Formulating a strategy for investing during periods of rate hikes requires a precise recalibration following the April 2026 Middle East disruptions. Global equities are absorbing an acute energy shock, and previous assumptions regarding monetary policy are rapidly shifting. Portfolios designed for stable growth must now adapt to a contradictory environment of supply bottlenecks and structural shifts.

The current macroeconomic environment is defined by sudden inflationary pressures intersecting with tight monetary policy. Crude oil surged to between $102.66 and $109.96 per barrel this month following targeted attacks on Gulf energy infrastructure. This sudden supply constriction disrupted the downward trajectory of consumer prices. OECD headline inflation registered at 3.4% in February 2026, forcing reserve authorities to maintain elevated borrowing costs.

Investors must understand the exact posture of major global central banks to position their capital effectively. The 10-year US Treasury yield currently stands at 4.36%, reflecting market expectations that borrowing costs will remain restricted for an extended period.

The current benchmark interest rates across major central banks highlight this coordinated restrictive stance:

US Federal Reserve: Policy rate held in the range of 3.5% to 3.75% as of 29 April 2026. Bank of England: Base rate held at 3.75%. * European Central Bank: Main interest rate stands at 2%.

The Collision of Supply Shocks and Disinflation

Geopolitical events artificially constrict resource supply, creating immediate price spikes that ripple through global supply chains. The closure of the Strait of Hormuz demonstrated how quickly regional conflicts translate into global energy premiums. These sudden shocks force consumer prices upward, regardless of underlying economic health.

However, these inflationary spikes are colliding with powerful structural forces that are suppressing widespread price growth. Advancements in artificial intelligence are driving significant efficiencies across corporate operations, while shifting international trade routes are normalising freight costs. Increased property availability and moderating salary trajectories are further containing service-sector inflation.

Understanding this tension between short-term geopolitical shocks and long-term economic structures prevents panic selling. Investors who recognise these contradictory forces can identify which price movements are temporary reactions and which reflect lasting economic shifts.

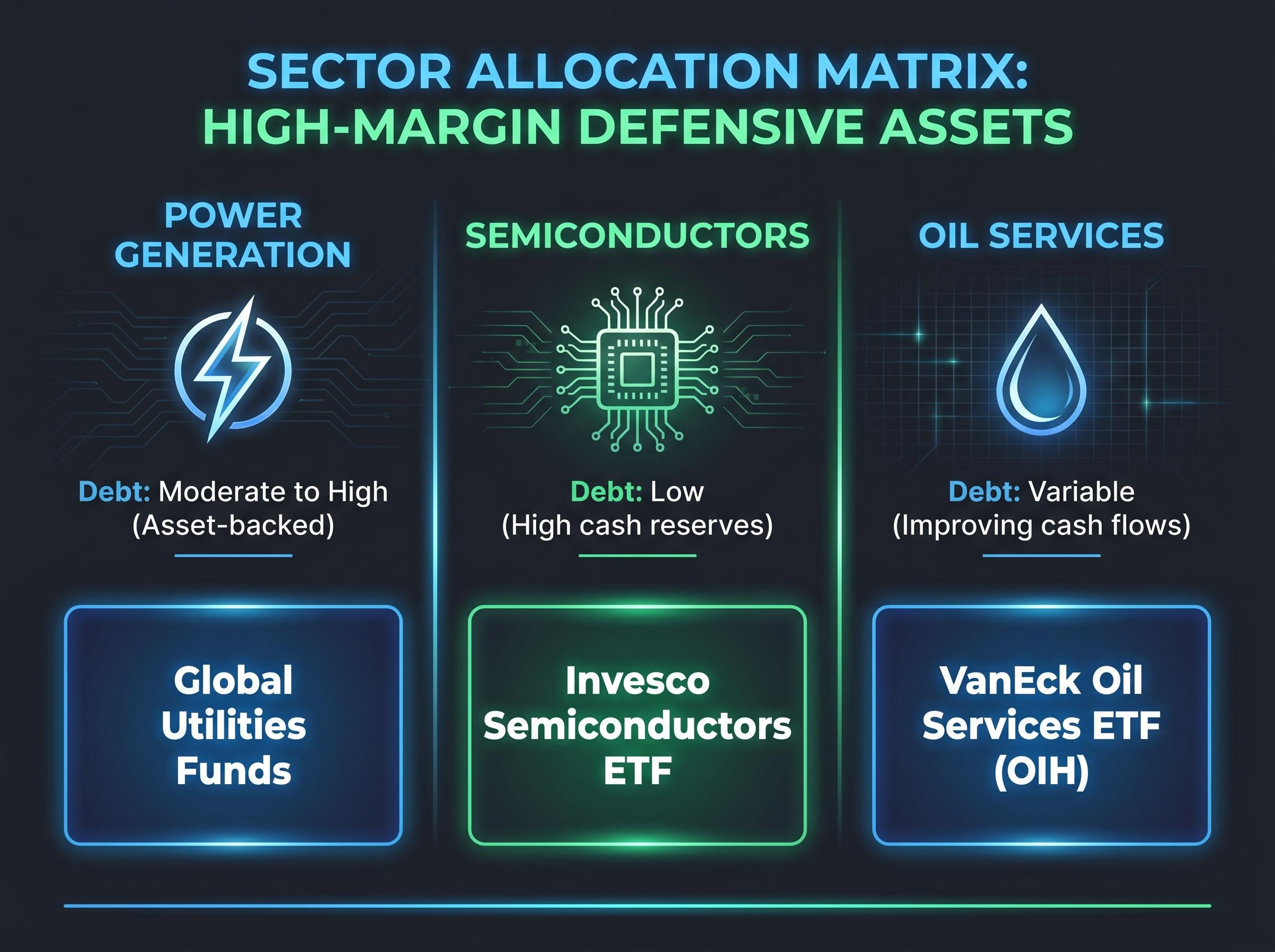

Sector Allocation: Pivoting to High-Margin, Low-Debt Equities

During periods of restricted financial circulation, corporate fundamentals replace speculative growth as the primary driver of equity returns. Capital allocation must shift toward highly profitable enterprises capable of funding their own operations. Companies requiring constant external financing face severe margin compression when borrowing costs remain elevated.

This necessary capital reallocation is increasingly evident as institutional money flows out of heavily indebted firms and moves toward resilient infrastructure and tech sectors that offer a stronger defensive shield against elevated operational costs.

The primary screening criteria for resilient equities in April 2026 centre on pricing power, high operating margins, and low total debt. Pricing power allows a business to pass supply-chain costs directly to consumers without sacrificing market share. High margins absorb unexpected operational expenses, while low debt profiles insulate the balance sheet from refinancing risks in a tight credit market.

Institutions are currently directing capital toward specific global sectors that benefit from geopolitical constraints and long-term technological advancement. Power Generation, Semiconductors, and Oil Services offer distinct advantages in the current macroeconomic climate. Exchange-traded products provide targeted exposure to these advantageous segments without the specific operational risks of individual stock selection.

| Sector Focus | Macroeconomic Catalyst | Typical Debt Profile | Example ETF Vehicle |

|---|---|---|---|

| Power Generation | Escalating energy demands from AI infrastructure expansion | Moderate to High (Asset-backed) | Global Utilities Funds |

| Semiconductors | Continued technological advancement and processing needs | Low (High cash reserves) | Invesco Semiconductors ETF |

| Oil Services | Ongoing Middle East energy disruptions and supply constraints | Variable (Improving cash flows) | VanEck Oil Services ETF (OIH) |

Securing International Diversification

Allocating capital toward internationally diversified equities mitigates the specific regional risks associated with the current energy shock. Different geographic zones absorb inflationary pressures at varying rates based on their domestic energy production and regulatory frameworks.

Global exposure captures economic rebounds regardless of which geographic region recovers first. Portfolios concentrated in a single domestic market remain highly vulnerable to local policy errors or isolated supply chain failures. Broadening geographic exposure ensures capital remains positioned for growth as different central banks adjust their monetary policies at different speeds.

Capital Deployment Frameworks for Volatile Markets

Volatility presents a mechanical opportunity for investors who separate capital deployment from emotional market reactions. Central banks are currently navigating a narrow policy corridor. They must balance the risk of premature easing, which could reignite inflation, against delayed action that might trigger an economic contraction.

Dollar-cost averaging provides a strategic defence against market timing errors in this data-dependent environment. By deploying fixed amounts of capital at regular intervals, investors automatically purchase more shares when valuations drop and fewer when markets peak. Vanguard studies analysing 1-year rolling periods demonstrate that this systematic approach outperforms lump-sum investing during high-volatility environments.

Institutional Vanguard research on cost averaging confirms that spreading capital deployment over time provides mathematical downside protection when equity markets experience severe drawdowns.

Maintaining liquid capital reserves is equally important when reserve authorities are actively managing borrowing costs. Historical case studies show that markets typically stabilise within a half-year to full-year period once acute resource constraints dissipate. Cash buffers allow investors to scale their positions opportunistically when overarching asset valuations drop significantly.

Implement a volatility-adjusted deployment schedule using these specific mechanical steps:

- Calculate total available capital and immediately ring-fence an untouchable liquidity buffer.

- Divide the remaining capital into equal tranches for deployment over a period.

- Execute scheduled purchases automatically on a set date each month, regardless of daily market headlines.

- Accelerate the deployment of a single tranche only if major index valuations drop from recent highs.

This structured approach removes hesitation from the investment process. Knowing how and when to deploy capital protects portfolios from sudden market drawdowns while ensuring participation in eventual recoveries.

How Benchmark Rate Decisions Drain Market Liquidity

Central banks use benchmark borrowing costs as their primary tool to manage runaway consumer prices. When the Federal Reserve or the Bank of England raises their baseline rates, commercial banks immediately increase the cost of mortgages, business loans, and credit lines. This process systematically strips excess liquidity from the financial system, reducing overall consumer demand to meet constrained supply.

Commodity markets often provide the clearest signal of how traders expect these supply bottlenecks to resolve. A backwardation in commodities occurs when near-term futures contracts trade at a premium to longer-dated contracts. This structure indicates that buyers are willing to pay a premium for immediate delivery, signalling that current supply constraints are viewed as acute but ultimately temporary.

Understanding historical rate escalations provides necessary context for current policy decisions. According to historical data, during the early 1980s, aggressive cost escalations successfully reduced US price growth from 14% to 3%, though this action drove unemployment above 10%. Modern central banks are attempting to avoid this level of economic destruction through more calibrated, data-dependent pauses.

Official Federal Reserve historical records detailing the Volcker era confirm that while aggressive monetary tightening successfully curtailed peak inflation levels, the resulting economic contraction pushed jobless rates to extreme highs.

The Taylor Rule and Baseline Borrowing Based on some models, according to the Taylor Rule guideline, reserve authorities must elevate borrowing costs by approximately 1.5% for each 1% that inflation exceeds targeted levels. This mathematical framework explains why benchmark rates remain elevated despite signs of economic cooling.

Forward guidance projections for late 2026 indicate a preference for maintaining current rates or initiating modest cuts toward a neutral 3.25%. Policymakers are demonstrating a willingness to tolerate slightly elevated inflation rather than risk a severe recession through aggressive tightening. This structural shift requires investors to prepare for a prolonged period of moderate borrowing costs rather than a rapid return to zero-interest environments.

Finalising Your Strategic Defense Playbook

The relationship between global interest rates, energy constraints, and portfolio positioning requires immediate defensive action. Global markets will remain highly state-contingent and data-driven throughout the remainder of 2026. Portfolios must be structured to withstand baseline underlying price growth minimums of 2% moving forward.

Investors must immediately avoid highly leveraged enterprises that cannot sustain elevated debt-servicing requirements. Companies relying on constant refinancing will face severe operational restrictions as credit markets remain tight. Profitability and pricing power are the only reliable metrics for equity selection in a capital-constrained environment.

Audit your current holdings to identify and remove excessive debt exposure. Realign your liquidity buffers to ensure sufficient cash reserves are available for opportunistic deployment. Taking these mechanical steps now will protect your capital from further macroeconomic shocks while positioning it for long-term compounding.

Investors exploring how to restructure their defensive holdings will find our dedicated guide to safe haven assets during energy shocks, which explains why traditional hedges like gold are failing due to severe correlation breakdowns and how to establish reliable income streams through global aggregate bond ETFs.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.