 12 month transition period. Financial projections are always subject to market conditions, but maintaining liquidity offers a buffer against immediate shocks. Australian portfolios structured around these defensive principles are better positioned to absorb near-term volatility while awaiting the eventual policy pivot.

For local investors looking to practically implement these defensive allocations, our dedicated guide to ASX portfolio protection outlines a comprehensive strategy for identifying companies with strong pricing power and deploying capital through disciplined risk rebalancing.

The Inevitable Pivot from Supply Shock to Rate Relief

The journey from the immediate April 2026 inflation panic to the ultimate resolution of this supply shock will require careful portfolio navigation. The Reserve Bank of Australia is currently forced to posture aggressively to manage sudden consumer price acceleration. However, the combination of extreme futures market backwardation and structural global deflation points toward a decisive eventual pivot.

This rapid escalation is forcing policymakers to rapidly reassess global inflation trajectories, as persistent commodity price spikes complicate standard monetary responses.

Investors must interpret upcoming central bank announcements over the next two quarters through this dual macroeconomic lens. Immediate policy statements will likely remain hawkish, reflecting the acute energy squeeze currently straining the domestic economy. Yet the underlying market mechanics suggest this immediate tightening cycle will eventually give way to rate relief once international supply chains normalise.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.